Donald and other friends;

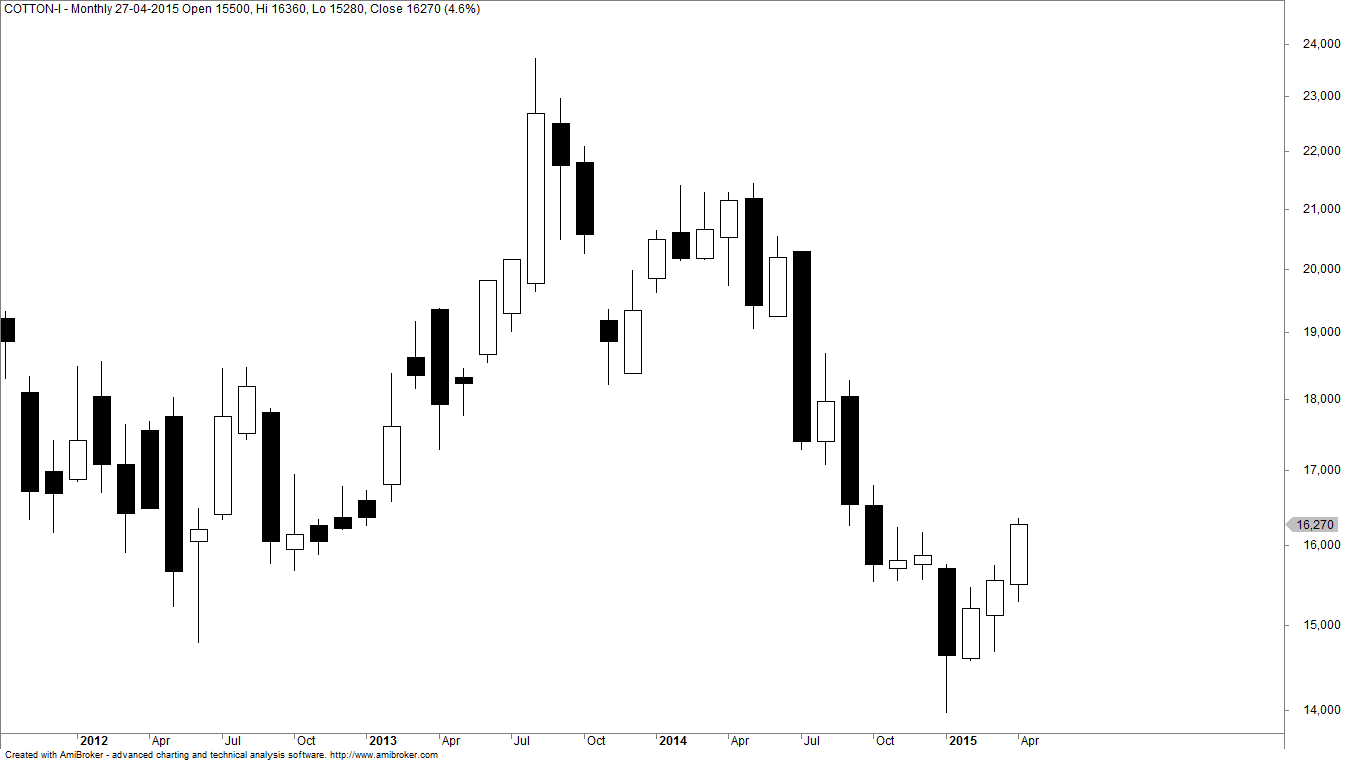

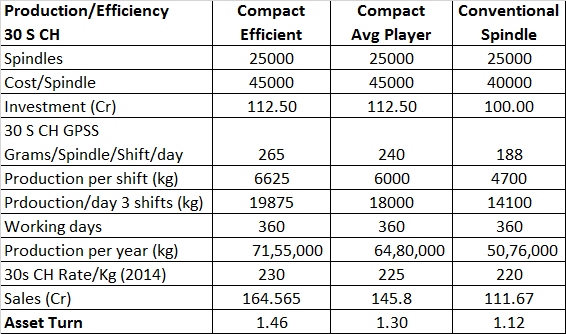

At the current capacity, the company would have limited scope for sales growth. If I look at sales and profit are moving mainly by capacity expansion. Also, I would also suggest to compare last 4-5 years margins. Geneal EBIDTA margin are around 14-16%. With Per spindle capacity of 50,000; production per spindle at around 150 kg per annum (150 gms/spindle/shift with 1000 operational shift) and price of around Rs 300/kg for Ambika, expected Realisation for spindle of Rs 45,000. While EBITDA has been around 20%, we shall get EBIDTA per spindle of Rs 9,000. Please note that in last three years, Indian cotton yarn industry has been major beneficiary of good domestic cotton crop. While Ambika is dependent on imported cotton, still globally also cotton price are expected to decline as ICAC.

In long term, with Rs 50,000 capex, Rs 40,000 sales, Rs 8,000 EBITDA, EBIT, Rs 7,000, ROCE, ~15%.

Hence, we need to consider cyclical nature of industry which has very high volatile raw material. The last 4 years were driven by lower cotton price. Considering the price record, Ambika shall be able to maintain the margin, the scope for margin expansion is limited.

I would need to understand how growth would be achive without capacity expansion and what would be impact of declining cotton price globally as forecasted by ICAC.

I am enclosing excel file in which I have compared FY2006-2009 various parameter for large spinning mills and taken average for all major Indian cotton yarn price. When cycle is against the sector, they do incur loss as we can in these data. The second file has Cotlook Index by which global cotton (mid staple) is measured. It is in cents per pound. I have converted at kg with Rs 63 per kg.

Hope this would assist you to assess the company. Since the free cashflow and margin are not consistent and also average ROCE is around 14-15%, I normally find difficult sector for wealth creation. Having said that, Ambika has show superior performance with virtually no working capital. That is really outstanding. So wanted to confirm that Ambika is like Page and not Maxwell/Rupa/Loveable before deciding to invest.

The worst thing which new annual reports has been they have done away with quantitative information which was available till 2009. The data for all players was available in annual report and I had compiled from same.

CY Industry Data FY2006 to FY2009.xlsx (39.9 KB) ICAC May 2015 Press release.pdf (79.8 KB)

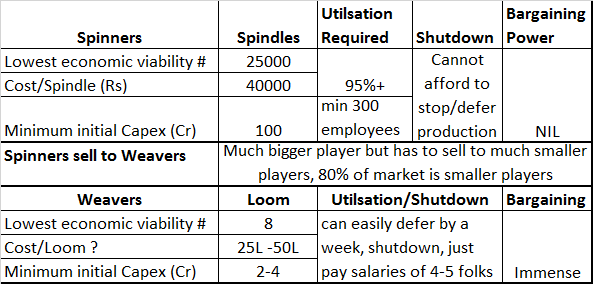

Ambika caters to premium shirting fabric / t-shirt segment which are mostly woven. Better quality cotton, entrenched current position, management focus towards this objective gives them an edge in holding on to that premium segment. Nitin mostly caters to comparatively better quality hosiery segment where cotton quality is important but available in India and can be made by relatively lower quality cotton.

Ambika caters to premium shirting fabric / t-shirt segment which are mostly woven. Better quality cotton, entrenched current position, management focus towards this objective gives them an edge in holding on to that premium segment. Nitin mostly caters to comparatively better quality hosiery segment where cotton quality is important but available in India and can be made by relatively lower quality cotton.