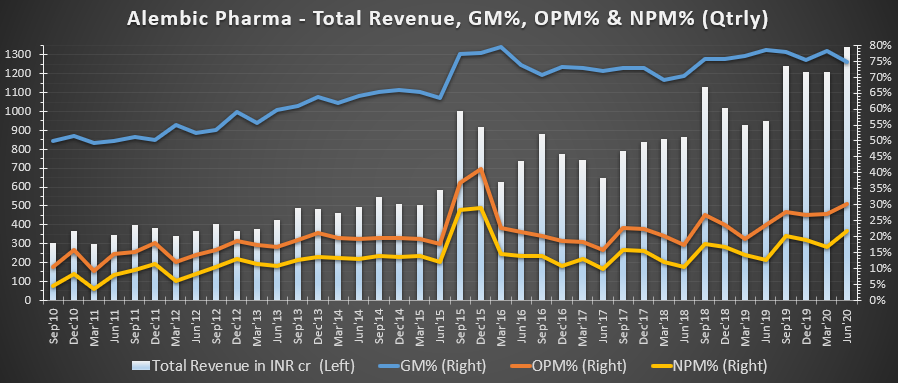

Alembic q1 fy 21 results have been along expected lines, with the sartans traction continuing and according to management commentary, not likely to fall off the cliff, as was the case with molecules like abilify.

The advantage alembic has is it is one company which has presence in most variants of sartans and their combinations. Plus it is present across various strengths. One thing to know about sartans is they are nowadays a first choice anti hypertensive medication because of their kidney protective effects. Now what does this mean? Normally in hypertension patients, over a period of time, the kidney tissue tends to get damaged but at a very very slow and negligible pace, provided hypertension is controlled well. But sartans if given to hypertension patients tends to reduce this risk to negligible levels. Hence they are universally preferred as a first choice anti hypertensive drugs. So one can clearly see what kind of volumes are involved in sale of sartans.

The oft asked question is how long the traction is going to last and what is the management doing about it. The best recourse is to keep following the same formula and be ready when you get lucky. Therefore the higher pace of filings to prepare a huge list of approved ANDAs and hope to get as many lucrative molecules in the market as possible and use shortages to the best advantage.

For me, the qip is something not worth doing a lot of bheja fry. They probably are not accustomed to high levels of debt and might want to pare it. Or maybe have a war chest ready for some acquisition of a nature that fits their strategy and vision. It could be a facility in a different geography, or a group of lucrative ANDA filings or whatever else that suits their purpose.

Talking to an expert, i got the feedback that for US sales, going from 250-300 million usd annual figure to 500 million usd should be easy. Beyond that will test the mettle of the company and management.

The recent softness in price probably could be due to prior run up and or nervousness related to qip pricing. That should be a temporary blip, according to my reading.

The real positive surprise for me was only 6% dip in domestic sales y on y. Most hospitals and clinics were closed for nearly half of the quarter and so this is a positive surprise for me. Need to compare with domestic sales figures of companies which will report numbers for q1 fy 21 hence forth. If going ahead, as indicated by management, domestic segment picks up, it will be an additional lever of high roe growth.

To add to the positives, rhizen pharma contribution is an icing on the cake. The outlicensed molecule has been approved for two varieties of leukaemia which are relatively less common. But tg therapeutics has sought approval for the molecule for the more prevalent chronic lymphoid leukaemia. If that approval comes through it can be a significant positive for alembic as it enhances royalty as well as manufacturing revenues.

I had trimmed some holding in the run up to results to maintain portfolio weightage to comfortable levels, but remain bullish on the company and maintain the bulk of my holdings. Might even look to add on declines or consolidation.

Intimation of board meeting for raising of funds

Intimation of board meeting for raising of funds