Is margin really a confidential info?!! What they have achieved by hiding it? Has market share improved? Has margin improved?

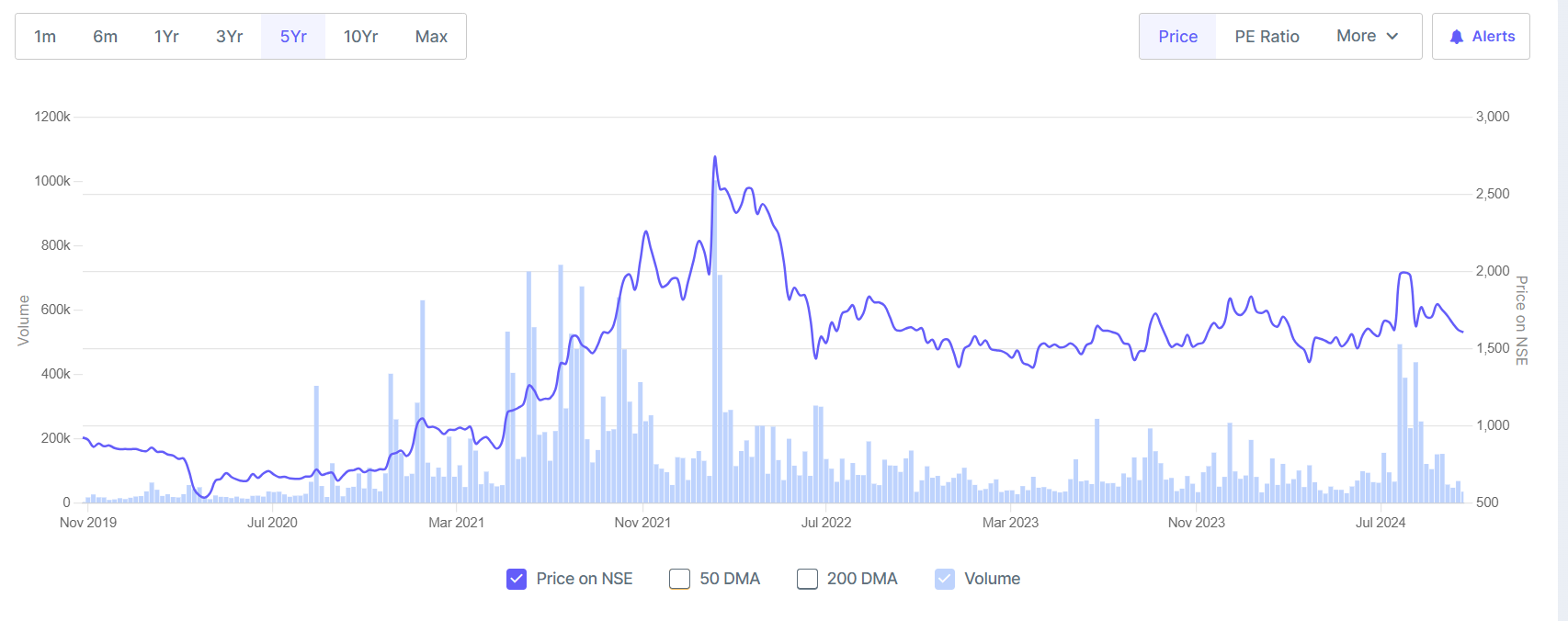

In last 10 years market cap of ambika is hardly doubled, in other hand nitin spinners is more than 10X in same time period even after disclosing that “confidential info”, that fabric margin is 1-2% more than yarn margin.

From what we know (from previous posters), Ambika has been exporting to Bangladesh for some time. Hopefully, with recent developments and the settling down of the country, we will see a smoother flow of transactions. The article is not too positive, but since the country will need to continue to commercially transact, I would assume the business sector will push for the normalcy that was missing so far. From what I know, India is the largest supplier of raw cotton to Bangladesh, fulfilling over 60% of its raw cotton requirements. The Bangladeshi textile industry employs around 4.5 million workers.

The textiles sector is in trend these days. Once the textile companies were not favourites even at P/E below 10 and now the sector has caught attention. Don’t know how long the frenzy goes.

Regarding Ambika , though a great management but a lot of cash is stucked into inventory. The margins were once around 20%+ 4 quarters back but have been below 15% in last 4 quarters. Do not know what gains they got for holding the inventories.

There are reports of early Cotton Crops in South. The sowing area is also increased vis a vis last year. A good Monsoon is seem to be on the table. Cotton prices may cool off. Lets see how Ambika dilutes it’s inventories and reaches back to 20+ Operating Margins. The sector seems to be Street’s favourite right now. Let’s see for how long.

Bangladesh’s garment factories, which account for 90% of the country’s exports, have reopened after a period of unrest, with factory owners assuring Western buyers of their reliability despite recent disruptions. The industry estimates a loss of six days of production due to the instability, which erupted in mid-July following large-scale wage protests last year. While the situation is now stabilizing under the caretaker government led by Nobel laureate Muhammad Yunus, the combination of recurring bouts of instability, higher wages, and long-term infrastructure challenges are raising concerns about Bangladesh’s competitiveness as a garment exporter.

Meanwhile, another low-cost rival, India, is gaining, thanks to its ability to produce its own fabric, which saves production time.

The company continues to deliver average results. EBITDA margin continues to be much below the past levels, and this mainly seems to stem from the fact that RM cost as a % revenue has stayed around 67-68% in the last 5-6 quarters as against 60 to 63% levels seen over the past few years.

However, the decline in profit margins is better explained by the volume and realisation data of the last few years.

All figures in Cr

ACM - Company level

Yarn

Knitted Fabric

Waste Cotton

Year

Total Revenue

EBITDA%

EBITDA/kg

Production

Sale

Revenue

Realisation

Production

Sale

Revenue

Realisation

Production

Sale

Revenue

Realisation

2024

823.46

13.4%

43

1.65

1.22

482

395

0.62

0.61

231

379

0.74

0.73

88

121

2023

847.5

20.7%

78

1.83

1.09

527

483

0.41

0.41

185

452

0.79

0.75

105

140

2022

920.52

29.4%

97

1.91

1.24

505

408

0.72

0.71

298

420

0.85

0.85

76

89

2021

633.36

19.9%

46

1.63

1.16

317

273

0.75

0.83

240

289

0.71

0.73

58

80

2020

623.09

17.0%

38

1.8

1.2

323

269

0.85

0.8

221

277

0.78

0.76

63

83

It is clear from this data that production and sales volumes have broadly stagnated for last several years and all the revenue growth has come from increased realisations brought about by high cotton prices. A very important thing to note here is that EBITDA/kg (on blended basis), has remained stable over the last 5 years, barring 2022 and 2023, which were years of exceptional profitability caused by inventory gains.

Thus, margin decline might be just optical, and there is no real deterioration in pricing power of the company. ACM seems to be operating on a cost-plus model rather than a fixed-margin model. This means two things -

We should perhaps not expect any significant increase in absolute EBITDA/PAT, unless there is real volume growth - which seems unlikely in near future given the circumstances ACM finds itself in. A growth in absolute operating profits due to reversion of EBITDA margin to past levels is probably unlikely, since margin will come back to past level if cotton prices decline to past levels, at which point even the revenue will revert to 2021 levels! So we will be back to PAT levels seen in 2021.

The return ratios (RoE/RoCE) of ACM are anaemic because of the huge inventory and cash holdings on the balance sheet. The high inventory levels also subject the company to price risk - expensive raw material stocked up during high prices will eat up into absolute EBITDA from future sales if the market prices come down. This is a real impact, even if we don’s see inventory write-down entries being passed in the income statement.

Finally, the management seems well-intentioned, and to be fair they are dealing with tough external environment. But the idea to look at the business from a perspective of capital efficiency seems to be missing.

CAPITAL ALLOCATION RISK( additional speculation thru unlisted equity shares) —The equity markets hype is sooo high that Mr. Chandran who publicly stated that his strategy of parking excess cash in cotton inventories yielded good results for the company changed his views and invested 14 cr in unlisted nse shares along with additional investment in two listed equity shares worth 25 lakhs… This is very concerning u turn as habits like these are dangerous for companies with high cash balance…they can invest in their business or return money to share holders —- speculating in cotton stock itself is risky, now speculating in stock market that too in unlisted shares with company cash is even more risky terrain….. ( this info is in page 82 of 2025 annual report of the company released yesterday) …. I will be more worried if this strategy yields positive result for the company as they may take it as validation and pour additional money into such stuff in future….