Is there any sales growth expected for Ambica in coming years because of all the domestic/global positive textile news?

Disc: Invested.

Is there any sales growth expected for Ambica in coming years because of all the domestic/global positive textile news?

Disc: Invested.

Q1 results

be73be03-4e60-442d-b381-88998f788b7b.pdf (2.2 MB)

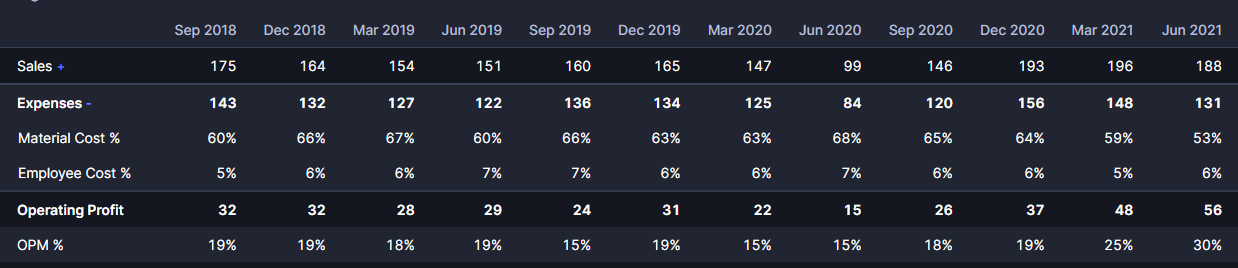

This company’s results over the last few quarters will put even the fmcg results to shame. If such a performance is sustained for couple of quarters, it will have approx. 120/130 cr PAT annualised while the mcap is only 880 cr. God knows what else market is expecting from this company. The highest standards of corporate governance, generous dividend sharing, decent growth. What else one needs ?

A recent article in Wall Street Journal on US pressing china on its child labour issue bodes well for yarn exporters. This is being reflected in current results as well.

Interestingly, there are no big names to show in the investor list. All exited before Dec 2020 and Valuequest India Moat Fund too. Nobody might have anticipated such results and turnaround.

Patience pays!

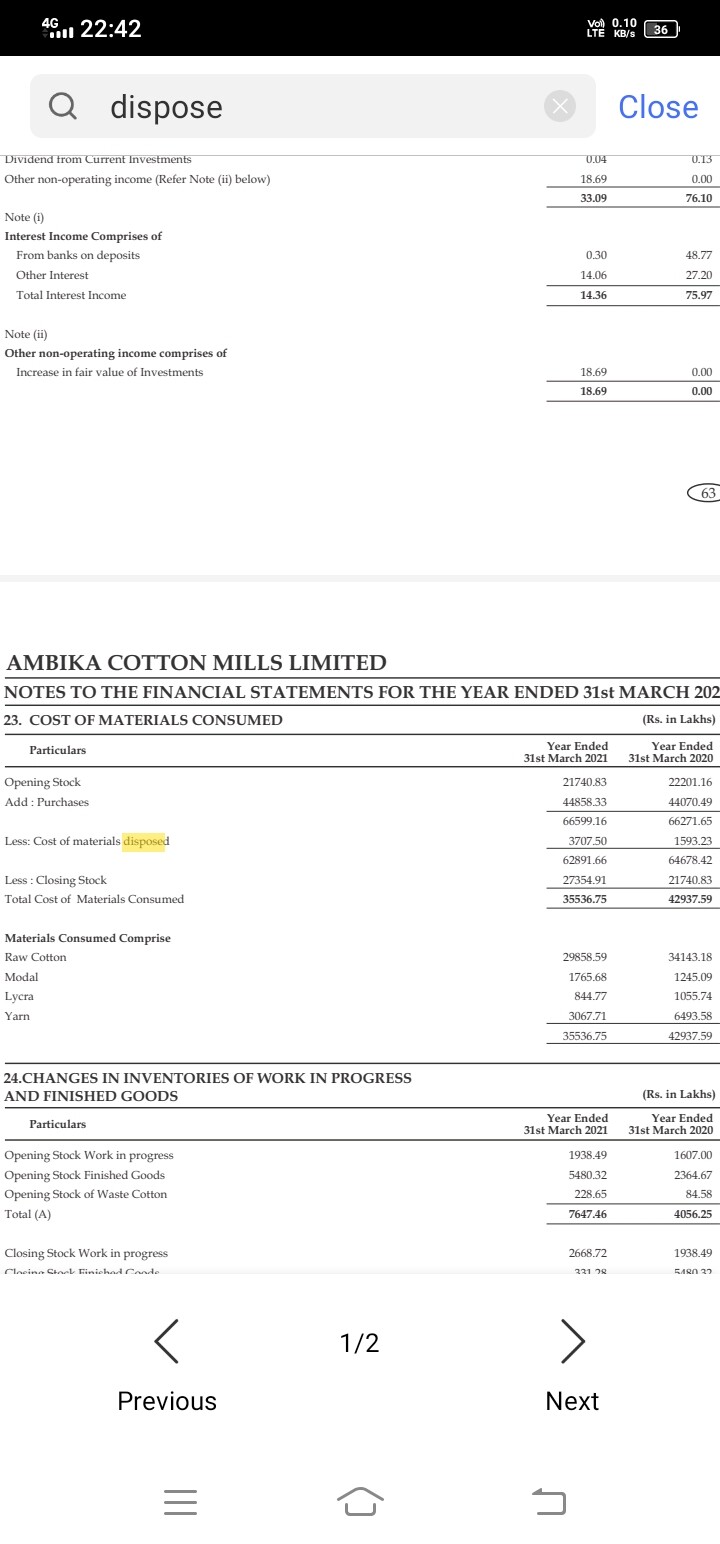

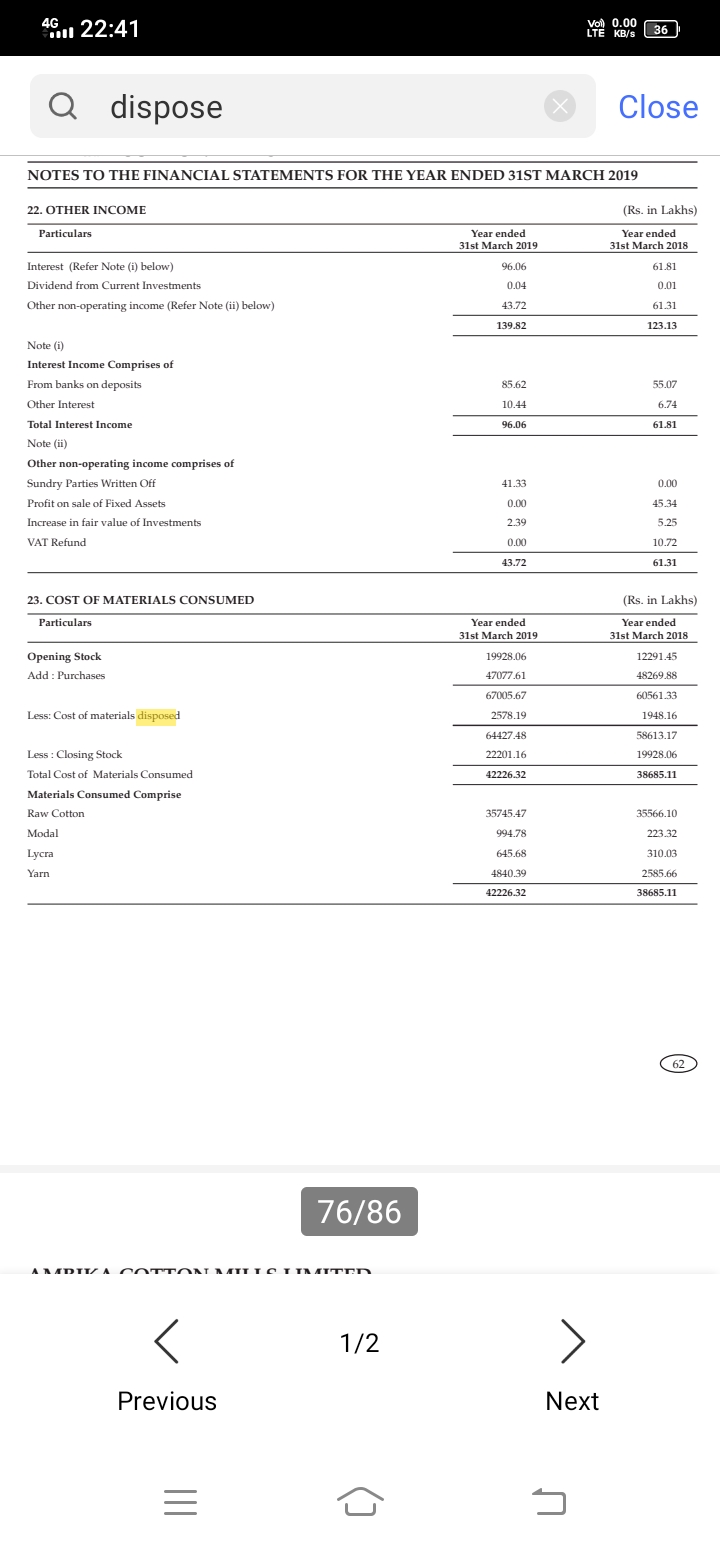

Can anyone pls reply what may be this, is it RM disposal due to obsolescence or anything elese which I m not getting? Can it be a sign of poor inventory planning ?

Check other yarn producers and you will realize what this is. Nothing negative.

Ambika is one of the most efficient and clean management.

I think they purchased RM but not used due to any reason so they sold it as it is that’s why reduced same amount from cost of materials consumed head. is it?

The company has a policy of “parking” cash in raw material. See this:

They buy in bulk before others when the crop is fresh and they get good rates as they can pay upfront cash. Later, some cotton may be sold off to other parties. Usually this happens at a profit – you will find an item “profit on disposal of raw material” as part of Other Operating Revenue every year.

Got my answer thanks, i read profit on disposal of RM but couldn’t relate it to “parking of extra cadh as RM” while it was mentioned in previous threads. This doubt comes bcz they r holding very high inventory from last 4- 5 yrs.

Holding high inventory is a rarity. They make specialized yarn. Have confirmed orders from long time customers and against that they procure raw material when cotton arrival is at peak. They are cash reach so can do that. Check out cotton prices variation from october to august and you will get idea. All agro commodity prices are cyclical and one has to have a good sense and a bit of luck to stock it close to bottom for any year.

hi All

went through the Ambika AR. The metrics that i closely track continue chugging along well -

| Realization per kg | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 |

|---|---|---|---|---|---|---|---|---|---|

| Cotton Yarn | 283 | 319 | 278 | 261 | 264 | 265 | 273 | 269 | 272 |

| Knitted Fabrics | 250 | 247 | 218 | 211 | 195 | 205 | 267 | 277 | 289 |

| Waste Cotton | 64 | 72 | 59 | 54 | 65 | 78 | 78 | 82 | 79 |

while fabric realizations continue improving, yarn realizations have been lacklustre. the company hasnt even been able to benefit from the forex movements.

| Inventories | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 |

|---|---|---|---|---|---|---|---|---|---|

| RM | 71 | 103 | 125 | 100 | 123 | 199 | 222 | 217 | 274 |

| WIP | 9 | 12 | 8 | 7 | 14 | 23 | 16 | 19 | 27 |

| FG | 7 | 12 | 5 | 11 | 8 | 10 | 24 | 55 | 3 |

| others | 6 | 6 | 6 | 6 | 7 | 8 | 10 | 12 | 9 |

| Total | 92 | 133 | 145 | 124 | 152 | 240 | 272 | 303 | 313.2 |

relieved to see the excess FG inventory out of the system.

while the Q1 results have been very good, i am not too sure of its sustainability.

the current fair value as per me is 1200, so continue to hold

AGM.pdf (1.7 MB)

Proceeding of the 33rd AGM notes issued by company.

Key points.

Thanks for the prompt upload. The annual turn over of 800 Cr , as expected by the management is more than 30 percent YoY and the highest so far. The Chairman has in para 3 of the AGM notes mentioned this

" The net profit for the QE 30 Jun 21 stood at Rs.35.84 Crores and Cash Profit at Rs.43.21 Crores The net profit for the quarter ( Jun2021 ) represents 53% of the earnings of the previous fiscal profit ( FY 2020-21) . "

Looking forward to QE Sep results for obvious reasons.

Any indication from the call if the higher turnover in the current year is driven by higher prices (cotton and so yarn prices must be in bill cycle like other commodities) or any capacity expansion.

It has been a few years when first management planned a 30% capacity expansion with more spindle addition. Since than there has been no update despite management reiterating about high demand of their products and inability to cater to more than current 10-12 customer set.

Any additional info here would be welcome and highly appreciated

Video link of the AGM

The AGM commentary by management included the following paragraph:

In the first quarter ended 30th June 2021 of the current year, the company had made a total sales turnover of Rs. 184.07 Crores, of which Direct export constituted Rs. 139.97Crores. The net profit for the period stood at Rs.35.84 Crores and Cash Profit at Rs.43.21 Crores. The net profit for the quarter represents 53% of the earnings of the previous fiscal profit. The Company up to 28th September 2021 had made a total turnover of Rs. 390.25 Crores of which Direct Exports amounted to Rs. 289.84 Crores.

By simple math, 390.25-184.07=206.18

So, if I understand correctly, Q2FY22 sales will be >= 206.18 Cr. Am I correct or am I missing something?

Disc- invested

Your understanding is correct, last 2 days of sales will be added to it. For some strange reason, they do this every year at the AGM. You can check past AGM transcripts as well.

What is the growth trigger for Ambika Cotton such that it is very obvious for it to grow from here ?