Results are very good. WC has improved too. Post QIP,balance sheet looks healthy as ever. Stock has consolidated and been rangebound since last quarter results,should do well from here.

Here is my 830 word summary of the 10,000 word Q2FY21 concall:

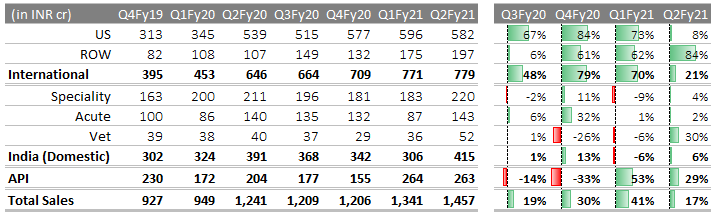

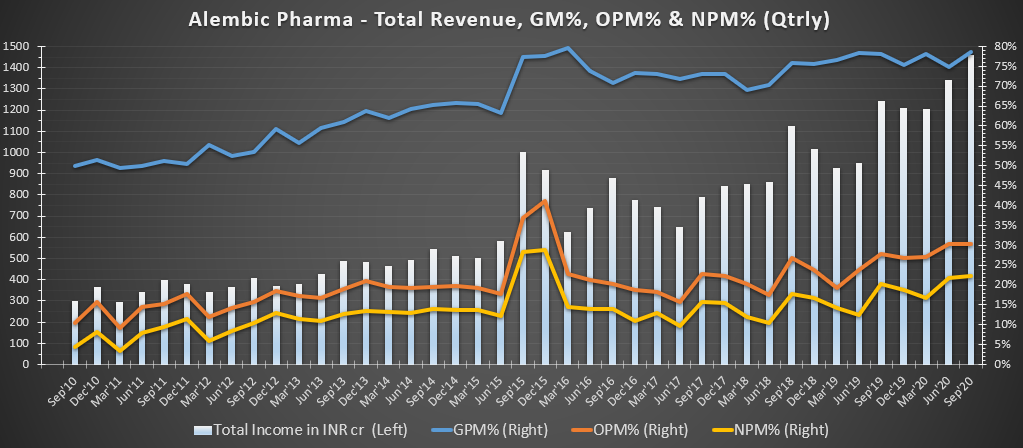

[Financials]: Revenue grew by 17% to INR 1,457 crores. EBITDA grew by 33% to INR 455 crores. EBITDA margin is 31%. Profit before tax went up by 36% to INR 406 crores, and profit after tax went up by 35% to INR 333 crores.

[EPS]: The EPS for Q2-FY21 is INR 17.24 on an expanded capital. The previous corresponding quarter, that is September '19, EPS was 13.06 on the old capital.

[Capex]: CapEx for the quarter is 168 cr. H1 is 311 cr. Cumulative CapEx for CWIP projects including the pre-operatives is 1825 cr.

[Debt]: Gross borrowing is 600 cr vs 1439 cr in June 2020. Company has 273 cr of cash. Net debt equity is at 0.07

[Outperformer Molecule]: Outperformer for the quarter was azithromycin solid. Saw significant growth in numbers along with a strong market share. We did our groundwork in Q1 in anticipation of this happening in Q2. We see this trend continuing for the next 2 quarters at least.

[Degrowth]: The only area which is still a concern for us is the cough and cold market, along with the pediatric segment. The market for these products are seeing negative growth for the quarter as for IMS data. We’ll start returning to outperforming the market as soon as the market reaches into some kind of neutral growth category.

[R&D]: R&D expenditure was 185 cr, which is 13% of sales.

[US portfolio]: Filed 7 ANDAs during Q2 & cumulative ANDAs at 198. We received 6 approvals, including 4 tentative approvals. We cumulatively have 131 ANDA approvals, including 18 tentative approvals. We launched 3 products during the quarter, and we plan to launch 5 to 6 more in the Q3.

[TG therapeutics]: TG Therapeutics had announced in the past acceptance of this NDA by the U.S. FDA for the treatment of patients with MZM, which is marginal zone lymphoma and follicular lymphoma. They’re targeting the regulatory submission for the CLL indication, which is chronic lymphocytic leukemia, or umbralisib, along with their proprietary product rituximab in early '21.

[Growth break-up]: International formulations business grew by 21% to INR 779 crores for the quarter. The U.S. generics grew by 8% to INR 582 crores for the quarter (despite large base). Ex USA Generics continued its robust growth and grew by 84% to INR 197 crores for the quarter. API business had a good Q2 as and grew by 29% to INR 263 crores for Q2.

[Onetime guidance on EPS]: We are guiding to an EPS of INR 60 per share in the current financial year. As regards to the next financial year, FY '22, there will be an additional expense of INR 450 crores hitting the P&L on account of the new formulation plants. In spite of this increase in operational expense, we expect an EPS of INR 50 per share in FY '22. Objective of giving this guidance is to allay the fears of some investors that how much business is sustainable

[USFDA inspection]: Company has requested USFDA to come for pre-approval inspection of new facilities, but is unsure how they’d come due to Covid. Jarod OSD facility that we’re waiting FDA to do either online or a physical audit.

[Flat past API Growth]: API growth was only 3% CAGR in the last 4 years. We were focussing on completing OSD and injectables plants. Will now focus on API. Good prospect for Growth.

[Sartans]: Due to Alembic having a large PF of 15 Sartan molecules, no meaningful price erosion, although new entrants keep coming.

[Injectables]: And next year onwards is when we’ll see injectables launches coming from the new facilities.

[ROW market]: ROW business, as you know, it’s only there are a few markets that we focus on, Europe, Australia, Canada, and we work through our partners in most of these markets.

[US market Future revenue]: Not a guidance per se, but with the new capacities and & capabilities coming up, we can envision going to $400 million to $500 million kind of revenue in the next 3 years

[Receivables and Inventory]: Were high in march due to some collection issues for US business. We had collected everything by April. Once the new plants start getting operational, the launch inventory starts getting built up.

[FY22 costs]: Will incur operating expenses of 450cr in FY22 for new plants. There is no capitalization of any cost that will happen in FY22.

[Domestic market future growth]: We’ll grow in line with the market growth.

[New Capabilities]: Our business is pretty much only generics right now. Reason for the new investments is to get new capabilities: injectables, derm, onco, onco injectables. That’s where we’re seeing growth from FY '22, '23, '24, a lot of this will come from that, from the newer capabilities. There are some areas that we definitely don’t want to get into that is biosimilars and investment required is very high at this stage. Biologics as well. But we’re evaluating other opportunities.

Overall the management commentary was positive. Already, the EPS for H1 is 33rs. I wonder why they have given the guidance even though one time as rs 60 for this full year ( 27 for H2) and rs 50 for next year. Is the management expecting a degrowth for next 6 quarters or eps getting adjusted due to equity dilution by QIP. Kindly correct me what I am missing.

Surprised that Azithromycin is outperforming. Heard somewhere that infections common cold/cough/flu are lower on account of lockdowns and people not getting out of home.

Overall great results. Significant reduction in debt despite the capex.

Hi Prasobh, could you please back this up with data or a source/link that mentions this?

Azithromycin is a commonly used broad-specturm antibiotic. These are prescribed not only as a direct treatment but also as supportive treatment for a lot of diseases that spread in India during the monsoon months. Antibiotics are also given to COVID19 patients who have lung involvement.

Unless the management gave a clear reason stating ‘people not getting out of their homes’ as a cause, or there is additional data pointing towards this, it would be presumptuous to make this claim.

Either way, azithromycin is a major product for Alembic in India so its outperformance is welcome.

Hi Nimish, saw this info in a malayalam daily quoting chemist/pharma dealers. It may be that the newspaper article is not based on any data. I ll try to find out the link and share.

Edit : links are below. Apologies that One is in Malayalam.

This stock is beyond my comprehension. There are consistent good results back to back but the price is coming down (even after consolidation of 3-4 months).

Not sure if market thinks that the growth numbers are one-off and not sustainable.

One reason for market’s worry could be this comment on their concall.

We are guiding to an EPS of INR 60 per share in the current financial year. As regards to the next financial year, FY '22, there will be an additional expense of INR 450 crores hitting the P&L on account of the new formulation plants. In spite of this increase in operational expense, we expect an EPS of INR 50 per share in FY '22.

Effectively they are saying next year’s profit’s will be lower than this year’s, which some market participants don’t like.

If stock prices rose the next day after good results and commentary every single time there’s be no investors … just people waiting for good results from companies who would buy and benefit from a days rise of 5 percent and then sell. This has been discussed in the granules thread too. Please have a look there (everything apart from asm applies here too). Day to day has too many moving parts. The guidance of 50 eps next year was to actually prove that this is not one off and sustainable and that growth can carry on for a few more years including FY 23 and 24 with increasing capex without too much compromise on eps in FY 22(even with 450 crores of additional expense which is more than half PAT of FY 20 they’ll maintain an eps of 50 and improve returns for FY 23 and FY 24 where the baseline eps will be higher and can then go higher with new capex contribution). So if anything as an investor I’ve gained confidence for a few more years instead of thinking of it as a FY 22 only bet. Patience prevails. Please flag and delete my post if needed. Cheers

Disc: invested. Not a sebi advisor. Could be wrong.

Can anyone who has listened to the concall please explain - has the mgt said any thing about how much topline revenues are they going to generate during Fy 22 from new plant (i.e. the year during which they would book 450 crore).

Also whether this expense of 450 crore will be the new base for this new plant or this is a one time expenditure kind of a thing?

New base. Maintenance (operating expenses) for new plants. My understanding is that the revenue would ramp-up slowly over time as the new capacities and capabilities are utilized more and more. As far as I understand it, no guidance on revenue in this concall. Operating leverage could kick in FY23 onwards imo.

I have talked to some market veterans, who has expressed displeasure and surprise on the amount of capex the company keeps doing. This is according to them is why a lot of people are staying away from the stock.

Guidance (barring unforeseen circumstances): FY21 EPS to be ~| 60 per share; FY22 EPS to be ~| 50 per share with additional | 450 crore expenses hitting the P&L from new plants; FY23 revenue growth to pick up with capacities coming online

o Growth ahead from injectables, dermatology, oncology and oncology injectables

For Q2FY21, the company filed seven ANDAs, received six final approvals and launched three products in the US

Total 75 products launched till date in the US (excluding seven with partner label). The company expects to launch 5+ products in the US in Q3FY21

Cumulative ANDAs filed were at 198. Cumulative approved: 131 (including 18 tentative approvals)

Gross debt was at ~| 600 crore (vs. | 1439 crore in Q1FY21), cash ~| 273 crore; net D:E – 0.07

R&D during the quarter was at | 185 crore (13% of sales)

Capex for Q2FY21 was | 168 crore. Cumulative capex was at~| 1825 crore

Aleor investment was at | 742 crore (cumulative); investment in thequarter - | 40 crore

Sartans saw some price erosion as a new player entered, which wasoffset by new opportunities, launches

Strong RoW growth – Due to addressing of serialisation issues inEurope

US: 15-20 new launches per year, going ahead, to drive growth

Domestic – strong traction in Azithromycin oral solids

o continued impact on liquids portfolio (antibiotics + cough & cold)

API growth – mainly due to market share gain in Azithromycin and other opportunities

o two DMFs filed in Q1FY21

Decline in other expenditure was on account of lower