Alembic Pharmaceuticals announces its joint venture, Aleor Dermaceuticals receives . USFDA Final Approval for Desonide Lotion, 0.05%.

Alembic Pharmaceuticals Limited (Alembic) today announced that its joint venture Aleor

Dermaceuticals Limited (Aleor) has received final approval from the US Food & Drug

Administration (USFDA) for its Abbreviated New Drug Application (ANDA) for Desonide

Lotion, 0.05%. The approved ANDA is therapeutically equivalent to the reference listed drug

product (RLD), DesOwen® Lotion, 0.05% of Galderma Laboratories LP. Desonide Lotion is

low to medium potency corticosteroids indicated for the relief of the Inflammatory and pruritic

manifestations of corticosteroid responsive dermatoses.

Desonide Lotion, 0.05% has an estimated market size of US$ 7 million for twelve months

ending June 2020 according to IQVIA.

Alembic has a cumulative total of 129 ANDA approvals (113 final approvals and 16 tentative

approvals) from USFDA.

Uday education trust is a charitable organisation which runs some schools in Baroda. It held 0.54% stake in alembic pharma as per June 2020 data from screener. After latest round of selling by the said trust, its holding stands reduced to 0.41%. I think the usual explanation is that it is a charitable organisation and might be in need of funds to deploy in its stated line of charity.

Also promoters have been buying shares in alembic. Quantum of buy in Alembic in August and September has been 16.22 cr. and quantum of sell in Alembic Pharma in August and September has been 20.55 cr. Probably promoters are smarter at capital allocation than most of us.

I find from screener data that current promoter holdings in Alembic Pharma is 73% and promoter holdings in Alembic is 69%.

If I read correctly, are they trying to switch few % from Alembic Pharma to Alembic to take advantage of the cheap valuation of Alembic !

The selling was by “UDAY EDUCATION SOCIETY” and possibly for their charitable purposes. This link also shows that Uday education’s most liquid holding is Alembic Pharma (so it was not possible for them to sell Alembic shares as far as I understand). My 2c are that I think it is difficult to read too much into this and tie this to the buying of Alembic shares by Nirayu.

Alembic gains 31% in Sept on stake purchase by promoters…

Even if I were the promoters, perhaps I would have also done the same thing when Alembic was available at 6 P/E. Market never gave a good valuation to Alembic since it was accompanied with real estate business.

While the promoters sold few percentages in Alembic Pharma , but still they are holding more than 70% stake in Alembic Pharma … it is among very few indian Pharma stocks where promoter holding is more than 70%.

But in no way the fundamentals of Alembic Pharma is affected. The stock is under pressure perhaps due to the stake sale in Alembic Pharma…but I expect considering fundamentals , it will recover fast . Market has given an opportunity to buy this stock .

Discl: Invested. Continue to add, seeing the product portfolio and future business prospects .

I may be biased and may be wrong in my assessment… please do your own assessment before investing

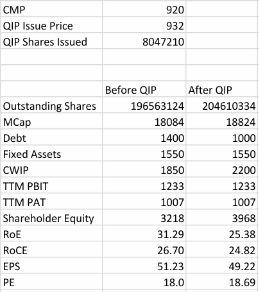

I did a quick calculation about the impact of recent QIP on the profitability ratios for Alembic Pharma.

Considering:

1.management commentary that out of 750Cr, 400Cr to be used for debt reduction and 350Cr to be used for further capex,

2. assuming that all the QIP money will translate to either reduction in debt or assets / WIP,

There is no significant impact to the PE, RoCE. These is a moderate impact to the RoE however this still remains to one of the high range RoE. I am hoping that the ~30% ROE should return soon provided the company continues to make growth in profits as it is expected at least in near future.

Please correct me if I am wrong, If I look at the screener data and compare with other Generic Pharma Companies , I find Alembic Pharma stands out on all return ratio’s even post QIP and post few % stake sale by promoter.

(1) Highest ROCE of 26.7 in the Generic pharma pack

(2) Highest ROE of 24.8 in the Generic pharma pack

(3) CAGR topline @14% during last 3 years is the highest in the Generic pharma industry

(4) CAGR bottom line @28% during last 3 years is the highest in generic pharma industry (IPCA could be an exception)

(5) If I take a longer 5 years duration, there is no one to beat Alembic Pharma in top line and bottom line CAGR % of 17 and 25… It indicates the track record of the company during this highly challenging period for pharma industry.

(6) Promoter holding is again 2nd highest @70% Cadilla has 74% promoter holding. Highest promoter holding indicates confidence of promoter in the company.

(8) It gives me a lot of comfort to invest at this P/E level which is again the most attractive among all generic Pharma stocks, though I have many other pharma stocks in my portfolio.

Discl: invested…may be biased…I may be wrong in my assessment… this is not a buy / sell recommendation . Please do your own assessment before investment.

There was a question regarding alembic not moving as much as other stocks. I think the key to remain calm is to focus on company’s business rather than stock prices.

If we focus on the fundamentals of the company, I cannot find anything that seems drastically wrong. The overhang of selling due to Uday trust and even Bhailal Amin trust will be a temporary headwind.

Business wise, my scuttlebutt tells me that the sartans traction continues. I also asked an employee about why alembic continues to enjoy the sartans traction since so long.

The reasons were:

Alembic is present in all 15-16 products (different permutations of products and combinations with other molecules like diuretics or other antihypertensives etc. ) No other company present in US has such presence. So making a sales pitch to the US pharmacy chains becomes easy for the US front end.

Alembic is vertically integrated in all most of these sartans and hence it is possible to supply a specific drug or its combination at short notice with a lot of certainty. This again provides a lot of muscle to the US front end while dealing with pharmacies.

Another molecule doing well for them over past few months has been famotidine. This again was a piece of luck with being prepared. Ranitidine was banned in US by USFDA in March 2020. Famotidine is a like to like replacement and alembic enjoys a strong presence in the molecule right from approval to manufacturing prowess.

Stock price movements in short to medium term are random things with a lot of factors affecting it. But over longer term it is a slave to earnings. So one has to have focus on earnings and quality of earnings. Sometimes its the darkest before dawn.

@hitesh2710 I was going through past few annual reports of Alembic. It is growing revenue in international generics(mainly US market) and international generics is 54% of revenue now. But it is not growing in domestic branded business(31% of total revenue) and API. Infact API revenue degrew from 771cr(2019) to 708 cr(2020). I see company has almost completed 2000cr of CAPEX and is one of the largest spender on R&D. Also they have plan for 25-30 filing every year. My question is that they are primarily dependent on US generic market only and their API and domestic branded business is not growing. Do you see it as a risk?

Along with annual reports, you should also have gone through the past 4-5 concalls. The answers to the queries are there.

API revenues has not gone anywhere because most of it is consumed in house to manufacture export formulations. That is alembic’s strength. It is vertically integrated in most molecules and this provides them with an edge in quality and in time delivery of formulations. Their sartans don’t have NDMA issues because they manufacture and consume APIs of sartans. And as a strategic move they don’t sell API of sartans to any other player, to protect their turf in US generics market.

Domestic branded business was revamped and its impact was felt till q4 fy 20, for around 4-5 quarters. I think in q4 fy 20 management mentioned that the whole overhaul was over and it expected growth to return in FY 21. But it seems the Corona situation could have pushed the revival by a quarter or two. As of now because the export market is doing well, lacklustre domestic growth will be taken in stride. Domestic sales in August I read somewhere, was around 7% which seems encouraging. We need to see how the domestic sales progresses though.

Alembic Press Release

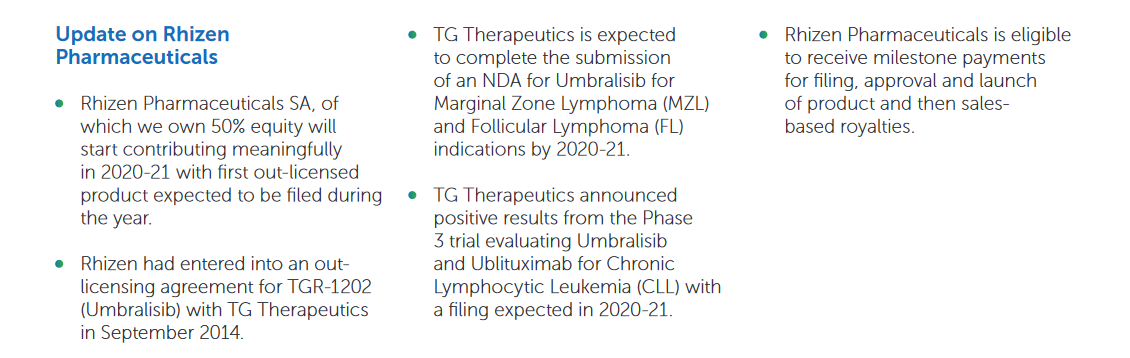

This is to inform the exchange that our Associate Company, Rhizen Pharmaceuticals (“Rhizen”) has released a Press Release announcing that it has entered into an exclusive license agreement with Curon Biopharmaceutical Limited for development and commercialization of Tenalisib, a Dual Pl3K Delta and Gamma Inhibitor for Oncology in Greater China. Please find enclosed herewith Rhizen’s press release. Alembic Pharmaceuticals Limited through its wholly owned subsidiary holds 50% ownership in Rhizen.

I have very little knowledge of the pharma sector so asking these noob questions:

Since Rhizen is a 50% subsidiary, is it ok to presume that the revenue/profit sharing will be in the same percentage ?

Since the trials are in stage 2, how long does it typically take to finish the trials ?

What is the significance of stage 2 ( How probable is the success rate from here onwards)

What might be the revenue/profit impact of this agreement going ahead.

@humbleInvestor I would try to answer based on my limited understanding.

I would request @hitesh2710 to add his comments as he knows the company very well.

My understanding is the profits will be added in the same proportion to the consolidated statements but cash will not flow unless Rhizen announces a dividend.

As per alembic FY20 AR (snippet attached) phase 3 data have already been submitted.

As the deal is only for greater China region, US could be even bigger. We will know more details in the upcoming earning call. This deal should also make Rhizen pharma self sufficient in its journey.