Alembic pharma gets USFDA approval for Deferasirox used in the treatment of chronic iron overload.(Innovator: Novartis)

1.Final approval for Tablet of 90 mg and 360 mg…market size US$ 415 million for 12 month ending Dec-2018.

competitors with approval: Zydus and MSN lab.

Final approval Tablet for oral suspension 125mg,250mg and 500 mg …market size: US$:135 million.

Total 6 competitors including Alkem,SUN pharma.

3.Tentative approval for 180 mg Tablet…market size of US$:59 million.

Total ANDA approvals: 107.(95 final and 12 tentative).

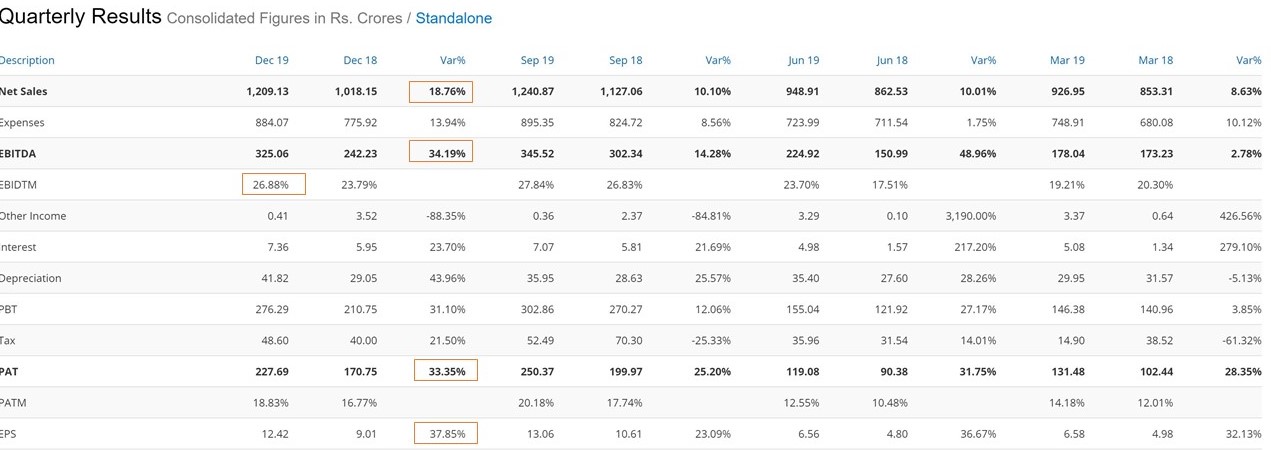

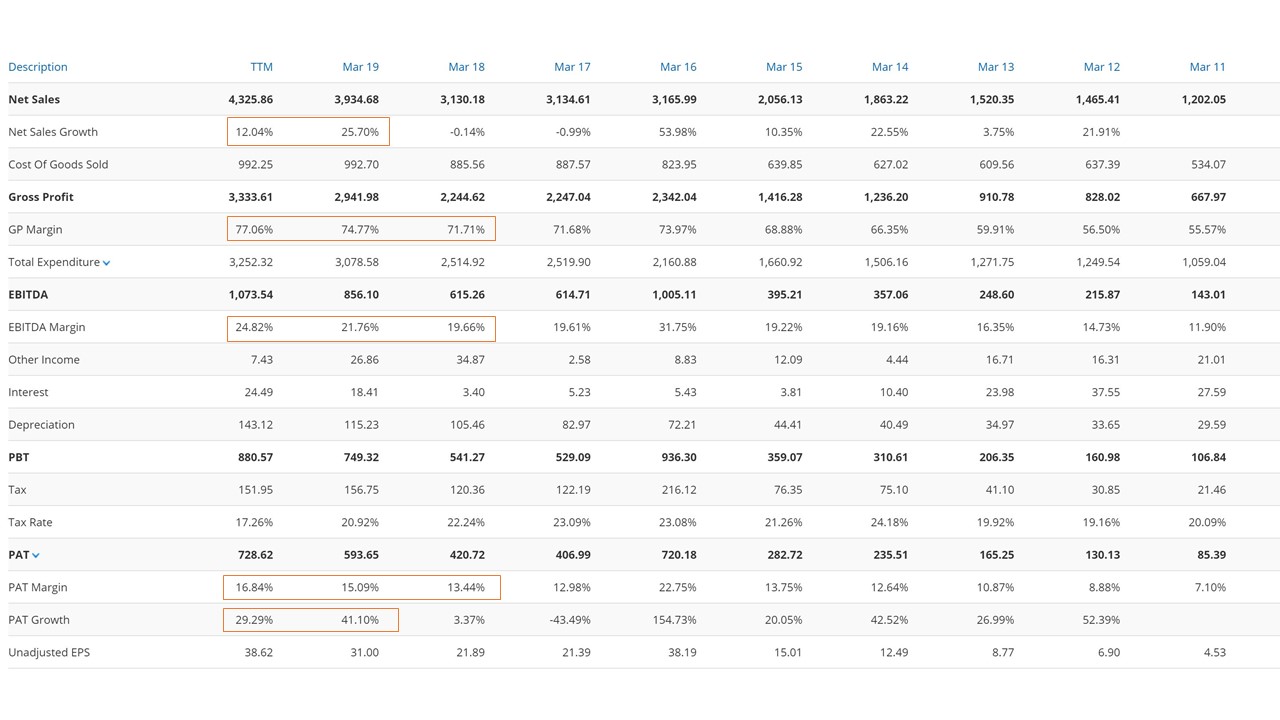

excellent set of results

Revenue for the quarter up 19% to Rs 1209 crores from Rs. 1018 crores

Net Profit for the quarter up 38% to Rs 234 crores from Rs 170 crores

International Business

• International formulations grew 48% to Rs 664 crores in the quarter.

• US Generics grew 61 % to Rs 515 crores in the quarter.

• Ex-US Sales grew 15% to Rs 149 crores in the quarter.

• 8 ANDA approvals received during the quarter and total tally stand at 110.

• 6 ANDA filings during the quarter; Cumulative ANDA filings at 176

India Formulations Business

• The India formulations business was Rs 368 crores for the quarter as against Rs

365 crores last year.

API Business

• The API business grew 2% to Rs 553 crores as against Rs 540 crores.

Disc - Invested

Net borrowings on balance sheet is Rs 1349 crores as on Dec 2019

R&D expenses was Rs 146 crores around 12% of sales in the quarter gone by

Received 8 approvals during the quarter and launched 7 products during the quarter in the USA

The projects are physically complete

The India formulations business was flat

Participants

Aviva Insurance

JM Financial

MAPL Value Investing Fund

HSBC

Lucky Investments

Research Delta Advisors

Axis Capital

IDFC Securities

Motilal Oswal

SPARK Capital

Antique Stock Broking

OldBridge Capital

Goldman Sachs

Dalal & Broacha

QnA

Have corrected the practice of giving extra discounts in the institutional business and it will start getting reflected once the comparable base gets corrected since April onwards

Full impact of growth in domestic business will be visible from Q1FY21 onwards

Have launched 17 products in US market so far this year and in some places have picked up market share

As more and more products are launched in US it gives more stability to the business

About 36% of sales in US market comes from top 5 products

Earlier was present in only oral solids in US market

The thought process behind the recent capex has been is to enter newer areas like ophthalmology, injectables so that the company can move higher up the value chain

The plants will only be commercialized when the first commercial batches come up for order

The higher gross margins can continue forward till opportunities exist in the market but the management doesn’t have an exact timeline on till when will the opportunities persist

The domestic pharma business is a very high ROCE business but growth opportunities in domestic market are limited

The international space has seen changing dynamics because of:

Consolidation among buyers

Higher competition due to higher growth

Not looking for any acquisitions in the domestic market as organic growth in domestic market is more attractive for the management

No major capex expected for new projects but regular recurring capex of Rs 300-350 crores is expected during the year

The number of MR’s remain around the same and in total there are around 3900 MR’s and 40% of them are in acute business and rest in specialty business

The capacity utilisation is peak in both the segments

Five products will be launched soon in the market and another 5-10 products may be launched by the company

The inventory days are around 60 days and receivable days are around 26 days in the domestic market

Last but not the least, on the price action front, stock has been consolidating since a long time, bunching of Guppy MMAs is currently taking place, RSI is showing strength and the stock also went through a shakeout.

Thank you for the detailed analysis. Wrf to SHP, Elara and Mathew India have not reduced their holding but they are clubbed under FPI, Similarly Cresta fund is also clubbed under FPI.

Nice work! Good to see a template which can be incorporated like a checklist to not miss out on the concern areas. Few thoughts on your observations:

Agree that promoter remuneration is at the highest level. Sadly we can’t do much as most of the listed cos extract the max limit allowed by the government. I really wish that we all should take this matter up with SEBI etc and suggest them to improve this. A good rule could be - if the directors are promoters of a company then salary+commission % should be really low. If done, this will lead promoters to think from minority shareholders perspective and take out money by way of dividend etc (If people like this suggestion then we must find a way to forward it to concerned authority)

Coming back to your inputs. Why are you comparing the purchase/sale value to net profit? Isn’t this wrong? I think it should be compared to turnover.

Out of 70 Cr of purchase from related party, 50 Cr has been consistently happening from several years from Alembic ltd which manufactures APIs. So this could be normal. The concern should be on the spike of dealings with Sherno Publications ( a co which doesn’t even seem to have a website). We should inquire about this.

On your query of capex and depreciation - accounting rules in themselves call for capitalization till the asset is put to use. So given the pharma industry, 3 years seems to be normal timeline for capex to start and finally get through USFDA approval…no? It would b wrong if the co starts providing for depreciation before they get the clearance as commercial activities wouldn’t have started. Perhaps the right way to check spend on capex should be to compare with industry number…any thoughts on that?

Thanks for the very structured way of recording and presenting your findings on forensic audits. Especially loved the Executive Summary at the Top. Someone (uninitiated in forensics) like me could easily get lost in the details that follow. But the Red Colour coding draws my attention. And then the words “a BIG red flag” is…makes me pay attention, which sometimes a natural optimist like me is prone to ignore.

We should write to management and ask for details on consolidated RPT disclosures for years prior to FY 2018. We can also check on the discrepancies as reported in different years for any clarifications.

Let’s wait for more responses to your observations from others invested/interested/tracking Alembic, and your rebuts if any. Also responses form other forensic experts most welcome @varadharajanr, @diffsoft@Mantri - will be good if you busy folks can find some time to educate us.

@ashwinidamani

Many thanks for your initiative. Do you want to start a Forensics Framework 2.0 thread - where you showcase your framework and explain the basics for newbies in forensics like me. I think most will find this very very useful, even forensic practitioners, who naturally like digging into these things first. The discussions there, and different examples brought in will make for very enriching discussions and bring the spotlight back on forensics; might help improve this framework and make it even better and simpler for us newbies to learn to spot/connect the dots better.

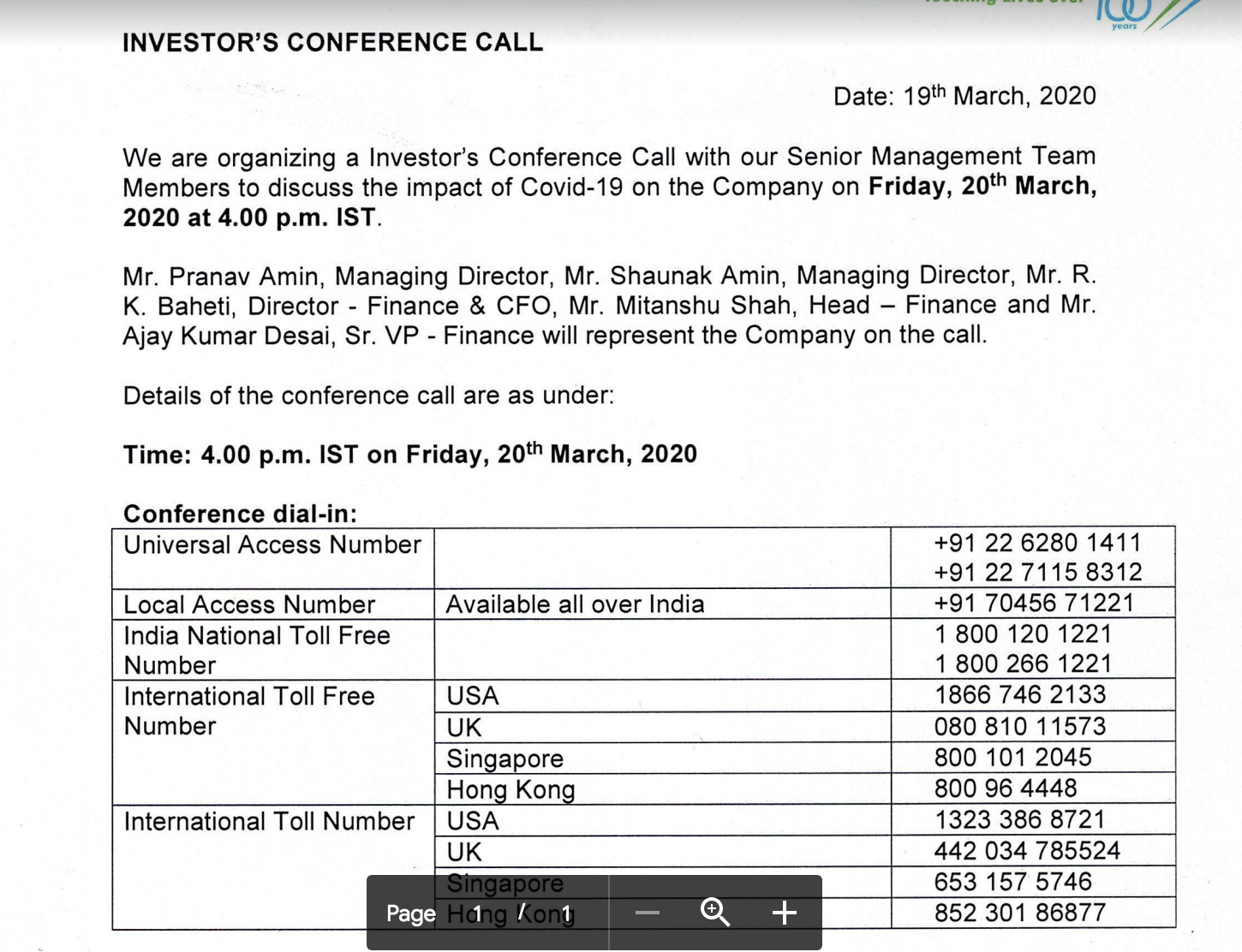

I attended the Concall today at 4 pm. Sorry for the short notice at 3pm, just escaped my mind for posting it early in the morning. The intimation was received last evening. Hope some others did too and can add to my top-of-mind notes (incomplete, non- exhaustive).

Quick Notes in no particular order - on stuff - that could move the needle significantly? There may be errors in my Notes, or the emphasis misplaced (Invested/bias). Others who made detailed notes, please correct.

Alembic Pharma Concall 4pm, Mar 20, 2020

US FDA Audit: F1 - Panelev, Main facility audited recently

4 483 observations, quite benign, all procedural, none related to data integrity. So our responses should be adequate, we should be able to file responses in 2-3 weeks. Don’t expect any impact/delay in any of the planned launches

F2 - oncology, twice audited, not expecting now

F3 - just filed products, not expecting audit before end of year

F4 - will be filing, so not before end of year

API facility - already audited and clear

Suspension of FDA activity by FDA: only Audits on hold, reviews and response to queries going on remotely as usual

New Govt ruling on API - makes it faster to apply and get approvals for setting up fresh capacity and/or expanded capacity in existing plants. Govt announced financial support/incentives also, details unclear/still being worked out by Ministry

API - rather than Constraints (intermediates supply disruption), we see more as Opportunities. Govt stance has changed, and fast tracking of approvals mechanism will be in place soon. Looking at expanding capacities in a big way. And hopeful of getting fast approvals. We have enough supply/stock of intermediates for key APIs; We see no constraints.

Up until 2 weeks, China supply disruption was an issue, but we had stocks and sourced from domestic as well, but now supplies from China have resumed for us

Business is as usual for us. Progressing in line with plans on all fronts. The only front we may have a bit of a constraint is Outbound logistics may get impacted a bit - delayed by one or two weeks; some reshuffling of packages, due to some flight cancellations

Logistics share between Inbound/Outbound Air and Sea Cargo.

80/20 sea/air on Inbound

90/10 air/sea on Outbound

Domestic - Fall under essential supplies - So no disruption. Seeing good traction as per plan. No constraints. Ramped up production, good availability of products at stock points

We have a large interest and large stake in a new product - chloroquine+azithromycin (azithral)+ some other (cant remember) drug combo for COVID trials; 20-patient non-aggressive study; ongoing and unfolding situation; got triggered 2-3 days ago

Azithromycin Base material/Intermediates sourcing from China, Europe - adequate stocks. China supplies also resumed

No direct Front-End in Europe. We sell through distributors. No change in forecasts. Continuing as usual

Building API capability trend in the industry is already there. for many players API/Intermediates 60-70% internal. bUt in Alembic case, Top 20% of our most profitable products - where 80% of the profitability comes from - we are almost completely backward integrated.

Rupee depreciation: Works to our advantage; we do only $sales, so benefit accrues to Alembic

Disruption due to Covid: We try to be nimble, and always try to take advantage of supply disruptions.

Happy to revive an old habit (read passion) meeting Entrepreneurs/Managements face to face after having done deep-dives on a business some of us TopContributors are mutually interested in.

Hope you enjoy going through this as much as we were while preparing and quizzing and transcribing the in-depth interview of close to 2 hours. Lot of hard work from @spatel and @ankitgupta needs mention. Rest of us were there to help guide them into making the questioning deeper, more complete and maintain proper discussion flow. Very impressed by the dedication & sincerity shown by entire team.

If you like the Graphs, you know who to thank - our resident lead data collation, slice n dice domain expert @spatel. Skill-sets of guys in Team VP today are way beyond what we used to do back then. Loving the experience again.

Alembic playing a role in treatment of COVID19 with azithromycin. Alembic is the largest player in the estimated ₹550-crore per month of azithromycin market with approx 30 per cent market share. The company makes the anti-biotic at its Panelav facility.

Supreme Court Judgement on Environmental Protection against Alembic. Though it doesn’t have significant financial impact it still raises valid questions on the approach on the management in addition to huge salaries that they draw!

2 units of Alembic shall deposit a compensation of ₹ 10 lakhs for having caused environmental degradation

(iii) Darshak Private Limited - the eight respondent; and

(iv) Nirayu Private Limited - the ninth respondent.

Alembic Ltd supplies APIs (and maybe even intermediates) to the Pharma business (I guess its to both the divisions - International and Domestic.)

The Alembic Ltd plant is located in the Alembic campus itself. Over last few years there has been talk of dismantling it and using the land for Real Estate development (done by the other promoter group entity under Alchemy brand.) But the plant is intact so far.

Regarding Shreno Publications - Please see this website - http://www.light-publications.com/. The Light Publications building is situated right on the opposite side of Alembic campus’ entrance. I understand that Alembic Pharma buys packing materials from Light Publications.

Light publications website says division of Sierra Investments.

Purchase of 11 Crores in previous year from Sierra Investments seems to tally with this. I guess subsequently Light Publications have been moved under Shreno Publications entity. Hence the 23.5 Crores purchase attributable to Shreno Publications.

Source: Currently staying in Vadodara. Light Publications is a known local brand. All the facilities / buildings can be seen personally.

Page 68 of 2018-19 Annual Report: [Section is General Shareholder Information].

The Company imports API/Intermediates/Key Starting Material (KSM)

which may be prone to commodity price risk. The Company does not

do any hedging except strategic procurement at times.

China is not mentioned specifically. I don’t know if the import trade data tracking through sites like Zauba still gives company wise details. Without customs data, it would be difficult to know.

Ashwini,

While it is your job to only wear the “forensic purist hat” and blast away. It is the job of experienced investors invested/interested/tracking the business to point out the obvious unsubstantiated nature of certain allegations.

Even as a devils advocate job is being done to perfection, it should be done with full responsibility. Any insinuation that falls flat on “data” from that business must be avoided. Because the position/role of a forensics auditor in VP is going to become more and more powerful, and more & more independent - so that individual biases of senior investors/or prolific contributor(s) to a thread are properly balanced out.

Coming to this part how come they are always there with the right API at the right time, manufactures the API, and makes huge profits, and implied …gets away with that?

This is easily demolished by a fact known to everyone who follows US Generics Pharma - that it is the most tightly regulated industry - no one can just make an API out of the blue…it must have filed for the API years ahead in time, got the approvals in place, got the plant inspected without 483 observations, and only then can make shipments.

So paper profits accruing from zero API filings for product, or zero shipments of product cannot be faked. I am sure that is obvious to someone like you too. Now I have seen this post after 2 weeks, so I am commenting now. Others investors/interested in Alembic may not have even seen this post in last 2 weeks busy as we are protecting our backsides

So lets NOT get carried away with playing the devils advocate role to perfection. Let’s stick to facts/data that CANNOT be disputed, which you are doing a great job of, and the community is grateful for that. Please continue to play the forensic purists role to perfection.

Let’s be extremely careful with insinuations - minus substantiating data - that’s what it is. If we are not quick to defend/are unavailable for some reason, that can influence newbies the wrong way given the weight of other substantiated data-points? Also it’s “unfair” to the business in question.

[PS: we need to get @pratyush to check if notification emails are being sent out properly for everyone (in my case I was not getting notified of new posts in my threads of interest due to some tech issues, resolved now]

Going by the estimates in this article, retail sales of Azithral (Alembic’s Azithromycin brand) have a significant upside.

Some excerpts from the article.

According to data with the research firm IQVIA, India sold 12 crore strips of the drug last year, which is around 60 crore tablets (an average of 5 tablets a strip). The top brand here is the Vadodara-based Alembic’s Azithral.

It is the largest player in the azithromycin market, estimated Rs 550 crore a month.

Alembic, which also claims to be the largest player in selling active pharmaceutical ingredients (APIs) of azithromycin to the world, holds 30 per cent market share in selling the finished tablets of the antibiotic in India.

“Our three manufacturing plants for the azithromycin APIs produce 20 tonnes every month, which can be expanded to 40 tonnes. Generally, one crore tablets are manufactured using 5 tonnes of API,” Rajkumar Kumar Baheti, Chief Financial Officer, Alembic Pharmaceuticals, told ThePrint.

Alembic exports all of its APIs. For finished tablets, the company, going by the estimates, can manufacture around 10 crore tablets per month.

Alembic Pharma receives 4 observations from USFDA for Panelav facility

None of the observations are related to data integrity or repetitive in nature.

“The company will provide comprehensive corrective action report to address each observation. The company is committed to maintaining highest quality standards that meet USFDA standards,”