Is there any site exits from where we can get information when USFDA visit will be scheduled in Alembic Pharma or any other pharma companies?

Like below, Here it is mentioned There was a scheduled inspection in Alembic Pharma . From where we can get to know that USFDA inspection is sceduled.

The above was a usfda audit which was cut short due to covid and company got these minor observations. Post that VAI (voluntary action initiated) status was accorded and on asking an employee I was told that FDA resolution should be swift.

Dear admins,

Seeking permission to post my blog link here.

I’ve written a blog on Alembic on my site and would like to get opposing views on the pointers that I have written in the blog.

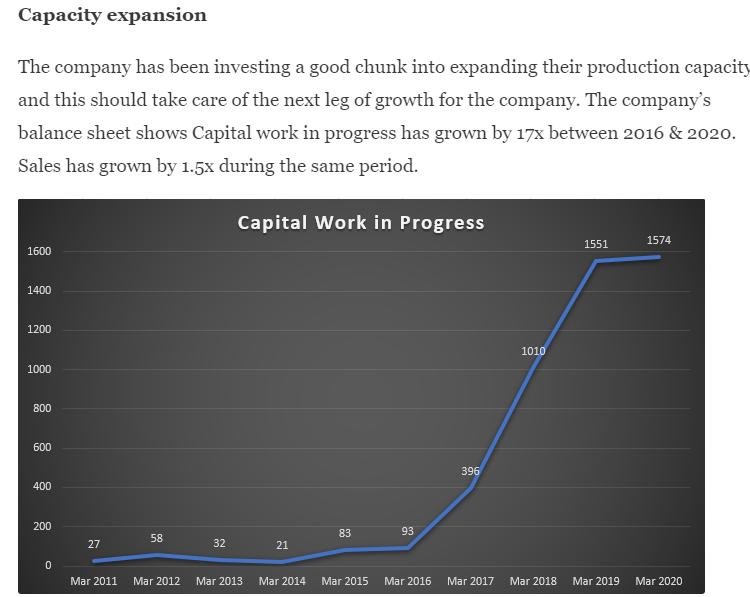

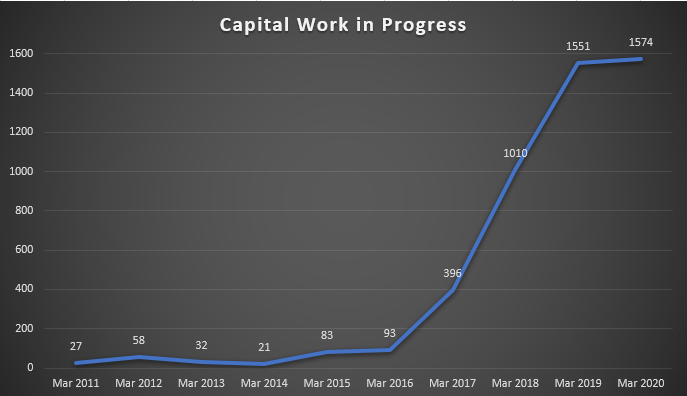

For example, increase in the co.'s CWIP. Now some people may consider it a positive while others may not consider it not too important.

So if I can get permission to post my blog link, I can post it here.

Regards,

Barath.

You can’t. Blog links are not allowed. Please post the contents here.

Based on inputs from VP admins, PFB, contents from my blog for your perusal.

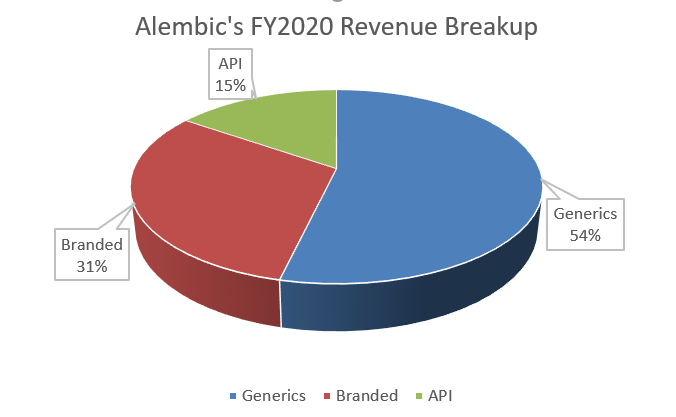

Revenue sources

Generics business growing well

CWIP increased rapidly between 2016 & 2020

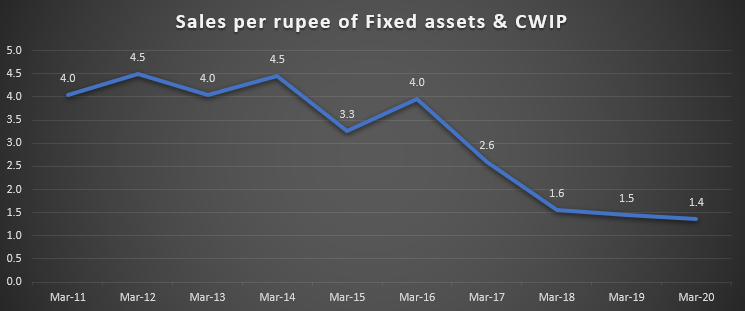

Scope for increase in Asset turns

Earnings quality check 1

Risks

Exporter risk – Early in March 2020, the government of India, banned exports of APIs and some basic chemicals. If the situation changes, and exports are banned again, for reasons (unknown-unknowns) that we can’t anticipate, this would adversely impact the company.

Infection risk at plants – At least 2 other pharma companies have reported several of their employees got infected, recently, possibly at work.

Pricing power risk – The company may not end up being able to pass on the increase in API costs or other raw materials to it’s customers. We will need to wait and see how this plays out over the next few quarters. This risk also applies to their generics business. Other generics players producing the same drugs may result in margin erosion for the company.

Other risks include Macro risks due to uncertainty around Covid19, Opportunity cost risk, Logistics / Raw material risks & Dilution / Leverage risk (The company has been growing faster than the ROE it delivers)

For example, data from an article from the US FDA site states, higher the number of generic players, lower the drug prices.

So if the branded drug sells at ₹100 and there is just 1 generics player, then the generic drug would sell at ₹61. However, if there are 6 Generics players, then the generic drug gets sold at an abysmal 5 bucks.

Valuation triggers

-

Lack of growth visibility in most sectors other than Pharma, particularly ones with a high % of chronic portfolio and ones with high reliance on exports

-

Lack of certainty in other sectors given the rapidly evolving Covid19 situation.

-

R&D / Capex expected to come down by FY22

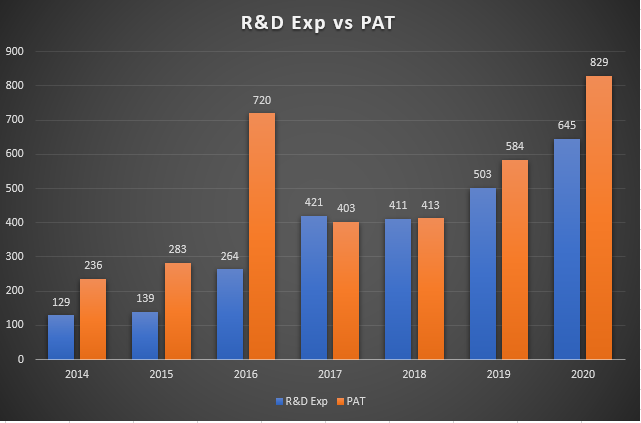

How did the company fund it’s massive R&D program?

-

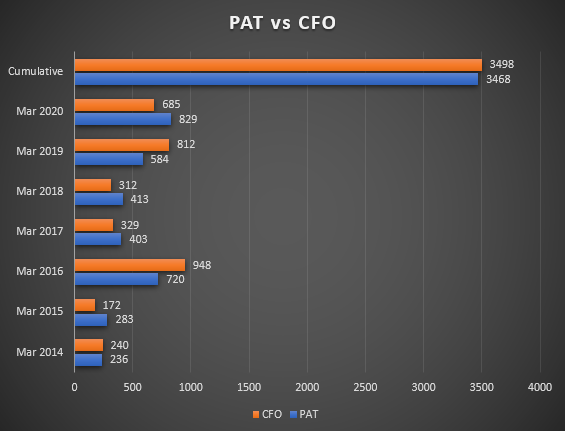

The company spent a total of 2900 Crs on R&D between 2012 & 2020.

-

In the same period, their debt increased by 1420 Crs.

-

Out of this 1420 Crs, 847 Crs were paid out to shareholders as Dividends.

-

So these guys went to the bank, borrowed 1420 Crs from the bank and out of this 1420 Cr loan that they took, they passed on 850 Crs to Shareholders as dividends.

-

So that left them with 573 Crs which they could now use to fund some portion of their R&D.

-

So, this means the company funded 2300 Crs or 80% of it’s R&D exp from cash flows that the business generated and 573 Crs or JUST 20% of R&D from debt.

-

Was it funded by diluting equity? No, because no new shares were issued.

-

So that leaves us with the only other source of funding which is Cash Flow from Operations.

-

So 80% of their R&D exp was generated by cash that the business generated.

The co. funded 80% of R&D Exp from internal cash flows and 20% from debt

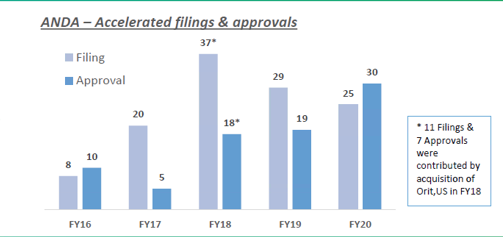

The outcome of all this R&D expenditure can be seen in the new approvals that the company receives from the US FDA.

Some folks I spoke to, raised concerns about high R&D expenses (investments?) by the company. Lets think about what happens when, a company has a lot of approvals.

By securing more approvals with potentially huge payoffs, the company gets more exposed to positive black swans. A case in point would be Alembic’s opportunistic plays at 3 different times. Alembic,

- benefited from the opportunity in Abilify drug back in 2016 or thereabouts

- is benefiting from the ongoing opportunity in Sartans drugs in 2018 (expected to last until Dec 2020 or beyond)

- has the potential to benefit from the ongoing opportunity in Azithromycin in 2020

Was it a case that company got lucky thrice or was it because the company had so many approved products / approvals in place, which ensured they were (almost) exclusive sellers of 3 products that were in solid demand? Were they thinking “Heads I win big, tails I don’t lose much”?

Managements’ thoughts on R&D exp, ROE and Free Cash Flows in the next few years.

Why are margins high?

The company’s FY19 annual report states – “A good supply chain helps protect margins and also provides us with some room to improve our pricing.”

I believe the reasons for higher margins could be the company’s supply chain + their US front-end marketing team + some pricing power due to the Sartans issue.

Detailed note

Alembic Pharma investment thesis - May 2020.pdf (1020.0 KB)

Do let me know if anything needs to be added/removed. Thanks…

Alembic pharma investment thesis if it is to be made in a few lines would be

-

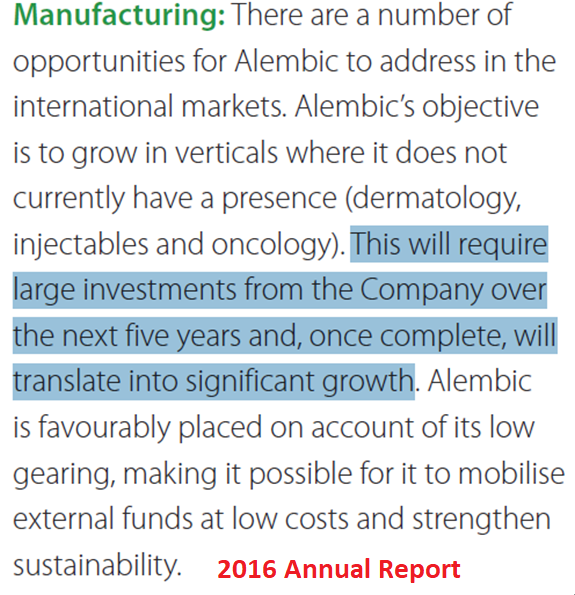

Good growth since FY 2019, continuing into FY 20 and likely to do so in FY 21. (need to see how growth happens in FY 22 but in second half of FY 22, the expanded capacities should start firing. And if that happens growth runway for another couple years could be clear as the capacities are sweated out)

-

Proactive management which has tried to utilise all levers of growth and has invested significant amounts of money in R&D and in capacity building. Money invested in R&D seems to be bearing fruits as company keeps filing new ANDAs and keeps getting approvals of earlier filed ANDAs on a regular basis.

-

One lever of growth which till now has not fired well has been the domestic porftolio. It occupies 30% of total revenues and has been growing at a sedate pace. If this too starts doing well, (management has indicated about domestic growth in recent concalls) it could be icing on the cake.

-

Clean FDA track record. For all US facing companies this assumes a lot of significance because Alembic has navigated this quicksand much better than peers.

-

Superb US front end team which knows how to utilise opportunities to the maximum. The top guy is a hard bargainer with the local pharmacy chains and has earned grudging respect from them.

-

Vertical integration in a lot of molecules it sells. This helps in maintaining quality and regular supply as they are not too dependent upon other guys for their important raw materials.

-

Very good think tank at the top. The top team has plans ready in advance for next few years. The company has got good execution capabilities to execute these plans.

-

Yet another important high margin growth opportunity could be manufacturing for the NDA they outlicensed to TG Therapeutics.

-

Most important is company is a lucky company.

You always want to partner with guys who always end up getting the rub of the green. Enough examples over the last few years where company got lucky and was at the same time prepared to utilise that luck to make big bucks. e.g abilify, theophylline, sartans (still goes on full steam), azithromyin (with its empirical use in corona), venlafexine esp in Europe.

You always want to partner with guys who always end up getting the rub of the green. Enough examples over the last few years where company got lucky and was at the same time prepared to utilise that luck to make big bucks. e.g abilify, theophylline, sartans (still goes on full steam), azithromyin (with its empirical use in corona), venlafexine esp in Europe.

Where should we worry?

1, Domestic portfolio

2, Debt - it can peak out at 1600-1800 crores.

3, Performance of expanded capacities.

4. Petering off of US growth.

Technically the stock price crossed its previous all time high posted in 2016 of 792, and has gone up to current levels of 900. Valuation wise we do not want to get into too much details because for stocks in strong uptrends (or in downtrends as the case may be), valuations can surprise big time.

disc: invested.

Some good prospects for domestic sales for Apll

A double digit growth in India business, in this difficult environment should be an encouraging sign.

Also, I think its quite achievable as the management has been walking the talk off-late. Plus the base in their India business is not too big.

This coupled with their sucess in US should keep the stock price in a bouyant mood.

Alembic Pharma seems to be striking all the right chords.

Disc: invested. Views may be biased.

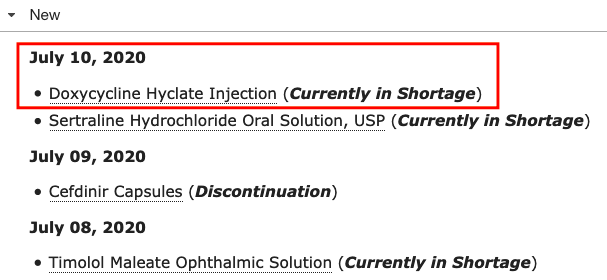

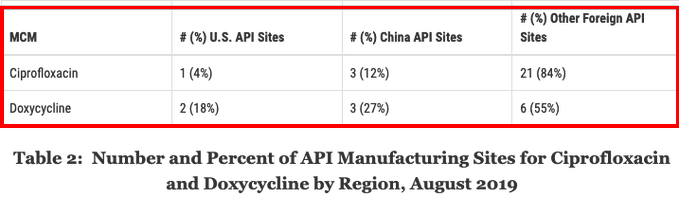

FDA added #doxycycline injection shortage in US on 10th July #Cadilahealthcare having USFDA nod to market Doxycycline injection,100mg/vial & 200mg/vial #Alembicpharma recently got USFDA nod for Doxycycline tab Doxycycline is considered critical as Medical Countermeasures in US

Ciprofloxacin & Doxycycline are two drugs considered critical as Medical Countermeasures in the US US has only 1 API facility for #Ciprofloxacin & 2 for #Doxycycline Recently, #Alembic got USFDA nod for Doxycycline tab

Hello Vivek, Can you tell me where was the shortage of Ciprofloxacin updated? I couldn;t find it.

Shortage Reason: Demand increase for the drug

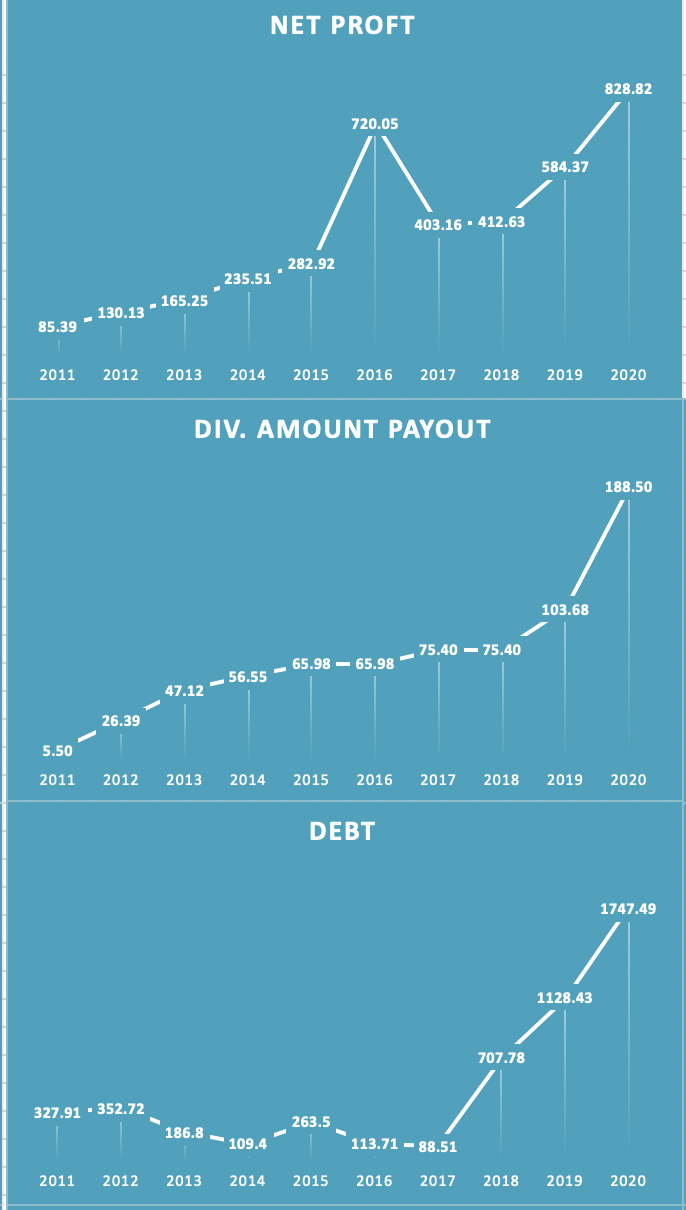

Great to know of r&d but isnt it a red flag if dividends are paid out of debt ?

They also made ~2500 Cr profit during that period which was shared with share holders. I have attached the debt, profit and div payout below… One could see that only 202 Div. payout was higher, but its still proportional to the profit.

True that it was proportional , but my query is what was need of debt to maintain proportionate payout as why cant dividend be reduced if capital can be deployed for lucrative growth opportunities?

On hindsight it is always easy to question these decisions… From 2015-2020 stock was consolidating between 400-600. Dividend was the only appreciation for the loyal share holders and promoters were consistent with the dividend payment. Also they were making profits, not that they borrowed and paid out as a dividend to the share holders.

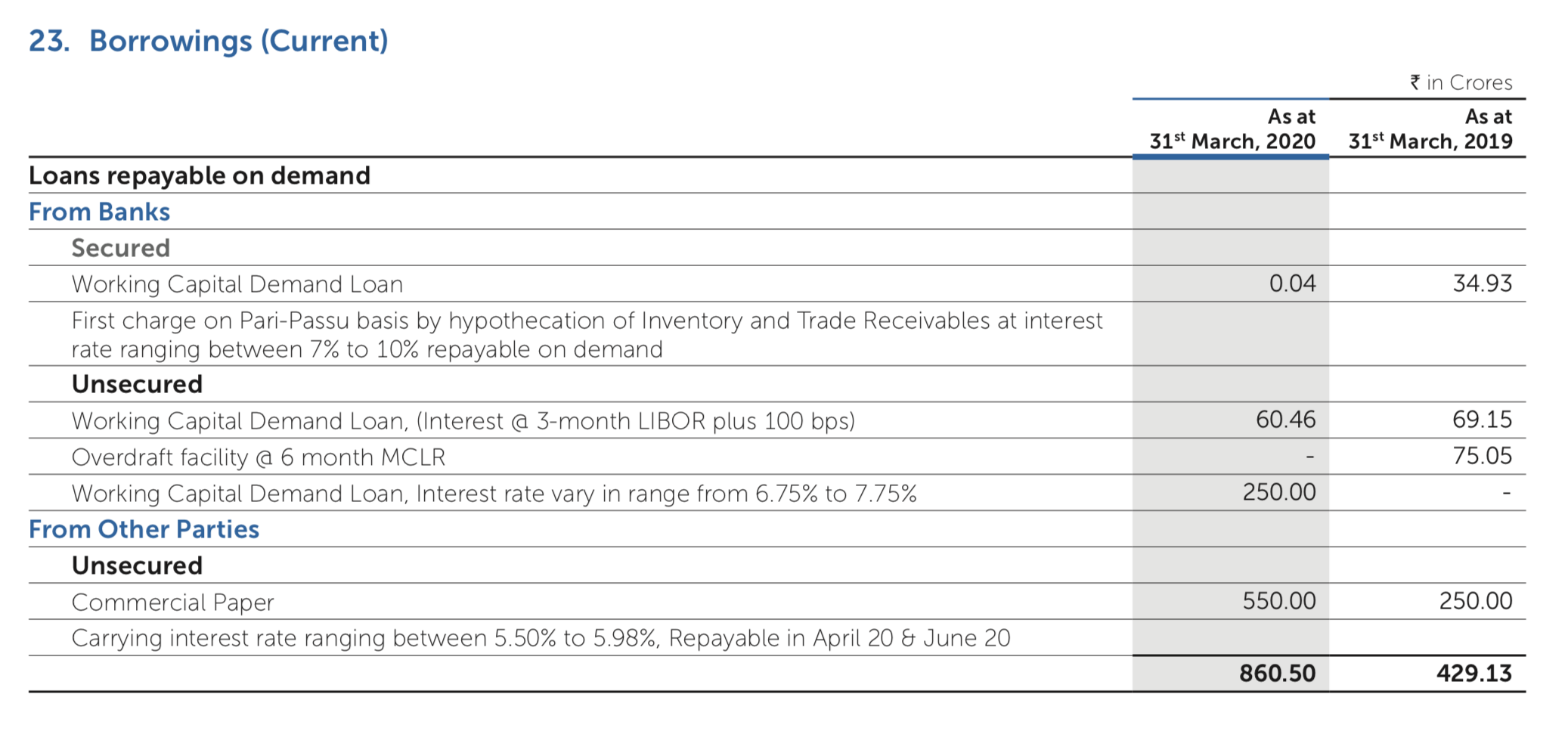

Moreover Alembic pays 27 Cr interest on 1747 Cr debt… I have attached the corresponding debt details from annual report

I don’t think I will add any more value to the forum if I continue discussing it further… so thats all from me regarding this.

It’s not about hindsight , dividend out of debt is present scenario

I am invested and like the company and its plan as well as operating cashflow

Disagree on current scenario as if capital can be put to more prudent high growth capital allocation, maintaining dividend for benefit of few shareholder preference doesnt arise . In fact shareholders would appreciate high growth capital allocation. Dividend is to be paid only when such opportunity doesnt exist . Perhaps high promoter holding is reason for higher dividend .

Of course they were making profits but then what use of borrowing ahd paying dividends simultaneously. Better borrow that much less . Company cant be paying dividends just for preference of few shareholders when high growth and return capital allocation opportunity exist

The test for dividends is sufficiency of profits. If profits are there, nothing wrong in paying dividend even if debt exists on balance sheet. Cost of debt is lower than cost of equity. A moderate amount of debt is not bad. It is not essential to become debt free before paying dividends.

How would you define sufficiency of profits?

IMO, any capital expense should be made which can provide maximum returns for company and shareholders.

A company in very high growth and high capex phase will be better of utilizing that additional income by investing back which will give high return on capital rather than paying dividend, which has low optimal usage.

Coming back to sufficiency of profits, I would expect company to give dividends only when it is generating free cash (CFO- capex).

Alembic is not generating Free cash each year and has increased dividend payout ratio, 18% to 23% on the base of higher profit. Not sure this is the best use of capital.

Company should have waited for next 1-2 years when high investment phase will be over to pay incremental dividend

This is the case with most companies. Think banks.

By the very nature of their business model, banks are required to borrow.

Does that mean they should not pay dividends?

If they don’t, what would happen to their valuation during a market downturn?

Dividends act as a sort of a floor when there are market downturns because people think “oh, this stock’s got a 3% dividend yield. So, let me buy it. And this arrests further price correction and keeps raiders at bay”

For dividend paying companies that have debt on their books, dividends are just a mental accounting trick in my view.

They borrow from the bank in the name of capacity expansion, working capital needs, etc.

Mentally, the management might be thinking hey we used that bank loan money to expand capacity.

And we paid out dividends out of the profits that the company made.

We did not use that bank loan money to pay dividends because we already used it up for capacity expansion.

Is that really so? I don’t think so ![]()

Had Alembic not paid out dividends all these years, it’s current debt would be 1747 Crs minus 847 Crs = 900 Crs. (This excludes the interest outgo towards the extra 847 Crs that the company borrowed to fund dividends, technically)

For high growth, high ROE companies, not paying dividends may be the correct capital allocation decision in my view.

But again a lot of shareholders wouldn’t agree (particularly the elderly ones ones who depend on their annual dividends for their monthly expenses. I am talking about the ones who’ve been invested for decades and have portfolios of a significant size with significant dividend yields, at cost).