Thanks for the response AJ. It helped me understanding the concept. I have a follow up question.

As per your formula Change in inventory = Opening inventory - Closing inventory

So, the change in inventory can be negative only if closing inventory is more than opening inventory.

Instead, don’t you think that the formula should be Closing inventory - Opening inventory?

Let’s put it in a simple way. Let’s say in the beginning of the period, the company has 100 units (Opening Inventory) and at the end of the period, it has 70 units (Closing inventory).

So the change in inventory is 70 - 100 = -30. This means the company has 30 units less than it had at the beginning.

Another question is that I checked the past annual reports and observed that the change in inventory is negative since last 4 years, but the balance sheet is showing the increase in the inventories year on year. How is this inventory getting increased?

company which just stocks up inventory year on year, without consuming anything for production, will not see any impact on P&L (as purchase of materials will be offset by (opening-closing inventory)).

Growing companies inventory level will only increase as they would need to stock cotton for next year requirement. And cotton availability is also seasonal in nature.

thanks for the link…a small article…From what I understood, their business performance is good…But the issue is PE…According to them Ambika stays in mid single digit and occasionally goes up to low double digits on PE…It was trading at 13 PE in 2018 and has come down to 8.56 now…

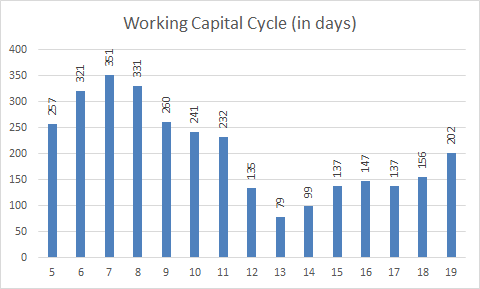

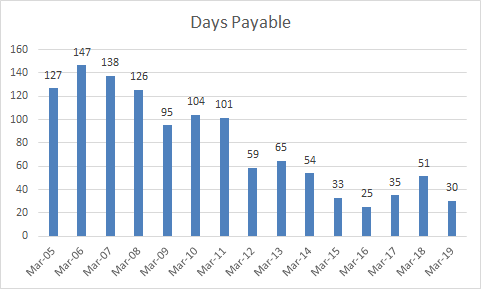

Attached is the working capital cycle for Ambika from 2005-2019

In 2019, the working capital cycle increased to 202 days. In 2019, short term working capital borrowings amounted to ~89 crores. As per the Crisil report they have utilized 18% of the 455 crore working capital limits.

As per my estimates, working capital requirements should be at least 200-250 crores based on the operating cycle. Shouldn’t they have utilized more ? 18% utilization seems a bit less to me to fund the current working capital requirement.

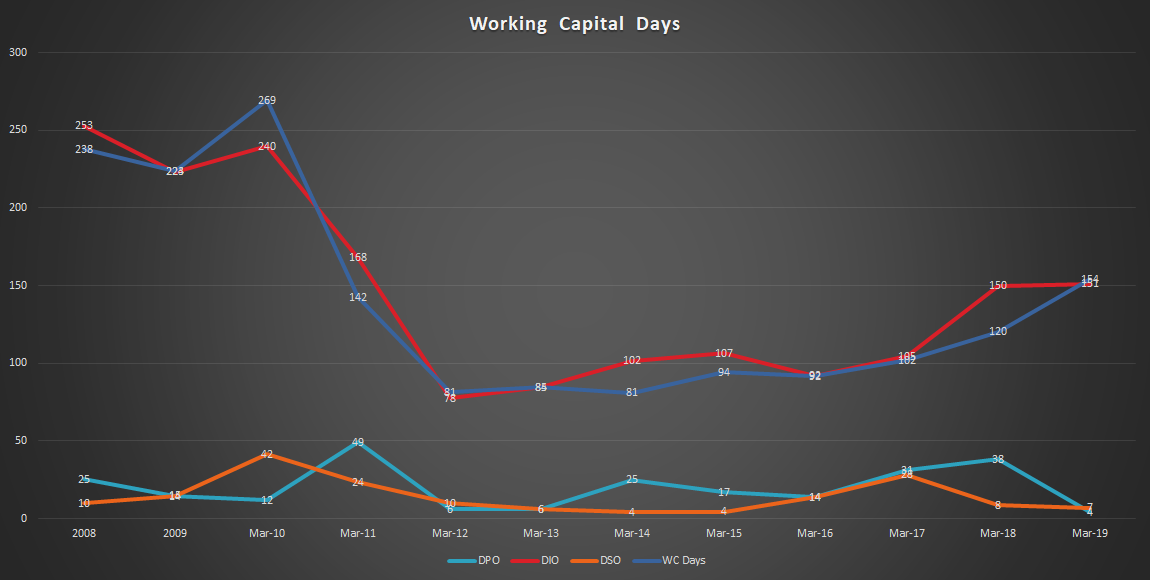

Any idea why the WC intensity reduced in the interim. Could you share the chart with dso, dpo, dio separately. If possible please share the excel also. Could they be funding the WC increase with internal accruals?

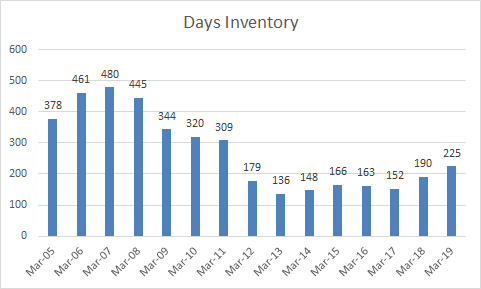

PS: Seems like the reduction in WC in 12-13 was due to reduction in inventory, I am guessing it was due to a fall in cotton prices. But it was an almost 50% fall in total value. It was the same year when OPM fell from 30% to 20%. In 2011 OPM spike from 20% to 30%. I am guessing this is due to FIFO inventory accounting and delay in passing on higher/lower RM prices to the customers.

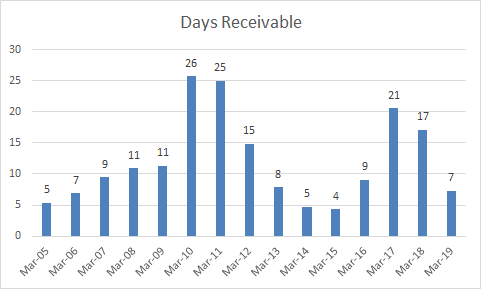

I haven’t studied all the past ARs but does anyone know how they maintain such low DSO. Someone in a blog said they were using receivables discounting. Has anyone found any proof to substantiate this theory? Normally I avoid such companies with wild movements in WC days. But I guess it might be the nature of this industry.

If you look at the B/S from Mar-08, there has been 400 cr odd addition in equity reserves, 260 odd cr reduction in borrowings. 175 cr has gone into funding WC.

The PAT and CFO generation in the past years (10-19) of about 440 cr & 576 cr respectively, which has funded this expansion in B/S. Unfortunately, none of this has lead to a meaningful increase in excess capital for the shareholders in the form of investments or cash on the B/S. Company has paid dividends of 61.5 cr since 2008.

Fixed assets have remained approximately the same since 2008, while sales in the same period have gone 4.2x. That is some crazy utilization of assets. Do they outsource some of their production?

If the same cash flow generation trend continues, we could see some build up FCF from here on as the debt has reduced now but further increase in WC intensity could reduce FCF. Also, I do not know how much further they can grow without investing in PPE in fixed assets. That could also lower FCF.

As far as i can tell, Ambika funded its significant working capital requirements through cash generation (before WC adj) of 123cr + 89cr WC borrowing =212 cr, which is roughly what it needs. I still think 18% utilization is less as the co paid cash interest of 9.42cr and Cash taxes of 29.33 cr adding to ~39 cr. I dont track Ambika as closely as other members of this thread so cant comment on why WC intensity reduced but i think maybe it had something to do with Ambika expanding its speciality cotton yarn capacities. If i remember correctly, it expanded its capacities to manufacture speciality cotton yarn in 2010 or thereabouts in response to better demand before becoming a pure speciality cotton yarn player.

For WC calculation one can refer to my post where i have uploaded the sheet

Annual Report of 2017-18 says “Generally the sales are made against specific orders and to those customers who have long term relationship. Export Sales are backed by irrevocable letter of credits. In respect of domestic sales advance payments are collected before delivery of goods. However exceptions are made based on the credit quality of customers”.

Mr. Chandran mentioned in that year’s AGM (which I attended) that “export bills are discounted with banks and cash is parked in cotton”.

Figures for Export Bills discounted will be available in Annual Report under Contingent Liabilities.

I was trying to understand the knitted fabric segment of company. On a high level, it looks that there are two methods of converting yarn to fabric. Weaving and knitting. Anything woven is not stretchable (imagine your 100% cotton shirt) and knitted is stretchable (like socks or sweater). But the problem with pure cotton knitted fabric is it gets stretched but does not come back to its normal form. Here comes Lycra and Modal. These are synthetic fibre, having very high stretchability. A 10% blend of Lycra to cotton can increase cloth’s stretchability by two times without deformation. Lycra mixed cotton facric is used mainly in underwears, waistbands of sweatpants, lounge wear, or any other types of underwear or bottoms that are designed to be stretchy, sports wear, swim wear. It is noticeable that expenses towards Modal: 10 Cr (2 Cr) and Lycra: 6 Cr (3 Cr) have increased significantly in 2018-19 as compared to past. The story about they selling fabrics to Jockey makes sense as this fabric is used for inner wears. Google search shows the price of Lycra cotton fabric to be Rs 450 per kg. Need to dig further deeper why the lycra cotton produced by Ambika is better than others?

IMO, their focus is selling cotton yarn, not the cotton itself. So lets say if the price of cotton increases suddenly, they will still have enough cushion. I would be really worried if this was finished goods instead of raw cotton.

This quarter result was very pivotal to see how much new capex which was planned to be completed in August would incrementally contribute to the topline and bottom-line.

Despite being fundamentally strong company, the growth has remained a concern. As such there is no mention of any capex completion in the footnote (which usually they do) keeps us doubtful if numbers are post capex or not.

Plus future growth drivers seems to missing currently. This looks like a ideal value stock but definitely not a growth stock in near future in my view.

Disclosure: No transaction in last few months. My views may change and can decide to buy/sell without any notice.

I have observed that the OPM and NPM have remained stable. In fact, improved slightly. When I compared these figures to one of the peers, Nitin Spinners, I have observed that these figures deteriorated.

One simple comparison might not be sufficient, so I will continue to compare the results of other companies that derive most of their revenue from cotton yarn. If the entire industry is under stress and still AC Mills has managed to improve the margins, then it’s a good sign.

I wanted to have more clear communication from the management. But I am of the opinion that the management has always been this way (although I haven’t been following the company for very long). Even the discussion in the annual reports seems to be a copy paste of the previous years. So I wouldn’t worry a lot about the communication part.

I would love to see what is the opinion of the other fellow members. It will only add to the collective wisdom.

Can the Coronavirous spread spell more trouble for Ambika Cotton Mills?

As their premium business of Cotton yarn which mainly gets exported to Asia and Europe can face demand issues.Again the worst affected area is China,which is kindly under lock down.Now the virus has also spread to Europe.

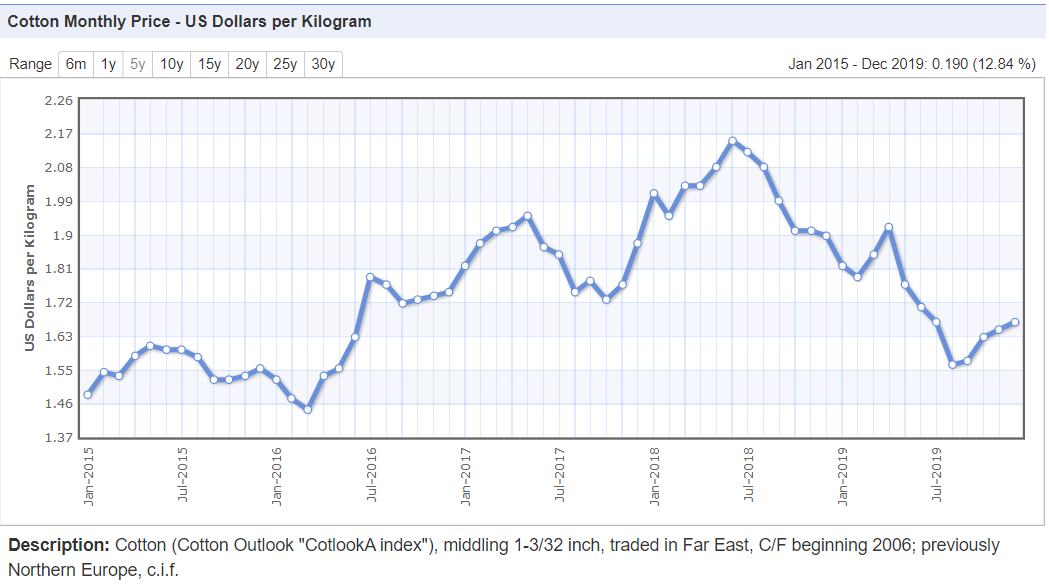

The cotton futures have dropped 17% in last 10 days.

Given that the company carries ~75% of it’s market cap as inventory, will it have to write down inventory?

Less people going out for shopping on account of coronavirus will continue to impact demand and new orders.

Yes yarn prices may not vary but demand may be sluggish.I am having no idea regarding their customers.but I feel demand might be impacted due to cornovirous.