Alembic has entered into a Joint Venture Agreement (‘JVA’) dated 7th May, 2019 with SPH SINE Pharmaceutical Laboratories Co Ltd, China (‘SPH Sine’) & Adia (Shanghai) Pharma Co Ltd, China (‘Adia’) to promote and sell pharmaceutical products for the Chinese market.

Initially this JV will commercialize products manufactured by Alembic Pharmaceuticals Limited. Subsequently the JV plans to set up a manufacturing facility in China.

The JV will commercialize products in the Chinese market which has an increasing demand for generic drugs.

It will initially launch with a portfolio of oral solids and is expected to widen to other areas like injectable, ophthalmology, dermatology & oncology which are being currently developed and manufactured by Alembic.

SPH Sine, Alembic & Adia shall hold 51 %, 44% & 5% equity in the JVA.

About China market opportunity for Indian pharma players - snippet from Natco Q2Fy19 conf call…

“What China has done is what I understand is introduced new rule that you have an approval in western country, they will fast track your Doxil to file that in China so I think if you look at portfolio of companies who has approved in western markets like the US, Indian companies obviously probably forefront in the numbers of approval in the US and China obviously is a very good market and has a great opportunity. So I think idea here is that if you file this on the fast track basis I think will get some break through. We have few filing pending and the intent to file product so we are bullish but I will said it is cautiously optimistic because this new rule change but if you get a hit in China, you get pretty nice numbers. I think there is no doubt like that if we get one product to succeed I think the sale numbers would be as good as good US launch or as a solid India branded launch.”

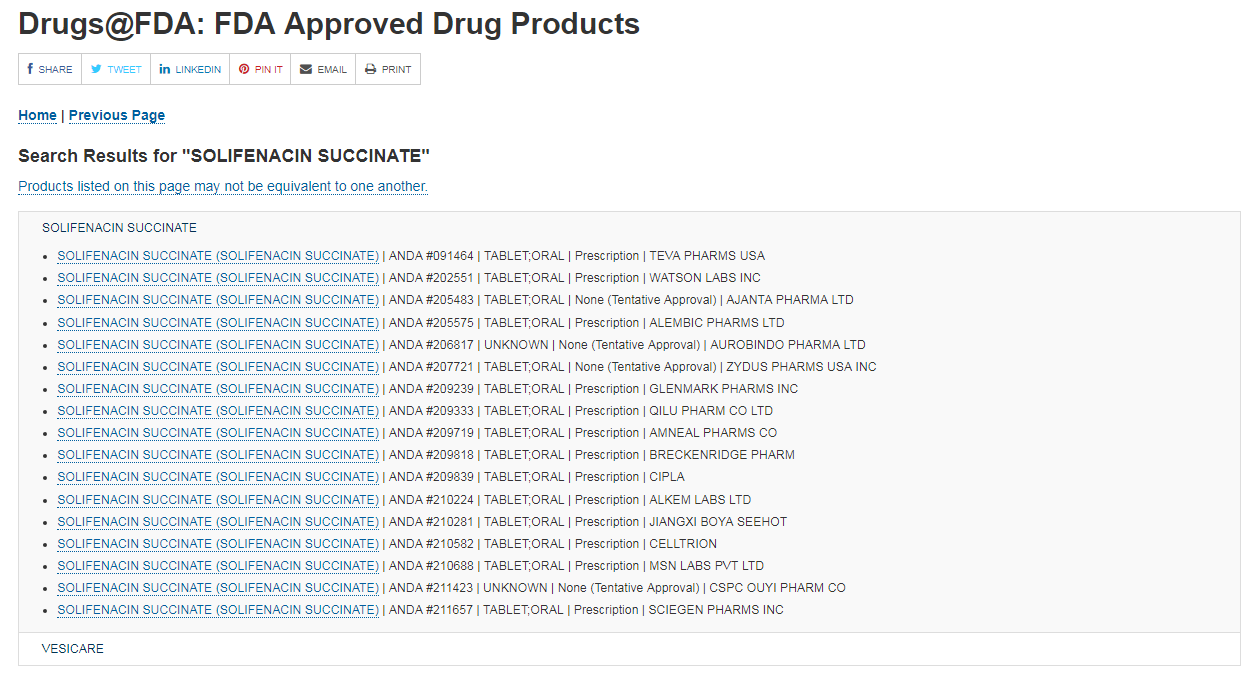

Alembic Pharma has received approval from the USFDA for its ANDA Solifenacin Succinate Tablets, 5 mg and 10 mg.

It is therapeutically equivalent to the reference listed drug (RLD), Vesicare Tablets, 5 mg and 10 mg, of Astellas Pharma US, Inc.

It is a muscarinic antagonist indicated for the treatment of overactive bladder with symptoms of urge urinary incontinence, urgency, and urinary frequency.

About 33 million Americans have overactive bladder.

It has an estimated market size of US$ 967 million for 12 months ending Dec’ 2018 according to IQVIA.

Seems very limited competition product. Teva has launched gVesicare recently in April 2019.

Yet another FDA approval for Carbidopa and Levodopa Extended-Release Tablets USP, 25 mg/100 mg and 50 mg/200 mg. Estimated market size of US$ 24 million for twelve months ending December 2018.

There are actually many many approved players in this market, with some tentatives also pending. Screenshot attached.

Who will get the market share is a different question, but the price erosion will be extreme on mass generic entry. Also, you’ll notice that in these press releases, companies typically give the market size of a few months ago, before generic entry. The actual opportunity becomes significantly smaller.

Recent drug litigations for Alembic include a product called Esbriet, manufactured by Genentech and having revenues of over US$ 1bn.

Earliest patent expiry is all the way in 2026. There are 15+ guys litigating.

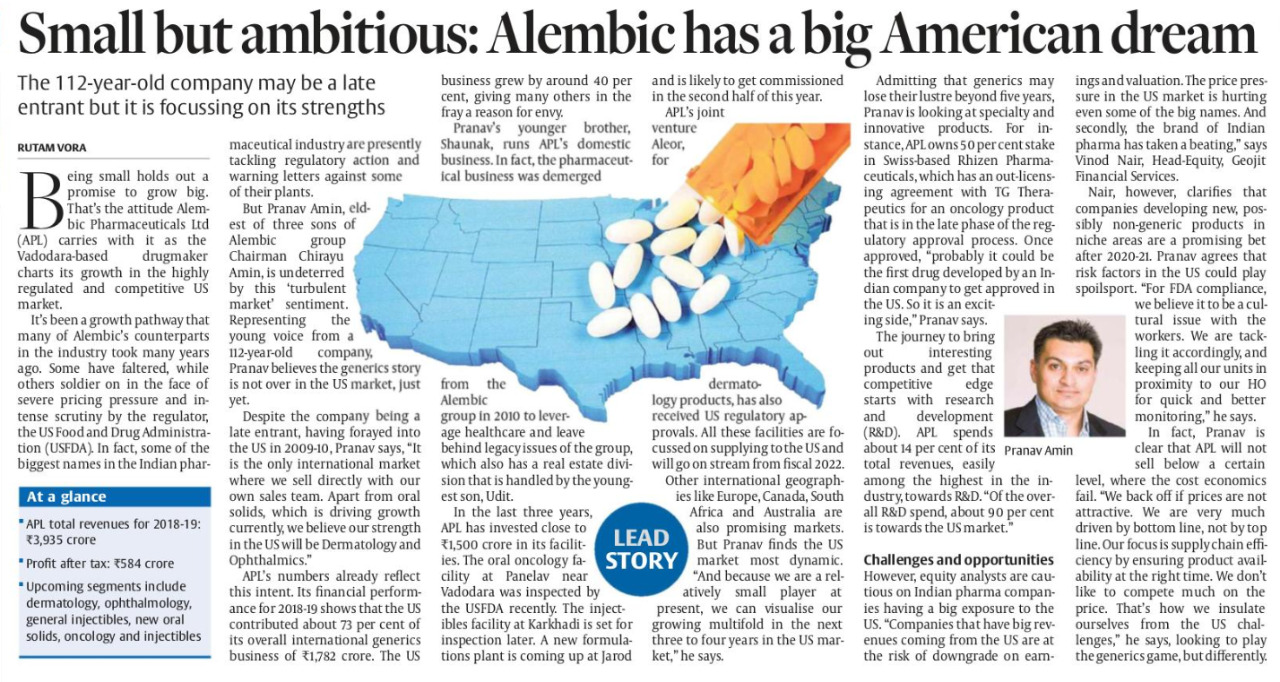

We manufacture branded formulations, international generics and APIs for the global market. Headquartered in Vadodara, we have three R&D centres in Vadodara, Hyderabad and USA and five state-of-the-art manufacturing facilities (including Dermatology) in Gujarat and Sikkim to which we shall be adding three new plants i.e. oncology oral solids and injectibles, general injectibles, ophthalmic and new oral solid plant.

In FY19, our revenue from operations on a consolidated basis amounted to 3,935 Crores vis-à-vis 3,131 Crores in FY18, recording a 14% CAGR over the last five years. The net profit after tax was recorded as 584 Crores compared to 413 Crores in the previous year. Our PAT has grown at a CAGR of 16% in the last five years.

R&D Spend Rs. 549 cr at 13.90%. (Rs. 481 cr in FY18). Our combined R&D strength today stands at 1,100 employees. Our long-term focus of the business is to build a stronger product pipeline for the US market for which we are working hard and have been able to ramp up our research product pipeline from 45 to 235 plus products.

The Company also maintained a strong Return on Equity (ROE) of over 20% despite significant increase in R&D spend and expects ROE to further improve once product commercialisation begins from new facilities.

Gross Capex Rs. 626 cr. Capital investment is expected to significantly come down from FY21 onwards since all new facilities will be commissioned. These facilities would be sufficient to address the Company’s needs for the next 3-4 years. Lower capex intensity should drive improvement in the Company’s free cash flow generation over next few years. (Total capex from Balance sheet including dep. and intangible assets is Rs. 821 cr.)

Increase in debt from 708 Crores in FY18 to 1129 Crores in FY19 to fund our capex programme. During the year we raised ` 500 Crores through NCD and locked ourselves at extremely attractive rate.

Total interest payment during the year was Rs. 70 cr. Booked in P&L Rs. 18 cr., rest is capitalised. (Average loan during the years is Rs. 918 cr, average interest rate is 70/918 = 7.6%).

Total remuneration to directors Rs. 64 cr.

Exports = 62%

Domestic 38%.

International Generics: 45%

Domestic: 35%

API: 20%

International Generics

USA: 72%

Other: 28%

Domestic Business

Chronic: 68%

Acute: 32%

International Generics

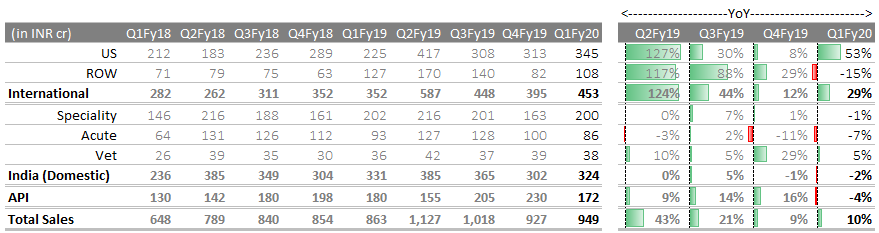

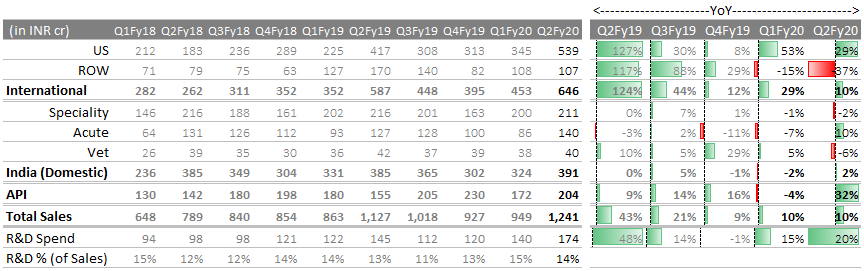

International Generics business grew by 48% to Rs. 1782 cr. This growth was largely contributed by a short-term supply opportunity that we leveraged in the second quarter of the fiscal. Our agile and nimble supply chain and high-quality products helped us deliver the required quantities, ensuring quick turnaround and opening avenues to forge deeper relationships with our customers.

USA business grew by 40 % to Rs. 1,288 Crores.

EROW business grew by 73% to Rs. 494 Crores

54 products launched through the US front-end (9 launched in FY19)

USFDA approved Aleor Derma JV plant

Around 20 new launches planned in FY20

Plants: Karkhadi, Panelav and Jarod

Total Revenue: Rs. 1782cr.

ANDA Filed in FY19: 29

Total ANDA filed: 161

Approvals Received in FY19: 16

Total Approvals: 89 (Including 12 tentatvie) Soon to be launched

Karkhadi Plant: Dermatology, Opthalmic***, General Injectables***.

Panelav Plant: Oncology OSD*, Oncology Injectables***

Jarod Plant: New Oral Solids**

API

API business grew by 18% Rs. 771 Crores

Plants: Karkhadi, Panelav

Total Sales: Rs. 771 cr.

Total filings: 100 DMF

New filings: 8 DMF

We have also witnessed a substantial rise in repeat orders and to service the rise in orders we enhanced effective capacity from 400 metric tonnes to 800 metric tonnes. This was achieved through a combined effort of capex spend of around ` 300 Crores over the last couple of years and planning and optimising manufacturing processes. We have also autotomised many processes to reduce human intervention and contamination. The API business is on a steady growth path.

Domestic Branded Business

Domestic branded business grew by 9% Rs. 1,382 Crores.

Plant: Sikkim

Our market share is 1.6% of the Indian Pharma space

93% new launches in specialty

5 brands in top 300.

Total Revenue: Rs. 1382 cr.

Marketing Team: 5000+.

We launched 15 new brands (43 SKUs).

Our Sikkim manufacturing facility which is dedicated to our domestic branded business ran to full capacity. We intend to increase capacity by investing online extensions and optimising production activities.

Aleor, our joint venture for dermatology products, filed eight ANDAs in the fiscal and received two ANDA approvals. Alembic made investment of Rs. 207 cr. in Aleor during the year through debentures.

The dermatology business shall start commercial production in FY20 for the US market. We are very enthused about this opportunity, as our dermatology facility has been designed to enable production of multiple dosage forms under a single roof.

Our acquisition of Orit Laboratories LLC has further bolstered our capabilities in the US with a competent R&D team bringing complementary skill sets in soft gelatin based oral solids and oral liquids.

Our associate Rhizen Pharmaceuticals SA has out licenced novel molecule (Umbralicib i.e. TGR 1202) to TG Theraputics, USA and the recent clinical data is very robust. The molecule is for the treatment of rare forms of blood cancer.

In India, 851 medicines are regulated under Government of India’s National List of Essential Medicines, 2015.

Recent credit rating report of Alembic Pharma by Crisil.

One interesting point is that Alembic is taking a kind of contra call on US markets. Where other companies are reducing exposure in USA by focusing on other countries, Alembic has been increasing it’s ANDA filings in US market.

Key Points from CRISIL report.

In fiscal 2019, Alembic capitalised on shortage of the hypertension drug, Valsartan in the US, which led to healthy growth in revenue and sustained profitability. Revenue rose by 26% in fiscal 2019, year-on-year, driven by 48% growth in international formulations. Domestic formulations grew 9% during the fiscal.

Steady demand for existing products and fresh product launches in the international and domestic segments will support growth momentum over the medium term.

Operating margin should sustain at 19-20%, given the price correction in the US and elevated R&D requirement (about 13% of sales), driven by focus on building abbreviated new drug applications (ANDAs), particularly for specialised generics.

The company continues to incur sizeable debt funded capital expenditure (capex) annually, primarily towards specialised generics. Capex of Rs 790 crore was incurred in fiscal 2019, to be followed by planned capex of Rs 600 crore, in fiscal 2020. Nonetheless, capital structure is expected to remain healthy with comfortable networth and gearing at 0.5 time, over the medium term.

The company has nearly completed its large capex of around Rs 2,000 crore towards specialised generics, which commenced in fiscal 2016. In fiscal 2020, the company plans to incur Rs 600 crore capex for additional lines. Post fiscal 2020, the annual capex is expected to be at Rs 400 ’ 450 crore over the medium term.

The company is among the top 20 players in the domestic formulations market, with revenue of Rs 1,382 crore for fiscal 2019. Growth in the branded formulations segment should maintain pace with the industry, backed by increased contribution from the chronic therapeutic segment and regular product launches, leading to volume growth.

On account of greater focus on the US, the company has gradually stepped up its ANDA filings in the last few years ’ 29 in fiscal 2019 from 8 in fiscal 2016.

In October 2018, the formulations facility in Panelav, Gujarat, received four procedural observations under form 483. These observations were subsequently cleared with no action indicated.

In the domestic market, regulatory impact of drug price control order (DPCO) and ban on some Fixed Dose Combinations (FDC) has adversely affected revenue and profits in the past; and may continue to do so over the medium term. With a quarter of domestic revenue under DPCO, turnover and profitability remain susceptible to regulatory changes.

Alembic Pharmaceuticals receives USFDA Approval for Bromfenac Ophthalmic Solution 0.09%. Alembic now has a total of 96 ANDA approvals (84 final approvals and 12 tentative approvals).

Alembic had a successful USFDA inspection of Oral Oncology OSD facility at Panelav. As per AR 2019 Company filed for ANDAs for oral oncology in H2 FY19.

Alembic Pharmaceuticals receives USFDA Approval for Pregabalin Capsules, 25 mg, 50 mg, 75 mg, 100 mg, 150 mg, 200 mg, 225 mg, and 300 mg. Pregabalin Capsules have an estimated market size of US$ 5.47 billion for twelve months ending December 2018 according to IQVIA.

Alembic now has a total of 98 ANDA approvals (88 final approvals and 10 tentative approvals) from USFDA.

Yet another today…

Alembic Pharmaceut icals receives USFDA Tentat ive Approval for Dapagliflozin Tablets, 5 mg and 10 mg. Dapagliflozin Tablets have an estimated market size of US$ 1.7 billion for twelve months ending December 2018 according to IQVIA.

Alembic now have a total of 99 ANDA approvals (88 final approvals and 11 tentative approvals) from USFDA.

But how many will launch is a question mark these days due to severe price erosion. I think 30-40% will not launch despite approvals.

Pharma per se is not doing good, especially generics. Amneil is at $3 from 25. Mylan is at multi 15+ years low… bad time for generics. But seems like the turn around may not be far with companies starting to skip unviable launches.

Let’s hope for the best…

Good results by Alembic Pharma. Great to see all that R&D exp and approvals in US bringing good growth in US Generic business. Rest all other segments underperformed.

9 ANDA approvals in the qtr is really high compared to 19 in whole FY19.