Ami plans Preferential issue of equity, just 15 months after raising Rs.200 crores in their IPO.

In the last concall, management said Capex for the current year and the next will be Rs.100 crore each, which will be mostly funded from internal accruals and debt. But the problem with the company is their working capital always looked stretched, with CFO just half of PAT in FY21 and negative in FY22. Working Capital Days have increased continuously for last six years (based on screener data), from 46 days in FY17 to 141 days in FY22.

Such an operating cycle becomes a constraint for growth, as new business opportunities cannot be taken up without raising fresh debt or equity dilution. Raising fresh equity now (presumably from external financial investors) would lead to lowering of promoter stake, which is already quite low at 39 %. Overall, not a great picture unless the company has really hit upon some gold mine in the last few months which justifies such an action as a one-time measure. We need to wait and see.

A lot of things are happening at Ami Organics. Management has promised a lot, and managed to deliver so far. A few more critical executions are expected in the coming year. Let’s see how this pans out but looks quite interesting at this stage. The results were in line and concall was quite bullish. Given below are a few points I managed to capture (though the actual call has a lot more I must say). Usual disclaimers of E & OE apply.:

Some highlights:

- Electrolyte additives which have been approved by six clients and some of them have released plant scale trial orders. Received commercial trial order from more customers.

- We have been able to sign long term exclusive contracts with some of our big customers (I think this is for pharma segment)

- New products in specialty division have high entry barriers.

- Expanded scope of Fermion contract to add more advance intermediates for the same API resulting in multi fold increase in contract value. Increased scope from 1 to 3 products.

- Added ~40 New Customers under API during the year and added ~20 new customers during the year under specialty chemicals

- Developed two new products: One Liquid electrolyte additive to increase electro capacity of Li batteries and one for Solid battery.

- Acquisition of 55% stake in Baba Fine Chemicals (BFC), a leading specialty chemicals company supplying products to the semiconductor industry. BFC has very niche products with high entry barriers. They have strong balance sheet with zero debt.

- We have 50-90% global market share key molecules (Which are these molecules - need to find out)

- Chronic Therapy focus: 91% in AI segment

- When will the Ankleshwar site be ready - Dec 2023. Asset Turnover will be 3X normally, since our products are high value products.

- Chinese chemical industry is back into the game which is hurting many players. But we are not affected.

- Working on plans for expanding capacity in chemicals. 2 more products in this segment

- Full year margins going ahead for FY24:

AI - 23 % target

Spec Chem - improvement of 50 -100 bps target - Spec Chem - 20 molecules developed, LOI signed and started qualifications. Target growth 25-30 % growth this year

- Capex for FY24 - Rs.35 crore maintenance capex + some for solar + some for electrolytes to be announced later

Greenfield capacity capex - Rs.160 - 170 crore

Total capex for the year - Rs.200 to 220 crores - Baba - will grow 4X per year and margins will be around 40 %

- Fermion - deliveries start in Q3 FY24 but in FY25, volumes will be very big as the product is growing 3X. They don’t have capacity.

- Working capital - currently 108 days wc cycle will try to bring it to 100 days.

Trying to get more credit from suppliers

Trying to reduce receivable days by 10 days. - Anti-Coagulant revenues - 12 % of total revenues currently

- Electrolyte - we have 4 products now, 2 in commercialization stage and 2 new. For the first 2, we have orders in hand and customers are outside India.

- This time all growth has come from volume growth whereas pricing is actually under pressure

- Current provisions - when invoices are pending for booking, they go under current provisions.

(Disc: Holding)

Export at 37%; domestic business at 63%

o Export – Exports were lower as for some of the products customer changed the API supplier from overseas

to India

✓ Advance Pharmaceutical Intermediates

o Fermion contract: Validation batches have been sent. We are expecting to start the production from

Q4FY24 onwards.

✓ Specialty Chemicals

o Strong volume traction in Methyl Salicylate and Parabens. Post introduction of flow chemistry process for

Methyl Salicylate, we are now globally competitive.

✓ Electrolyte additives update

o Electrolyte samples approved at plant trial scale by 6 customers.

o We are in advance stages of negotiation of contract with couple of customers.

✓ Capex Update

o Civil work for production and admin block completed. Tank farm and warehouse is more than 60%

completed. Machinery installation is in progress in block-1.

o Started the recruitment process for the new facility. On track to commence the production activity in Q4

FY24.

Concall highlights:

- The Pharmaceutical Intermediates business grew by 5% during Q1 FY24, with slower growth in the export market but robust traction in the domestic market.

- The Specialty Chemical business saw a 25% year-on-year increase in revenue, driven by streamlining operations and upgrading processes.

- The company is close to signing contracts for electrolyte additives with larger-than-anticipated contract sizes.

- The company aims to improve EBITDA margins by 50 to 100 basis points every quarter in the Specialty Chemical business.

- The Fermion contract is a long-term contract with one product, and the company expects sizable orders and revenue from it.

- The company expects the Specialty Chemical business to grow sustainably, with a focus on technology aggregation and cost-effectiveness.

- The company is confident in achieving 20% to 25% growth in revenue for FY24, despite current pricing pressures in the market.

- CAPEX plans include dedicating one block in Ankleshwar to the Fermion contract and exploring opportunities for future products and customers.

- Better pricing in the electrolyte market compared to China is anticipated due to customer preferences and market dynamics.

- The company aims to improve EBITDA margins in the pharmaceutical intermediate business by 50 to 100 basis points compared to the previous year.

- Margins in the electrolyte business are expected to be similar to or better than the current margins.

Is AMI Lifesciences forward Integrated with AMI Organics. ?

I have not read this thread fully , forgive me if it was discussed earlier

Note: Have taken a position recently

AMI Organics Q1 FY 24 concall -

Sales - 142 cr, up 9 pc

EBITDA - 25 cr, up 10 pc

PAT - 16 cr, up 12 pc

Gross margins at 44.8 vs 48.8 pc due change in product mix

Export:Domestic sales @ 37:63

Fermion contract - validation batches sent. Commercial production to begin in Q4

Electrolyte additives samples approved by 06 customers. In advanced stages of contract negotiation with a couple of customers

Revenue split -

Pharma Intermediates:Speciality chems - 84:16

Company produces advanced Pharma intermediates across 17 therapeutic areas

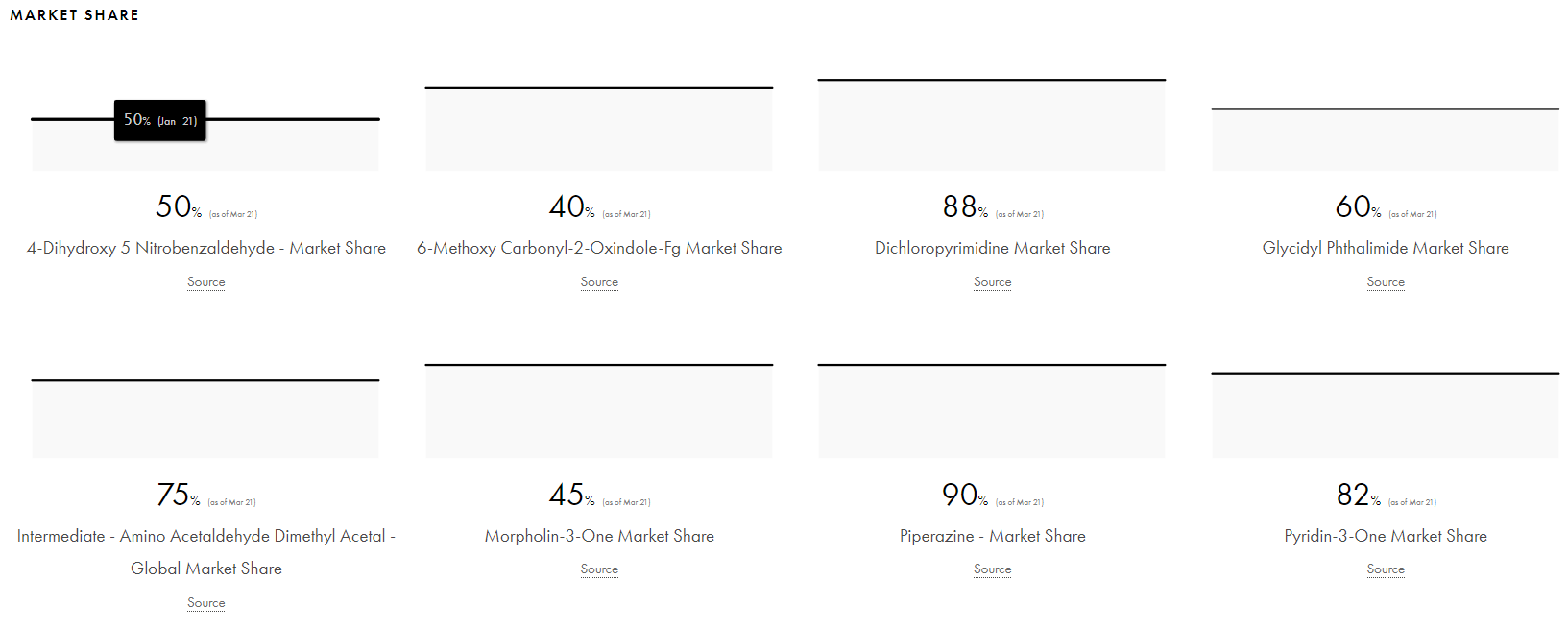

Has developed 185+ products with 90 pc plus products with chronic therapy focus. Majority products backward integrated to basic chemical level. Has 50-90 pc global mkt share in key molecules

Last 4 yrs sales CAGR @ 31 pc in Pharma intermediates

190 cr capex lined up for Pharma intermediates

Expect to continue to grow sales at historical rates

Speciality Chemicals sales up from 7.4 cr to 99 cr in last 4 yrs

Ami has successfully developed a core electrolyte additive for cells used in energy storage

First global company outside China to develop this. Samples approved by 06 customers

Spec Chem business to grow at rates > Pharma intermediates growth rates

Existing Spec Chem business supplies KSMs to Agrochem and fine chemicals industry

In Q1, pharma intermediates, spec Chems grew by 5pc and 25 pc respectively. This when Chinese manufacturers have been dumping all kinds of intermediates, Spec Chems and causing huge pricing pressures

Q1 is historically the weakest Qtr for the company

Did not disclose the capex/preparations required for supply of electrolyte additives citing confidentiality

Fermion orders are for 10 yrs. Supplies to begin in Q4. Full impact to be seen in FY25. Did not disclose the revenue potential from this again citing confidentiality

Fermion contract is for supply of Pharma intermediates for their on patent API

Electrolyte additives business likely to be much bigger than initially anticipated by the company

Q1 numbers do not include the numbers of Baba Finechem (where the company acquired 55 pc stake in Q1)

Company expects the current electrolyte capacity to be sold out in FY 24

Pharma Intermediate EBITDA margins in Q1 were around 20 pc. Should move up for the rest of the year

The margin profile of Electrolyte business to be similar or better than company avg

To understand the true potential of the company, this video link posted below may be really helpful. Also explains why the company trades at such expensive valuations

Disc: holding

Ami Organics FY2023 Annual Report is quite detailed and informative. Some highlights:

- Total revenue for the year increased 18 % from Rs.520 crore to Rs.617 crore. Exports are 59 % of the revenue and grew 21 % for the year.

- Pharma intermediate revenue was Rs.518 crore and Speciality Chemicals revenue was Rs.99 crore.

- Operating profits grew 18 % from Rs.104 crore to Rs.123 crore. OPM stood almost flat at around 20 %. PAT for the year increased from Rs.72 crore to Rs.83 crore

- Cash flows have turned positive as supply chains have returned to normal. CFO for the year was Rs.66 crore which still lags PAT. Capex was Rs.96 crore. Dividend has been retained at Rs.3 per share giving a payout ratio of around 13 %.

- Expenditure on R & D stood at Rs.7.7 crore which was 1.25 % of revenues

- Promoter remuneration was at 1.5 % of sales. The promoters are giving themselves a hike in the forthcoming AGM.

- The total manufacturing capacity stands at 6,060 MTPA and reactor capacity at 436 KL.

- In the current year, 60 new customers were added and 70 new products introduced.

- Company has developed two electrolyte additives for Lithium-Ion batteries and these products are in final stages of vendor qualification.

- Entered into a definitive agreement to sell advance pharma intermediates to Fermion. This is a multi-year, multi-tonne, multi-million Euro agreement for being the exclusive supplier for the product

- Shifted many of the top products with high volumes to flow technology

- Sachin unit is expected to reach its full capacity shortly. During the year, company has acquired an industrial plot admeasuring 8000 sq. metre in Sachin, Surat and has been developed as Warehouse II for catering to the incremental warehousing requirement

- Capex planned at Ankleshwar site is of Rs. 190 crore and it will help in robust growth till 2028 when it will reach its maximum capacity. The Project is on track and is slated to commence the production activity in Q4 FY24

- Announced the acquisition of Baba Fine Chemicals which manufactures super niche chemicals for the semiconductor industry. This acquisition will help foray into a very high entry barrier semiconductor industry with a strong brand name of Baba Fine Chemicals. Baba Fine Chemicals makes very high purity chemicals, Part per trillion kind of purity with its main application in photo resistance chemicals in semiconductor industries

- In the majority of the products, Ami Organics is First-to-Market. Has capability to manufacture a product from stage N-1 to stage N-8 using a single intermediate utilising diverse synthesis technique

- Company’s key products have a global market share of 70 to 80%

- Almost 73% of the raw materials are procured from domestic vendors

- Key export areas - Spain 18 %, Italy 34 %, Finland - 19 %

- Customer concentration - 58% of revenue generated from top 10 customers in FY23. Top clients for Pharma intermediates are Organike, Sun Pharma, Midas Pharma, Cipla, Zydus, Lupin etc. Top clients for speciality chemicals are Sharon Laboratories, Bayer, Himalaya etc.

- API business - 50 to 90 % market share in key molecules, 40 new customers added during the year, 185 customers cumulative, 60 new products launched during the year, 2 manufacturing facilities at Surat & Ankleshwar

- Spec Chem business - 300 customers, 1 manufacturing facility at Jhagadia, 3 new products launched during the year, 20 new customers added and 50 products cumulative. In Jhagadia, 15,830 square metres of land is available for brownfield expansion

- Speciality chemical business is expected to grow faster than the core pharma intermediate business.

- On Ami Onco-Theranostics (JV): The joint venture company along with its co venturer Photolitec LLC has developed several technologies for cancer imaging and therapy and few of the Protocols for cancer treatment have received FDA approval in USA. Phase II clinical trials for Photodynamic Therapy (PDT) for usage in variety of cancers are ongoing. However, commercialisation of joint venture company’s products / technology is awaited upon receipt of necessary regulatory approvals

(Disc.: Holding)

These are the molecules i could find through Tijori exceeds +50% of market share, and the source is DRHP of the company itself.

This seem a legit concern going ahead…, Have you came to any further conclusions on this or insights from the recent AR’s or concalls. Yet to complete few of the recent concall reports would lover to hear your insights if any. thanks.

Discl: Not invested; tracking

Hi, Thank you for the information on key molecules. On the promoter stake, the Chovatia family classified as public hold around 17 % stake and appear to be close to the promoters based on information available in public domain. Thus the effective promoter holding would be much higher if one decides to include them.

Great, thanks @Chandragupta for the update. After going through their concalls and recent disclosures, what i could sense is that the company is trying to project (rather excessively) the untapped opportunity towards ‘semicon’ as well as the multi-milllion, and multiyear contract with the Fermion (Finnish) co.,

Though company mentioned this in multiple times and even a press release two days back (Sept.15th) on the same (seems another/additional contract with Fermion), but there was no Quantifiable numbers/dates available. Dont you feel this is somekind of marketing gimmick and simply to lure the retailors into it…? May be i am totally wrong here or misreading the context, though just a thought…

Discl: Not invested; tracking.

In fact, it’s quite the Opposite. Just see some of the management interviews on business channels where the TV anchors are trying to guess ( informed guesses … mind u ) the kind of numbers that these contracts can bring in

The CEO keeps trying not to confirm to their informed guesses. In one of the interviews, Mr Naresh Patel even goes on to the extent and say - " please let me refrain from spelling out the value of these contracts as I don’t company’s stock to trade at valuations that are astronomical" ( basically words to that effect )

Just my 2 cents

I am invested and biased

I read whole thread, also watched video of promoter with Varinder Bansal.

1 thing is for sure that company might grow easily at 20-25% CAGR for next few years.

-

Who are their competitors? Does any indian chemical company have large presence mainly in pharma with so many molecules? I am asking bcoz to make 20-25% margin who are suppliers of API is not easy & If ami is making it, what’s the status of competitors?

-

Business is growing fast & market is giving higher multiple to stock for it. Any other concern apart from low Promoter holding?

Ami Organics Q2/H1 results highlights -

Q2 results -

Sales - 172 vs 147 cr, up 17 pc

Gross Margins @ 41 vs 48 pc due - steep price erosions in finished products due oversupply from Chinese manufacturers, higher sale of lower margin products. Also, high cost inventory of RM was a head wind

Expecting much better performance in H2 due healthy order book that the company has

EBITDA - 25 vs 28 cr ( margins @ 14 vs 19 pc )

Lower EBITDA margins due - lower Gross margins, higher employee cost due annual increments, hiring for Ankleshwar Unit and ESOPs

Adjusted PAT - 15 vs 19 cr ( without factoring the impairment of JV - Ami Oncotheranostics )

Have signed another contract with Fermion taking the total number of products to be supplied to 3, enhancing revenue visibility for coming years. Commercial production to start from Q4 FY 24 from Ankleshwar facility (validation batches). Have a few more products in pipeline for which manufacturing contracts may materialise for Ami Organics with Fermion and other innovators

One UV Observer - speciality chemical product for paint Industry ( for metallic paints used in Auto Industry ) is scheduled for launch in Q3. The product uses Swiss technology. Validation batches have already been approved

Electrolyte Additives (for energy storage) update - in advanced stages of negotiation of contract with a couple of customers ( first Indian and global company outside China to develop the product ) - product already approved by 6 buyers

Ankleshwar plant to commence commercial production in Q4 ( basically the new 190 cr brownfield capex for advanced intermediates to go live )

Completed acquisition of majority stake in Baba Fine chemicals ( 55 pc stake ) in Q4

Q2 Sales breakup -

Advanced Pharma Intermediates - 134 vs 125 cr

Speciality Chemicals - 38 vs 22 cr (rapid growth due smaller base)

Current manufacturing facilities for advanced Pharma intermediates and speciality chemicals - 03 + 01 R&D facility

59 pc - exports

41 pc - domestic sales

Revenues from top 10 customers @ 58 pc

Cash and cash equivalents @ 104 cr as on 31 Sep

Chinese over supply is not a direct threat to the company. Its just that company’s competitors got cheaper RMs from China and hence the downward pressure on finished products

Company should be back to 48 pc gross margins in next 2 Qtrs

Capex in H1 @ 100 cr. Another 105 cr lined up for H2

Electrolyte manufacturing supply to begin in Q3. Commercial supplies to begin in Q4

Full capacity ramp up of molecules being supplied to Fermion expected to happen in FY 25 - Q3 onwards

Baba Finechem - long term revenue target of 200 cr. Expect exponential ramp up at Baba Finechem from next FY onwards

Aiming to ramp up speciality chemical sales to 2.5 times of current sales in about 2-3 years

Company’s domestic business is mostly spot business. Most of the export business is contract business

Ankleshwar plant has 3 blocks. One of them is Dedicated to Fermion Ltd ( 33 pc of capacity ). This block is fully booked. Other two will be used by the company for business expansion till FY 27

Increase in inventory due build up in anticipation of execution of Fermion contract

Baba Finechem’s H1 sales are 21 cr, PAT is 14 cr !!!

Disc: holding, biased, not SEBI registered

The three Fermion products they are talking about have a sale potential of Rs 500 cr each. Plus the electrolyte additive business has a sales potential of about 800 cr

Inside next 2 yrs, all this will be in the topline

The bottomline can potentially blast from here ![]()

![]()

![]()

![]()

![]()

![]()

Disc: holding, planning to add more

Pls share the source for these potential sales figures. ![]()

I posted a management interview with Omkara Capital on Sep 3 above ( in this thread )

U can just scroll up and watch it from 37 min onwards

Its also freely avlb on Youtube - just type Ami Organics + Dhanda + Omkara capital

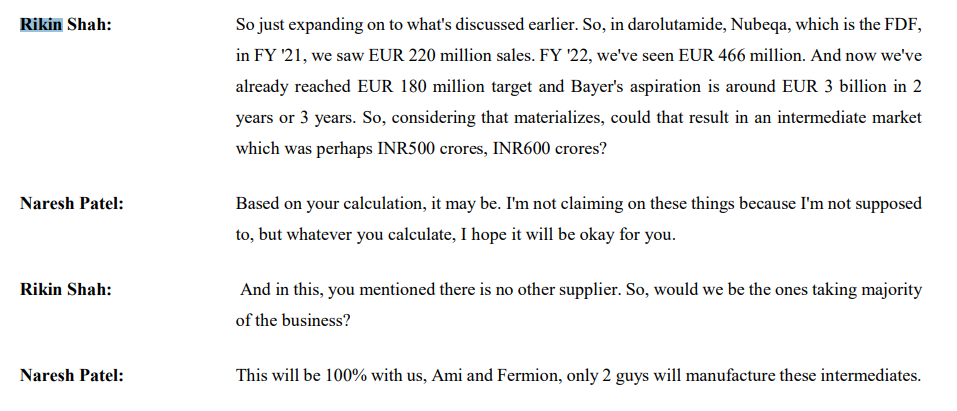

Hi Rikin,

Darolutamide has 7 intermediates. Ami has signed contract for ~3 molecules so far with Fermion (no confirmation on whether all of them are for Darolutamide). Can you share your basis of 500cr-600cr?