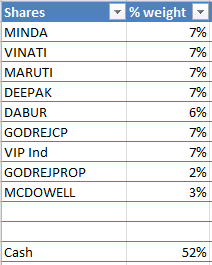

VIP Industries

From your portfolio, I would say VIP Industries certainly has some near term risks, especially in the form of the Chinese wage inflation. In my blog post, I had assumed that the management will be able to shift all production to Bangladesh (Currently ~10%), but the commentary in the last Concall makes it clear that there are labor and integration issues there.

There is an evident trend of companies shifting production out of China in large swaths. So I would say, make peace with whether VIP will be able to either continue to pay low wages in China (I sincerely doubt that) or shift production out without any issues. Seeing as how low cost production is kind of VIP’s niche, I believe this will be a big focus area to consider. I am not saying it’s a black swan, but it’s certainly worth additional attention.

Secondly, it was actually Mrs. Radhika Piramal who was spearhearing change and innovation at VIP for the last couple of years. Most importantly, she introduced Skybags and Caprese, opening up a whole new lines of business for VIP. Unfortunately, she’s moved to London since last year for personal reasons. She is still being paid a salary, but her involvement in the business is nowhere close to what it was half a decade back.

There’s no doubt that VIP Industries is an excellent enterprise, with a proven decades-long track record. But I think management succession is crucial, because the bags business is in many ways going to be the company’s future. Will Mrs. Radhika Piramal get back to her active role in the management of the company? I think that is also a question worth asking.

Finally, tracking activity by Samsonite and Safari is also essential. The new kids (Not so ‘new’ anymore, really) on the block have managed to wrestle a respectable market share from VIP for themselves. If you haven’t already read it, do read this wonderful research report on the luggage industry in India.

Dabur and GCPL

I don’t understand why Dabur and GCPL have the ‘same story’. They are both FMCG firms. But Dabur is more FMCG than GCPL. GCPL is, for lack of better phrasing, a MMCG.

A close comparison to GCPL would actually be Marico. Both of these firms are trying to reinvest / extend their brands into men’s grooming. Marico has recently acquired Beardo and GCPL has started the Cinthol line of men’s grooming range. I personally think men’s grooming has a lot of potential in India (And only a ~2% penetration). I am more inclined towards GCPL, because they are also into hair care, which is another huge industry all by itself.

But my point is, make sure you understand what you are getting into. GCPL is not like Dabur or Britannia. GCPL and Marico (If they continue with their vision) are getting into new ventures by themselves. So, there is a considerable risk that comes along with it.

Maruti and Minda

I have no qualms here. These are two great companies. But if you believe the Auto industry is indeed going through a temporary downtrend, and it seems to be a bad one at that, why not just bet on the OEM (i.e. Maruti Suzuki)? Certainly, you don’t make better returns by betting on two similar ideas, so why not concentrate your energy on just the one? You already have enough companies in your PF, with some cash to boot, so you don’t need diversification too. Just a thought, but nothing to write home about.

Ion Exchange

I’m most interested in hearing about why you think Ion Exchange would make a good investment. Clearly, you don’t have to convince me. It’s the second-largest holding in my PF. But I would love to hear you out anyway.

All the best for your investment journey.