Has anybody received the dividend?

Has anyone attended AGM ?

Not yet. Hold 250 shares and no dividend received

I attended the AGM. Questions asked by shareholders to PV Chandran & answers-

-Why a steep increase in commission & insurance expenses even when sales decreased compared to last year? Not answered

-300Cr inventory -will inventory level return to 2016 level- the answer was it’s like a pendulum.It won’t remain at one point.It would improve. Due to lockdown, they were not able to move a lot of finished goods.There is premium quality of cotton that their business requires which they need to store at times.He said based on his 20/30 years of experience & considering 3/4% interst rate regime, it was better to invest in cotton than storing money in bank & earn 3/4%.Shareholders shall not be worrie since even after that current ratio is more than 4.

-Capex in 30000 spindle capacity- This was not done even after all approvals as conditions surrounding decision changed .TUFF benefit was taken away some other states giving many more benefits to yarn companies than Tamilnadu .All those things impacted the payback period & ROI of that decision.Instead he thought that there were better returns if he spent money on knitting & that’s what was done. He looks at maximizing profits while comparing different options.

-Why no buyback considering depressed prices - Answer was not very clear to me .He said he knows that shareholders won’t tender the shares .Instead he would try to increase dividend to reward shareholders .Don’t judge the company by share price. Assets are higher than value .

-Future growth plans,Price of Supima cotton he bought, Operating margins of knitting vs spinning ,capacity utilization etc-he did not reveal & opined that revealing such info is a detriment to the interest of the company

Succession plan -His daughter & son in saw have started participating in the company & at a suitable time, he would hand over control.

Stangnant operating margins & decreasing EBITDA since lat few years -He focusses on absolute profit/yield per KG of cotton & not on EBITDA.

other comments -

the next target for the company is to reach 800 cr revenue.

shareholders should not wait till AGM to ask questions. If the question does not reveal business-critical sensitive information, they would be answered.

-30000 Spindle capacity addition will happen eventually since they have all approvals.

-He does not visit the factory floor & instead focusses on managing & administration of business

-They were able to report profit & deliver some orders with much fewer people irrespective of covid related restrictions on movement of people & labour intensive nature of industry

- Export share as % of revenue has increased

-Wind mill investment was 160cr and is now 45% depreciated but still producing good profits.

Request others to add in case i missed something or misinterpreted.

24 Likes

He has explained this two years back here:

3 Likes

Ambika Cotton Mills Limited 32nd Annual General Meeting on 29.09.2020

18 Likes

Bit out dated. Good analysis report - https://marshmallowcapital.files.wordpress.com/2016/04/ambika_blog.pdf

1 Like

I’m holding this stock from Mar 2020. One question I have on promoter group. Currently Chandran Sir two daughters are in board of directors but majority of stake is on Bhavya Chandran only and no stake given to Vidya Jyothi. Can I know if Bhavya Chandran is only successor of Ambika in future. Not sure if its a dumb question I asked.

None of the daughters hold any shares… its in the name of Mrs. C.Bhavani who holds the majority stake. I guess she is Mr. Chandran’s Wife (cannot confirm).

Also Bhavya’s husband Rohan Menon is helping with the business (fabric finishing) and has experience in sales.

1 Like

I found something good about promoters integrity. Here is the link to Sanjay Sir’s article:

2 Likes

They are providing good dividends.

good post

2 Likes

I am big fan of the management form what I have read from prof sanjay bakshi and Dr vijay malik…

While Going through the annual reports, I found below data interesting…

Please correct me if I am moving in the wrong direction with below analysis …

I feel the company is performing good on realization part …

but what I have failed to understand is increase in (work-in-progress + Finished Goods) and decrease in Cotton Yarn sales quantity over the years

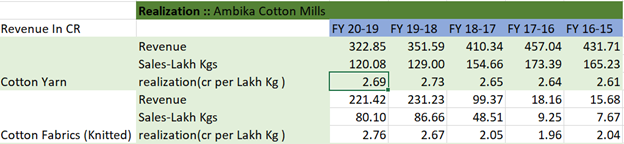

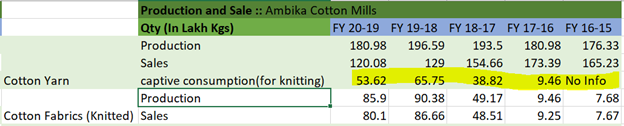

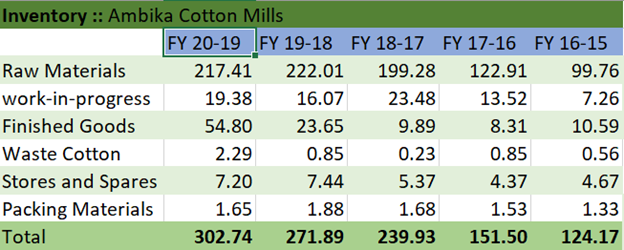

We have 3 screen shots (which needs to be read together as they interwoven)

- Realization :-

- Cotton Yarn stable around 2.7 cr per Lakh Kgs

- Knitted has increased from 1.96 cr per Lakh Kgs to 2.76 cr per Lakh Kgs

- Knitted Realization in line with Cotton Yarn during the year FY 20-19

- Production and Sale

- cotton Yarn sale quantity has been reducing (what could be wrong , being a premium brand one would expect it to hold the ground if not increase )

- Knitted sales have been moving up which argues will for the company

- As per below number , its seems that complete cotton yarn production is being used up for sales (sales + Captive Consumption for knitting)… but the inventory has been increasing (correct me if I missed something here)

- Inventory

- (work-in-progress + Finished Goods) part on inventory has been increasing (even if 20-19 is ignored)

Note : I am not invested and but biased on management

3 Likes

hi

i agree with your point on declining yarn sales (in crores below) -

| Particulars | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 |

|---|---|---|---|---|---|---|---|---|

| Cotton Yarn | 124 | 132 | 153 | 165 | 173 | 155 | 129 | 120 |

| Knitted Fabrics | 1 | 2 | 10 | 8 | 9 | 49 | 87 | 80 |

| Waste Cotton | 48 | 49 | 59 | 67 | 63 | 77 | 80 | 77 |

| Total | 174 | 182 | 223 | 240 | 246 | 280 | 295 | 277 |

i think some amount of this yarn has been diverted to their own knitting division since their capacity in spindles has been static for quite some time. Further, the blend of imported cotton is lower in the knitted fabric, so the realizations are lower.

(their OP margins havent seen a decline too)

FG inventory is something i have been keeping an eye on and the situation has not improved much in the Sep BS also.

If you are okay sharing, what is it that stops you from investing in this idea at this price?

hope the above is helpful.

2 Likes

the company is on my investment radar, but below points are holding me back

- Promotors succession

- decrease in sales of Cotton yarn (being a premium company I assume the company should have had at least constant sales in Quantity )

- does this mean the company is losing customers

- stagnation in the realization

- FG and work in progress increases with decrease in sales quantity

2 and 3 I feel are impacting the growth

Note : I am not invested and but biased on present management

Hi, what is the issue on Promoters succession you are stating in point1. I had read this annual report and it looked like the Promoter has 2 daughters who are both on the board and it looks likely that they will succeed. while I dont see them on the executive positions, so I am assuming they will succeed. Otherwise the rest of the management seemed diverse.

I actually dont understand Cotton yarn markets too well, this is a tail stock in my portfolio (will keep an eye on it and buy on momentum, if at all) .

But, I looked at their P&L and financials , yoy looks like a strong company, there was consistent growth, and everything on the balance sheet and the cashflow looked good too. Receivables , inventory and payables looked fine (dont have it to hand, I just recall my impressions, had done this a couple of weeks ago)

I also liked the fact that their annual report was very bare bones and factual, nothing unnecessarily fancy.

Finally the P/E compared to others in the industry seemed much more lucrative, around 9 compared to late teens for competition, decent ROCE and consistent growth (which looks like it can be funded internally).

so, I liked what I saw and have bought a few shares to hold in tail

1 Like

I came in at the tailend of a conversation, had not seen some of the responses above. Gives me conviction that this is a company worth holding in my portfolio , though small qty

Thanks Guys for quality responses here.

2 Likes

Seems both cotton and yarn prices have moved upwards…ambika has massive cotton inventory. Hope good for them.

5 Likes

1 Like

Ambika Cotton shareholding as on December. Both Value Quest and VLS Finance not showing… so either exited or below 1%.

I read it as good news.

Shareholding Pattern Public ShareHolder

2 Likes