PM MITRA plan of Rs 4400 cr (approx.) PLI for textile Rs 10636 (approx.) are they key tailwinds to textile industry.

5 Likes

The cotton prices have generally gone up in the last one year.

It looks like they were able to control the cost mostly because of the inventory pile they had.

1 Like

What an excellent result declared by the company!

1 Like

If we analyse the demand in cotton yarn Ambika Cotton Mills has able to utilize the opportunity and post fabulous results.

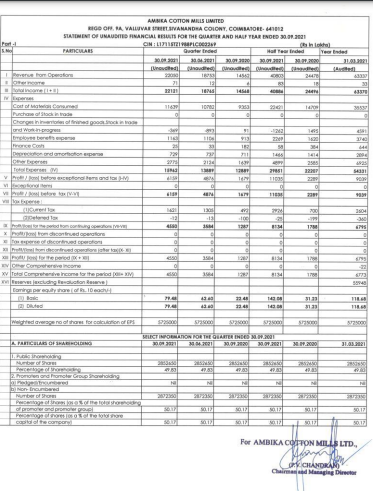

The half yearly PAT is more than 81 Cr which incidentally is more than the Yearly NP declared by the company since inception. The revenue is approx 71 percent from exports and balance from renowned Domestic clients like Arvind Mills, Raymond, Aashima Textiles and Morarjee. With another 2 quarters to go by the yearly NP & EPS is anyone’s guess. The only dampner is likely to be the cotton prices which are at an all time high ( cotton constitutes almost 60 percent of RM cost ).

Topline has grown and as per the Chairman the company is aiming for 800 Cr as yearly topline - which seems achievable ( considering that the half yearly topline is 408 Cr). With OPM improving the bottom line is any one’s imagination.

4 Likes

2 Likes

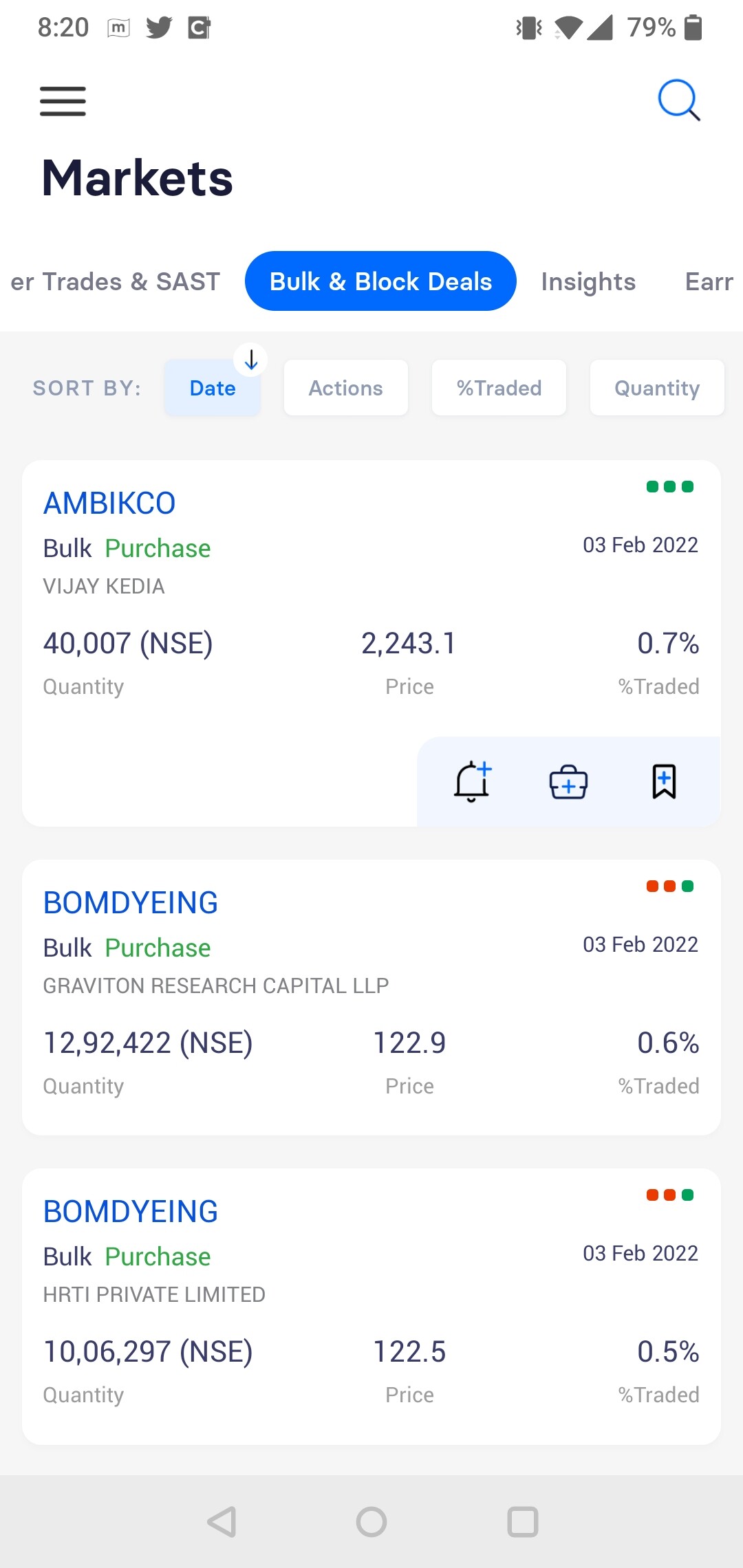

Indeed, Q2 sales are at 220.5 Cr

But I am curious, how did they do additional 14.32 Cr sales in 2 days? (avg for last 2 days is 7.16 Cr)

220.5/60 (assuming 60 weekdays in a quarter)=3.67 Cr average sales per day

So avg for last 2 days is double that of full quarter avg daily sales. Is this normal or an aggressive practice of booking sales early (aggressive revenue recognition)? (no allegations, only trying to understand)

Disc- holding

1 Like

Ambika is a good fundamental company, and management is shareholder friendly.

With current market cap of 1250 cr and 186 cr in cash equivalent, the total company is avl for roughly 1050 cr.

The current free cash flow is in excess of 130 to 140 cr.

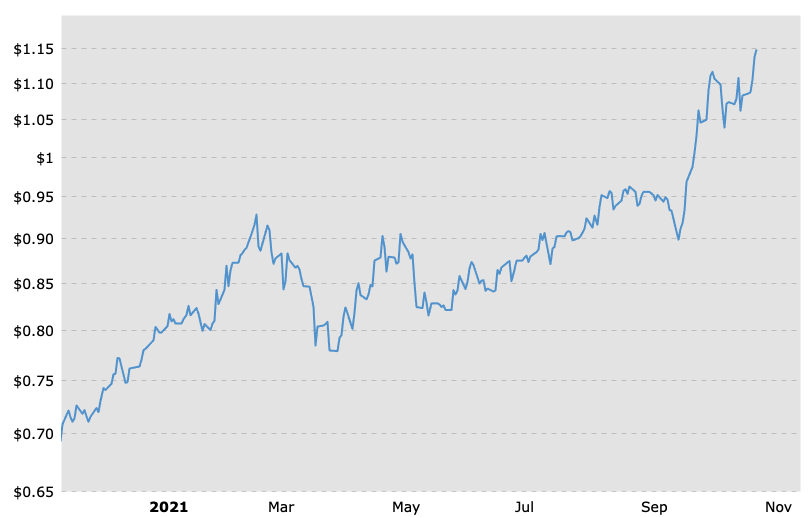

Though the CMP is at a historical high, the company still is Avl at a reasonable valuation.

My concern is the terminal value and longevity of the business, as Mr. P chandran is almost at retirement age, and i am not sure if there are future leaders like him to take this company to the next level.

Your thoughts on the next 5 to 10 year journey of this company pls.

Thanks

3 Likes

Last few days of the quarter/year always have higher bookings as companies are in a hurry to finalize the orders before the close of quarter/year.

3 Likes

The whole textile sector has got rerated. Most are declaring good revenue and profits growth with increasing margins.

Trigger might be due to US banning cotton import from China and PLI from govt might be adding to the sector tailwind.

Disc - Holding Ambika Cotton

1 Like

Xinjiang produces 85% of China’s cotton and 71% of its yarn. Biden’s latest law against Xinjiang products can be a game changer for Ambika’s sales growth

2 Likes

Ambika Cotton is up due to higher margins. Reason for that was cheap cotton inventory which they had bought during lockdown. Same cannot be achieved in near future.

2 Likes

Is anyone having knowledge about their expansion plan and what capacity expansion are they doing ?

I believe this was asked on the last 2 conf calls. While they would expand, I don’t believe they have announced the expansion plans yet.

Excellent set of numbers as expected from Ambika. EPS grew nearly 2.5 times YoY and about 15% QoQ. Valuation continues to be attractive.

Quarterly revenue has crossed 250 Crore and profits crossed 50 Crore respectively for the first time in companies history. Kudos to Mr. Chandran and his team.

See the results here.

Disclosure: Invested from lower levels and accordingly consider my views as biased.

AJ

10 Likes

Yes, that is an excellent result. All this is mainly operational efficiency driven. Capacity growth is on the table for the last 1+ yr but yet to be formalised. During that time, they have consistently increased topline as Mr. Chandran had mentioned. On top, they made the most of tailwinds and expanded margins (~21% PAT margins) as well.

Is there any further scope for margin expansion? I guess capacity expansion should provide the next trigger for growth.

Disc: Invested, 3% of PF.

2 Likes

Hi everyone,

could anyone comment on revenue concentration? who are the top 3 clients of Ambika cotton?

{kind=link}

is it like they have got a big client to whom they are selling fabrics?

its been almost 4 years since they have started generating a significant amount of revenue from knitted fabrics and realization on fabrics have been better.

If anyone can comment on what are avg realization for knitted fabrics one can expect? (I only want to understand, once the RM benefits can get and company will come back to normalized 17-18% OPM in yarn, will knitted fabrics help them to improve margins because I believe some amount of operating leverage will kick in due to forward integrated higher per KG realisation product.

3 Likes

Can anyone explain the approx thesis, why he bought so late in this scrip.Future projections ?

What about handing over leagacy to next generation ?

Found an interesting read :

: The textiles industry provides 2nd largest direct and non-direct employment in India, the first being Agriculture. This might make Ambika Cotton Mills the best stock to buy now.

Value chain of the textile industry:

- Fiber

- Spinning / Twisting

- Weaving / Knitting

- Dying / Bleaching / Printing

- Styling / designing

- retailing

The textile business has grown over the years in such a manner that much of the power is put into the hands of retailers and marketers at the end of the value chain.

Even though it is at the beginning of this chain, Ambika Cotton has a unique position in this value chain that will become evident as you read on.

Let’s dig deeper into best the stock to buy research for Ambika Cotton Mills now.

About Business :

Ambika Cotton Mills Limited (ACML), situated in Coimbatore, Southern India, produces top-grade Compact and Elitwist cotton yarn for hosiery and weaving. We are a well-established participant in the international and local yarn markets, with exports accounting for around 60% of total revenue.

The firm was founded in 1988, and its four manufacturing plants are located in Dindigul, Tamil Nadu, with a total spindle capacity of 1,08,288 Compacting System spindles.

Reason 1 - Extra Long Staple (ELS) cotton

Ambika Cotton’s raw material is Extra Long Staple (ELS) cotton, which is of the finest grade. A general ELS cotton fiber is 1 3/8" or longer, as opposed to Long Staple cotton, which has a long-range of 1 14" but less than 1 3/8" and normal cotton, which is less than 1 14". ELS cotton is one of the smoothest and most durable cotton fibers available.

The fabric was originally intended for the British Army in WW2 to be cool and pleasant on land but warm and impervious when it came into touch with water. Whenever wet, the ELS cotton fibers expand, creating a protective barrier that shields the user from the elements. Outdoor enthusiasts searching for a breathable textile for their trips rapidly learned about this technology.

Reason 2 - Supima certificate from Supima Association (USA)

Ambika possesses the Supima certificate from the Supima Association (USA), the GOTS certification for organic yarn from Control Union (originally SCAL), and the Oeko-Tex Standard 100 Product Class I certificate from Oeko-Tex.

Kinds of cotton aren’t all made equal. Cotton cultivated in the United States is known as Supima. It accounts for less than 1% of global cotton production. The extra-long staple fiber that provides Supima its premium attributes of strength, softness, and color retention distinguishes it from another cotton.

Extra Long Staple (ELS) finer fibers absorb the dye more deeply and for a longer period. As a result, the fabric keeps its color longer than conventional kinds of cotton. This ensures that Supima goods maintain their brilliance wash after wash, permitting you to use them for many years.

Reason 3 - 0 debt in a bad industry

The textile industry as a whole has massive debt on its financial sheet. To pay their loans, firms in this industry continue to dilute their equity. It’s no surprise that the industry has never achieved a PE in the double digits and has never truly participated in a bull market.

On the other hand, Ambika Cotton started shedding debt in FY10 and went completely 0 debt by FY21.

A sluggish economy or a rise in interest rates does not effect on debt-free firms. They can continue to operate their company even if the economy slows. Because they are debt-free firms, they may give greater returns. Debt is merely a short-term solution to a financial problem. Debt has a larger long-term cost. A debt-free firm provides a greater dividend yield and has a better return on equity.

Reason 4 - Modernization of plant

Despite the fact that the firm hasn’t grown capacity in a long time, it has been able to meet volume increases year after year. The Company’s modernized product line in the knitting segment has opened up new opportunities in the knitting industry.

Even though knitted realizations are smaller, the ROCE can be significantly larger.

Reason 5- Succession plan

P K Ganeshwar, Rathanasamy, and P V Chandran founded the corporation with the goal of establishing a cotton spinning factory.

They steadily increased their capacity over time. The capacity was increased by 43,000 spindles in 2007, bringing it to its present level of 108,000 spindles.

Mr. Ganeshwar and Mr. Rathanasamy, the two promoters, appear to have quit the firm during FY 2006 for unclear reasons. The promoters held a combined stake of 70% at the end of FY 2005. Mr. Chandran now owns 25% of the company after the other two promoters sold their shares at the end of FY 2006.

Mr. PV Chandran, who is also a major stakeholder, is currently in charge of the company. Mr. Chandran has steadily raised his stake in the company over the years, rising to 35 percent in the fiscal year 2008, 40 percent in the fiscal year 2011, 46 percent in the fiscal year 2012, and 50 percent in fiscal year 21.

According to him, his daughter and son-in-law have begun to work in the firm, and he plans to take over leadership at a later date.

Reason 6 - Long-lasting B2B Clients

Arvind Mills, Raymond, Aashima Textiles, and Morarjee are among Ambika Cotton’s domestic customers. Quannitex Enterprise Corporation of Taiwan, Pacific Textiles of Hong Kong, and Winnitex Investment Company of Hong Kong are its key international clients, as are branded players such as Uniqlo of Japan.

They stated in their annual report that they are not looking to add any more clients beyond the 12 they now have since they are unable to meet their current expectations.

Reason 7 - No CAPEX in 30000 spindle capacity (Bad)

According to the promoter, this was not done even after all permissions since the facts surrounding the choice changed. Some other states have taken away the TUFF (Technology Upgradation Fund Scheme) perk, which provided far greater benefits to yarn producers than Tamilnadu.

All of these factors had an influence on the decision’s payback duration and return on investment. Instead, he reasoned that investing in knitting would yield higher results, so that’s what he did. He considers how to improve the bottom line while weighing various choices.

Reason 8 - Good dividend yield

There would be no repurchase since, according to the promoters, shareholders will be compensated with dividends. The current assumption is that the company’s stock suffers from a lack of liquidity and that stock buybacks diminish the floating shares even further.

Ambika Cotton Mills has announced an equity dividend of 350.00 percent, or Rs 35 per share, for the fiscal year ending March 2021. At the current share price of Rs 2374.00, this equates to a 1.47 percent dividend yield.

Reason 9 - Turnover sources

Best stock to buy right now Ambika Cotton has 3 main products to sell & here is its breakdown for FY21

- Cotton Yarn: 50%

- Knitted Fabrics: 38%

- Waste Cotton: 9%%

- Total Turnover: Rs 633 cr for FY21

They are about to cross Rs 800 Cr + first time for FY22

Reason 10 - FII Holdings (bad)

FIIs holding has dropped from 4.6% to 2.3% + in the last 3 years.

Reason 11 - NPM

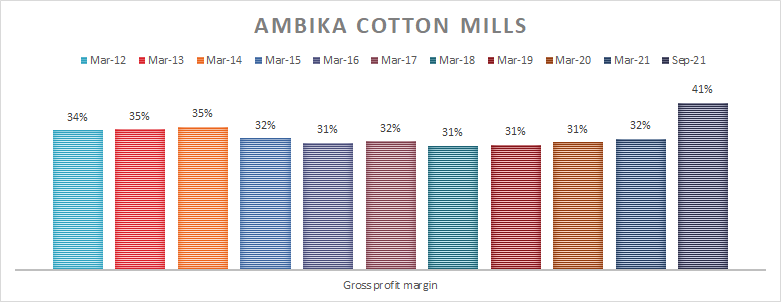

Net Profit Margin (NPM) has hovered around 10% for many years till Covid hit then it shot up to above 20% + due to increasing cotton commodity prices.

27 Likes

Even though their profits have almost tripled.They are increasing the dividend only a little.Very surprising as the promoter is known to have a honest and shareholder friendly image.What will he do with the accruals?

2 Likes