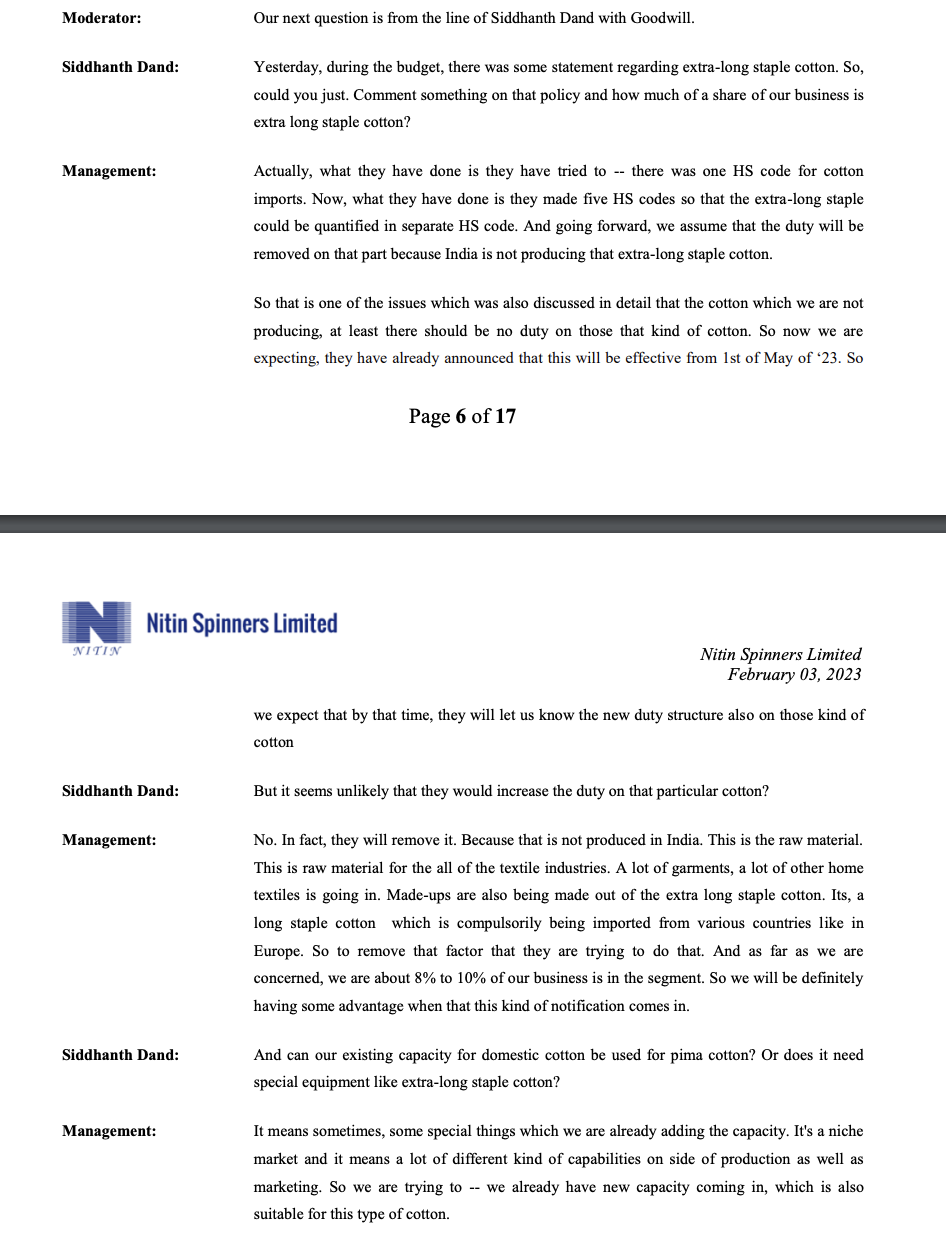

In my interaction with the management of Nitin Spinners they raised a very interesting point about HSN codes being split for reducing duty on cotton not produced in India.

Common sense says that AMBIKA could be the direct beneficiary.

But how long can they protect the niche they have in Extra Long Staple Cotton? and is there a risk of others also adding excess capacity there if govt gives incentives.

Also Ideally the co should add capacity and use cash if the duty on ELSC is removed, otherwise tough to see a lot of shareholder value being created.

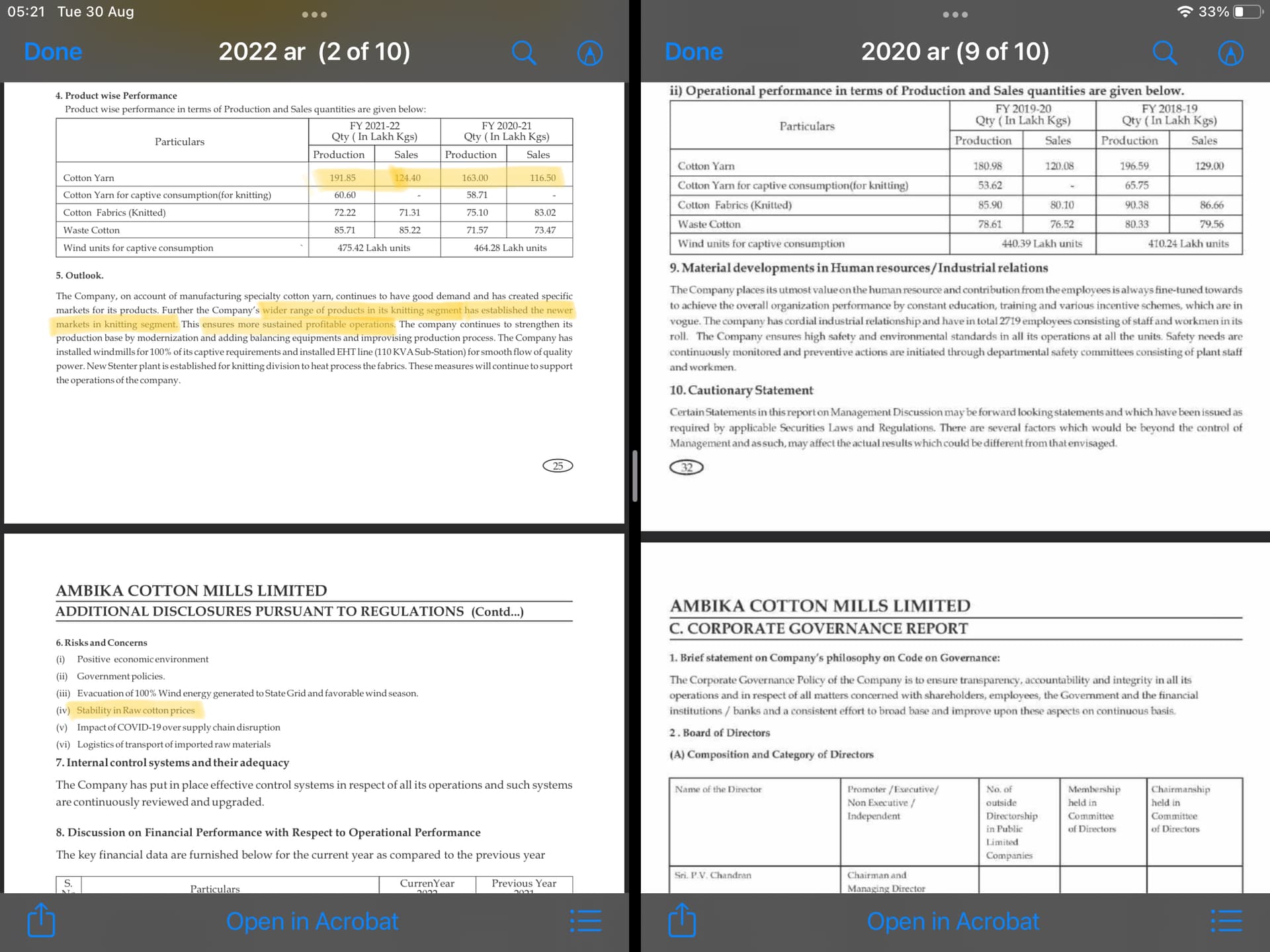

Yes my mistake, In fy2018-19 coy achieved max pdcn of yarn 197 lakh kg and knitted fabrics 90.38 lakh kg while sales volume was also maximum in both category in that year. So imo no need to do capex till coy is not able to sell same or higher quantities in coming years.

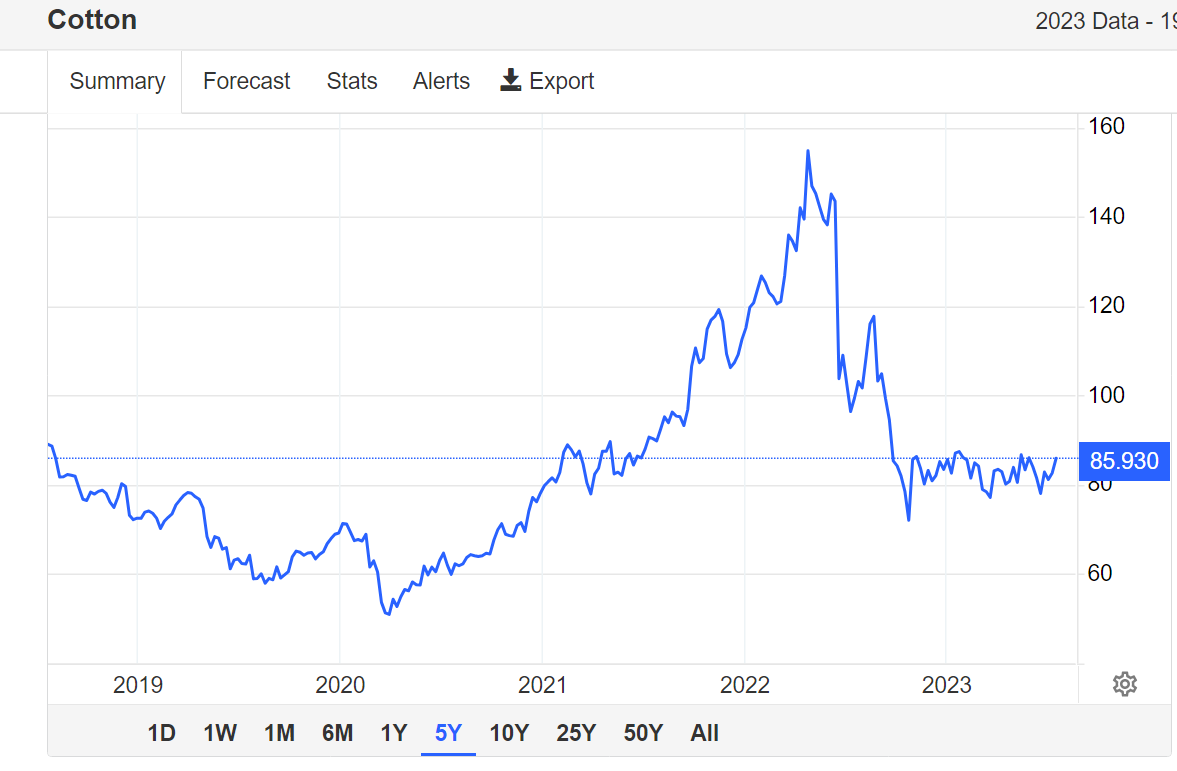

Yarn prices have also come down a lot. Data for spreads of cotton-yarn required. Volume growth would be muted due to overall slowdown in export economies and sluggish domestic demand.

Results for PDS Ltd (that sources textiles and sells overseas) has also been very muted. Management commentary says that the overseas market is very slow at the moment.

Cotton yarn exports is picking up ,good demand for yan from exports as well as domestic markets since last one month, most of quality yarn spinning mills are having yarn bookings for next 2 months

An interesting case of this company with the honest promoter having nearly 800 cr Mcap, 400 cr inventory and nearly 300 cr cash or equivalent, is this company available for free of cast? Disc invested.

What prompts you to guess that the promoter is not going to be shareholder friendly ?

If your view is that 300 Cr cash on book is too much for 800 cr networth company, it should be noted that most of this cash is accumulated in the last 2 financial years due to huge profits compared to historic average. The company has consistently maintained dividends of 20%(which is ok for a company which had no excess cash but some debt till FY20) and RoE of 16%.

I find the management very sensible in deploying some of the cash when they decide to go for 8.4MW rooftop solar power capacity in their Dindugal manufacturing plant. @alokinvestor is right. At 1 X P/B, 1 X P/S, 3 X EV/EBITDA, 2.5% dividend yield, it is undervalued.

management has repeatedly stated they won’t do buyback because trading volumes are very low, won’t have meaningful impact. Tried it once, not satisfied with the results.

Industry::Textiles is a cyclical industry, presently with high cotton (raw material) prices and muted export demand. The conditions are a strong deterrence to both earnings growth and multiple re-rating probabilities;

Company:their business is in a very competitive industry - they have had great double-digit margins bc. of their loyal customer base (compared to Nitin Spinners and so on), not their exceptional operational ability (i.e. page industries). This is an advantage they can lose easily, given brands do not particularly have high supplier loyalty.

Lastly, the management: is old and conservative. That is not necessarily a bad thing. But in an industry which is hyper-competitive and extremely vulnerable to demand and supply trends, I want to see management which strives for sectoral leadership by taking bold steps. The survival rates for textile mills are among the lowest (funeral homes being the highest). Thus, if they do not snatch market share, their share will always be eaten away by other sharks. Moreover, in an industry which has immense potential to draw investment out of China, Bangladesh, Vietnam and into India (mainly bc. India has close proximity to cotton as a raw material domestically and from Pakistan + cheap labour), I just do not see the management of Ambika taking the risk and trying to grow. They have been and always will be in survival mode.

In conclusion, the stock presents a limited downside due to cheap valuations and a strong balance sheet but does not present multi-bagger-like growth opportunities. Expect 10-15% earnings growth and equivalent share price growth.

INDUSTRY : my views are same as yours.however, this perception wrt industry can also provide low price points wrt value to enter the company.

Company : I am putting my trust in management when they say their superior margins are due to technical and specialised products, and, management comes across as frugal as anybody can get and operationally exceptional in sweating the assets.

Management : Agree to some of the points. They come across as conservative, content and satisfied with the size of business (and wealth, controlling stake just above 50% to fend off any possible attack) they have built. I believe there was a mention somewhere Promoter stated he wants to live a simple life and dividend income is sufficient enough to take care of his expenses. I do not think this (their mindset) qualifies as survival mode, rather just the very opposite. In the recent AGMs they have stated cash on books is for growth (organic or inorganic) purpose but only when they probability of success is very high.

I do not think this is a high flyer, but if you check their FCF generation, return metrics (post adjusting for additional inventory and cash they are carrying, additional inventory liquidated during favourable times and cash hopefully utilised for growth purpose - no timeline) and 10-15% long term CAGR earnings (and FCF) growth whenever it happens, this can be decent addition. Of course based on personal investment targets and time-horizons. Other key parameters: what will be utilisation of additional FCF generated, if any. Test for your temperament. Price points you enter at.

Disclosure: Invested. I have small position wrt PF, will add to it using favourable part of cycle, or, Growth capex announcement as a trigger (off course depending on the price available at that point of time). Enjoying average dividend yield and sitting on cash(in company’s balance sheet, not mine) till then, or, may be my patience will run out.

Regarding questions on inventory, Mr. Chandran had clarified in the AGM 2-3 years ago that they trade heavily in cotton. They have good insight of cotton market & use cash to park in inventory than to keep in bank.

“The cost under SOFR regime is high at 6% as against at 1% under LIBOR.”

What cost being discussed here? Interest cost or the cost of raw materials or tax or something else?

Sounds like, this is a permanent change in the regime. So probably understanding what this means is critical to understand the impact on the company.

From what I read, it sounds like interest cost. Why is Ambika impacted by this, as the company entirely depends on internal accruals and with nearly no debt?

Any help to understand this is appreciated. Thanks.