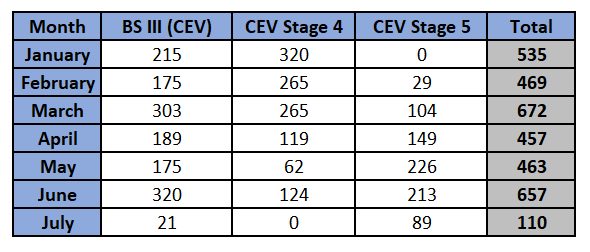

@drjpatwa - When I check in Parivahan, the CEV STAGE IV count is 124 and CEV STAGE V is 211 for June, which I think is good progress.

For July, till now everything is sold as CEV 5 with count of 66

@drjpatwa - When I check in Parivahan, the CEV STAGE IV count is 124 and CEV STAGE V is 211 for June, which I think is good progress.

For July, till now everything is sold as CEV 5 with count of 66

Does anyone have Q2 sales numbers for Ajax Engineering from VAHAAN portal?

**Company: Ajax Engineering**

Sector: Concrete Production

**Basic Details**

• Market Cap: About \~7000 crore

• Issue Price: ₹ 600\~

• Current Price: ₹480\~

• Listing Date: Feb 2025

The company has strong fundamentals with YOY increase in net profit, no debt, high ROE and clean balance sheet. Lowest PE since Feb 2025. Fall in price seems to be attributable to profit booking by investors. IPO price around 600\~ now trading at 480\~. All time high \~800. At all time low.

Can be a good medium to long term investment. No news which has justified drop in share price so much. Only stock which seems to be lending this kind of opportunity in small-midcaps(not micro caps).

Please share your views if you think there is something missing

On a high level, very good company, 1st gen entrepreneurs, IITian.

Almost a monopoly in SLCMs, very good cash flow conversion, high ROE.

SLCM as a segment in concrete industry is growing and will only expand.

But heavy dependency on Infra spent and real estate cycles.

Other risk I see is regulatory frame work on emission and sound in the urban areas going forward, because these are heavy diesel engines, and a big issue for pollution. I tried to model if battery powered SLCM can be good technology adjustment to address this, but current battery chemistry (energy density) doesn’t suit it. May be down the line

overall at this price it might be a good long term investment, I had spent lot of time around IPO , it looked a bit expensive. But might be worth relooking at now.

It’s takes century to convert to battery, ajax doesn’t have any good compitator, cause ajax can make concrete in site every location.when u can’t fixed batching plant a minimum cost of batching plant is more than 30 lakh and u need also more RMC truck to carry concrete to site.so i really close to it cause I am contractor in civil in my 15 yr experience i told you that ajax is good company.and best part if you have any problem or difficulty in your ajax company’s any machinary they site visit and repair it on the spot.

I am sorry but I did not understand regarding batching can you simplify it.how difficult it is for tata,escorts,ace,…etc to replicate and how much is the trust level on ajax .any civil contractors here can add to this question.

Batching plant is where u set a machine that automatically takes aggregate and sand cement also.without any manpower but sometimes need jcb for fill their tank or cement tank for manpower.so that also need demand if you wanna set a batching plant ur engeneer or plant machinary cost etc.or ajax doesn’t need anything it’s go can ur site with narrow lane or it’s a movable.

Issue seems drop on OPM from 13% to 10%. For newly listed company such drop in margin is disaster.

Due to that even revenue YOY increased to 48%, profit increased just 15%. What should be the reason for drop in OPM? Need to check upcoming results to OPM remains depressed than recovery may take time, if otherwise seems good investment.

Disc: Tracking but not invested.

They mentioned 2 reasons - Firstly they upgraded their vehicle to meet the new emission norms while not taking a price hike so margins dropped. Secondly they undertook a large govt like order where margins were low. They said that they expect margins to uplift in H2

Q1 Concall

Our business anyways is skewed towards the second half of the fiscal, with around 65% of our annual revenue coming in the second half. The unseasonal rains, the transition to the new emission norms, and a slower pace of project execution have all had an impact on the business in Q1 FY '26. The CEV-4 inventories, which we had built up until December 2024, was largely cleared in Q4 FY '25 and the balance was completely sold out in Q1 FY '26. With the 30th June deadline looming for the sale of CEV-4 machines**, we witnessed some highly unsustainable business practices in the industry during Q1.** However, we continued to maintain our financial discipline during this period. Also, we continued to see reasonable momentum in our CEV-5 portfolio during the quarter. We believe that the decline in the overall market share in the SLCM segment that you see in this quarter is only a temporary phase, driven by the reasons which I had just mentioned.

The 450 basis points I will attribute roughly 50%-50% or 60:40, 60% to the DMC or direct material cost change for the CEV-5 and the paver kind of having a significant contribution as well in terms of the gross margin decline. In terms of the pricing increase, I think we have been transparent and consistent over the last several conversations with all of you that we will have a closer look at the pricing as we progress in the year. We anticipate that we will be able to start nudging the pricing up towards end of Q2. The reason being that Q1, both the type of machines were available in the market, CEV-4 and CEV-5, and that obviously impacts or impinges our effort in terms of increasing the pricing when both the variants are available. July, August, we expect to be more tempered in terms of demand. And once the market kind of gets back to demand, let’s say, after Janmashtami, Ganesh Chaturthi, which is more towards the end of Q2, that’s when we would be able to push the pricing up as we progress into the market. So, while we would not be able to give a very sacrosanct view of how much we will be successful, all we can say is that we will try to bring the margin back to the corridors, which we have experienced previously.

Q2 Concall

We had sales of slipform pavers in H1 of last year, which is not there this year. Pavers are a high ticket size and higher margin product. Despite the significant impact on the gross margin level, we have cushioned the impact on EBITDA through operating leverage and cost optimization. With volumes expected to pick up as they do in the second half of the year, we expect an improvement in the margin profile owing to the operating leverage.

Q on Large Order Executed in Q2 - The large order was executed completely in Q2. There is no spillover which is expected in the second half of the year**. It was for SLCMs and 110 plus machines were as part of quasi government authority tender**. This was a very marquee project and given the size of the contract and such a large order volume, there was competitive pricing and AJAX felt that it’s in its best interest that it contributes to the nation building and also forms a grip on these large orders. This was done at, let’s say, far more aggressive pricing.

Q on H2 Margin - No, I understand. And the guidance has been given by me. So, I’ll probably just say, I am not sure. See, H1, first of all, H1 EBITDA margin is 11.7%. So, we are round about 12%. For us to get to in the range of 13% for whole year, or thereabout on the EBITDA, we will have to do close to about 14.5% to 15% for the rest of the year. And as we’re aware that H1, H2 volumes also skew differently in our industry. Then the operating leverage, does the pricing increase, which we are talking about, both should allow us to get to that margin corridor for H2.

Plz remember there is significant quality difference between concrete made out of ALCM and Batching plant..(this is what I was told by a senior manager in the SLCM equipment industry)

What this meant during the discussion was, the high rise residential building or similar structure where concrete quality is a criteria, will go for concrete from batching plant.

Q4 numbers have started to pick up. January month has seen good demand. But in no way they will be able to match the high base of h2fy25. Management mentioned in the concall.