Has the management given any sales target here?

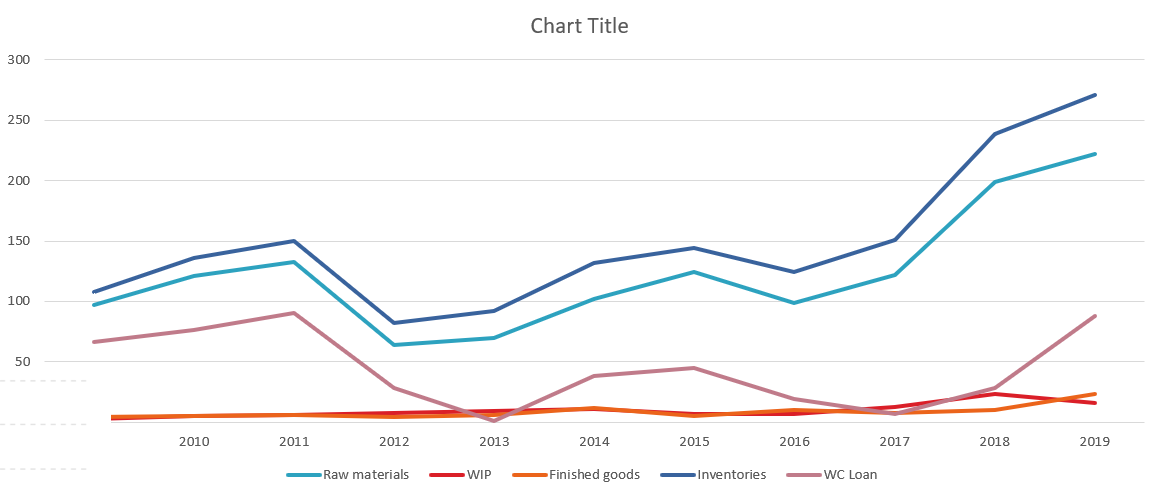

Huge inventory could be a risk specially if the demand is slow. Several countries are in lockdown and the economy as a whole is going to suffer.

Having said that, the average of last 10 (2010-2019) years of sale/inventory ratio is 2.98. And that of 2019 is 2.41. Whereas the same figure for first five years (2010-2014) is 3.20. This means that they had more inventory compared to sales in the first five years compared to the recent years and the ratio for 2019 is even less than the last 10 years average.

Its not that the inventory is gone out of proportion recently. Also, the majority of the inventory is raw cotton and not finished goods. This gives a bit of comfort to me.

I am of the opinion that this might prove as an advantage because they can readily use the raw cotton whenever the demand picks up without needing more WC or facing any delays. Not sure how right or wrong am I on this. There could be downside of this which I might be missing.

But yes, the concern of slowdown is real. It will be a challenge for many businesses to navigate through these tough times. Only time will tell. IMO the sales will definitely suffer.

5 Likes

@Donald, can you please point out how we analyze these things ?

Hi Ricky,

Think there are enough pointers in this Ambika Cotton thread - how we went about establishing exactly that - sustainability of Margins and growth for a business like Ambika Cotton.

Please go through the thread in detail …and you will see enough pointers on how we analysed competition and their margin profiles and why Ambika had a different profile - going on to different buyer profiles…why Ambika is always the first choice of buyers due to superior yarn quality (less breakage and hence higher efficiency for looms), and the like, slow methodical way.

If I remember correctly, we did identify while Margins could be sustainable, Scalability is a problem in this business - due in part also to absence of a proper succession plan in the Management. There were other better scalable businesses with similar earnings profile, and hence I chose to stay away. I did use it for parking spare cash though as it is a good stable business, and good dividend yield acts as a support base.

14 Likes

@Donald Sir, as advised by you, I have gone through the thread (not very minutely though) and in the process I have been able to pick up some newbie like conclusions (just a couple of them only) from the information provided by you and other contributors to this thread. Please go through them and kindly let me know whether my understandings are correct.

There are some ways how competitors can manufacture similar quality yarn. The easier ways include altering the blending of different varieties of cottons.

The “not so easy” ways includes getting rid of machinery capable of producing only the traditional varieties and replacing them with ones that are capable of manufacturing quality that matches with that of Ambika.

Here also , apart from reasons like absence of proper succession, another big problem was restrictions from Regulating authorities and Government 5 years ago but conditions are improving with time as the restrictions are being eased.

BUT, scaling up beyond a point will almost IMMEDIATELY lead to overcapacity (and high exit barriers) as the market is narrow for Ambika ,i.e, not many customers are looking for the fine quality yarn manufactured by Ambika.

1 Like

hello,

ambika cotton seems to be shifting from its yarn business to knitting, any idea what can be the reason behind it other than international competitive market in Yarn business?

secondly 2018 and 2019 cash conversion is poor, since the knitting business is now commanding big part of the company which is new for them, can u throw some lights on what will be the drivers for this?

1 Like

I would like to understand the rationale behind comparing the stock prices of Ambika Cottons and Page industries.

Very good management that takes moderate salary and succession planning in place in the company.

Has the company made any announcement on this front?

Can you provide a source for Ambika being a supplier to page industries?

1 Like

some of thoughts on ACML

Cheap for a reason?

First disclosure – I am long on Ambika Cotton Mills and sitting on a decent paper loss. As the market cap of the company has nearly halved from its peak in Jan 2018

If someone looks at the company today it will look optically cheap

– 7 times earnings

– 75% of book value

– 50% of Annual Sales

with decent first level economics

– Mid teen ROCE

– Sales CAGR / Profit of ~10% for the last few years

– Now No long term debt with a continuous reduction in the last 10 years

– Knowledgeable and experienced promoter

– Selling a product out of commodity (Cotton) and still holding margins

Even the Credit agencies have a good opinion see the extract from the latest one

Highlights in bold mine

ACML enjoys strong pricing flexibility , aided by its premium positioning in the cotton yarn market and its adequate captive power facilities. This had resulted in stable operating margin at 17.7-19.6%, over the four years through fiscal 2019.Going forward, continued focus on operating efficiency to result in strong operating margin of 19.5 percent and cash accrual of around Rs.100 crore.

ACML continues to have a robust financial risk profile; total outside liability to tangible net worth (TOLTNW) is expected to be at 0.4 time over the medium term. Despite management plans to add spindle capacity, the capital structure to remain healthy as it is expected to be funded by internal accruals. Additionally, healthy profitability and prudent working capital management should support the key financial metrics over the medium term

And a cursory look at Annual reports would tell some of the best minds in value investing are invested over the long term

-VALUEQUEST INDIA MOAT FUND LIMITED

-CATAMARAN ADVISORS LLP

So why is Mr. Market pricing Ambika pricing so cheap?

Here is my version of the story

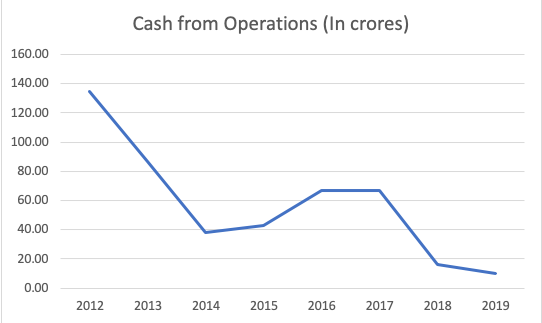

A. The cash generation has slowed down and the market has got a whiff of it

Current and prospective investors have to assess if the phenomenon is temporary or permanent

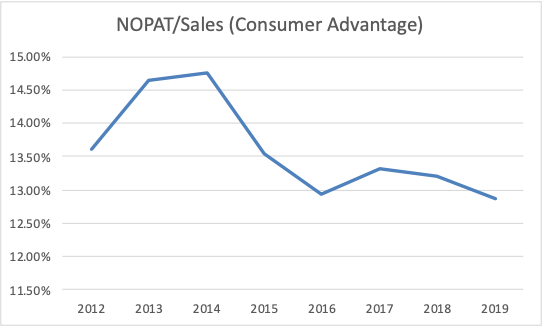

B. Ambika cotton mills as rightly pointed by Crisil has strong pricing flexibility but limited or no pricing power over customers

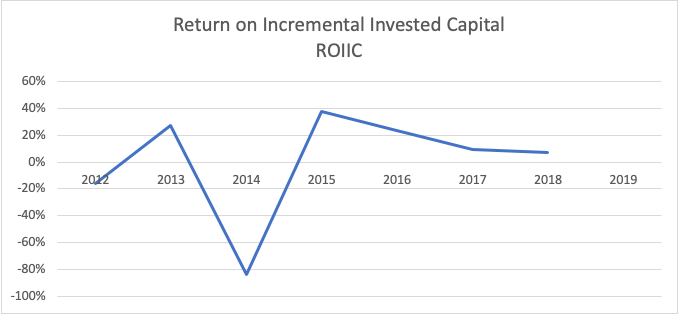

C. While the ROIC is steady ~15% the incremental ROIC has drastically reduced in the last two reported fiscals

In my past experience, I have seen that when companies deleverage some of the incremental returns that leverage gives goes away when they become debt-free. We need to monitor this trend as existing investors

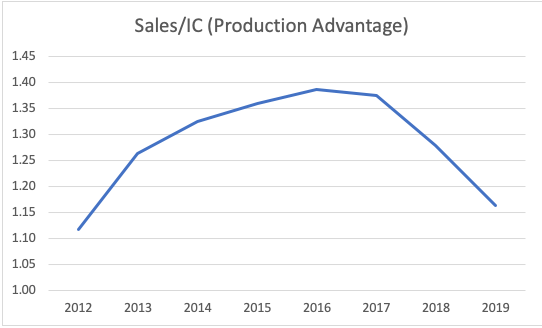

D. Fixed assets are sweating so well between 2012 and 2019 the gross block of fixed assets has reduced by 20% but the top line has increased by 70% WoW! However, using a different lens the Sales / Invested Capital has declined indicating some sluggishness in operations

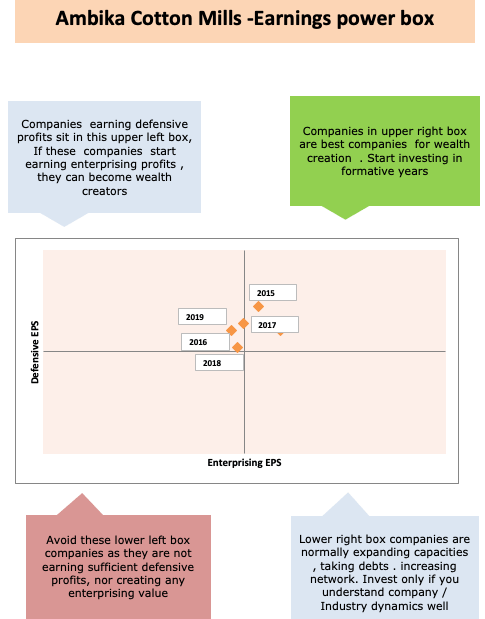

E. When I took position it was in the wealth maximization quadrant of [Earnings Power Box]

The company is expanding capacity as stated with the addition of 30,000 spindles this is funded from accruals and should support topline growth.

However, as investors, unless the company improves on above 5 parameters or takes the pain of communicating to shareholders, Sorry not all of us can attend AGM. The company would find it difficult to sell over its last 5 years Median PE (10) in the near term.

I am though happy with my dividends keep them coming !

22 Likes

- Margins shrank

- Inventories increased

- CFO improved (49.5 cr), mainly because of the difference in Trade Payables compared to the last year

- Dividends lower compared to the last year (I think this is a good sign, though)

- Management says they have enough liquidity and have not availed any moratorium

6 Likes

Nice analysis Vivek! CFO coming down does indeed seem worrisome!

However pls help me understand, why is the market valuing it below the Book value.

Reserves itself is more than 500Cr, while the Enterprise value is less than 470Cr

I see this in Banco Products also… does the market doubt the management integrity is the reason? else why value a profitable company at such low valuation…

2 Likes

The few things which are not in favour of ACML

- Low market cap

- Secular Topline growth is not predicable

- Lack of management effort on communication to investors

- Part of unsexy, Old economy Industry

Also remember market is not expected to be rational otherwise Ben Graham would not have called him Mr Maniac

1 Like

If you look at other players in the Textile Industry on Screener, all of them at trading below their book value. It seems market is not excited about this industry at all at the moment at least.

This news may not have direct impact on Ambika. But overall textile industry is getting impacted due to China India border issue and there is no sign of it going down anytime soon…

1 Like

True. I feel market does not like value stocks, and thats the reason value goes to deep value before buying emerges… eg… look at Hero Moto.

Otherwise market really likes the growth stories and frankly Textile as an industry seems a sunset industry… so not much market interest in these, however from a long term perspective i feel they are good buys…

This thread on ACML is one of the great example of collective efforts in discovery of value. Thank you VP team and members for your great insightful views and hard work done. I got lately interested in ACML when looking for value stocks in current pandemic scenario. Gone through this entire thread in detail at slow pace.

Putting a consolidated list of concerns/issues here which can be thrown light from the persons having more information on the points mentioned. Q1 results are out y’day. But for the obvious reason its not comparable and hence ignoring that.

-

Cash flow from operation improved to 48 Cr for FY20 from low of 12 Cr last year.

-

No update on capacity addition completion. Has 30,000 spindles operational and adding to production? It was targetted to complete by Aug/Sept 2019.

-

Inventory levels are seen obscene at 300+ cr - concern raised many times on VP thread and understand seasonal buying. But isn’t it worth working with low inventory levels as the company was following a couple of years back?

-

More knitting facility addition and using of spinning output for knitting - is the real value addition there? Knitting realization in range of 202 Rs/Kg and Spinning in range of 265 Rs/Kg. Some members tried to respond to this basis lower length yarn being used for knitting etc. But there is no clear understanding given by management on this point.

-

Current Pandemic will have an effect on demand for premium shirting in near future. More WFH culture is going to stay and will have some effect in long run on demand for this discretionary spend.

-

Supima cotton production is a going concern and management said some time back that customers are already asking for “Supima like grades”. Is the quality moat intact for business?

-

Working capital and overall prudent capital management is concern in recent times particularly from FY’20 onwards

-

550 Cr new capex plan? There was update on new investments in TN by TN govt. Not seen any management commentary on this

-

Value Quest ( Prof Sanjay Bakshi) holding down from 4.47% to 4.29% in March’20 qrtr. Further down to 4.27% in Jun’20 qrtr

-

Catamaran (Narayan Murthy trust) has a complete exit from Sep 2019 to Mar 20.

Discl: Interested but not invested

10 Likes

In earlier communication, management indicated some progress being made on 30k spindle addition by Aug19. However, it appears nothing has been materialised so far. Post addition of knitting facility it was expected (as you go up in the value chain) to have higher margins, again things have not gone as expected. Have been invested for many years and communication has always been very limited. But lately this has become even more less.

This time the AGM is going to be an online affair which kind of gives an opportunity to be able to connect with management and get some of the answer ( I hope so  ). Can anyone share their experience of any such e-agm conducted this year or any previous experience of AC mills agm (someone who might have attended).

). Can anyone share their experience of any such e-agm conducted this year or any previous experience of AC mills agm (someone who might have attended).

Without sufficient knowledge it has been very difficult to hold our investment with a huge leap of faith on management. TIA

3 Likes

Recordings of several online AGM’s which have taken place are already available online (e.g. see Orient Refractories thread). The procedure to ask questions during online AGM is detailed in the Notice to the AGM sent to the Stock Exchange. Reports of Ambika’s past AGMs must be there in this thread, please check. I have myself put up one for the 2018 AGM. If you have any specific query, you can write to the company, they do reply though you may have to do a little bit of follow up sometimes. Once I even received a call from Mr. Chandran personally on my mobile to answer a query, though I am just a retail investor.

(Disc.: No longer tracking)

10 Likes

Hi,

Thanks for details provided. Please correct if my understanding is incorrect -

figures from FY20 AR -

Operational quantity :

Cotton Yarn for captive consumption(for knitting) production - 53.62 Lakh kgs Sales-0

Cotton Fabrics (Knitted) Production - 85.90 lakh kgs & sales -80.10 lakh kgs.

Notes to Income statement:

Sale of Products Comprises

Knitted Fabrics 22141.99 lakhs.

Realization = 22141.99/80.10 = 276.

Thanks,

Rohil