Either FY22 guidance will be met by better performance in rest of year or guidance to be revised downwards, concall will be key for outlook, mkt has taken a pessimistic view solely based on US Generics ignoring mutiple triggers that are looking healthy ( non usa Generics growing well, Injectable facility coming online soon/ F3 plant, domestic branded doing very well, API segment growth looking decent).

Could only attend part of the Concall. Posting what I noted down:

Volumes were fine in the USA but pricing pressure due to competition led to degrowth. This was expected… But not to the extent we ve seen

Guidance of 50 eps for FY21 has gone out the window. No fresh guidance given. Expect next 1 to 2 quarters to be bad too

kharkadi situation is still up in the air. Management is hoping the USFDA gives an update next few months.

Gross margins are lower and this should be the expected margins for sometime. The previous high 70s weren’t sustainable.

The market was right to punish the stock… But I think the punishment was a bit too much than what was deserved. While the degrowth in the USA was harsh… It was expected to happen at some point. The India branded business growth was fantastic… Finally contributing more than the USA. Personally I’m hoping the next few years India continues outperforming and slowly we get stability through it. Api and ex usa contributing meaningfully too so dependance on the USA slowly but surely will go away. Note that Management is bullish long term on the USA but things look very murky in the short term.

Disc: started rebuilding my position slowly today

it has reached 52 week low today

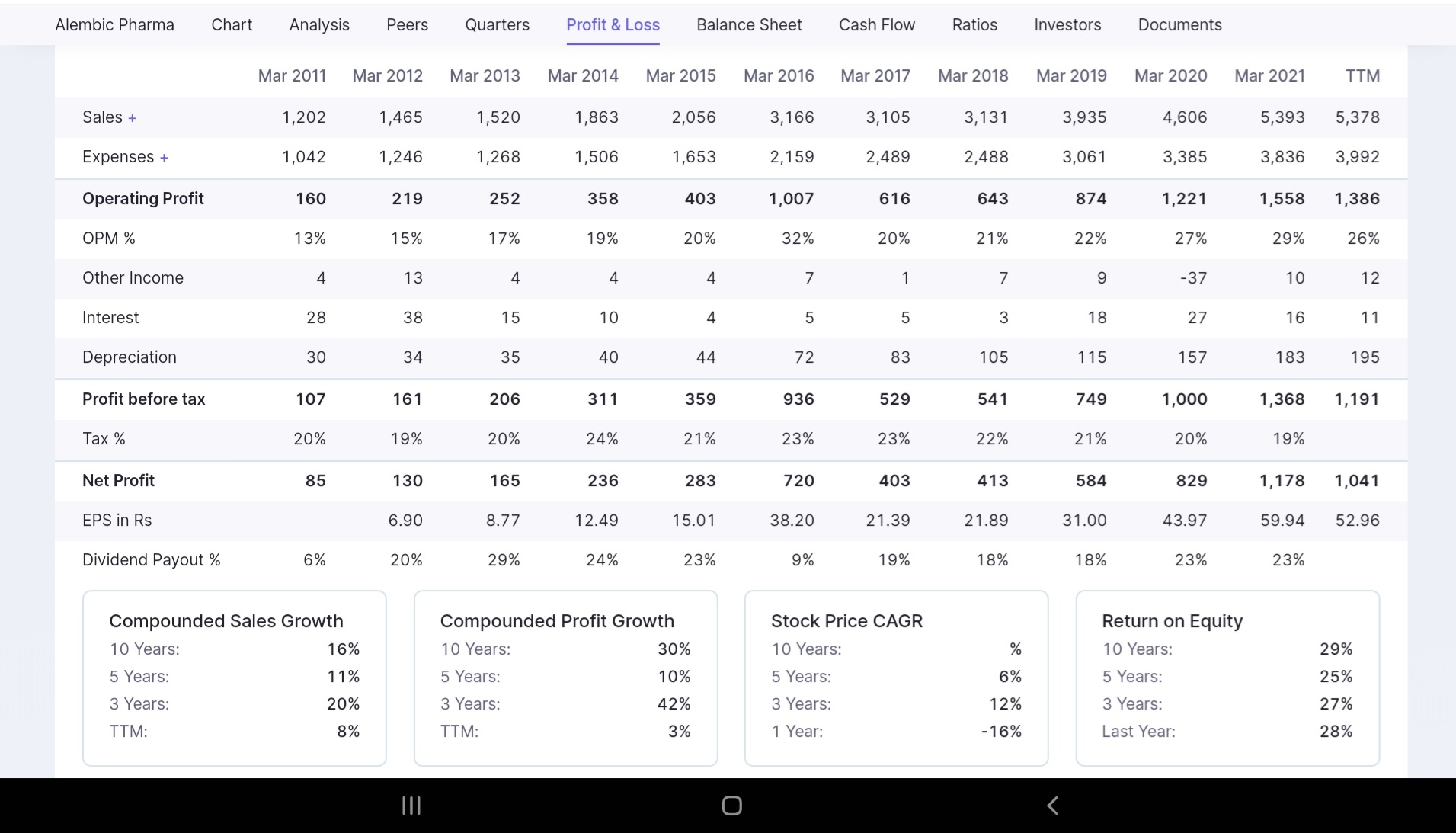

market cap : ₹ 17,883 Cr. TTM top line is 5,378 i.e available at 3x the valuations are attarctive but has some negatives

highest ever inventory to the tune of 1450 crs

highest ever liabilities

proceeded from shares under cash from financing activity 734 crs

FII reduced their exposure in the counter

it seems that it will take a bit long time to recover … but how long i think when the number support the operations as the management itself is sounding that the next 3 4 quarters will have subdue performance one must relook their rational behind the numbers .

disc ; no position in the counter . i am not any sebi approved analyst this is not any recommendation to buy sell or hold

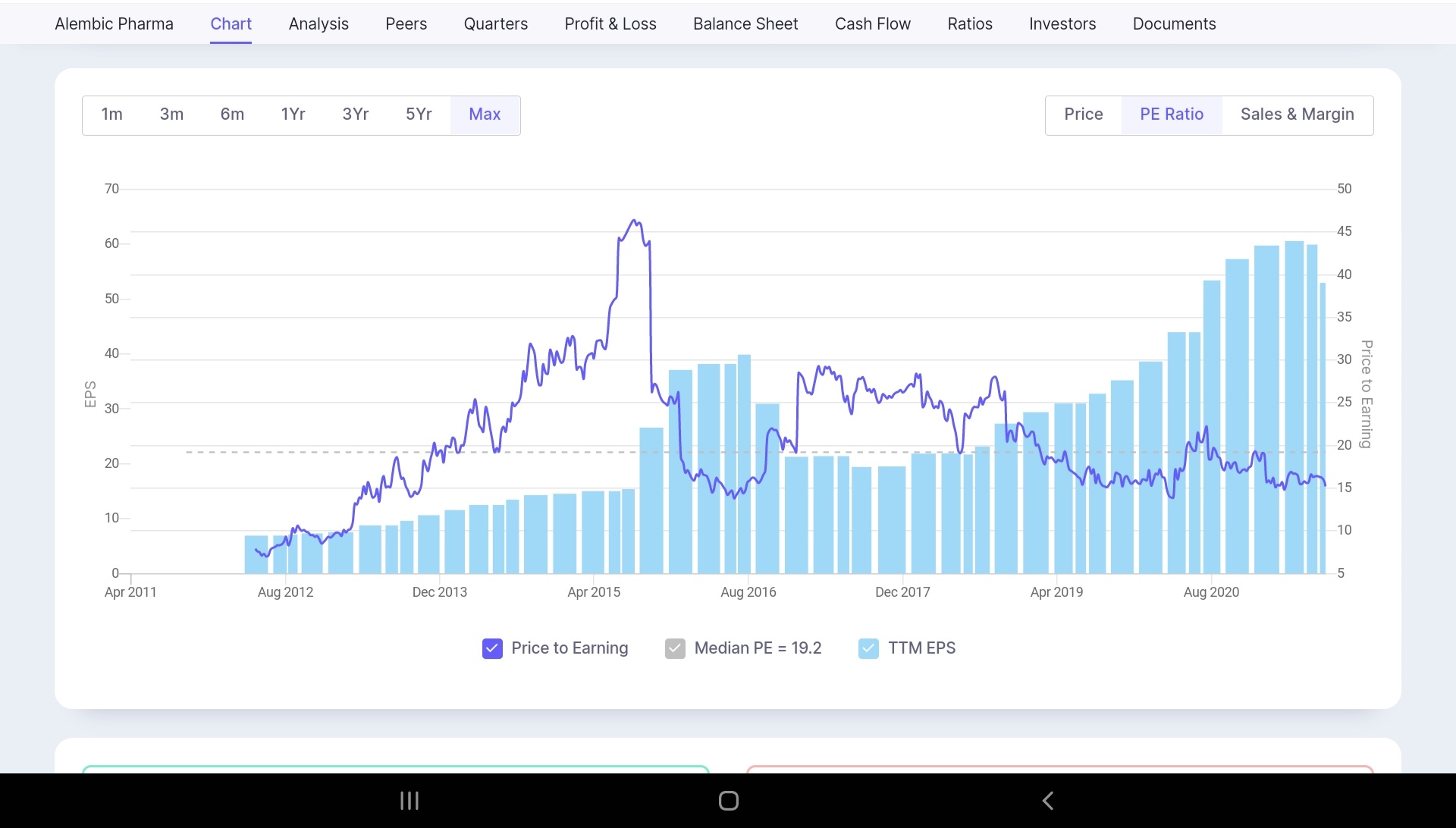

Alembic is now very close to July 15 high price of 770, at that point it was approx 2100 cr revenue, 300 cr profit and 16 EPS) whereas TTM numbers now are 5400 cr revenue, 1000 cr profit and 50+ EPS. As we can seen 3X on all parameters but at same price…almost no return over 5 year periods.

While EPS has consistently grown, from mid 2015 till date there is a derating broadly speaking.

One can also argue about hardly any participation in last one year+ post covid rally as well( 660 in Feb 20 to 800 now), of course had visited 1100+ briefly but we are where we are after 1 qtr of underperformance.

While today’s market reaction could be knee jerk reaction- fueled by pessimism on con call for near future and other Pharma biggies missing expectations.

However a long term look at Op Margins as above suggest sustainable margins in the range of 20% vicinity barring few exceptions such as FY16 and 20/21.

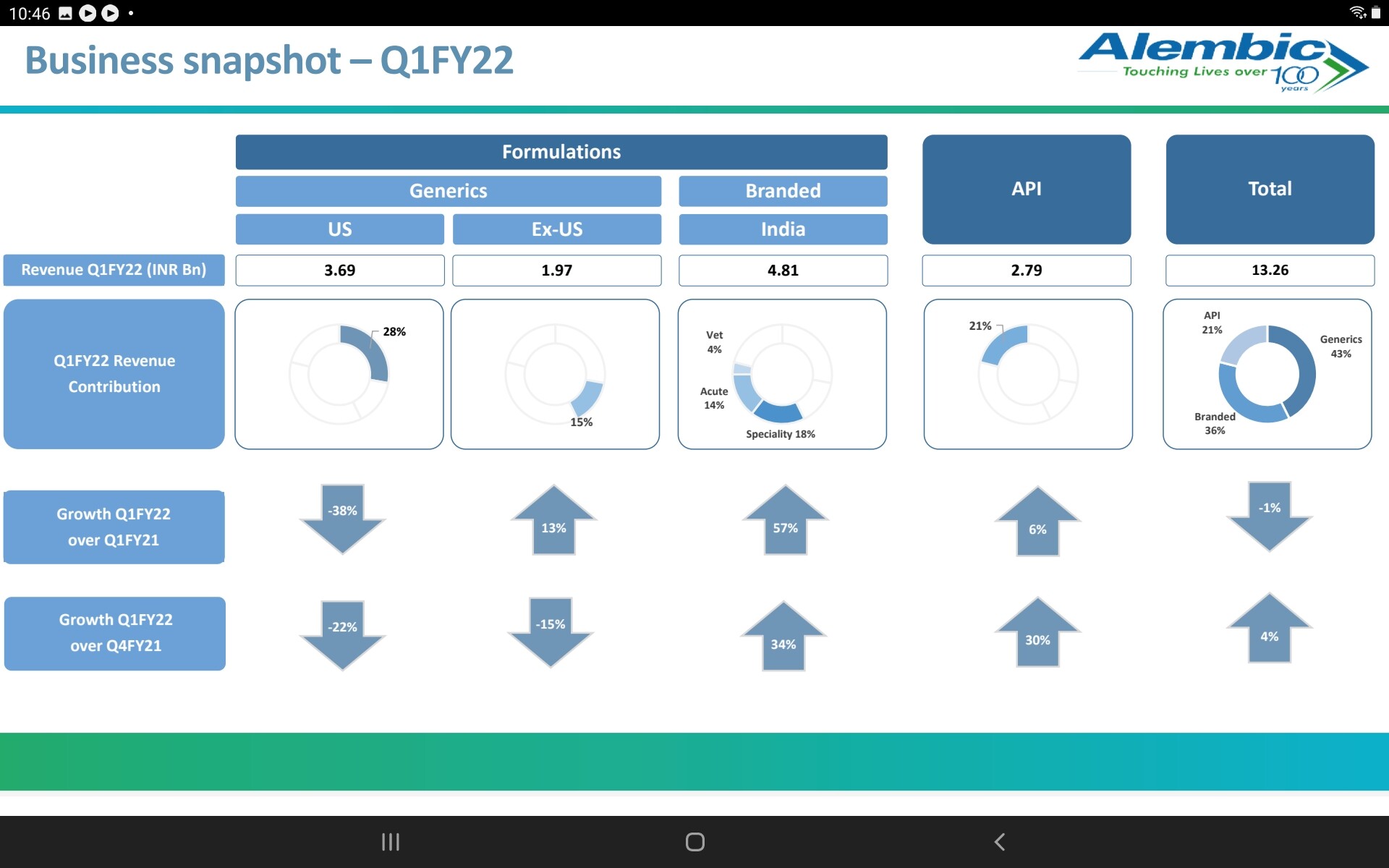

Q1 22 - $15M type degrowth in Generics revenue is well compensated by growth in India and API biz etc but Op Margins take a hit from 27% to 18%, that is less than 8% of revenue mix change causes such magnitude of impact on Margins causing it to drop by almost 30%.

Combining facts such as long term( 10+ years) perception of market valuation ( PE ratio de rating) inspite of wonderful metrics on return ratio , growth on all fronts etc.

Collapse of Margins inspite of Sartans a known aspect, management commentary sounding everything but in control.

Will market ever give a good valuation even if they were to stabilize in 1-2 qtrs on Generics biz and deliver $400m in 2024 in Generics as they mentioned in call?

Invested - plan to trim down to tracking on bounce backs.

Nice analysis and I observed all of these points as well.

On this one, can we compare Alembic’s US generic business with Dr Reddy’s US generic business? Now I don’t understand pharma that well so happy for more knowledgeable guys to come in here.

However, if I look at DRL’s business - it’s EBITDA margins are highly comparable ie. a high teens to low twenties EBITDA margin business and it’s avg P/E for last 10+ years has been 25x for 10% sales and 7% PAT CAGR (maybe some lumpiness in reported earnings where as OCF compounding is way better around 15%).

Now if these 2 are actually comparable - Alembic being a third of DRL’S size has grown way faster at 15%+ topline and 25%+ bottomline CAGR in last 10 years. Just purely going on historical business performance, excellent return ratios, good dividend payout, low debt and good management execution - there is no way this business deserves to be at 17-18x multiples compared to DRL unless it’s performance falls off a cliff going forward.

This fulfills all the characteristics of a Coffee Can business in my view.

Disc: Invested with good exposure in last few days

Markets hate unpredictability. The generics space is proving to be highly unpredictable with booms due to timing of andas for when patents end and busts when competition inevitably comes in… Making it difficult to valuate them. Ideally, going forward alembic needs to setup a predictable base from which they can then go boom or bust with sartan type opportunities. Once the India branded business reaches a bigger scale(if q1 isn’t a one off then arguably that could be the case very soon) and the api business continues gaining traction next few years then we could see a potential re rating since there would be a more stable base to jump from and the downside could be better predicted. Based on management comments I suspect they understand this too now and I’m hoping we go in this direction. Right now the play is on the hope that alembic will find the next sartan type opportunity… As these opportunities end their margins can potentially take a huge hit along with profitability as has played out. And it’s being

valuated for this unpredictable business and rightly so. That being said, They keep all their chess pieces in play with their huge R&D spends and anda filings so I have no doubt that they’ll find another sartanesque opportunity over the next few years especially with the amount of patents due to end within 2 years. So once their sticky branded business gains enough scale then we could see a re rating in my worthless opinion :)… The kharkadi plant delay has added to this reverse lollapalooza(along with the crash in nifty pharma) . Until then in the short to medium term the rising interest costs and potential crashing of yearly eps to under 40 will require a Few quarters of patience and trust in what I consider to be blue chip management(this period will really put this thesis of blue chip to the test though). In the long term a company like this shouldn’t be at under 3x sales. But in the short term considering there are better opportunities around even in the pharma space(for eg pharmova is even more undervalued and the likes of Laurus are well placed for growth even at higher valuations) I can see (or rather I hope so I can continue accumulating ) there is a further de rating especially since the management themselves are uncertain about the short to medium term and market perception of a company’s business model takes a long while to recover from a shock like this.

Disc: added and continue to add in this fall. There will be opportunity cost and a chance of further pain here so I’m staggering my buying for the next few quarters.

A great management and gruesome business = still underperformance.

Opportunity cost for Generics heavy player is visible over last decade and trend is again visible in this Quarter numbers. Trend doesn’t seem reversible in near future as per mgmt own admissions.

Technical charts can always help us on loading back again when performance improves, why block money at this point rather than deploying elsewhere in same sector or others - I have been guilty of same in past, cutting losses quickly has helped out on improving our investment own RoCE

Again each has own investment style and rhythm, flowing with least friction is the art we learn over time.

I believe Alembic results followed by Dr. Reddy’s results are the signs that tide is turning away from the pharma sector. Pharma sector had fabulous run for last 2 years which makes everyone forget sector performance from 2016-19 where USFDA issues and price competition for US facing pharma companies and price caps for domestic pharma companies were the issues depressing profitability of all pharma stocks. Post covid lockdowns, USFDA is back in action and we have started seeing inspections and warning letters rising around the world. If so, smart money will move quickly to the undervalued sector

This is true for the whole Pharma sector,especially the generic companies.Back in 2015,there was this narrative that these are recession proof,high margin,capital efficient businesses.Indian companies have a clear competitive advantage,regulatory standards provide a ‘moat’ and keep away competitors and so on.However,the market had completely overlooked the strong pricing environment for all generic companies.They had a dream run starting from 2009 that lasted 5-6 years with volumes & approvals also moving at a good clip.Even the currency was a tailwind.This had led to a gold rush among Indian cos.,everyone wanted a piece of the pie.I remember Sun Pharma used to make 40%+ EBITDA on a consistent basis & was valued at 40x P/E.As the rally progressed,the smaller companies started being valued with Sun Pharma as the standard,leading to large ‘discounts’ vs. the largest company.A small company named Nectar Life had also expressed it’s desire to enter the US generics market.Stock surged 20% straightaway on huge volumes.With this piling competition,at some point the pricing collapsed for all companies with very few Pharma cos. having enough F2F,Para-IV type molecules to offset the damage.The margins crashed and so did the multiples.So I highly doubt generic companies will ever get the same valuations.The volumes are non-cyclical,but pricing isn’t and moves abruptly just like a normal commodity.A generic drug’s pricing is pure demand & supply.

APL is however a quality company that has proven it’s mettle time & time again.They know their strengths & have an excellent compliance track record.So,the company will recover from this too.However,earnings uncertainty is a big issue & markets will punish it the way it has.Unless some blockbuster approvals come in,stock will continue to meander imho.

If you like Alembic Pharma business and prefer margin of safety, you may consider buying Alembic limited the parent company of Alembic pharma.

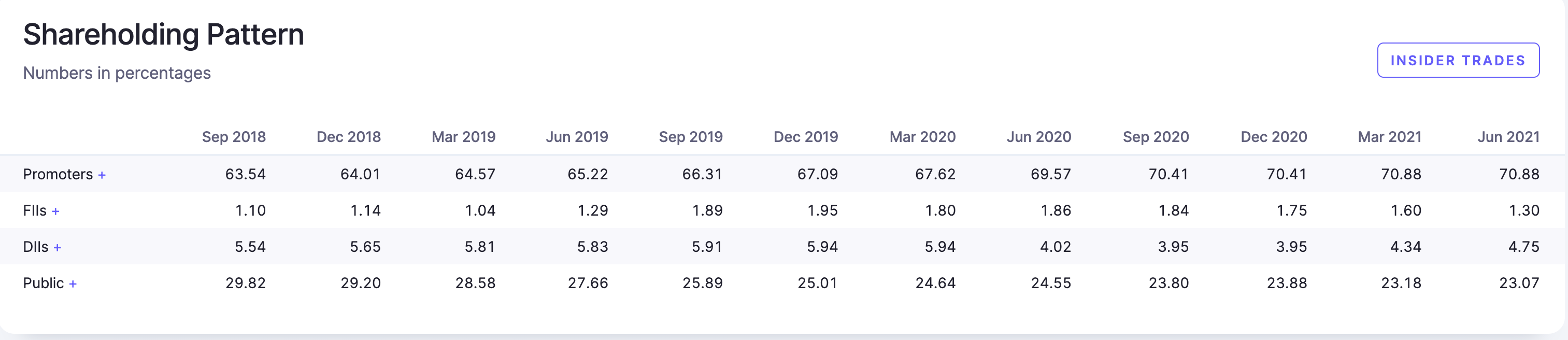

The parent company holds 28.4% of Alembic Pharma.

On August 9, 2021, the market cap of Alembic Pharma is 15,184cr (stock price is 772rs).

28.4% of 15,184cr is 4312cr.

The market cap of Alembic Limited is 2,936cr (stock price is 114rs). The discount is 46% (1376cr) and plus gets the parent company’s real estate business and API business for free. Both real estate and API businesses are profitable.

The promoters increased their holding of the parent company from 67.62% (March 2020) to 70.88% (June 2021)

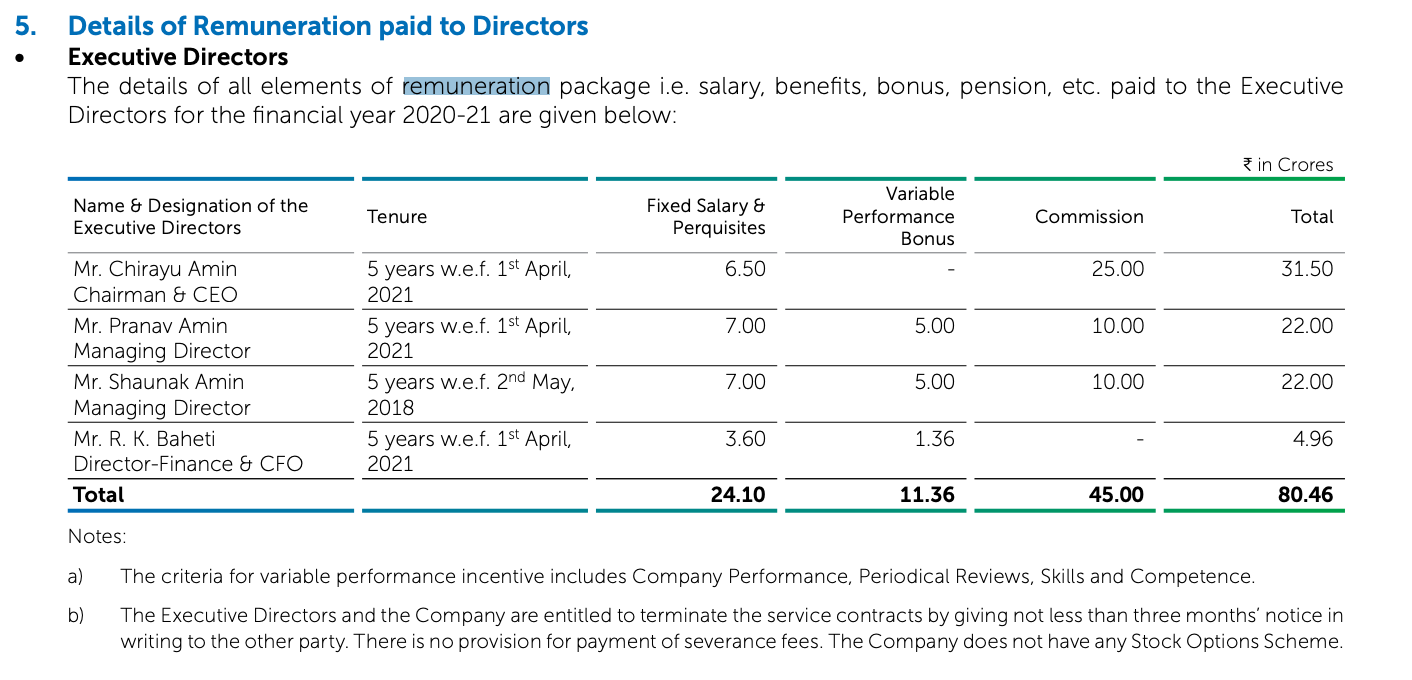

Question: Alembic paid 80cr to the Executive directors (Chairmen, both MDs, and CFO) as salary, bonus, and commission in FY20-21. I wonder Is it above or average pharma industry standard?

FY21

Employee Benefits Expense: 1051cr

Net profit: 1178cr

CFO salary is professional salary and market driven. Promoters are just taking whatever they want. It is definitely very high. e.g. In a company where higher management is professionals typically MD salary would never be 4.5 times CFO salary.

Selexipag Tablets, 200 mcg, 400 mcg, 600 mcg, 800 mcg, 1,400 mcg, and 1,600

mcg have an estimated market size of US$ 461 million for twelve months ending

September 2021 according to IQVIA.

Alembic has received year to date (YTD) 15 approvals (11 final approvals and 4

tentative approvals) and a cumulative total of 154 ANDA 'approvals (134 final

approvals arid 20 tentative approvals) from USFDA.

For more details:

This year approvals is almost 10% of total ANDA approvals of 154.

Alembic Pharmaceuticals Limited (Alembic) has announced today that it has made .a

strategic investment in RIGlmmune Inc., a biopharmaceutical research company cofounded by two prominent Yale University professors.

Company has acquired preferred stock in RIGlmmune amounting to a 19.97% postmoney stake in the first closing of the series seed round that was completed recently. (Not mentioned valuation of acquisition yet)

Hello, I am new to investing.

I needed help in understanding the large amount of CWIP that is building up in the balance-sheet of the company. There is more than 2,000 cr. of capital work in progress as per the latest balance-sheet.

Does this represent new manufacturing units, Or Capitalization of research expenses? If this is capitalization of research expenses, could company be inflating the profitability?

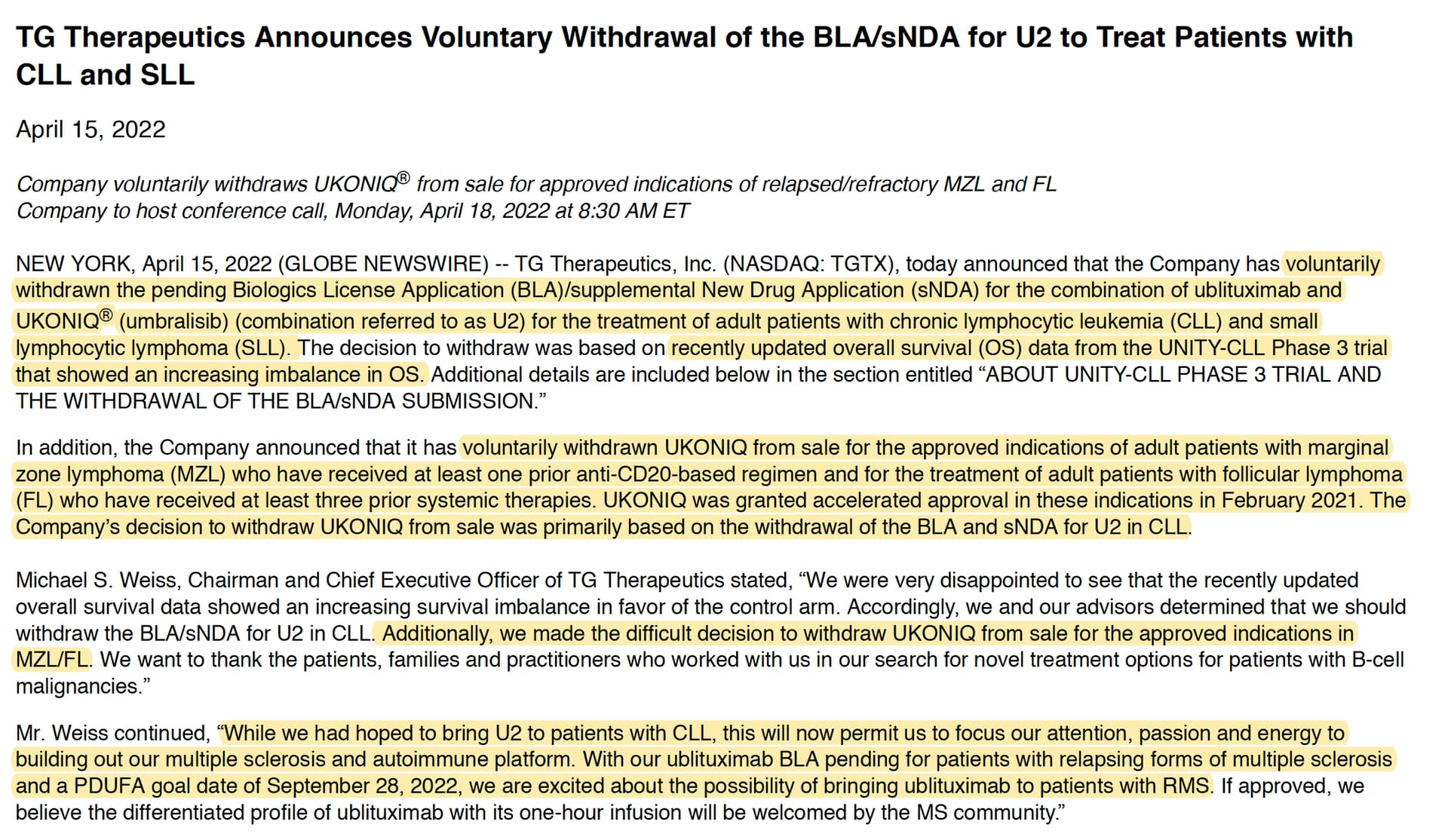

TG Therapeutics voluntarily withdraws its UKONIQ approval for applications in marginal zone lymphoma (MZL) and follicular lymphoma (FL) that it had received from US FDA in February 2021. This is based on recent data for Unity Phase 3 trials. Although, the product never accounted for large part of Alembic’s revenues as it was in build up phase, its a little sad as this was the first NDA approval for a drug developed by Indian scientists. The detailed press release is below.

Disclosure: Invested (position size here, bought few shares in last 30 days)

Updates: As I read through the press release, it seems that the initial Phase 3 study had passed the primary endpoint. However, there was a secondary endpoint which wasn’t met initially, company claims that this was because the trials were not designed to collect that data properly. FDA wanted to be sure that the secondary end point was also met and they called a committee to judge the scientific appropriatness of the same while judging a subsequent BLA/sNDA application by TG Therapeutics. For this new application, there was another trial which was organized where the secondary data point was properly collected. As results of the secondary data point was analyzed, company realized that the therapy doesn’t do what its supposed to do. Thus, they withdrew their new application and along with retracting their older approval. Note: I might have oversimplified this explanation, this is what the press release kind of says. Although, I am not a biology/drug expert, so please read the press release for yourself at the link above.