I am not tracking Sanghvi Brands at present.

Senco Gold quarterly update

- 26% YoY Revenue growth in Q2.

- Same Store Sales Growth (SSSG) which was 21% in Q1, was range bound in Q2 and at H1 level SSSG was 19% .

- Gross Margin % is likely to be range bound in Q2.

- Stud ratio was 11.4% (as against 9.8% H1.

- Launched ‘Sencoverse’ which is lndia’s first virtual jewellery showroom on metaverse.

3 Likes

Write up on Magson Retail by Progressive Grocer India Edition of October,2023.

https://nsearchives.nseindia.com/corporate/MAGSON_03112023164308_MagazineWriteup.pdf

Future outlook by management

“By 2026, MagSon plans to add 25 new stores in the stable. These stores will come up in different parts of Gujarat, Madhya Pradesh, Rajasthan, and Maharashtra, where the brand is already currently operational and has existing stores.

Most of these stores will operate under the franchise/shareholder model followed by the company since it turned public. They estimate that their turnover will touch around Rs. 120 crore in another two years from now.”

2 Likes

I have exited Studds accesories, Lotus chocolate and Borosil Ltd recently. I will enter Borosil after demerger.

Current portfolio comprises of

Senco Gold

Magson Retail

Central Depository Services Ltd

4 Likes

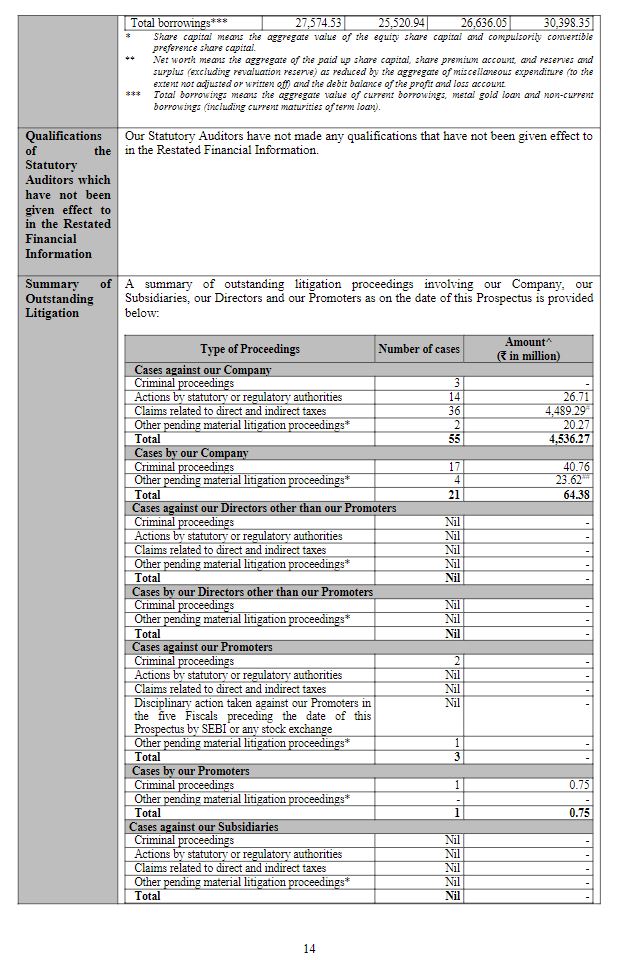

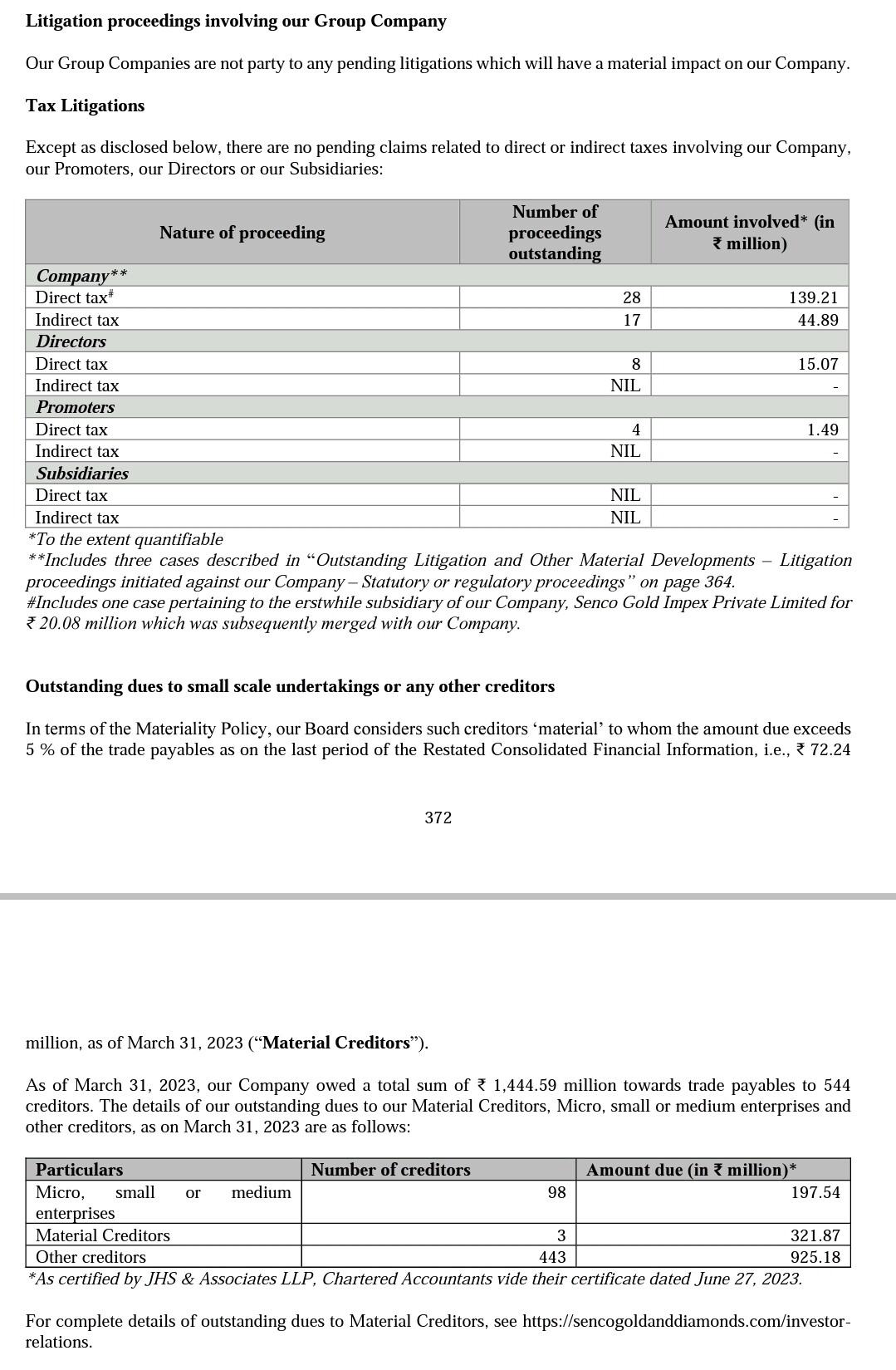

Senco Gold had helped customers during demonetisation by selling gold using old currency notes. They have come clean and revealed the names of customers, most of them have since come clean and made deposits under the Pradhan Mantri Garib Kalyan Yojana (PMGKY), an amnesty scheme.

They have also paid voluntary paid some amount regarding this and the total tax litigation remaining is not material at present. Final order related to this is still pending.

I use the parameter of Contingent liabilities to Net worth to detect off balance sheet risk. The contingent liabilities is 23.3 Cr (from Screener.in and drhp shown below) and Contingent liabilities to Net worth is 2.41% which is acceptable.

If you can provide your source of information, I will further look into it.

2 Likes

Thanks Akash, Understood. Actually I was not sure whether it would have a any adverse effect on the company profile/stock eventually if company looses the cases. By the way I also found this information in DRHP only.

2 Likes

I have taken a position in Indian Renewable Energy Development Agency (IREDA).

Detailed analysis on IREDA by a reddit user is in the link below.

Risk factors according to the same user.

https://www.reddit.com/r/IndianStreetBets/comments/184xa9b/comment/kaz2c5i/

I think IREDA is a good proxy for renewable energy projects in areas of solar, wind or green hydrogen. I generally avoid lending financial companies and PSUs but this one appears to have better prospects and is growth oriented.

6 Likes

On Navratna status: Meeting was successful and all criteria are met. Hopefully the process will complete soon.

On Retail division: PM Kusum scheme will provide solar power in agriculture. E-mobility (E-rickshaw and EV cars) financing will be done by funding NBFCs to reduce their cost of lending.

4 Likes

what is you’re take on current valuations now ,biz is very good but the p/b is very high now or maybe it’ll stay at those levels only

after getting navratna status what benefits will they get ,can you help me understand?

High valuation is a moat for finance companies as it will allow them to raise more money by providing less amount of shares. Its market cap should be at least 50000 Cr as they will fund all major upcoming renewable projects in the country.

Navaratna status gives more autonomy, improve the credit rating and exposure to the company. But since it already has AAA rating, I don’t think it will have any impact on business.

2 Likes

I have invested in Inox India Ltd. It is the market leader in cryogenic equipment manufacturing in India and among top 10 in the world.

Valuation is on the higher side at present, I will increase position size if it falls in the coming months.

3 Likes

what is you’re take on valuation gap between irdea vs rec/pfc?

Major differences between IREDA versus REC and PFC is that IREDA’s cost of funds, at 6.2% in FY23, is lower compared to 7.3% for REC and 7.5% for PFC. They can use green bonds for all of their projects whereas others can only use them for their renewable energy projects.

Further they can grow for longer duration at higher rate due to lower base.

IREDA is trading at higher valuation versus REC and PFC on PE basis at present but I will still prefer it.

4 Likes

What is their cost to income currently would be really helpful if you can tell me ![]()

Operating income for FY 2023 = ₹3411 Cr

Operating expenses for FY 2023 = ₹2242 Cr

Cost to income ratio = 65.7%

Please verify yourself, my calculation may have mistake.

1 Like

Happy New Year everyone. My current portfolio has the following companies.

| Company | Sector | Industry |

|---|---|---|

| Senco Gold Limited | Consumer Durables | Gems and Jewellery |

| Indian Renewable Energy Development Agency | Financial Services | Renewable Energy Finance |

| Central Depository Services Ltd | Financial Services | Depositories |

Every year I try new strategies. Some of investing strategies I have tried till now are:

- Index investing

- Absolute momentum portfolio

- Value investing

- IPO investing

- Special situations - Takeover and Rights issue

- Breakout strategy

- Buy and hold strategy

- Smallcase investing

- Relative momentum strategy

- Mutual funds

- Factor investing - direct and through ETF

I don’t have the temperament to follow these techniques. They do work for people who can follow them systematically. I have realized that buying growth stocks at reasonable valuations (GARP) has worked for me till now. I will try to continue following the same this year and keep distractions in control. May this year bring prosperity and joy to all.

8 Likes

I have taken a position in Bajel Products Ltd.

It was formed by the demerger of Bajaj Electricals Ltd. This is from their website:

“Bajel Projects Limited (BPL), formerly a division of Bajaj Electricals Limited, is a leading company in the Engineering, Procurement and Construction (EPC) business. The company operates through its four business verticals - Power Transmission, Power Distribution, Monopoles, International EPC and has its own world-class manufacturing facility with state-of-the-art machineries at Ranjangaon MIDC, Pune.

With over two decades in business, Bajel Projects is the go-to partner for high voltage and extra high-voltage transmission line projects, substations, UG cabling, poles, monopoles, high mast and electrification projects along with feeder separation and lift irrigation projects on a full turnkey basis.

BPL has a proven track record for its national and international business with an enviable clientele consisting of Power Grid Corporation of India Ltd (PGCIL), Madhya Pradesh Power Transmission Company Ltd (MPPTCL), Haryana Vidyut Prasaran Nigam Ltd (HVPNL), Torrent Power Ltd , Zambia Electricity Supply Corporation (ZESCO), Kenya Power & Lighting Company (KPLC), North Bihar Power distribution Company Ltd (NBPDCL), South Bihar Power distribution Company Ltd (SBPDCL) and West Bengal State Electricity Distribution Company Ltd (WBSEDCL) among others.”

https://bajelprojects.com/about-us.html

Quote from credit rating report:

“Strengths:

- Track record in the EPC business: The EPC business has been in existence for more than 15 years and due to the track record, it is qualified to execute complex projects.

- Strong order book: The company has been able to increase the order book to ~Rs 1600 crore as on March 31, 2023 from reputed customers like Power Grid Corporation of India Ltd ensuring revenue visibility for the next 1.5 to 2 years.

- Backward integration: The company is also backward integrated through its manufacturing of towers and poles, which can help the company improving cost efficiencies going forward.

- Comfortable capital structure: The company is expected to remain debt free in the near term and healthy liquidity is expected to support the financial risk profile.

- Expected financial support from parent: The company is expected to get financial support from the strong profile of the Bajaj group and expected financial support, as may be required from one of the group holding companies, Jamnalal Sons Private Limited (JSPL). JSPL has a healthy financial flexibility as reflected in its holding in various companies of Bajaj Group and low debt obligations or contingent liabilities.

Weaknesses:

2. Modest but improving profitability: Power T&D business is exposed to intense competition due to low entry barriers. Additionally, cost overruns in the past and some inefficiencies impacted profitability of the company. The company has taken several corrective actions which is expected to improve the performance going forward. Cost efficiency improvements, prudent selection of counter parties and robust pre-bid assessment of contracts are expected to support the margins going forward. While the EPC business has achieved breakeven in fiscal 2023, material expansion in profitability remains a key monitorable.

2. Execution risk: Any large-scale project deferrals or slow project execution could lead to cost overruns impacting profitability. However, these risks are mitigated by the execution capabilities of the company in the power T&D EPC segment.

3. Working capital-intensive operations: Operations of BPL are working capital intensive owing to the inherent nature of the business and the long project execution cycle of 18-24 months. Receivables are typically high in the business due to the sizeable retention money blocked in completed projects till the defect liability period is over. Receivable recovery risk is partially mitigated as majority of projects are backed by central public sector undertakings. Efficient working capital management, especially with growing scale of operations will remain a key monitorable.”

The stock seems to have consolidated after heavy selling due to demerger. Fundamental picture will be clear after the quarterly result.

4 Likes