@Donald Thanks Donald. This is counter intuitive that small weavers set the price. I spoke to someone in the polyester market he mentioned that reliance and garden bareily are price setters and the more fragments market of weavers don’t have any bargaining power. His view was it shouldn’t be any different in the cotton yarn market. But it would be good to double check. In terms of economics my understanding is also pretty much the same. If you try to calculate incremental RoCE then it’s pretty average atleast for a lower count player…I have some back of the envelope calculations for Nitin it comes to be around 10-12%. For the spinning industry last two years the prices of yarn were firm and the external demand due to China was very good this numbers are brilliant plus the exchange benefits

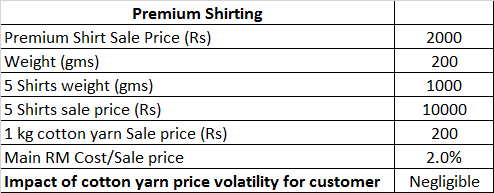

Now let’s examine things from the perspective of the end customer - the Premium Shirting buyer ![]()

What are your interpretations of this data point?

a) customers will tend to stick to preferred suppliers?? and, and

b)

c)

@rohitbalakrish_

Polyster market dynamics are totally opposite because of the giant.

Cotton yarn market dynamics - No yarn player is a giant even a Vardhman (not even $1Bn sale) is pretty miniscule compared to the total market. When they buy cotton for example some impact is there, but no earth-shaking

that’s what I did (edited the file) … and I fully agree that same data shouldn’t be put again by another poster without checking if it is already there

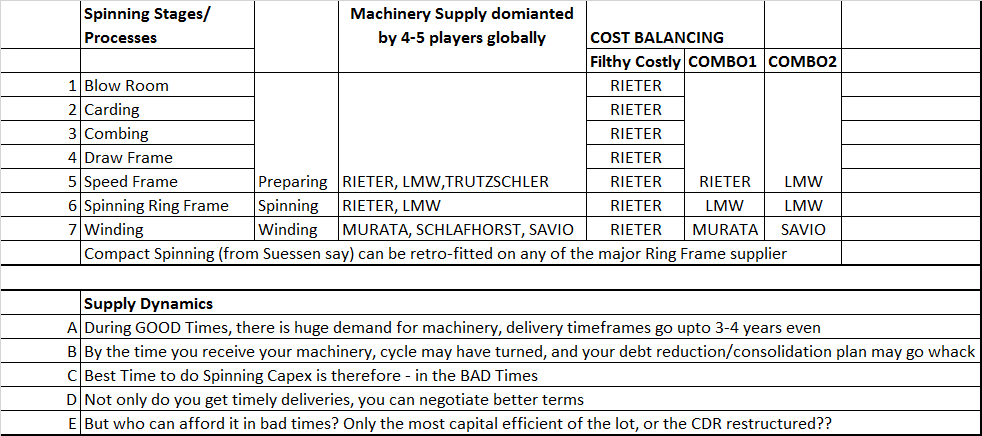

Moving on to examining the Technology supply dynamics

Disc: First-cut understanding from discussions with an ex-spinner, so supplier data may be a bit dated. Please try and confirm the players/dynamics independently

We can refine all above with 2nd/3rd level talks and fill in gaps, etc

So far we have tried to map for everyone’s benefit, following :

So far we have tried to map for everyone’s benefit, following :

- Market dynamics

- Technology Supply dynamics

- Production/Efficiency dynamics

Missing Maps - Higher-Count Mills

- Competitive Intensity

the most important pieces in the information puzzle still going missing.

the most important pieces in the information puzzle still going missing.

Hoping someone will get inspired now take this forward

Why are we taking so much trouble, if someone cant resist asking- Hey, Why is Donald spending so much time over this?

a) We thought documenting this progressively like above, will give a peek into the VP PROCESS - that empowers us with a rich background to carry out smoothly flowing conversation flow with industry experts/managements/any stakeholders. We are usually prepared with 2nd/3rd level data-points.

b) By the time we complete an exercise like this, most times we have our own hypothesis quite well-formed - which only means we can EXTRACT the most out of the valuable time that any domain-expert or say Management is kind enough to give us.

c) We earn the respect of these people - that we are not wasting their time - its okay to ask open-ended questions - but usually such conversations do not last beyond an hour or so. If it does, then the expert/professional is not doing his work

d) as you may be aware VP Management Q&A usually lasts for over 2.5 -3 hours the first time. A more complex industry like say Avanti Feeds took 4.5 hours to cover everything - almost always if we have done diligence to the VP process, we get more than adequate time

Next value-addition is to document/illustrate the VP Process with a live example

Ambika Cotton is as good as any to get started on nailing down the VP-Process.

Attached is the Excel - with all these Maps, plus Notes from Ambika ARs ![]()

Ambika-Notes.xlsx (41.3 KB)

Hoping once we are through with the Ambika exercise, we can enhance this excel and proudly unveil the VP Process document - for use by every passionate learner.

Despite all the acclaim, we have been accused of spoon-feeding the community, not really doing a value-addition job. The main objection being, where is your process document - and I would be like stumped ![]()

This is an effort in that direction. We hope to see many hands up to help us create that document together! We hope to have the next meeting with the industry guru - where we can get a process-pat on the back. And ask him, what next? where d we go from here?

Higher-Count Mills Map???

Whom can I count on - I am really stubbornly stuck on not doing that exercise myself. Its not difficult if you go after it, the right way. don’t try using Mill websites - that’s very inefficient -it will take you ages. Rather 30 mins spent with the right industry expert will fill you in on the real issues - that otherwise may take you a month or two, and you still wont have the hang of the real questions to ask.

At VP we pride ourselves on a very hard work ethos, but we must also work SMART!

Cheers

@Donald thanks a lot for providing us with a thorough coverage…this is extremely helpful…I spoke to a credit analyst who has been covering the textile spinning sector for over 4 years…he provided me the following insights that are in line with your findings (some info may be repetitive from earlier posts, but have provided them for comparison).

Overall Industry

- Cyclical business, where in bad years the industry operating margin was as low as 5%

- Price sensitive and commoditized buyers of yarn - even 1 or 2 Rupee lower price you could sell your entire stock…so price setting is done by traders/ small buyers

- Players are always over expanding in good times, taking on too much debt, and then cycle turns and then many go into CDR or out of business…

- TUFS scheme has been reduced from 5% interest subsidy to 2% which is sponsored by central govt (states like Rajasthan, Maharashtra, Gujarat and MP have come out with their own incentives giving 6-7% subsidy in addition)…players have already started adding capacity, but actual cash hasnt come as this is a recent policy by states.

- North players are focused on all types of yarn - they would do lower count, finer count and also manmade (polyester) etc…they have diversified operations to balance against cotton cycles

- South players have focused on finer count, and this is where we will find the top 10 high count players

- North average would be 26 - 32s, whereas south would be >40s

- In FY14, operating margin was 13% on an average, and depending on leverage, net profit margins would be in the range of 3-4%

What is borderline for finer count - 40s

What is minimum economy of scale needed?

- 25000 spindles is minimum, however recently some of these have also started going out of business

- ~40,000 - 50,000 spindles as per him would be the new minimum scale needed to sustain going forward

What is capex per spindle?

- Rs 40,000 per spindle

- So for 25,000 spindles, 100 crore would be required

- Generally financed through 80% debt and 20% equity (high incentive under TUFS)

For finer counts – can blend use 20% ELS and 80% normal staple or all ELS?

- For finer counts almost all would be ELS, atleast more than 50%

What is the typical product mix for specialty yarn guys like Ambika? How much of finer counts and how much of lower counts?

- In the North - most players would have only 20 - 25% finer count, as they use polyester also (Nahar, Vardhman would have very high number of spindles, but <20% would be finer count)

- North average is 26 - 32s count

- Southern players - 75% would be doing finer count of (>40s average)

Why aren’t many players moving towards specialty yarn if it has higher margins? What about the larger players?

- Lower count is very easy to sell (very price sensitive - can sell all the stock for 1 or 2 Rs lower than market price)

- Higher count market is small, and companies have established suppliers such as Ambika which has a loyal customer list

- Higher count segment not growing very rapidly, so larger players have diversified into various yarn

- Every large player is present in higher count - but would have ~20 - 25% higher count capacity

- Even if players have higher count capacity, they could be doing lower count yarn

- Lower count players have higher sales, and lower margins, and higher count players would have lower sales but higher margins.

Competitive landscape

- Will come back to me with names in a couple of days

- Said very tough to understand from company websites whether the Company is in higher count or not, and what the average count would be…its a company specific metric…

- Mostly should be South based players (or Gujarat, Maharashtra)

- Shamugavel, Rajapalayam Mills, Vardhman, Govindaraja Mills, KPR Mills, Winsome Textiles, Bannari Amman (possible), Ramco, Thiagrajar, Premier Textiles are players where he said could potentially have higher count, but will confirm in a couple of days

- Sportking does not do higher count - its average is 32s…75% is high value added product…uses polyester cotton…hadnt heard of LS Mills…

- Maharaja Shree Umaid, Nahar Spinning, Trident, Alok, SEL, Banswara Syntex, Deepak Spinners are certainly not in higher count

- Indo Count Industries (1500 crore player) seems to be doing well, and worth looking into

I will update once I do hear back from him on the players.

Cheers

Disc: starter position to track

@Naman

Excellent work and great value-added inputs. Thank you for reaching out to friends familiar with the domain. They are the ones who can help us get to the bottom quickly.

You have asked most questions that need to be asked

Add 1 more crucial question/ sub-questions

- if GPSS of 80s count is only 34, then you will only generate some ~50 Cr Sales (@400/kg) on an investment of 100 Cr (25000 spindles). Asset Turns will be 0.5x

So how can someone run a predominantly higher count operation (upwards of 60s and 80s) and grow Topline. Bottomline would be better with higher realisation and lower RM/Sales probably - How is it viable to do 100 count and 140 count in any significant share of Product Mix. Product mix will have to be tilted to lower counts.

- So essentially can someone do only 80s count and higher and be viable? How

Look forward to some of the Top names in higher counts

Also we have no idea of the size of the higher count world market and international competition there for Ambika. Can he help get some leads there?

Who are the major buyers from East & SE Asia which is the fastest growing geographic sector for Ambika and probably other higher count exporters from India?

Hong Kong listed Texhong textile group ( mkt cap USD 1bn) is a major high quality yarn producer with around 1.5 m spindles. It also produces fabrics and spandex yarn. I have not come across any focused listed yarn producer in China, they are all vertically integrated into fabrics and some into garments.

The outlook for yarn players in general is quite dismal over the medium term as China releases its cotton stockpile at low prices domestically leading to lower yarn prices globally.

One also needs to consider the recent exodus of Chinese yarn players to Vietnam where they are able to import high quality cotton from anywhere to produce yarn similar to what Ambika offers. Texhong itself has 750k spindles in Vietnam.

@Donald Im willing to the Higher-Count Mill Map… Im from the Textile Industry, that is a advantage but also a very big disadvantage… a few factors that I was thinking to be normal/general thinking seems to be peculiar nature to textiles/yarn industry… so it would be great if you could give me a set of questions that I need to get answers… will try improvise on that and get a complete picture…

Team VP,

Just to carry discussion futher, find enclosed NSE Adjusted price (which I have sourced from Quant Partners, again shared by one of VP member) for all textile companies. In fact, cotton yarn spinning companies all time high was during 1991-95 period, when Manmohan Singh Liberalised textile sector. The price of GTN Industry, Vardhaman Textile, Suryavanshi Spinning (I purchased Suryavanshi spinning at 87 on Jan 27 1995 to sold at Rs 7 in December 27 2011, with current price of Rs 10. ). Even adjusting for management, very few companies have able to give more than 10%+ growth. The data provided here does not seggregated in Cotton spinning, Blended spinning, Cotton Fabric, Denim, Banded Apparel, Apparel exports. However, please go through data and you would understand the point I am making.

Having said that, if there is some secular shift in trend which would drive the sector, then one must notice that take a call. However, in my understanding, same would be true for most of chemical, steel, paper, sugar, fertiliser sector. Only way to make money is to enter at lower point and more importantly exit at right price. You may afford miss Balkrisha, Astral, Mayur as price would catch up in couple of quarter to year. But if you missed in spinning, you might have to wait for a decade !!!

Textile Sector Adjusted Market price of 21 years.xlsx (30.5 KB)

Thank you Donald! was wondering precisely the same. As a new comer to this forum, following a research process is exciting. My biggest question was when we figure out that the industry is highly competitive with low entry barriers, why do we put up so much time understanding the industry just for the sake of it?

If we see a shining knight in a very competitive industry, who has a good track record over last 10 years- and has clearly bucked the cyclical trend - it attracts our attention- obviously doing something special.

One may not have totally impregnable barriers, but if you examine the data - there is enough evidence of quality - that there is substance. The debt free status, margins above 20% for 10 years, major improvements in debtors and inventory. Business is becoming more efficient. From 50% import RM usual levels, last 2 years there is a drastic rise to 80%. Company moving on to a higher realisation game? With the next investment in Capex it will have to take on debt, which will boost RoE further.

These are all interesting patterns to observe. May be his competitive advantage is getting far stronger? Maybe nobody cam dislodge him? Does he have a very long runway? His business sure has predictability. Will it be sustainable??

The VP Process about doing all this work is to establish only 1 thing - Demolish the investment hypothesis, or come back fully convinced. All VP Portfolio success stories have come from that hard detailed work.

VP Portfolio is a concentrated portfolio. You can’t bet strongly if you don’t have high conviction. For us high conviction comes only from establishing what looks extra special as indeed so - by doing the solid grounds-up work.

Besides, as Ayush is fond of saying - this is the only way to learn, grounds up. We will learn what is to be valued highly, or the practicalities of what is Ignorable and what is not. By working this hard - another interesting thing happens - you start knowing more than most people on the business and industry dynamics. People start seeking you out to learn more on your insights or special take on the business/industry - in turn the same 10 people that might have called you will make you more knowledgeable collectively.

If you do the initial hard work extremely well like we try to do at VP, then remaining on top of your business gets extremely easy. You don’t get shaken by small developments because of knowing what matters, what is ignorable and what is not. Folks (those who get shaken) make sure you remain updated of every event, newsflow or trigger - you don’t have to gather intelligence - it comes to you

Another spin-off of the 1-time hard work. You may have missed the bus this time, but your decision-making becomes very fast when you know all about that business. The next time Mr Market gives the opportunity 1 or 2 years down the line (as it always does), you will be the quickest off the block - as getting updated will take no time!

Over 5 years the number of businesses that you understand well can become a very valuable chest you carry around - provided you do your job - honestly with proper due-diligence, follow the process.

Folks,

I was reading through Sintex’ results today. Looks like they have added capacities worth 3.2 lakh spindles in the last 1 year. (with a target of adding 10 lakh spindles in the next 2 years.) They are venturing into production of finer count yarns(I m still trying to understand the break-up of how much of this investment is exactly getting into finer count yarns. But going by what the CEO says, it is mostly into finer count yarns.). All their machines are state-of-the art, fully automated(very similar to Ambika’s).

The below url has more details on this:

http://www.indiantextilemagazine.in/cover-story/sintex-adopts-no-touch-yarn-policy-for-new-spindles-plant/

Am not sure how much the above information would be helpful.

- On the question of Global market potential for finer count yarns , I came across(googled) a research report which has some information on Chinese market. Please refer to the url (2010 report. Bit old, but one can assume a growth rate of 5% to the Market potential #).

http://www.hkexnews.hk/listedco/listconews/sehk/2012/0629/01616_1381209/E114.pdf

Am trying to dig-up more on this. Will post if I get something useful.

Thanks,

Ravi S

Disc - Invested <2% of p/f only for tracking purposes.

Building on the above, I have compiled the following data:

Based on the above, efficiency per employee is much higher in Ambika compared to others.

Few Questions:

-

Why is the tax rate significantly lower in the company even though there have been no losses over the last decade (MAT credit is eligible for maximum 8 years)?

-

They were net importers in 2014. Can falling rupee be a significant risk? They have the unhedged foreign currency liabilities of over 60 crores.

Hi BeingGraham,

The tax rate is lower as they have substantial investments in wind mills and hence must be getting the 80IA tax benefits.

The co’s export and import value is sort of equal now…so should be neutral to currency changes to a great extent.

Ayush

Excellent discussion on Ambika

After reading what donald has written I realised what I have done is quite basic work. Even then I am sharing link to my work so that a beginner can come to speed quickly

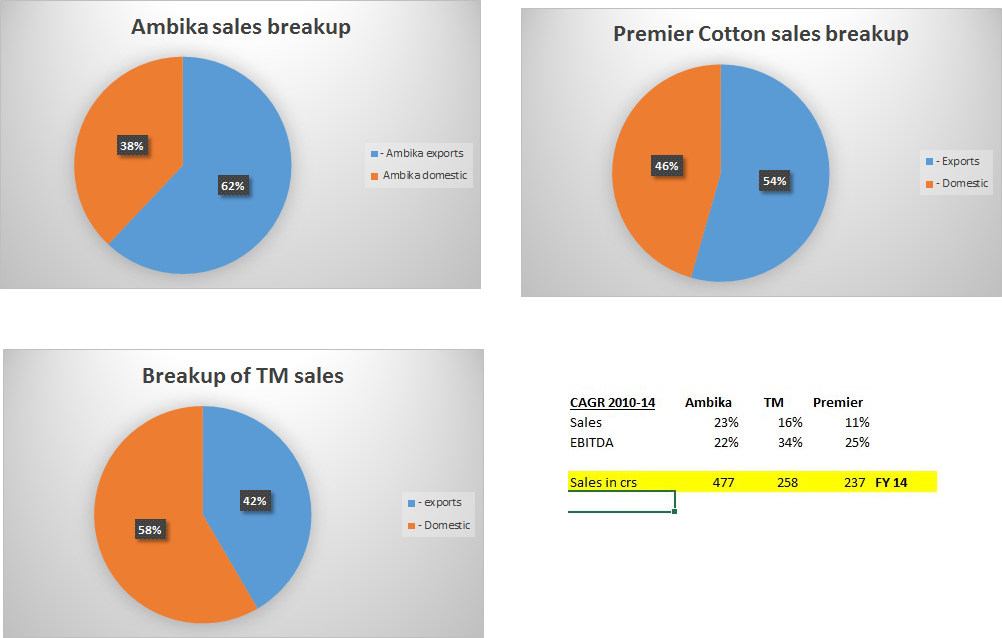

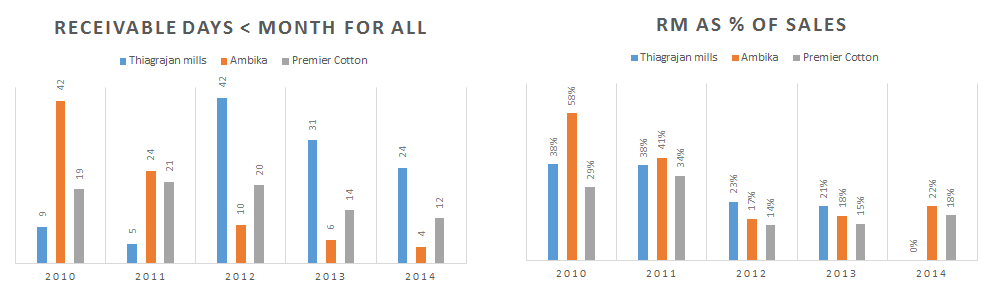

Quite late to post, but might still be helpful. Comparison between Ambika, Thiagaraja mills, Premier mills. Puzzle is why Premier EBITDA margins so high…

Dhiraj,…good work. Shocking, as I go through the data. No wonder, Textiles, as a sector gets such low valuations. Except cos like Welspun, not many seem to have distinguished themselves. Kitex ofcourse is a phenomenal story but even there, outsized returns from here only a pipedream

(IMHO)

PS - Not a reco. pl do your own research