I was wondering if anyone here had any insights on Acetonitrile, it has been a big contributor to revenues and margins for Alkyl and Balaji. Both are also expanding capacities. This clearly has been a BIG tailwind for the stock. Neither company, however, provide much colour on revenues/margins related to Acetonitrile.

Anyone with any insights on demand/supply dynamics and pricing going forward?

So from the analysis data it seems Balaji amines is looking as a better prospect than Alkyl Amines…I am heavily invested in alkyl amines and plan to hold for long term…do u see any long term impact on the stock

As per my limited understanding, Alkyl has a superior business in comparison to Balaji. But Balaji is catching up very fast. Look at the pace with which Balaji is expanding its capacity since 2019.

Alkyl is and will also expand its capacities. But the only risk that I see in Alkyl is that Acetonitrile is driving its topline and margin. Currently, the margins are at a peak level and the company’s valuation is also at peak levels. So if the Acetonitrile party stops then the margins would erode.

Now the margins can drop tomorrow also or can stay elevated for the next 5 years. But I as an investor want to reduce my risk by either making a basket (Alkyl + Balaji) or only playing Balaji.

Just an observation in the latest results, which may be so because the same was not approved by 31st-March: EPS for the Qtr and Year is calculated using old share count (2.04Cr). However, the latest share count is 5.1 Cr.

Hi Aman - Thanks for sharing article. Very well written. However, in your below post, you mentioned that Alkyl has a superior business in comparison to Balaji. Curious to understand why you think so as Balaji’s has better product mix - tilted towards more higher margins – amine derivatives & speciality chemicals and is on an expansion phase?

The management of Alkyl Amines has never misallocated their capital in the past. (A big positive for me).

And the decision of not misallocating capital by not investing in non-core areas and by investing in the core business (Chemical business) has created a lot of wealth for Alkyl’s shareholders.

Fun Fact,

PBT growth of Alkyl Amines since 2010: 26x

PBT growth of Balaji Amines since 2010: 10x

So, I give a lot of emphasis on the capital allocation decisions as that determines your growth and return ratios going ahead.

But, Balaji has also started aggressively investing in the core business since the last 3 years. So good times going ahead for Balaji as well.

what reason - only retail investors valuing it huge… they encash and later enter into lower price… nothing to justify… always the retail investors are last people to buy and lost people to exit.

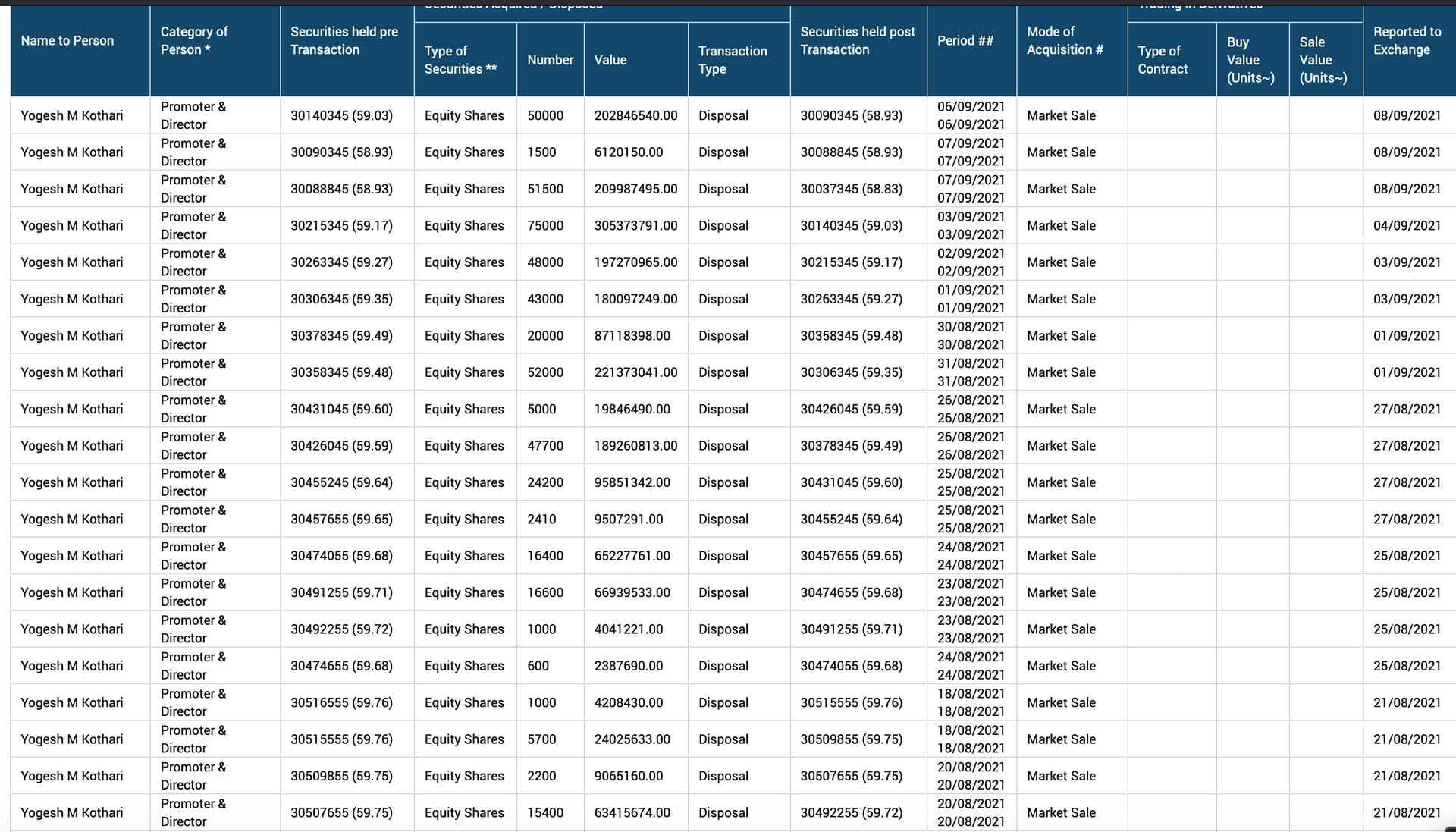

I can only say, as per my knowledge this is the first time since listing 15 years back the promoter has sold ~1% stake in a single quarter. And the frequency of the selling is quite surprising, daily offloading 30-40% of the traded volumes over 3 weeks vs trying to get it over with in few days.

Q2 results will definitely be worth waiting for, if business momentum were to fade, could unravel quickly.

yes its interesting!!! Promotors have never decreased stake before sep’20 quarter. However, Yogesh M kothari has reduced from 59.85 to 58.93 in last 3-4 quarters which is still around 0.92 but this quarter was on higher side which is close to 0.83.