Ajax Engineering, a concrete equipment manufacturer is doing an IPO. The issue will be open from 10th to 12th Feb and the company will list on the bourses on 17th Feb.

The Offer

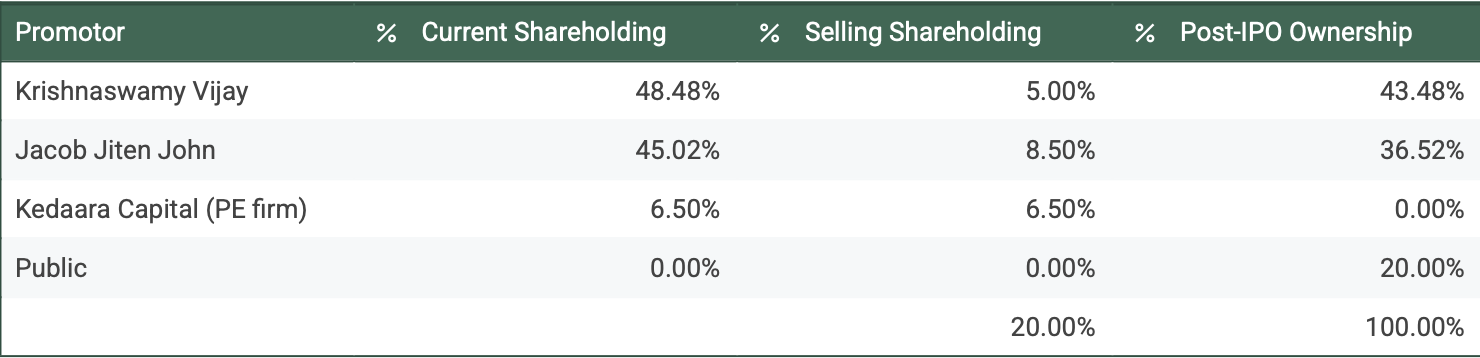

The IPO is unusual in the sense that it is entirely an OFS with no fresh issue of shares.

It sees the complete exit of its investor, a PE firm called Kedaara Capital and partial sale of shares of promoters.

Business

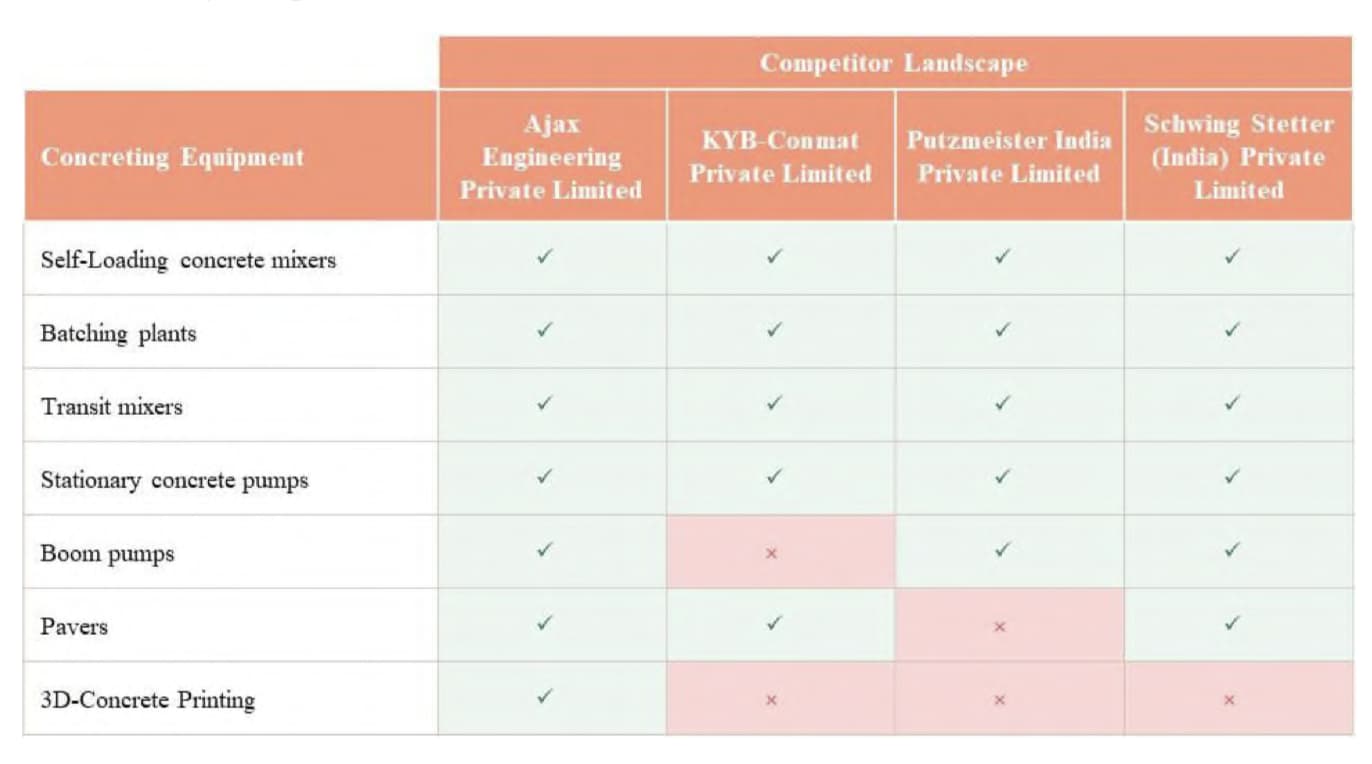

They manufacturer a bunch of different products - listed below (product descriptions are provided by Perplexity AI)

-

Self-Loading Concrete Mixers: These are versatile machines that combine concrete batching, mixing, and transportation in one unit. Equipped with a self-loading arm, they automatically load raw materials like cement, sand, and aggregates into a rotating drum for mixing. Ideal for small to medium-scale projects and remote sites, they save time and labor while ensuring consistent concrete quality.

-

Batching Plants: These facilities produce high-quality ready-mix concrete by precisely blending raw materials such as cement, water, and aggregates. Available in stationary and mobile types, batching plants are crucial for large-scale projects requiring consistent concrete supply. They automate the mixing process, reducing errors and enhancing efficiency.

-

Transit Mixers: These truck-mounted mixers transport freshly mixed or partially mixed concrete from batching plants to construction sites. Their rotating drum keeps the concrete in a liquid state during transit, ensuring it remains usable upon arrival. They are essential for delivering concrete to distant or hard-to-reach locations.

-

Self-Propelled Boom Pumps: These machines feature a robotic hydraulic arm (boom) mounted on a truck chassis for precise concrete placement at elevated or hard-to-access areas. Self-propelled boom pumps are compact and highly maneuverable, making them suitable for urban construction and infrastructure projects like bridges and high-rise buildings

-

Concrete Self-Form Pavers: Also known as slipform pavers, these machines continuously mold and finish concrete pavements without the need for fixed forms. Used in road construction, airport runways, and bridge decks, they ensure high precision and durability while reducing construction time.

-

3D Concrete Printers: This innovative technology uses large-scale 3D printers to construct buildings or components layer by layer using specialized concrete mixtures. It offers unparalleled design flexibility, reduces material waste, lowers costs, and accelerates project timelines. Applications include residential housing, infrastructure projects, and customized architectural designs.

However, almost the entire business revenues comes from one product - Self-Loading Concrete Mixers

There are three ways to manufacture concrete from cement

- On-site, Manually - Used in small sized projects where cement is mixed by hand or in small drums to produce concrete

- On-site, Mechanized - Used in medium sized projects where SLCMs are used to produce concrete from cement

- Remotely, Mechanized - Used by large sized projects where Batching Plants are used to produce concrete from cement and then its transported to the site using Transit Mixers.

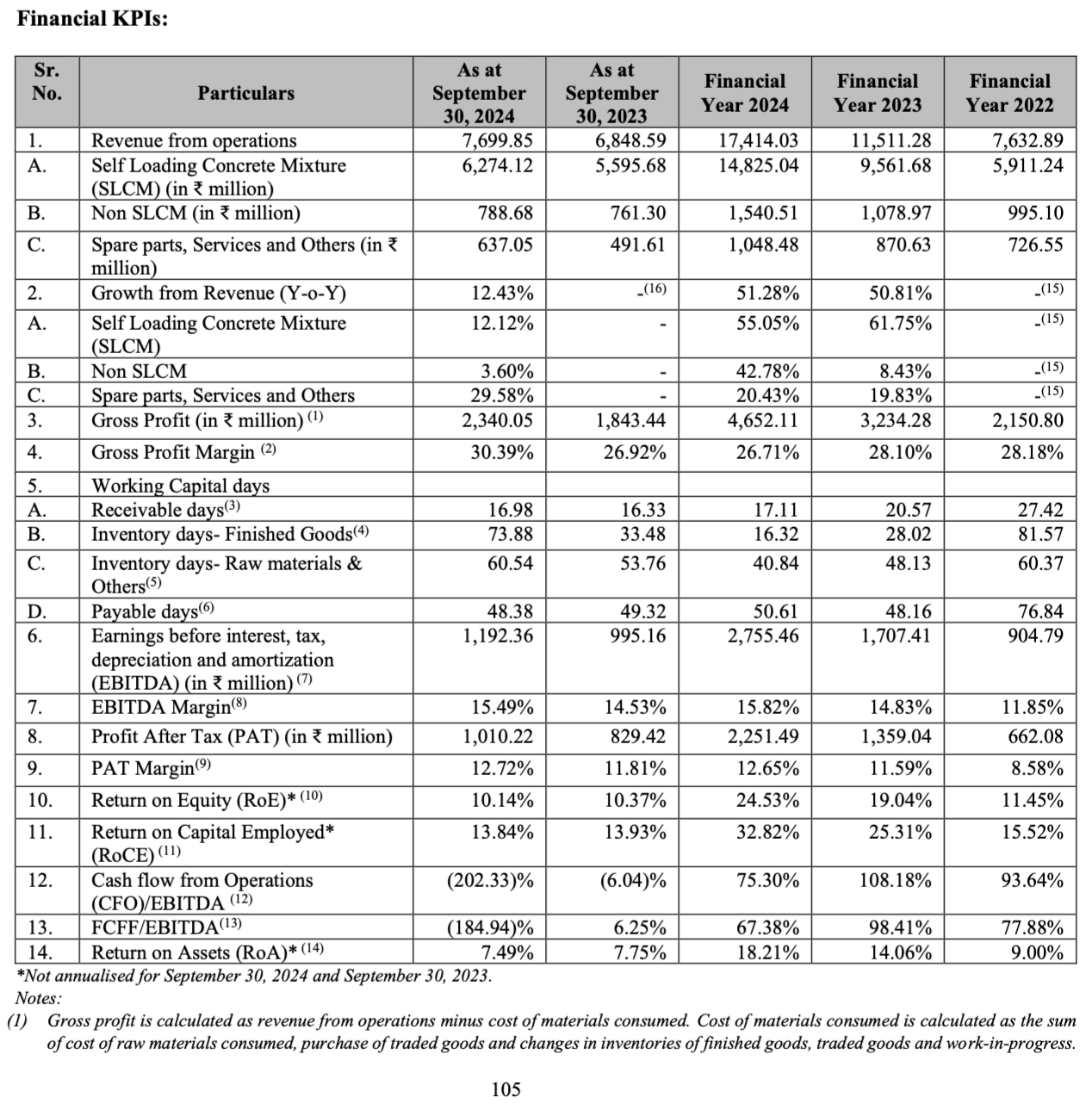

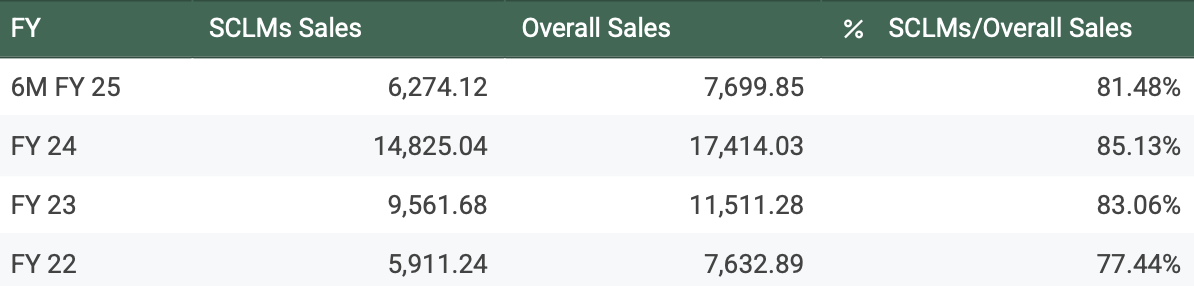

Relevant Financials

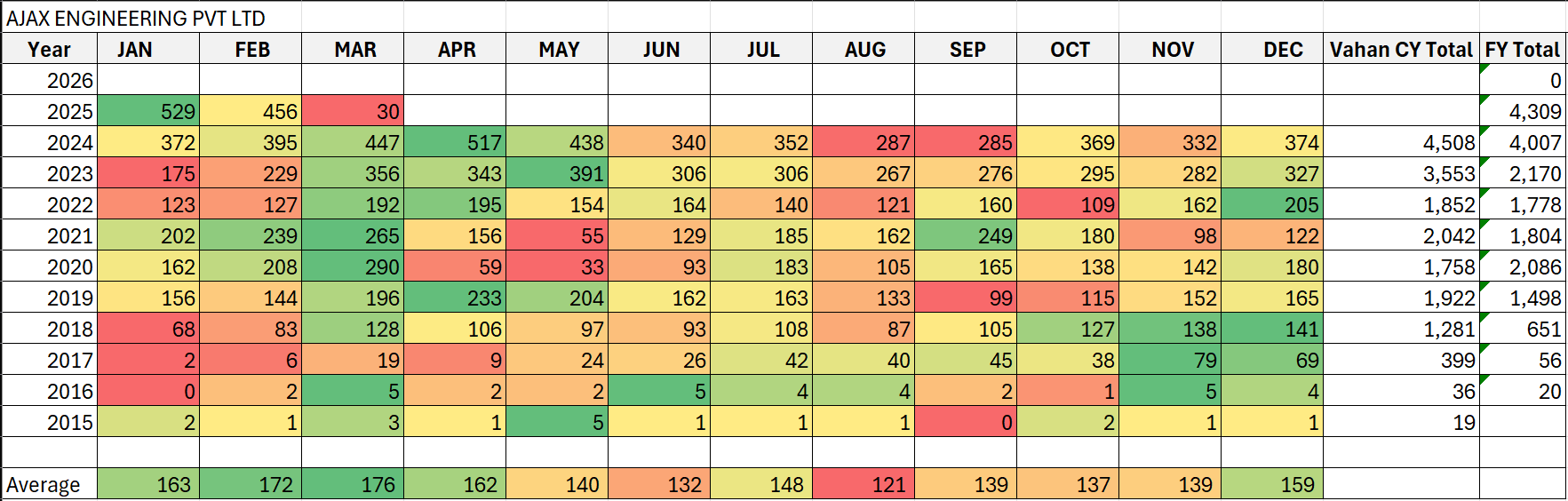

Good sales growth but appears to slowing down in FY25

FY23 and FY24 sales grew at ~50% but 6M FY25 sales grow at only ~12.5% and 6M FY25 are currently at 44% of FY24 sales which means FY25 might see a sales degrowth.

To me, it is unclear whether this represents an issue with the business or the general environment. There has been a slowdown in government infrastructure spending in FY25 due to general elections so it is plausible that it is the primary source.

Healthy gross margins and PAT

Gross margins range from 26% to 30%, giving the company lots of room to work it in terms of labour. Additionally, PAT margins seem to be creeping upwards demonstrating operational leverage (see below)

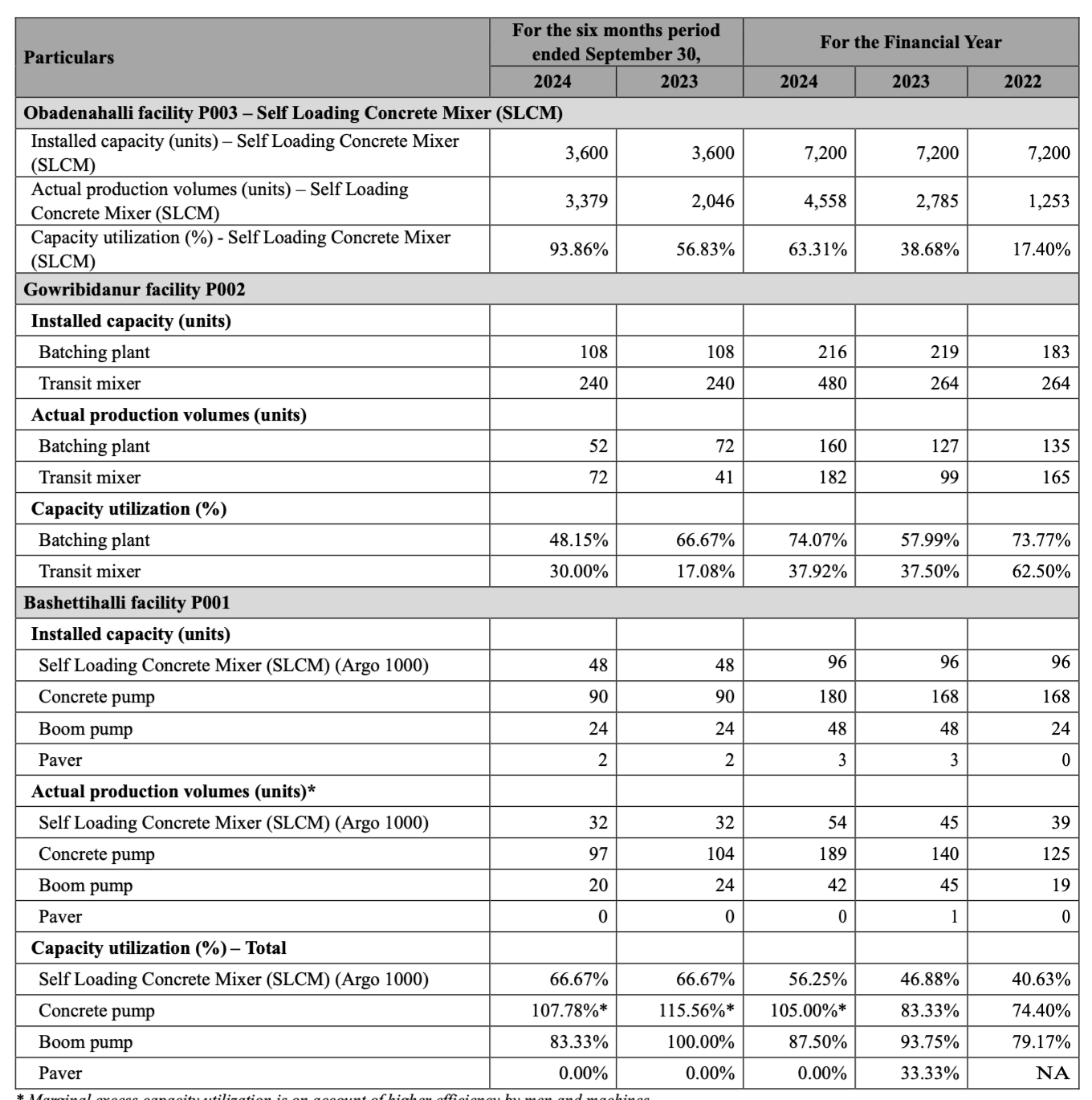

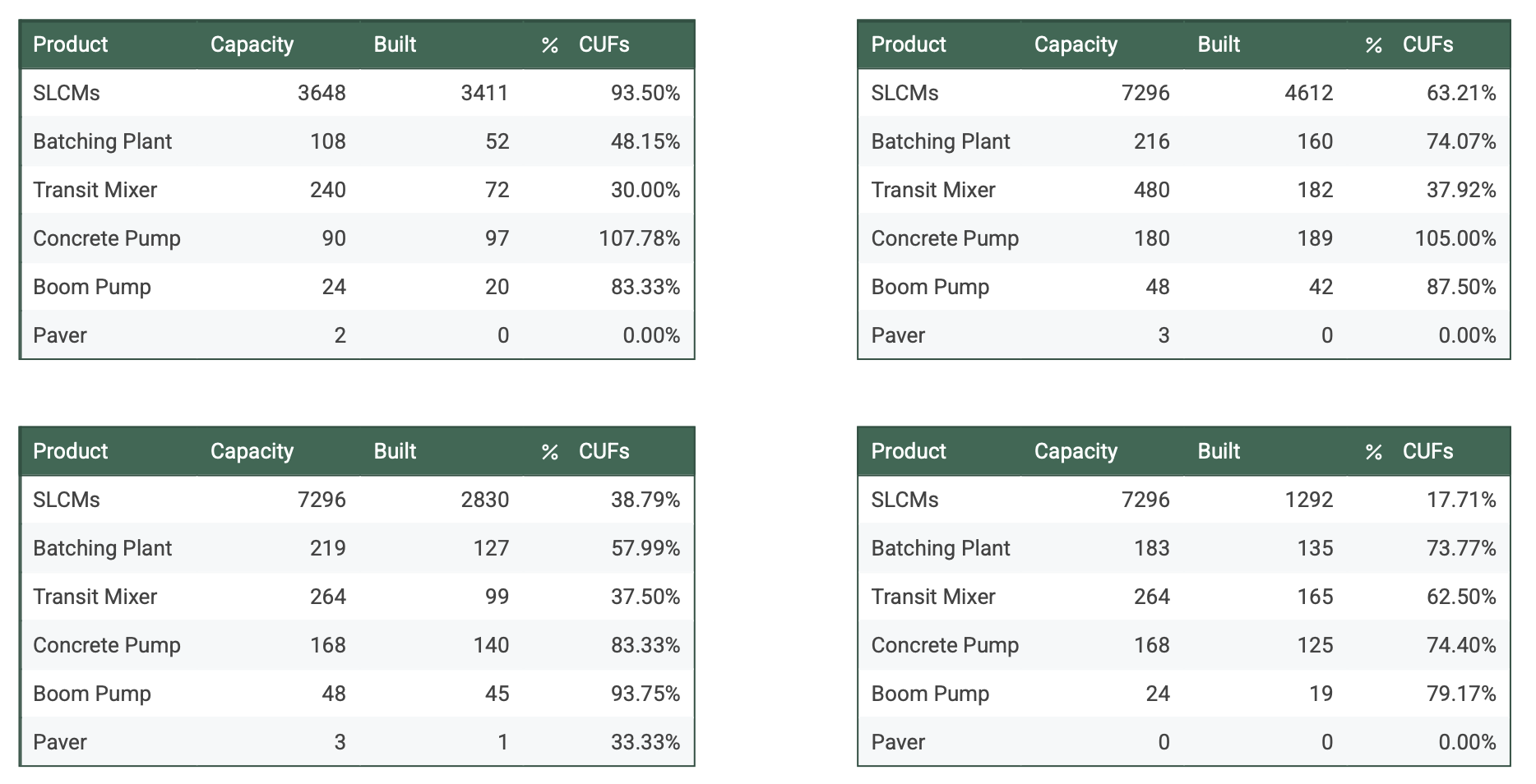

Company appears to have made a strategic decision to produce at full capacity

For SLCMs, CUF has grown from 17.71% in FY22 to 93.50% in 6M FY25.

However, while inventory days went from 81.57 days in FY22 to 16.32 days in FY24, it has jumped back to 73.88 days in 6M FY25.

This suggests that Ajax Engineering probably misjudged the demand

(From top left, clockwise - 6M FY25, FY24, FY23 and F22)

Debt free balance sheet

Company has no neglible borrowings and negligible lease liabilities

It has about ~640 cr in cash equivalents (investments + cash + other) and ~500 cr in inventory

For its Plant 4 that will be operational in March 2025, it appears that its existing assets are enough to fund it (though no details on the exact capex required is mentioned in the RHP)

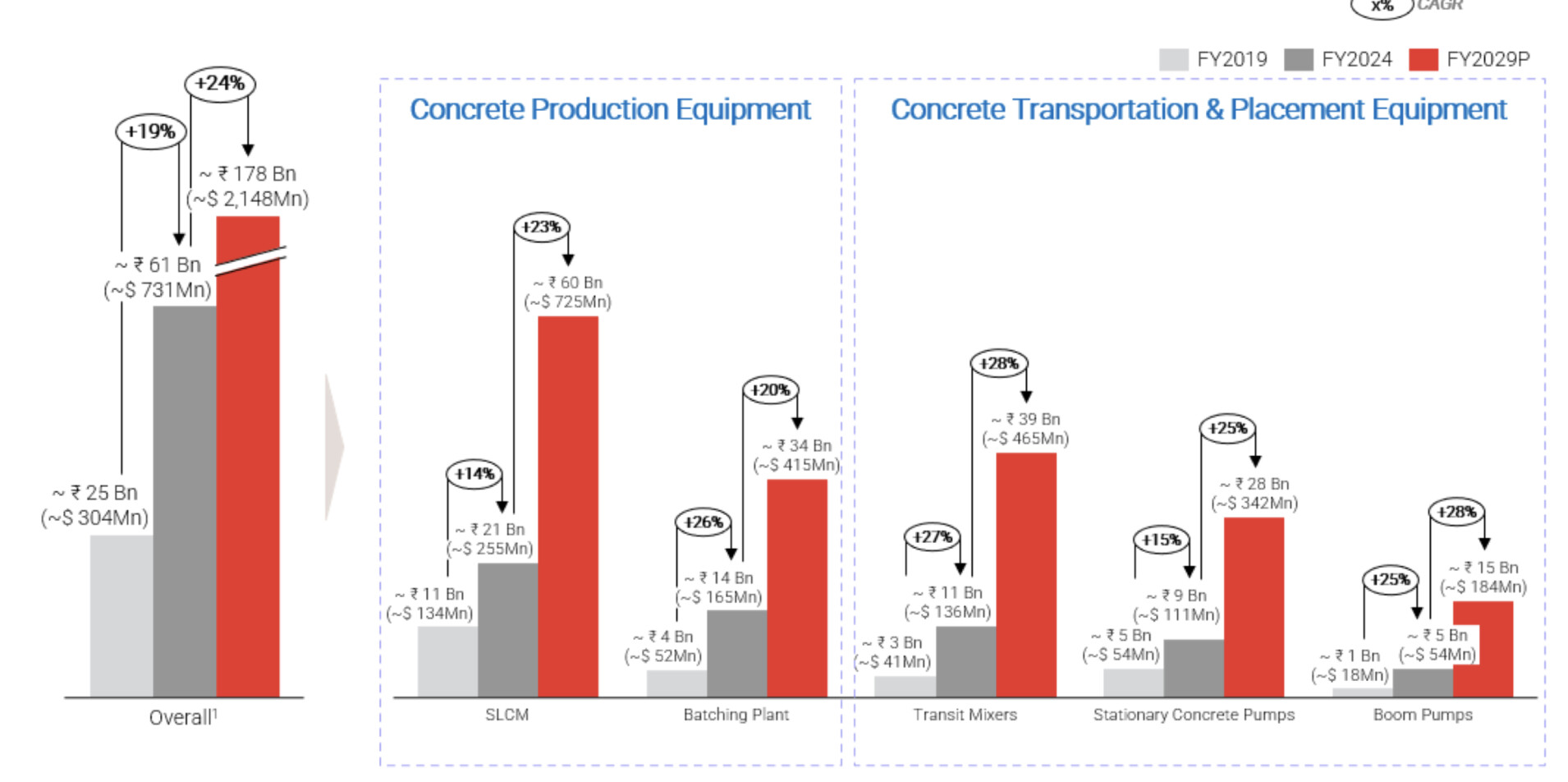

Total Addressable Market (TAM)

Company claims via Industry Overview section of RHP that 10,000 Mn INR of SLCMs were purchased from FY19-FY24. However, the math doesn’t add up with Ajax Engineerings sales figures which totalled approx 30,000 Mn INR in SLCM sales from FY22-FY24 which are 3x the growth! (the export revenue is very marginal so can’t be it)

(I’m probably missing something here - will update when I or someone else figures it out).

Risks

-

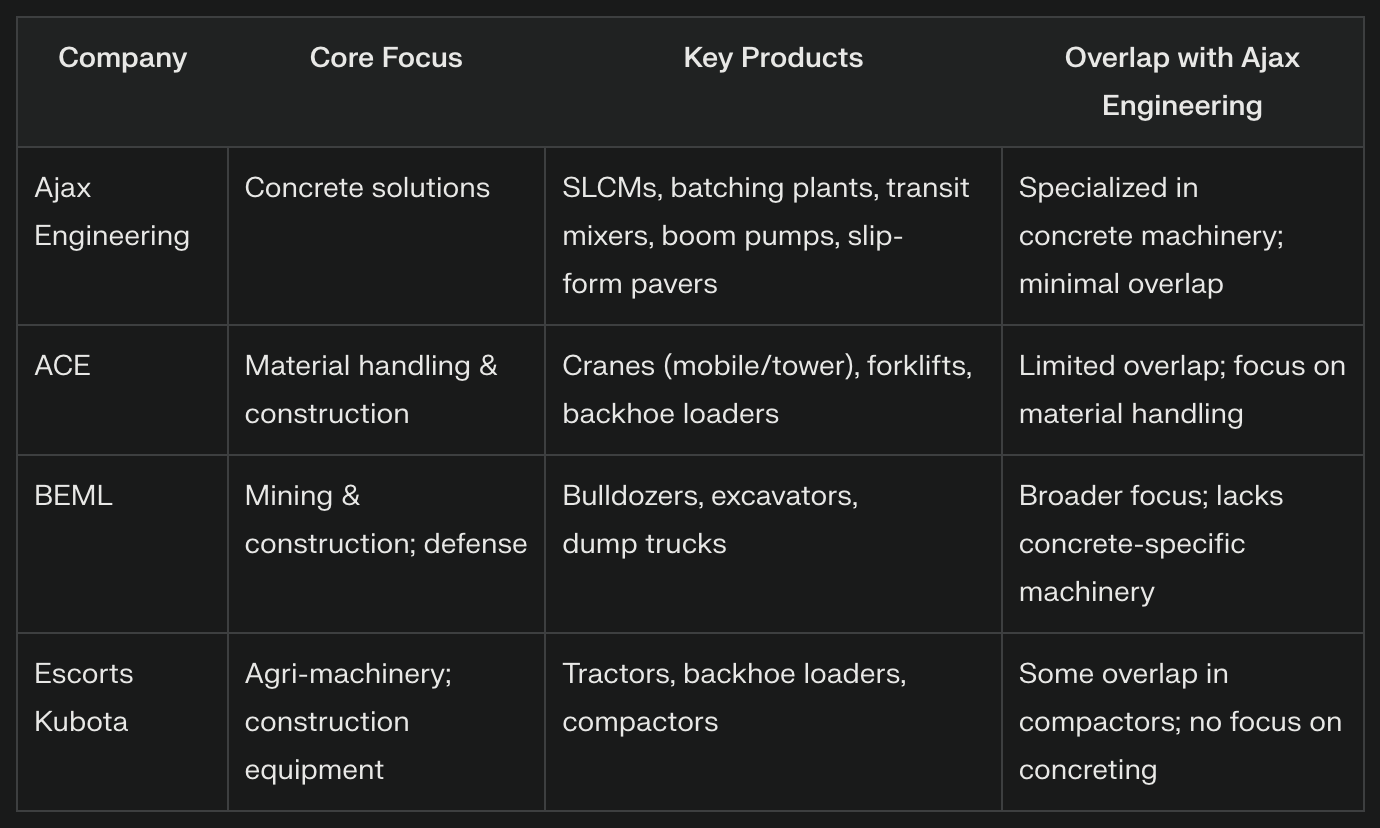

No Diversification - Almost all their revenue and their only growth driver appears to be one product - SLCMs. I haven’t looked at its peers but I am sure they have a substantially more diversified mix.

-

No Clear Growth Plans - They have not shared their capacity of their new plant in their RHP. Nor have their provided a clear picture on what the TAM of SLCMs in India is.

-

Not Clear on what SLCM’s Moat is - I am not from the construction industry so I have no idea how defensible SLCM’s moat is & how vulnerable they are to domestic and foreign competing products.

If you work in the construction industry, sharing your experiences on how their SLCM product is perceived would be extremely helpful

Disc: Not subscribing to IPO, will wait for more clarity on growth plans and moat to construct a valuation