See recent AGM video on YouTube. The Chairman opined that the slump was almost over and Demand should pick up after December 2023.

1 Like

Last three Quarters `Preformatted the EBIDTA for Ambika is down vs their historic 20 %. Working capital interest cost has increased 3 times vs last Dec though they have so much money in FDs. Promoters are not finding use of the cash, they are not expanding or buying. It is good though 1large portion of electricity is now with the wind.

Hope this compression in EBIDTA is due to the high-cost inventory of cotton that they carry not because of loss of margins for good.

Disc: Invested since 2017 here

1 Like

As per the last BalanceSheet published in Sept23, Cash Equivalent was 234Cr; whereas short and long term borrowings were ‘Zero’. Am not able to understand what is accounting for this Interest cost?

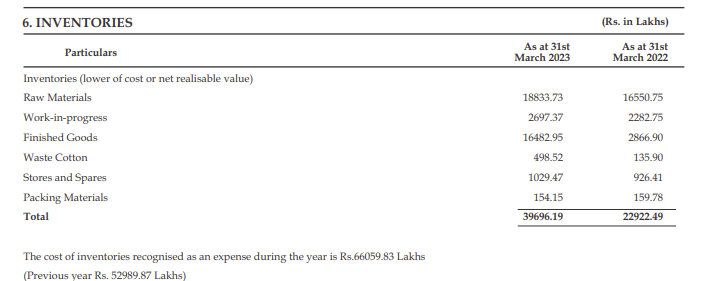

The inventories at 496Cr!! Almost 96Cr rise in last 3 quarters!!

More than 2 quarters of sales is tied up in inventory…

If its raw cotton inventory, why do they speculate and buy so much in advance… Does it show that they are not able to pass down the increased raw material cost and hence consider hoarding cheap raw material as their real moat…

What if the cycle does not turn soon and they are forced to liquidate at the low point of the cycle after holding for long? Why cant they hedge through commodity exchanges. Currently they are not doing the same, check point 6 below from their last annual report.

I was hoping that finished goods would be a small miniscule portion of this inventory, since that would loose value as the fashion fades in future. however the below disclosures in their last annual report (Mar23 data) are a little worrying. Raw Material had increased slightly from 165Cr to 188Cr, however Finished Goods had increased from less than 29Cr to 165Cr. (as per last annual report). Only hope can be that the FG is majorly in yarm form rather than knitted as mentioned by @sunilkumarca3101 above

But pls note that Knitted Fabrics is more than 22% of Revenue while Yarn is 64%; so inventory can be in similar ratio…

Disclosure: Holding since i consider it cheap, however now worried that it maybe cheap given this reason of growing inventory over multiple quarters…

3 Likes

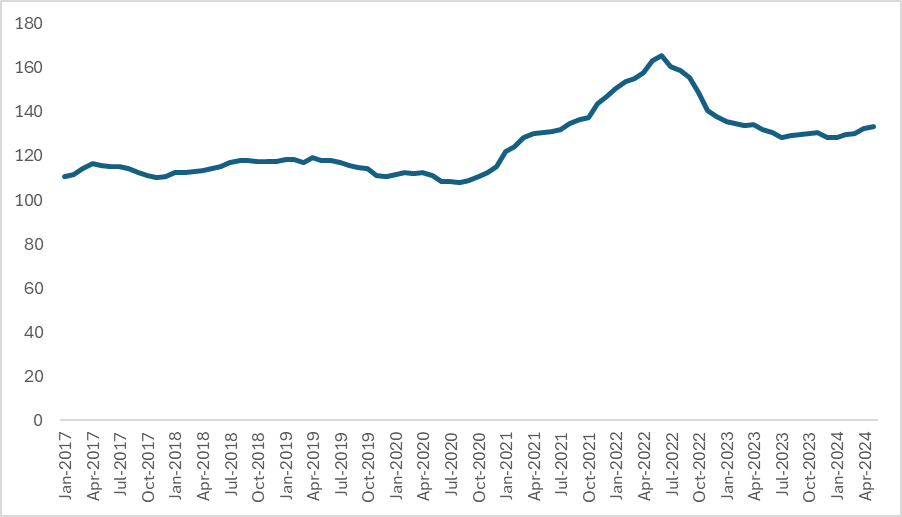

The observed correlation, as illustrated in the diagram provided by @jose, supports the above notion that an increase in cotton prices translates to commensurate gains in market returns.

2 Likes

I would say that the understanding of cotton cycle would be their moat instead of hoarding cotton. And share of Knitted fabrics could be less than the ratio of turnover for last year. Knitted fabrics would be mostly manufactured on order due to the very same reason you mentioned. I think it is to optimise the various costs that the company is converting at a faster pace than they are selling. The company is seen becoming stronger after each cycle.

Hi @Jose, Maybe understanding the cotton cycle is their real moat; but then instead of tying up cash in inventory what stops them from hedging Cotton at Agri exchanges like MCX

Inventories as you very well explained in your previous post have actually seen a steeper rise; As per Dec Qtr results, crossing 60% of annual sales for the first time in the last decade. Proportion of FG inventories have risen which is more worrying;

Wish if we had more details around FG inventory type, Yarn Vs Knitted Fabric…

Why do you think they are becoming stronger in each cycle?

1 Like

It is not about hedging cotton. It is a mindset. They operate on pull model, do not dilute their brand and sit on Inventory during downtimes. They sell only on certain profitability even if it comes at the cost of holding inventory.

4 Likes

This is one thing I like about this company. They are ethical and whatever may be the situation they won’t sell at lower margins/profitability. But I wonder how the CS and CFO are working with such low compensation. This is a company that when the cycle turns will give handsome profits and the rest of the time will just do okay. This is not the one that will compound profits at 15-16% and it will always give lumpy returns. Risks are very limited in this as well as rewards IMHO.

Disc- Holding for the last 7 years.

8 Likes

Govt have removed duty on extra staple cotton.It will benifit Ambika Cotton

3 Likes

Absolutely, from 11% import duty to Nill. Should help the bottom line of Ambika

India uses 20Lakh bales of extra long staple (ELS) cotton while local manufacturing is only 5L bales. Rest are imported.

3 Likes

The reduce in Import duty would definitely be an improvement going forward , however considering they have a huge stock pile of old inventory on which they have already paid the duty this may be a bit counterintuitive. Their competitors will be producing with the lower cost raw material.

9 Likes

As per Annual Report FY23, Apart from Mr Chandran, nobody in the company is paid compesation more than 6 LPA.

How can one hire talant (CFO, COO etc) at this cost? Is this sort of compensation a norm in Cotton Yarn Industry?

1 Like

For the location (Coimbatore), I’d say that’s fair.

The Average Compensations for CFOs in Coimbatore is actually much lesser: https://www.glassdoor.co.in/Salaries/coimbatore-cfo-salary-SRCH_IL.0,10_IC2836047_KO11,14.htm

This glassdoor information is not reliable. I dont think the location matters for a designation of CFO, COO, etc., and yet Coimbatore is a big city and expensive.They must be paid 20 LPA. There must be some other benefits which we are unable to see.

1 Like

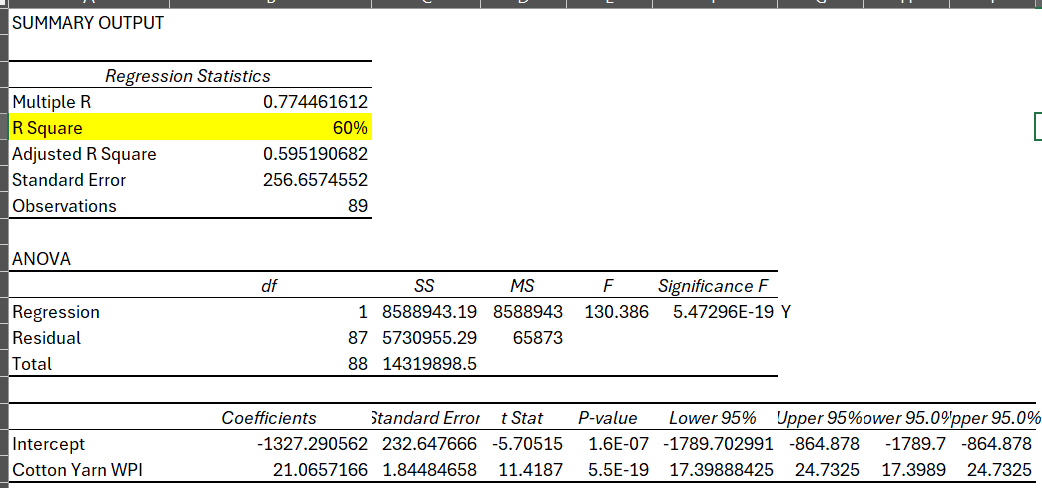

I did a linear regression of Cotton Yarn WPI monthly price data vis-a-vis monthly stock price of major listed cotton yarn players - It looks like Ambika’s stock price is the one that most closely follows the cotton yarn price

| Company | CMP correlation with Cotton Yarn Price |

|---|---|

| AMBIKA | 60% |

| VART | 49% |

| Rajapalayam | 1% |

| NITIN | 47% |

Now that we’ve established that cotton yarn price increase will also lead to increase in Ambika’s stock price, how do we establish that cotton yarn prices are rebounding back to previous peak?

I looked at the WPI data and it looks like 2022 was a major exception in terms of cotton yarn price increase. No other year has the cotton yarn prices have increased so much.

Honestly, cotton yarn prices had remained static for 8 years prior to 2020 irrespective of inflation.

| Calendar Year | Index |

|---|---|

| 2023 | 131.4 |

| 2022 | 154 |

| 2021 | 133.2 |

| 2020 | 111 |

| 2019 | 116.1 |

| 2018 | 115.5 |

| 2017 | 113.2 |

| 2016 | 108.4 |

| 2015 | 107.7 |

| 2014 | 117.5 |

| 2013 | 113.7 |

If anyone with experience in this sector could chime in? @sunilkumarca3101

7 Likes

Cotton Prices rose in 2022 because of higher demand for knits due to WFH around COVID and major upgrades of home textiles by US buyers. Post that, the textile mix should again go back to formal clothes / outer clothes - which are cotton, cotton mix or pure synthetic…

In short - the 2022 trend is not going to repeat itself. We may see cotton price increase once the demand from US picks up since that is where most of our garments, home textiles and knitwear is exported to.

Same holds for domestic demand. Barring Dollar, no other innerwear co or fashion clothing co is reporting double digit volume growth or 20%+ rev growth yet.

4 Likes

Hi- None can predict cotton price as it is a global commodity which depends on many factors out of anyone’s control like rainfall, acreage, availability of quality seeds etc… I found it very uncomfortable Ambika management blocking so much money on inventory… Cotton prices rose after covid for which Ambika got benefit and I am reasonably sure that Ambika mngt also didn’t predict it ( If they have predicted cotton price rise, they would have stocked up taking loans as their balance sheet is debt free) . So when they couldn’t predict cotton price movement in the past, I should reasonably assume that Ambika may not successfully predict even now and hence they may lose if cotton price falls…If they are lucky enough, cotton price rises and they pocket the benefit of rise on the cotton stock…… And when Ambika mngt with decades of experience couldn’t predict cotton prices, I don’t think outsiders like us can predict its movements with certainty……current facts are cotton seed producers like kaveri mentioned that seed stocks are low… but at the same time, cotton yarn/ fabric exports are under severe pressure as consumers in western markets are reeling under financial stress owing to high inflation etc and hence their discretionary spends are affected… so quite difficult to make a prediction with certainity reg cotton price…

9 Likes

Just like any agri commodity cotton prices are generally very volatile. During peak arrival season prices and availability of right kind of cotton are favorable. Only cash rich mills can stock up full year requirement and this is a very standard practice. Also they get better price. So we have no choice but to accept large cotton inventory if we want to be Ambika share holder.

6 Likes

when we see the trend of cotton inventory ( value) to turn over, it is around 30% ( max 40%) range over reasonably long period, it is almost 64% now. So it is reasonably clear that they are speculating with cotton prices. Moreover , In one AGM, Mr.Chandran himself spoke that he favours converting cash into cotton inventory rather than holding it in bank FDS…Plus when you see past annual reports of Ambika, there are good number on instances in which they have gains on inventory sales, which show that they have speculated earlier …Holding stocks for production is fine , but holding stocks for speculation is a double edged sword…If lucky, it shall benefit, otherwise , it may backfire…Lets hope Mr.Chandran and Ambika share holders are lucky …

7 Likes

If he is so keen to talk to the investors then why not doing concall?