Could you please explain why you consider it as good news.

Thanks

3 Likes

They have been selling for a few quarters. Likely reason would have been lack of expansion and not return ratios/ profitability. So this has been an overhang on the stock. This is not to say that the sellers reasoning was wrong, infact they must have switched to better ideas.

For the new buyers, the business outlook has improved (lucky). If expansion projects are announced then it will be a bonus. Valuations are still reasonable at 5x normalised ebitda, which basis historical median can be 20% of gross block or 125crs.

3 Likes

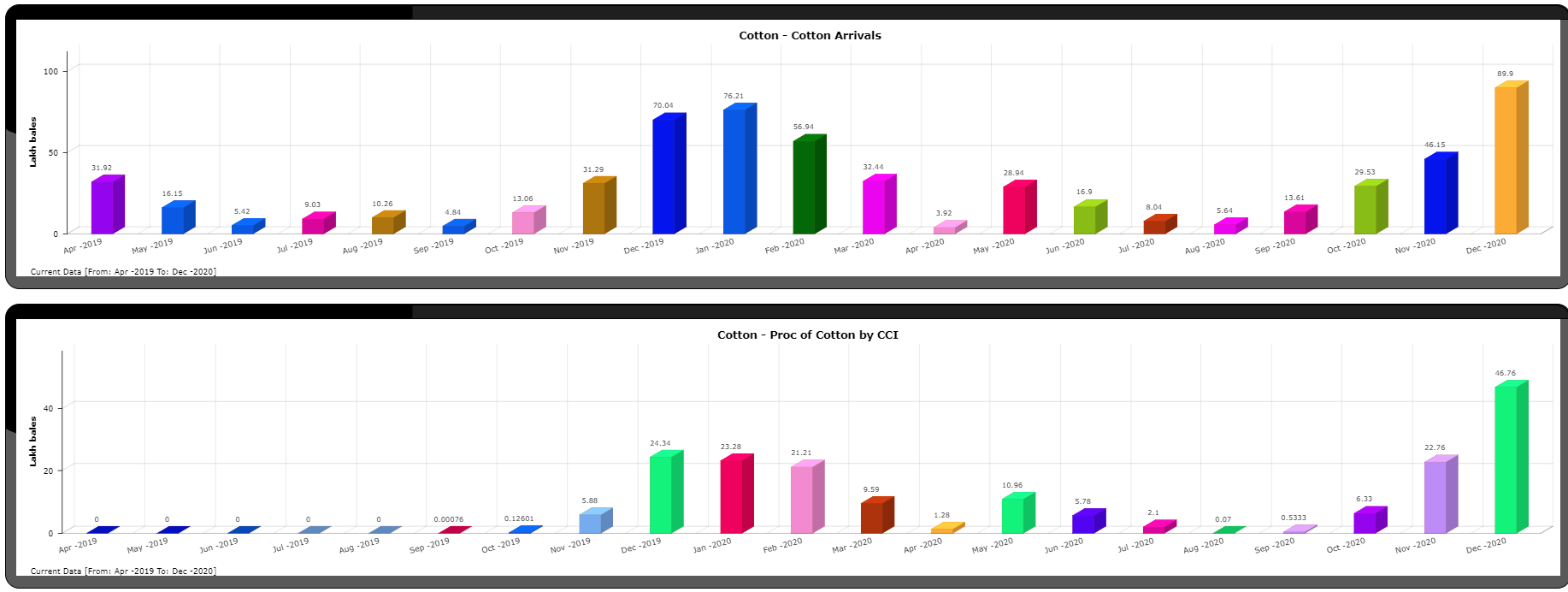

The market is seeing heavy arrivals (supply) of cotton due to fear of another lockdown in key importing countries. Though CCI is trying hard to keep the same pace in procuring the cotton bales, it is not able to do due to limited spaces for storing. This may put pressure on cotton prices to correct a bit or at least remain stable which will be good for this industry

2 Likes

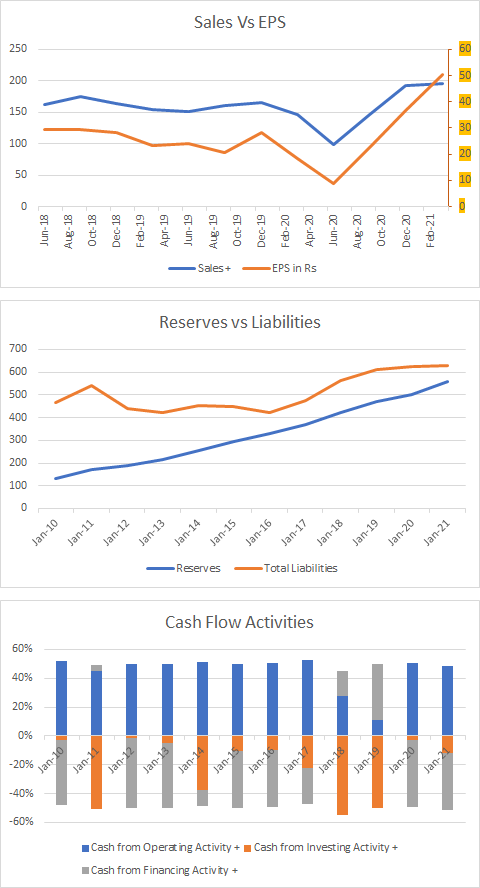

Can you pls help with understanding/interpretation of the graph ?

Also the overhang of the big guys selling is out now and any big purchase will now lead to exponential growth in price.

1 Like

Huge addition in inventories /wip also is a indication that things are good wrt to demand visibility. This can also be attributed to the additional 10% duty on imported cotton announced in the budget. Hence adding inventory makes sence for ACML.

1 Like

Right @Guru_Prasad, the 10% duty on fabric imports is indeed a dampener structurally, if not short term but definitely long term and that may be explain the reason of market reaction.

Results would have been much better if this was not done. They will have best year in a decade

- The industry association has already made representation to the concerned ministry via PMO. The rationale being that most players import cotton of a specific variety (in this case from the USA), that is for special purpose or not available in India. So hopeful of some concession.

- The manufacturers can still import against advance license scheme, wherein there will be no customs duty, but they will have to forego, the export incentive, so the hit will be marginal.

- History denotes ability to pass on raw material px increase.

7 Likes

Tirupur Exporters Association: Tirupur garment units to down shutters on Monday against steep rise in yarn prices, Retail News, ET Retail This price uptick in yarn with huge inventory buildup during last few qr

should definetly help ACL in short term.

1 Like

My understanding is that price uptick can go either ways. Company focuses on realization per kg. There has been a declining trend in realizations/kg from 2010-2020. It could be because of knitting segment which has a lower realization compared to yarn in % terms. So results are probably dependent on volumes sold as a main factor and stability in realizations compared to 2019 & 2020.

Disc: Invested

2 Likes

Hi @satish58

please share the source of increase in global demand in yarn beyond capacity?

In case you have idea of yarn prices, can you calculate Ambika’s profit from this?

Last AGM, MD said quote “am holding Rs. 330/- worth of yarn corresponding to 1 equity share of Ambika” unquote.

This is the only interesting aspect left in this particular stock.

Disc. : Invested

1 Like

Kindly go to the thread of Commodity and Cyclical Play of this very Value Picker forum.

You will notice a post from Shri, about 2 -3 days ago.

I read it and posted here ( for the benefit of those who may have missed it ) since I am also invested in this share.

1 Like

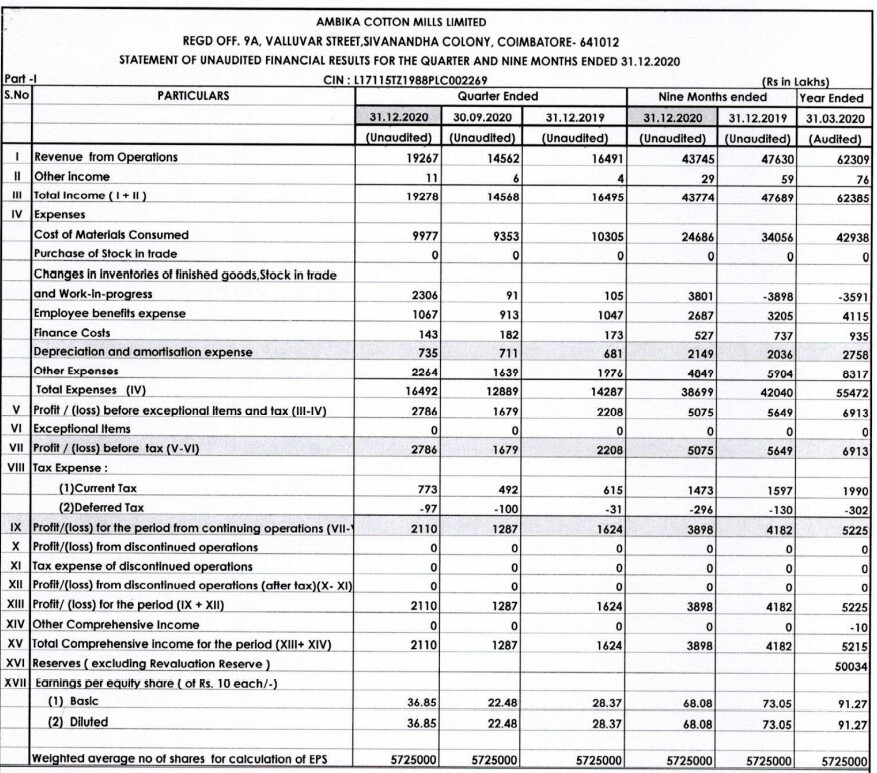

Good set of numbers from YoY perspective and improved margins

Announced Rs 35 per share dividend

4 Likes

Thats Great!

But as we know there’s a limit up to which bottomline / EPS can improve without a growth in topline.

And there are 2 factors that lead to growth in topline - Capacity expansion & Rise in selling price of products/services. Capacity expansion being the stronger among the two.

Are there any news that Ambika is going for capacity addition?

1 Like

Financially they seem very stable, Sales are up.

However sales are flat for many years, is the spike just because of suppressed demand overflow from the Covid shut down?

Also, I see that investment seems to have increased recently. Does anyone have ideas of what this implies?

1 Like

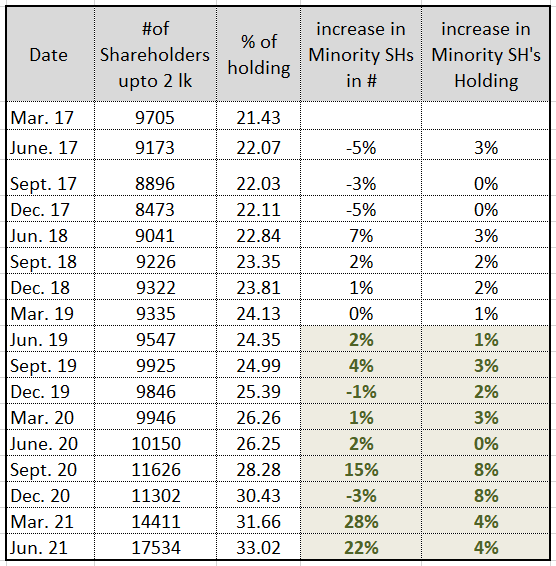

Interesting changes in the shareholding pattern. Are the retail investors getting smarter?

Disc: Invested in family acs and PMS

10 Likes

Of course @ayushmit ,with the help of screener.i can’t imagine investing without screener. We Retail investors are very grateful for screener.Thank you so much

4 Likes

Main difference has come in minority shareholders (upto capital of 2 lakhs) holding. I mapped number of shareholders & change in holding pattern for last 4 years, see below:

There is 69% increase in number of minority shareholders & 32% increase in absolute holding in last 2 years.

If we go by street wisdom, such increase is red flag. While Ambika is defying this & no other red flag has also come up. This makes the company interesting.

Disc.: Holding from lower levels, one of the top 5 holdings in PF

2 Likes

BIG POSITIVE for COTTON TEXTILE

US Senate passes bill to ban all products from China’s Xinjiang Textile Province . This Province produces 80% of China’s cotton and has 35% market share in apparel exports of the global trade. For the Indian Textile Industry its a Huge opportunity.

14 Likes