It will effect Severely to Indian generic Pharma companies who manufactures US prescription drugs.

4 Likes

Thanks ranjan. Even though this was published 24 hours ago I totally missed it. And you are right… this is a huge worry. Especially for someone who has shifted their portfolio to majority pharma. Even though it’s still just speculation which are the other pharma companies apart from alembic you see being affected by this? Leave it to trump to burst the pharma bubble. This has made a lot of annual reports and quarter reports and commentary a bit meaningless and I can’t get my head around it fully. I currently am invested in IOLCP, Laurus, Syngene, Granules, Alembic, suven and solara and nearly all of them have some connection to the US be it a 10% contribution to their topline or in some cases a lot more. Going to be a sleepless night ahead and a lot of re reading of annual reports now

Hi @Malkd , I am not pharma expert . @hitesh2710 bhai have deep insight on pharma sector and also he is doctor. He can throw some light on this.

In my opinion API and CDMO players will not be affected much as they don’t sell prescription drugs . I can be wrong.

The more I read about this latest trump move the more it seems like it’s just another red herring from his side to stir up his voter base. Quoting one of the articles I read below and I agree… this looks like just another ploy by Trump. I can go to sleep now

"However, the moves are largely symbolic because the orders are unlikely to take effect anytime soon, if they do so at all, because the power to implement drug pricing policy through executive order is limited. Voters will not see an impact before the November elections, and the drug industry is sure to challenge them in court. "

3 Likes

In my limited understanding, the order has more to do with the big sellers ( like Hospital chains ) not passing on the huge discounts that they get from generic pharma companies to the end users. Cant see this affecting Indian generic pharma.

Also, no Indian media channel / internet - seems to be reporting it. That somehow makes me feel that my interpretation is correct.

However, I will wait for more clarity.

Disc: invested in Dr Reddy, Alembic, Cipla, Sun, Lupin, Natco and Alkem…among the generic players.

7 Likes

Out of all the executive orders signed by Trump, the fourth one which emphasises pricing for generics at a similar level to that seen in various other countries would be the most worrisome for Indian generic players. However the proposed date for this order has been extended to 24 th August and this is with a view to give time to companies to respond and provide their point of view.

Indian pharma companies have been the backbone of US generic markets and help in lowering costs by providing off patent drugs at cheap prices.

This whole antic seems to be a gimmick to gain some cheap popularity in the run up to the presidential elections. There will be challenges to these orders if they are going to be implemented and these are long drawn procedures and may take time to get implemented.

If these measures are implemented, it will in all probability cause shortages in a lot more molecules than current levels. (there are alraedy shortages in some kay molecules because of a variety of reasons. )

All in all it seems that there can be initial knee jerk reactions in response to these orders but post that it could be business as usual. But we need to keep track of developments and see how things pan out.

25 Likes

Under this transformative order, Medicare will be required to purchase drugs at the same price as other countries pay. So we would pay four or five times more for a drug. We now pay — if somebody else pays $1 and we pay $5, we’re paying $1. Now what’s going to happen is their number will go up, our number will come very substantially down, and we’ll all agree at two and a half or two or whatever the final number is.

(under forth order)

Structure of whole pharma industry can change and drugs could be more costly than ever for ROW. Not easy to implement the forth one.

3 Likes

2 Likes

Interesting article in Forbes on the Trump orders.

Trump’s executive order may have very limited effect on indian pharma companies says HDFC securities…names of Indian Pharma companies likely to get affected…

Discl: I am overweight in pharma and I continue to add…I may be biased …

1 Like

All,

I am a novice in the field of value investing and still trying to learn the so called ‘art of investing’ which includes underlying aspects such as reading the Balance Sheets / PL detals. analyzing the Company Management quality and valuation of Business etc. So ple. forgive the question I mentioned below if it appears to be coming out of not doing enough analysis of info already available.

I see that Alembic Pharma has been doing quite well in grabbing and monetizing the shortage opportunities in IG markets over last few years. And this is also counted as one if their niche skills or speciality. And they have been extemely lucky than many competitors in couple of such opportunities. However I am trying to understand how does such opportunities fare vis a vis capacity utilization.

- Is the company always having spare capacity to grab the shortage oppurtunity without affcting the ongoing orders?

- If not, how is the company managing to ramp down / ramp up other production to cater to such opportunities.

Also on this same line, I am trying to figure out how are the capacity utilizations levels at different facilities or overall for the company. I could find some references as below to capacity expansions in recent AR but not the exact utilization figures. Nor could I find this in Management QA that was conducted in Feb this year. Can we take it as capacity utilizations is not a concern for analysis of this business and management is nicely navigating across this area?

Some excerpts from last AR:

“Major capacity expansion nearing completion:

We are on track to finish our large capex projects worth `2,000 Crores in 2020-21. Post this capacity expansion, we will have enhanced new dosage offerings and will be able to cater to the strong demand in US generics segment.”

“Our international generics business span USA, Canada, Europe, Australia, South Africa and Brazil. In recent years, we have undertaken capacity expansion to build manufacturing capabilities to cater to these markets.”

“Over the past two to three years, we doubled our API capacity to 1,100 metric tonnes per annum in order to meet the rising demand.”

1 Like

Alembic Pharmaceuticals Limited. - QIP Launched

Key Deal Specs

Bloomberg: ALPM IN;

NSE: APLLTD; BSE: 533573

Indicative Deal Size: *Up to INR 6,500 MM (USD 86.35 MM) with an option to upsize upto INR 7,500 MM (USD 99.64 MM)

Indicative Offer Price: ₹932.00 per equity share

SEBI Floor Price: ₹ 980.75 per equity share

Last Closing Price: ₹ 985.05 (as per NSE on August 3, 2020)

Indicative Discount to last closing price: 5.38%

Indicative Discount to SEBI Floor price: 4.97%

Key Timelines

Launch of Transaction: Monday, August 3, 2020 (after market close)

Receipt of EOIs (Issuer retains the option to early close) – Tuesday, August 4, 2020

Receive filled-in application form along with pay-in of subscription money: On or around Thursday, August 6, 2020

Listing and Trading: On or around Tuesday, August 22, 2020

BRLM: HDFC Bank Limited

1 Like

Alembic Pharma gets USFDA nod for Erectile dysfunction drug !

3 Likes

Post QIP , Long term Growth Drivers remain in tact for Alembic .

https://www.pressreader.com/india/business-standard/20200729/282144998674513

I came across this small Analytical Article in The Economic Times which speaks a lot about Alembic pharma. The last paragraph reads as follows which is exactly in line with what our most respected Dr Hitesh has been telling.

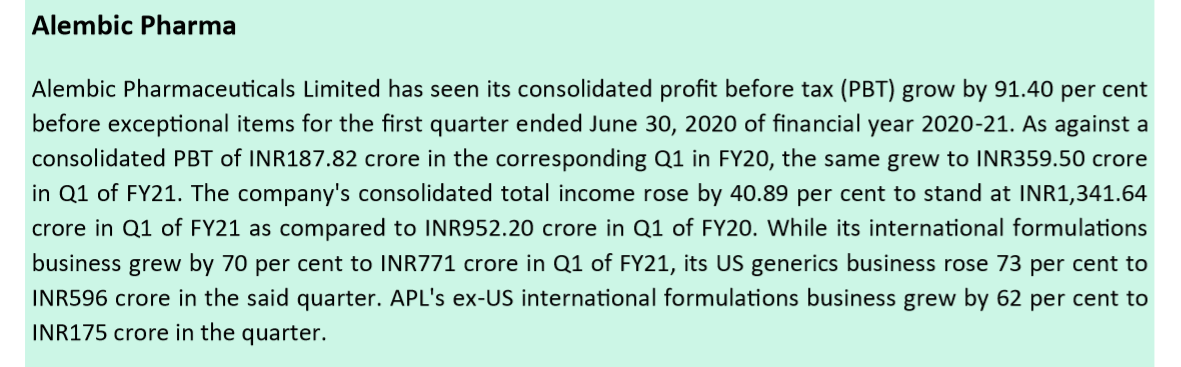

From a valuation perspective, Alembic remains one of the cheapest bets amongst its peers, trading at a PE ratio of 18.7x on FY21 estimates. With healthy EBITDA margins of 31% in Q1FY21 and superior ROEs of 26.8%, Alembic remains a worthy Re-rating candidate, Vaibhav Shah, managing director of Monarch Networth Capital said.

Now since API is the flavour of the season,

Was trying to understand it’s API making capability. It has 3 API plants- all USFDA complied and it appears it has increased its API capacity from 30 metric Tonnes per month to 100 metric Tonnes per month and awaiting for Govt approval to enhance to 250 metric tonnes per month…

From Alembic Pharma’s website , it claims it has filed 84 API’s with USDMF, 34 with Europe , 15 with Japan, 35 with China,22 with South Korea, 25 with Mexico.

Well , what are these API’s??? I confirmed the name of all these API’s from a third party website…so it appears that Alembic aiming to be a major player in API business considering its growth potential …

Needless to say , On formulation front, Alembic has already proved its worth over the years with its wide range of formulations presence in many segments both Chronic and Acute and it continues to enjoy leadership position in some of these drugs:

(1) Sartan’s called ARB’s are preferred as popular Anti Hypertension drugs due to least side effects.

(2) Sartan standalone being prescribed for kidney disease and for reducing proteinuria.

(3) Sartan nowadays being prescribed for all Diabetes patients as a standard protocol for Renal protection and blood pressure control along with Blood sugar lowering drugs.

(4) Its respiratory portfolio consisting of antibiotic range of Microlides such as Azithromycin, Clarithromycin, Erythromycin, Roxithromycin and a wide range of Cough and Cold medicines.

We need to see how Alembic delivers in coming quarters. With Promoter stake of 73% and now that it has cleared it’s debt from the QIP…

https://www.alembicpharmaceuticals.com/active-pharmaceutical-ingredients/

Discl: Invested and I may be biased. Please apply due diligence before putting your hard earned money in stock market.

17 Likes

In my opinion, its an appropriate accounting treatment.

The plants it the gross block when they get commercialised. Before they get commercialised they are generally up for taking batches and samples for the purpose of testing and regulatory filling for which the plants are up and running. Hence pre-op expenditure capitalised before the plant getting commercialised seems appropriate accounting treatment.

Most of the pharma plants have a lead time between ready for production and commercialisation on account of pending approvals. And most of the pharma companies also follow similar accounting treatment.

Pertinent to note that Alembic follows rather conservative accounting treatment many aspects including R&D - 100% expenditure (ex Aleor & Rhizen)

Cheers,

Vineet

6 Likes

Rhizen can throw up surprises in Alembic - FDA accepted NDA application for MZL & FL on August 13. Hopefully they fast track this.

CL, being the larger indication, both NDA filing and approval will be a key trigger for a milestone based payment from TGT. Approval for CL may come in late H2FY21 / H1FY22. Nonetheless, significant milestone payments should be able to recoup good part of the Pre-op hit on the P&L.

Cheers,

Vineet

11 Likes

The major overhand for me is the company is eyeing a capex of Rs ~1,400 crore over next three years with nearly Rs 650 crore in the current year. With current absolute level of debt, froth building up in Pharma, the free cash flows will remain depressed. With continuous expansion, past four years and negative cash flows, I dont see a prudent strategy of distributing dividend of Rs 80-100 crore per annum and carrying debt on the books. Debt levels in absolute terms have ballooned in last four years and the Company has been continuously capitalizing the interest cost. At 20 times trailing earnings, the stock looks a little overvalued.

1 Like

(1) I like the management for its agility and Alembic’s nimble supply chain as indicated by Alembic’s performance in Q1-2021 during pandemic when most of its peers failed to achieve similar Results.

(2) Capex may be bad if the promoter is using money for diversifying in to unrelated business…However , if it is using Capex for its existing business which is growing rapidly , it is desirable…

It successfully raised Capex through QIP…Capex in my view in this case is a welcome step when there is a tailwind and demand for its products both domestic and overseas market… I am ok as long as the company is investing in its existing business which is growing and get return out of it and going by the past record of the promoter and the fact that Alembic is a 100 years old business - they should be able to deliver …

(3)It is expanding its API capacity at a time when indian govt is encouraging API production and API now is a sunrise industry-there is an increasing demand both in domestic and Exports…

(4) Respiratory portfolio… I appreciate the cough and cold brands … for example Wikoryl is very popular brand I know since last 30 years…used it by doctor prescription and found to be highly effective .

Leader in Microlides class of drugs including its API…Azithromycin … for respiratory infection…perhaps the safest antibiotic with least side effects…even dentists choose this antibiotic for dental procedure … If someone is allergic to penicillin, then Azithromycin is the antibiotic of choice. .

Alembic’s wide range of Sartan’s used in Chronic diseases like hypertension, Diabetes, Kidney protection … There is always a persistent demand for Sartan’s across the world…

(4) Valuation wise considering its past performance, valuable product range and future potential, I find more comfort in buying Alembic at current level than all its peers…

Discl; invested and may be biased… many times I go wrong in my assessment…

Please do your own assessment before putting your hard earned money.

21 Likes