Even i got the same doubt, but i feel that he is talking about the customers and their retailers.

because of the higher interest rate they may postpone the buying.

This is what i understand, any one can please comment and explain

Even i got the same doubt, but i feel that he is talking about the customers and their retailers.

because of the higher interest rate they may postpone the buying.

This is what i understand, any one can please comment and explain

Q2FY24 results are out

Company added 100 Cr. in inventory which is now at ~498 Cr.

Cash equivalents ~ Rs.233 Cr.

Mcap ~ 880 Cr.

Management’s reply in AGM when asked about high inventory levels.

(https://youtu.be/ZrKdOYeM1D8?t=2539)

The above inventory levels suggest management is walking the talk and is bullish in near future.

Gokaldas exports quartely presentation is a good read to understand global demand scenario for apparels. (https://www.gokaldasexports.com/wp-content/uploads/2023/10/Investor-Presentation-2QFY24-Gokaldas-Exports-1.pdf)

"We are expecting a decent momentum in the second half of the year, particularly with Q3 production for Spring 2024, as brands have more or less destocked their inventory and are increasing their

order placements. We anticipate sequential growth to pick up in the next two quarters."

Welsupn and Indo Count (Bedding, Towels etc) have also seen increased buying from all major retailers for the upcoming holiday season in the US.

FTA with UK will provide huge tailwind to the sector. Overall, the sector seems to be in good bullish trend. It will be interesting to see how Ambika management’s call plays out in next 2-3 quarters.

Discl: Invested

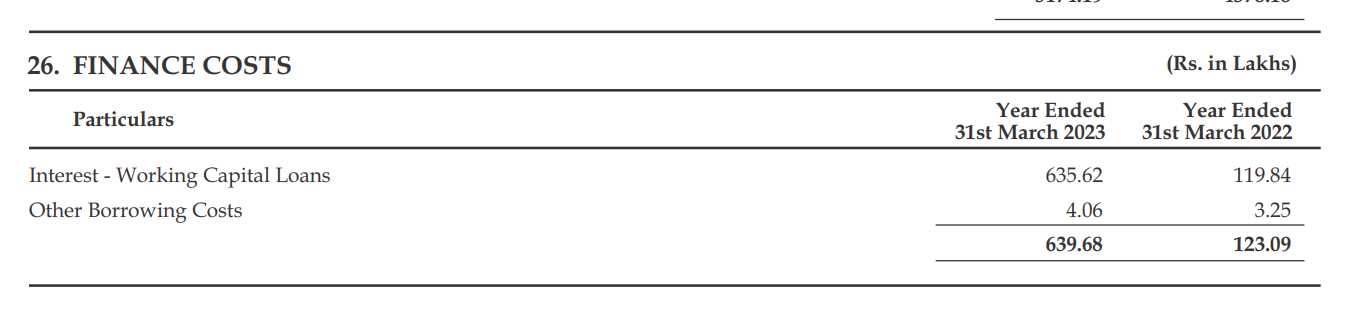

I believe the reference was to Working Capital Loans. See Note 26 in the latest Annual Report as an example.

The short version of my answer is - without any disrespect to the Chairman, I think interest costs have risen simply because interest rates have gone up worldwide - and most definitely in the U.S. I don’t think it mattered whether the reference rate was LIBOR or SOFR. For detailed response, read on.

The interest on most Corporate Loans are charged as Reference + Spread. Earlier, this reference rate was LIBOR. So if LIBOR was 0.5% and the bank decides a spread of 1%, the loan would be quoted at a floating rate of 1.5% (LIBOR being the floating component). Recently, LIBOR has been abandoned and has been replaced by the Secured Overnight Funding Rate (SOFR). More on why LIBOR was abandoned here: What Is Libor And Why Is It Being Abandoned

You can check out recent history of SOFR rates here: Secured Overnight Financing Rate Data - FEDERAL RESERVE BANK of NEW YORK

This clearly show that SOFR rates have moved up from around 0.5% in early 2022 to 6% today. My point is that even if LIBOR was somehow retained in wide global use, interest cost would have gone up because LIBOR will have also risen with the general interest rate increases around the world. Anyway, if it’s any consolation, SOFR forward rates indicates a softnening towards 4% (Source), although it might take a while.

To summarize my personal understanding - any sort of leverage or working capital loan has become quite costly. Energy costs are another reason quoted. All of this aligns with the information from the Management that many of their Competitors aborad had to shut down.

Overall, what is the impact on Ambika?

Increase in Interest Costs from 2-5 Crores to 10-12 Crores. Although that’s a sizeable increase, not much can be done by the company. All the firms in the industry will be suffering from the same issue.

Increase in Energy costs. According to logic provided in this Hindu BusinessLine article, the increase in Energy costs for Ambika could be as much as Rs. 5 Crores. Again, similarly all players in the industry would be facing the same issue. You can find many articles, including this one, where Indian Yarn Manufacturers are protesting the increase in unit prices and even stopping production.

What can/will Ambika do?

The increase in Working Capital cost can be partially or fully offset by passing it on to the customers. I don’t think it’s easy to do that when demand scenario is stagnant. I expect it would be possible once demand picks up, whenever that happens. (This is partly referenced to in many areas of the AGM - that Ambika will only sell with favorable Margins and will not succumb to cost pressures)

Ambika is installing Solar Panels to mitigate the rise in energy costs. According to the Chairman, the company has spent 40 Crs. to install Solar Panels that produce 8.33 MW of power and this will provide them with an IRR of around 10 Crs. per year. In gross for the coming year, 63 Million units out of 78 Million units required for production will be via internal energy generation (Wind and Solar power). The future plan is to take care of the entire energy requirement for production through internal energy generation. (See Chairman’s speech from the 40:23 mark)

Ultimately, in my mind, these minor cost increases are short term pains and not long term detriments. Ignore and move on.

Why don’t they do some buyback?

This question was asked and discussed multiple times in this thread. Please help yourself searching this thread with “buyback” and repost your question if it’s over and above what’s already answered!

I’m finding it difficult to think of reasons why this isn’t a great investment with a huge margin of safety.

1000cr market cap with 800cr in net worth, 0 debt. Assets are 1000cr with 250cr in PPE, 450cr in RM inventory, and 250cr in Cash. The management has never showed any inclination or interest in making risky bets, so one way or another that raw material and cash is going to come back to shareholders.

Admittedly, terrible industry - cyclical, competitive, easy entry. But ACML has a 200bps op margin advantage over all competitors in India suggesting pricing power and trust from customers, as they claim repeatedly.

Thoughts?

It’s just that the market is hitting all time highs and what looks great now might not when there is a correction. It is safer to buy good companies when the markets are correcting than when it is hitting all time highs. I prefer to sit on the sidelines during times like these.

So you agree that ACML is a good company, but there is systemic risk from an overall market correction…or did I misunderstand you?

ACML management from their actions so far seem to be shareholder friendly. But as you have already stated, they are in a tough industry and I personally would wait for a much lower share price with enough margin of safety to consider buying.

As the markets seem to keep going higher and higher, it is a constant struggle for pretty much every human being involved to refrain from buying into this market though. Personally, if I buy anything it will be a few shares for tracking good companies which would then make it easier for me to average down if( ![]() ) and when the market corrects.

) and when the market corrects.

At the moment, it looks like the market uptrend is unassailable. However, I just have to remind myself of Covid 19, Russia-Ukraine War, and Israel-Palestine conflict to not get carried away by the euphoria.

Market going up is never the concern but the valuation going up is the concern. It is true that nifty is overvalued at 22-23PE (20-21PE could be nominal.so 5-10% correction is nominal).

But that is not applicable to ACML since its OPM of 15% in last 3 quarters is well below its historic average of 19%. Hence it will mean revert since its a cyclical business. Also, one must consider that even under this depressed OPM, the EV/EBITDA right now is 6.5. we all know the management is great for a small cap standard. So margin of safety already exist. one cannot assume MoS exists only at 4xEV/EBITDA. we should not refrain from buying just because nifty is trading above historic valuation.

Disclosure: Not invested

Consider an empirical inquiry:

Monitor the fluctuations in cotton prices vis-à-vis Ambika’s stock prices.

The hypothesis posits a direct correlation between the price of cotton and Ambika’s stock value. Specifically, a surge in cotton prices is anticipated to coincide with an upswing in share prices.

The underlying theory suggests that Ambika mgmt operates within the company’s its distinct economic horizon and cycle.

The company strategically procures raw materials at low prevailing prices but refrains from immediate sales. Instead, relying its financial capacity, Ambika stockpiles raw materials until market cycles turn and raw material costs escalate. Consequently, an ensuing surge in Ambika’s stock prices is expected, driven by the company using and processing its stored supplies to its buyers.

This is a conjecture, and any inherent flaws necessitate further examination.

Disclosure ( No position)

Pros:

Cons:

2.Their inability to grow by setting up factories in states outside Tamilnadu where more benefits are given for setting up textile mills…If they can crack this, it shall be great…but mngt seems comfortable only in tamil nadu…

4.Huge cash balance - unable to communicate properly to share holders whats the deployment plan

Adding to the cons.

Disc : Tracking position

Ambika Cotton Mills

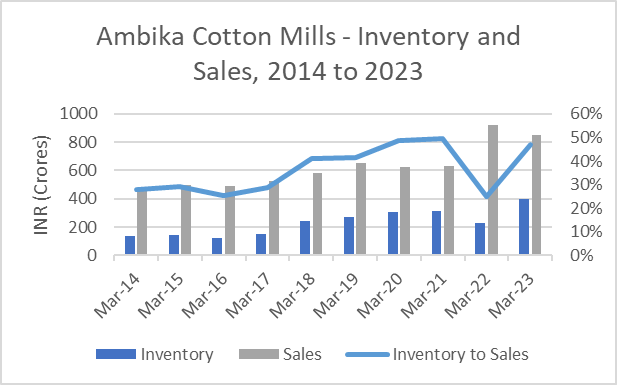

I have been looking at the charts of Ambika Cotton Mills and Cotton prices. Prices seem to be moving in perfect correlation with cotton prices except for a deviation in 2014. The company has been existence for a very long time and has gone through many difficult cycles. The company is known to have maintained inventory levels quite well in the previous cycles.

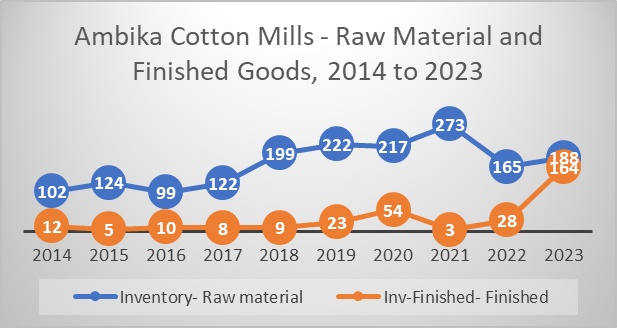

I tried to plot how inventory has changed with cotton prices. Just wanted to know how well the company has managed the inventory over the cycles. Inventory has increased over the years as sales has. So I plotted Inventory to sales over the years. Inventory to sales has remained the lowest in 2022 when cotton prices were at the peak point. Also to be noted the inventory especially raw materials were at the highest point in 2021 when cotton prices began to increase. However, one significant difference that I have noticed this time was the increase in finished goods inventory. Every year until now finished goods inventory was only a small share of overall inventory. However, the finished goods inventory has significantly increased this time around.

The company may be finding it difficult to sell its finished inventory. Noticed the chairman saying in the AGM that they are not selling at lower margins to increase the sales. Inventory has further increased in half year from 397 crores to 498 crores.

Inventory may go increase further going forward until the cycle reverses. Most of these inventory would be yarns and other related items which has a high shelf life. Similarly, the company doesn’t have to worry about the style or anything of that sort which should affect the selling price once cycle reverses. I think the strong cash position is one of the company’s competitive advantages. The company can still run business as usual, even if cotton prices fell further. Even at the current rate of cash conversion into inventory it can comfortably run for 4 to 5 quarters without taking on any external debt The company is run like a traditional business with focus being solely on the core business. That could be one of the reason why company was not very positive on buybacks. The company never had a lot of cash on their balance sheet until 2022, and they are already in a poor cycle. So the next time cycle reverses the company may have to look for better utilization of cash. Also, the current market rates are good as well. The company had an interest income of 5 crores in the current quarter, so the return on the cash is not very bad either.

Disclosure: Not invested

https://www.screener.in/company/AMBIKCO/#chart

@Jose ,

Thank you for clarifying the data and analyzing the Inventory/Finished goods ratio.

The company demonstrates a comprehensive understanding of the cotton/finished goods cycle and the temporal parameters governing its operations. This comprehension facilitates heightened profitability during periods of elevated cotton prices, leading to an augmented operating profit margin (OPM) and an appreciable surge in the market share price. Conversely, a decline in OPM during the low cotton price phase of the cycle results in a market derating.

It is evident that the informed retail shareholder should align their investment strategy with the same cyclical pattern, adopting a time horizon spanning 3 to 4 years. Drawing parallels to financial instruments, the company, based on historical performance, can be likened to a 2-year fixed deposit.

Capturing that exact low and selling at that exact high may be possible for the raw cotton price enthusiast :).

Before finalizing our algorithms, it is noteworthy, as per @Jose 's discerning observation, that the inventory/finished goods ratio is notably high. Additionally, @praveen_potnuru highlighted that a significant portion of exports is directed towards Bangladesh. The recent upheavals, such as violent protests, have adversely impacted the garment industry, attracting attention and likely affecting Ambika.

One could suppose that this problem is deeply embedded and had an impact on Ambika prior to the bursting of the boil. Pure speculation on my part.

Even so, these problems will eventually be solved, and Ambika should be back to its regularly scheduled cycle.

A more substantial concern that the Cotton/Finished Good ratio raises, albeit with a lower probability, is the prospect of Ambika facing heightened competition and a consequent erosion of customer loyalty. Such a scenario could exert considerable influence on the OPM, thereby diminishing returns for the retail shareholder.

thank you @Jose and @praveen_potnuru for the insight.

I read in one of the posts that they run “Make to order” meaning they shall produce only against an order rather than searching for buyer after production. In that case, I wonder why the FG inventory jumped a lot. Moreover if FG inventory is yarn, its fine as yarn can be sold in the market if price game is played even in bad markets with less margin but if its fabric ( knitted) , then I am skeptical about the instant liquidity of the same as fabrics are made with specifications and they cant be sold just like that in market without loosing great amount of money.

Relevant news. It seems the slump is not over yet. Management commentary said otherwise. Let’s wait and watch.

which management commentary, can you share?