the way alkyl amines is raising - not sure this commodity nature can give such profits in future…

1 Like

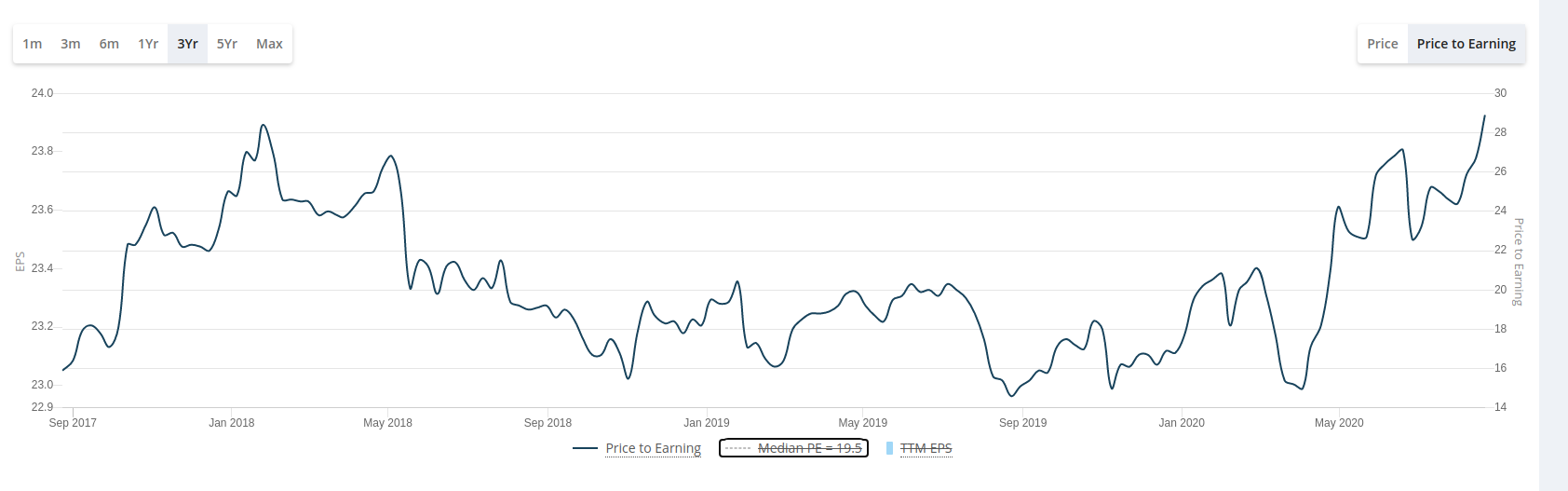

Alkyl Amines P/E is still reasonable. Long term growth in Alkyl Amines has always come from earnings compounding

The P/E of Alkyl Amines was 28.4, the same as it is now in Jan 2018. It fell to 15 in Sep 2019 and Mar 2020 as we see in the chart below

The prices were 662 in Jan 2018 at 28 P/E and 750 odd in Sep 2019 at 15 P/E. So even if you bought in Jan 2018 at 28 P/E, you still made a 15% return in 18 months from earnings compounding. Even in March 2020, when it crashed to 15 P/E the price was still 1174. So if you bought in Jan 2018 at 18 P/E, even during market crash, you almost doubled money.

Though the prices are high, there is a lot of bullishness seen in Alkyl amines stock. That is because the market knows the past history and is expecting more earnings compounding from here. Also stock might get re-rated further as a result.

2 Likes

Folks all the parameters towards this stock seem positive and looks like a multibagger .

Any insight into why no mutual funds arent showing any interest ? Barring Kotak small cap, I don’t see anyone else invested.

2 Likes

Request to provide transcript of Q1 FY 21 Concall or Highlights of Concall of Alkyl Amine.

Thanks,

Hi,

The recent performance of the stock was primarily driven by a great show in one of the key chemicals : Acetonitrile. The chemical sells for around Rs 250 + and the prices have been elevated in the international markets because of strong demand from Pharma. Just wanted to understand roughly how much margins the company is making on the product. Its seems like a fairly simple molecule: CH3CN and I am assuming that the cost of production per kg would not be that high(correct me if I am wrong). My concern is that if there is a mean reversion of margins , the stock can take a hit.

Would love to hear from you guys.

1 Like

@Max8645 Alkyl has been planning to expand Acetonitrile capacity while Balaji is struggling to keep up with the pace. That’s why it trades richly - Acetonitrile is highly margin accretive. And Alkyl has been developing this product since 3 years while Balaji is still unable to increase its capacity. Which makes me think the chemistry is not so simple and this is a moat for Alkyl.

3 Likes

Hi,

This video discusses the moat behind Alkyl Amines, probably helpful. Not a promotion or anything.

https://www.youtube.com/watch?v=YY4sRbQs85k

Disc: Invested.

Regards,

Anto

4 Likes

I think both Balaji and Alkyl are planning to expand their Acetonitrle capacity by 9K and 15k MTPA respectively. Alkyl’s capacity would come online in FY21; Not sure about Balaji’s capacity. Current

Acetonitrile capacity for both is roughly the same- 9k for Balaji and 10k for Alkyl. Despite that it seems that Alkyl has been a bigger beneficiary of the firm Acetonitrile prices. Do you think thats the case?

1 Like

Amines market in India is Oligopoly in nature. Balaji has come out with good Q2 FY21 result. Amines & Specialty revenue for Q2FY21 has increased from 225 Cr to 280 Cr,Amines segment PBT has increased from 43 Cr in Q2FY20 to 73 Cr in Q2FY21 . Balaji is going for a new Methylamines plant with capacity of 40K to 50K MT/year in MIDC Solapur. Balaji’s current Methylamines capacity is 45K MT/Year. Alkyl’s Methylamines current capacity at 30K MT/Year. additional capacity of 15K MT of Alkyl’s Methylamines will come online by Oct-2020.

3 Likes

Good article from Marcellus on Alkyl and Amines industry

3 Likes

Alkyl Amines Q2FY21 Concall Notes

I will be dividing this into Business, Risk & Management

Business

-Demand has been quite good from Pharma, and other segments where Amines are used have started catching up.

-Margin expansion: Benign RM prices and finished goods prices have been really good.This is what led to margin expansion coupled with high Acetonitrile prices sustaining.

Capex

-Projects for Acetonitrile expansion to be commissioned in Q3FY21, for which we are spending close to 170-180 crores, some of the Amine Derivatives Projects have been commissioned.

-Methylamines debottlenecking from 30,000MTPA to 45,000MTPA has been commissioned. Only took less than 10 crores of capex.

-This year capex spend will be closer to 150 crores and next year capex will be closer to 200 crores.

-We have an Ethylamines project on the drawing board, today we have 25,000 MTPA of capacity across 2 plants. This project will have higher capacity than the capacity that we have today. (likely timeline: 18-20 months from now). This plant will come at Patalganga.

-Lot of imports are coming from China and Europe of Ehtylamines, we are also putting up a new plant shortly. Hardy any imports come for Methylamines which is more hazardous and bulky.

-We will be investing in other debottlenecking exercises.

-We are increasingly importing our needs for Ethyl Alcohol, as government has given incentives for Ethanol, which makes the domestic prices of Ethyl Alcohol unviable for us. Some new products are also in the pipeline.

-Apart from acetonitrile, prices are inline for all the other chemicals that we make.

-Balaji Amines and Deepak Novochem are the other players in Acetonitrile. There are no entry barriers, but it took us a lot of time to get the product quality right, it is not so easy as well.One major shutdown globally.

-PLI scheme will impact us indirectly in a positive way as the end-user of Amines will start expanding.

-Overall volume growth was at 18%, rest came from value growth (24% was the topline growth). See this trend of 10-15% growth sustaining and can even post higher growth.

-Some of our Amines which are used in Anti-Viral APIs are experiencing strong growth, in terms of total usage more than 25-30 molecules will be using Amines. Nearly the entire Indian Pharma industry is our customer today.

-Product mix: Derivatives are 25-30%, Amines 50% and Speciality chemicals at 20%

Management

-We expect to add 1000 crores to our topline in next 3-4 years, once all are projects are ramped up.

-Market leaders in Ethylamines, Acetonitrile, DMA HCL,hydroxylamine(only 2 players in the world) and Isopropylamine. Another product where we have majority of the market share is isopropyl ethylexyl.

-5 types of Amines categories:

- Aliphatic Amines, in which we operate, include Ethylamines, Methyl Amines, etc. Has 200-250 end usages and use Alcohol and Ammonia.

2.Ethylene Amines, where we are not getting into unlike Balaji and Diamines. This uses EDC and Ammonia. (More volatile: reason Cited)

3)Alkanol Amines, this uses Propylene oxide and Ammonia.

4)Fatty Amines.

5)Speciality Amines.

There are 1000s of derivatives and Europe and USA are the largest markets, but India and China are growing faster.

Risks

-The biggest risk is the Acetonitrile prices, its foolish to think that these prices will remain at elevated levels of Rs270 per kg. Going forward these will comedown, don’t know when that happens.

-Second, the biggest risk I see today is that the Co is trading at decade high Valuations with Decade high margins, these stories often end in a painful way.

-Thirdly, Balaji Amines has also announced a 50,000MTPA capacity for Methylamines and they are doubling their Acetonitrile Capacity. What happens when Acetonitrile prices come off?

My views: When I initially bought the stock it was trading at low teens multiple, such is the unpredictability of investing, the bottom line number which I thought would come in 4-5 years, came in 18 months due to the hike in Acetonitrile prices. Selling is all about pattern recognition, Personally no longer invested in this story due to decade high margins and decade high multiples.

Not a recommendation to buy or sell.

18 Likes

Alkyl Amines Q2FY21 Earnings Con call Transcript

I find myself thinking hard about this business, it has been a better than expected ride so far.

Assuming the growth plans go as per plan and the company does scale up to 2,000 Cr revenue 4 years from now, what EBITDA margin can the company do at this scale? The last couple of quarters have been abnormally high on the margin front, 30%+ EBITDA cannot be sustained over the long term. The 10 year history tells us that 20% EBITDA is doable given the industry structure and the niche products the company is into.

Working with a 25% EBITDA margin (which is still a bit generous) assumption at a revenue of 2,000 Cr, the business can churn out EBITDA of around 500 Cr. Setting aside 45-50 Cr for depreciation and assuming the interest cost is zero, PBT should be in the range of 450 Cr at this scale. Effectively a PAT of ~330 Cr assuming everything goes well.

Now what multiple would the market give for a specialty chemicals business that can grow volumes in the range of 15-16% over the long term? Let us go with 30 TTM PE, which is 20% lower than the current multiple.

Assuming all of these assumptions play out, at 2,000 Cr revenue 3-4 years out, the market in it’s right mind should value this business close to 10,000 Cr. This right now trades at ~8,200 Cr.

This is one of the few businesses that has good medium term growth visibility but this is no top quality consumer business where the range of outcomes is limited. In chemicals, a large plant coming onstream over the next 2 years can completely change the dynamics of pricing and as a result, the margin profile.

I have always believed that every business in India (barring those 15-20 exceptional businesses) becomes an easy sell beyond a threshold price, what is that price for this business?

Not coming to any conclusions yet but the above summarizes my current line of thinking about this business.

Disclosure: Invested for self and other investors, I am a SEBI registered IA. No transactions over the past 30 days.

16 Likes

Personally, I am convinced on the management’s ability to come up with new products. For instance, Alkyl was the first to come up with acetonitrile which has led to great realisations and margins. Further, management’s capital allocation has been stellar - they only pick projects with strong incremental RoCE. So ultimately, there is always a risk that acetonitrile market will saturate and hence margins will take a hit. But Amines is a huge industry. Global Amines market is USD 4 Bn (INR 30,000 Cr). Indian companies contribute INR 3,000 Cr to this market. So over a decade, there is a chance for India based players to capture greater share of the market.

Regarding valuations, the end users are majorly based in pharma followed by agrochemicals. Pharma sector itself is going through tailwinds and offers predictiblity in revenue growth which could support a PE of 30-35. Operating leverage could compensate for loss in margins due to fall in acetonitrile prices. Factors such as high quality of earnings (Alkyl has a better EBITDA to OCF conversion over a 5 year horizon compared even to some of the best in class large cap players like Asian Paints or HUL), capex funding through primarily internal accruals and laser sharp focus on execution (eg: management chooses not to invest into ethylene amines) need to be considered as a larger picture. Key man risk exists as I haven’t seen the promoter’s son attend any of the conference calls, but the core engineering team seems to be talented. Price might have run ahead of fundamentals in the short term, but in the long term, this is a quality midcap in the making.

Disc: invested

5 Likes

Playing the role of devil’s advocate here:

-

Are we extrapolating a cyclical uptick? Why weren’t the volumes growing at double digits between 2014-2017?

-

Given the Acetonitrile realizations, don’t you think margin compression can be severe going forward? Or are we extrapolating this is the new normal?

-

Decade high margins+Decade high Valuations. How could this double ,if an investor with a 5 year view invests at current Valuations. One cyclical downturn or margin correction, these Valuations might not sustain.

Disclosure: Sold recently. Buying was done at 700. Not a coffee can type company, when margins expand due to commodity prices. At these Valuations, just doesn’t seem that risk/reward is favourable. Assuming an investor is willing to make 15% Cagr, likely Mcap by end of 5years should be at 16-18k crore. Given the sales guidance of 2k crore. Can it trade at 8-9times price/sales multiple. Seems too much of a longshot at these Valuations.

13 Likes

Good view points. But the current valuations seem to have priced in lot of positives.

But given this is a oligopolistic industry with some entry barriers both AA and BA (Balaji amines) should continue to see low double digit growth for next 3-5 yrs in my view.

BA as compared to AA trades at lower valuations. Although BA has its own issues (capital allocation, capex, etc). Don’t you think having a basket of both companies would be better, especially given that AA trades a higher levels than BA.

Thanks

Disc. Invested in BA and tracking AA.

1 Like

@Worldlywiseinvestors I have seen the earnings call transcript during 2014-17 period and volume growth has always been there for the firm - 10-15% on average. However pricing is dependent on a lot of factors like supply from Korea, Taiwan, Europe and of course China. They export to Europe and Euro depreciation led to fall in value of revenue.

I think volume growth of 15-20% should be sustained for the next 5 years. But pricing could be tricky as Acetonitrile prices are at record highs. If acryonitrile production picks up, then acetonitrile should see a drop in prices.

3 Likes

Gentlemen @zygo23554 and @Worldlywiseinvestors both of you have raised all the valid points. Very good discussion. I’m invested in Alkyl Amine and plan to hold it. Although there is very little left to write after both of you, still some points…

- Market is giving higher multiple to Alkyl than Balaji, owing to previous 4 years performance, so expect it to retain an edge over Balaji in terms of valuations.

- Top Speciality chemicals companies are commanding PE of more than 40, take that into account

- Management’s guidance of achieving 2000 cr revenue is in 3-4 years, since management’s are generally conservative in giving their growth guidance, I’m expecting their revenue target to be achieved before 4 years

- Do expect launch of some new speciality products by the company

- Pharma tailwinds will keep demand of amine and amine derivatives products high in coming years, expect some margin rise there to compensate loss in acetonitrile margin

- Going forward percentage of acetonitrile in their overall revenue mix is expected to go down

6 Likes

@Experts - I just observed that the Trade receivables and Payables are increasing YoY. Any reason for the same?

A revenues increase means transactions aka receivables & payables. If a corresponding increase in reserves & better cash flows would mean this increase is normal business growth. Keep an eye out for huge write-offs, unhealthy liabilities will show-up eventually.

2 Likes