For A - I would not venture anything other than hybrid mutual funds

For B - If I am managing someone else’s money, it would be Midcap and Hybrid Mutual fund probably in ratio of 60% to 40%. I would venture to direct equity only for those who wants Highest possible risk or if its my money and I have to answer only myself in case the invested company is closed or bankrupt, which is so common even with good names in India

[quote=“sujay85, post:35, topic:23480”]

except Nestle, unless it starts growing in high teens. Nestle on the other hand has a better portfolio, better pricing power, and increasing aggressiveness.

I agree that other are more qualitatively better . Growth is an important ingredient that’s missing in Dabur since last 3 years . I find Nestle better in terms of parent support , new product introduction, monopoly in noodles and baby food segment compared to Dabur . Have seen more shelf space too allocated in many stores to Nestle products . IMHO , Nestle parent seems to have a grand strategy in place to participate in Indias growth story looking at the higher growth on a higher base in past few years . Dabur has great portfolio but aggression isnt seen yet and focused approach on growth isnt seen as compared to other companies stated above .

Similarly in addition to pe ratio , opportunity size , growth consistency and long runway etc are also important qualitative aspects that must be considered while valuing a company. If growth consistency isnt shown , price wouldn’t appreciate much and it would be more like Hawkins ( not comparable but just as an extreme example as to what lack of growth can do to the price despite high ROCE and high quality business that ticks various other boxes ) .

I would suggest you to read One up on wall street by Peter Lynch that I have found it to be an excellent read and very useful .

Disc - Invested in some of the above names and I am not a sebi registered analyst. Pls do your own diligence before investing

Some of my learnings as a beginner in past 1 year and learning from valuepickr seniors especially from Hitesh bhai @hitesh2710 on his portfolio thread

1 I believe this was a period of down cycle in stock market for mid and small caps that were at excessively high valuations and hence there was a long correction. Even I too got caught in the wrong end of the cycle . Investment in small caps or mid caps if to be done must have a horizon of atleast 5 years and only into quality market leaders in their own niche segments.

2 As Hitesh bhai @hitesh2710 rightly pointed out in his thread , we are always on the lookout for the next Bajaj Finance or HDFC bank but these are one of a kind . And base rate of small caps or midcaps getting bigger is very low .

I personally believe in investing in large and high quality midcaps with secular growth so that one can expect to make 14-15 percent . Agreed that returns are outsized in small caps but management information is normally not easily available and hence if still one must invest in small caps , it should be in quality management, great cash flows and market leaders in their field with little or no debt and a very small portion of ones portfolio if one doesnt have hang of small cap investing.

3 I now try to avoid cyclicals ( a lot of money can be made provided one has a hang on cycles which I find it difficult) and mostly try to focus on secular growth stocks in large caps and high quality mid caps . One more thing it’s a myth that all large caps return less ( although it’s mostly true )as all large caps arent made similar and ones with high growth give above average returns in comparison to other large caps . Eg Bajaj finance

4 If investing in growth stocks with fairly high pe , one must monitor the growth story . Quality companies have a bad quarter or two . However if it prolongs more than that and it seems that management promises more than performance,

then it’s best to take a reality check and trim holdings else there are mighty chances of pe derating. Great companies are given more time of a year or two by market before pe derating happens but it does happen . Eg Page industries.

5 This matrix based on book by Bharat Shah - illustration on safal niveshak website by Vishal Khandelwal I find it pretty helpful.

Growth must be coupled with High ROCE to be value accretive. If ROCE is less than cost of capital, high growth can be value destructive

6 if you haven’t gone through Hitesh bhais portfolio thread and portfolio capital allocation thread , highly recommend to go through the same .

Disclosure- Invested . I am not a sebi registered analyst . Standard investing disclosures apply .

When I did valuation of Nestle, Britannia, ITC, etc, I noticed that ITC was severely overvalued (when compared to Nestle or Britannia) if you expect it to be an FMCG company with declining tobacco volume. The margins of tobacco was something like 50 or 70% while other FMCG margins were at 0.5% to 2% ranges. Even if it improves to 10%, replacing lost sales of tobacco will be very hard. If one believes in tobacco volumes picking up and sustaining for a very long time, ITC may appear reasonably priced or rather cheap.

Disclosure: I hold Nestle and Britannia. No holdings in ITC.

Hi @sarthakkumar19_,

Last I checked, it is growing from paltry 0.5% to 2 odd %. Let’s assume it goes to 10% or beyond like other FMCG companies. However it cannot get the margins of Cigarettes. So lost revenue (if you predict it) of cigarettes cannot be compensated by fmcg.

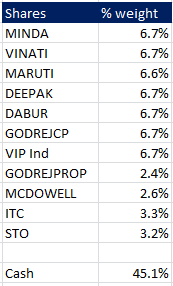

Another quick update: I have deployed 6% cash in 2 short term (30-45 days) opportunity. My cash levels are hence 37%. I intend to stay on these cash levels and wait till the next result season.

Sure,

Moderator, if this is against the guidelines you may remove the post.

Kajaria ceramics- I have been following the kajaria story for some time now, it has been improving its market share and volumes, and at the same time I think the trigger point should come from stimulus which will be aimed towards real estate sector. I have taken the help of technicals at this point as this is an attempt to time the market where I have a good chance of failing.

Indigo- This is on a pure scuttlebutt basis, as I saw the business is booming on daily and non daily routes. The reason that it is not in my long term bet is due to the promoter issue overhang.

The timeline for both is 30-45 days. But if the upside comes, I will be profit booking. This is the only time I have also used stop loss for individual stock.

Why not keep Kajaria as long term holding. It has all the materials for becoming one. They are constantly adding & improving portfolio with regular high A&P spends. Kajaria Ply also is gaining market share rapidly from unorganized players.

Yes, Kajaria is a good company. But earnings are paramount, even though it has been improving sales y-o-y, it has stopped earnings neither the bottom line neither the cash flow growth since 2016.

Until and unless I see a change in that, it becomes a difficult long term play for me.

The 2 day carnage gave me an itch to buy, to break thy rule of thy portfolio. There are a couple of urges I have with regards to the buying portion:

APL apollo, GMM Pfaudler. There is also CRAMS in my radar now.

But I have not transacted in the 2 days because the above stocks didn’t fall. Their resilience is commendable but also very annoying.

Interesting way of looking at it. I feel ITC to be valued as a dividend player for its low growth and eventually degrowth cigarette business (as has historically happened with Tobacco companies in developed economies) and valuing its FMCG business can be real tricky. Thats probably because although margin is low, and even growth in current quarter maybe low but they have a perennial source of cash from cigarettes. Now, this source of huge cash can be a boon or a doom, depending on how management keeps deploying it and categories and businesses they chose to invest in. If they chose right business and right FMCG categories, growth can explode as compared to peers in a short span. Overall, a difficult company to value. I would chose dividend yield as a signal to value and invest. I maybe completely wrong. Thanks

I exited Kajaria today. The timeline was considered for 1 month and I had a stoploss prepared and it was triggered. Also, it doesn’t look like government will be able to come up with relief for real estate and hence the thesis is revised.

Poor timing when it came to Kajaria. This is my lesson from this, stoploss works both ways, stopping profits and losses. In most circumstances like RBl it helped me save capital.

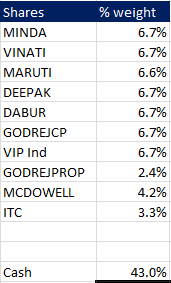

I had exited McDowell due to the sudden Diageo probe involvement in Chidambaram’s case. I did not know if the issue could escalade or not and it lead a decision of exiting with minimal gains.

I have added Syngene, and IOL Chemicals and Pharma and incresed allocation in Indigo.

I’m sitting on 31% cash now.

How would this impact the listed company? If any fines etc it will be on Diageo. Keen to know your thought process since I also hold United Spirits, bought after Diageo came. Came across the following article on this -