Promoter needs some funds and wants to sell some shares. Company is supposed to buy those shares, why? Company is cash rich, why don’t they start giving dividends? Promoters will get the money they want and minority shareholders will benefit too.

The impact of buyback is similar to dividend when promoters participate except that the company does not pay dividend distribution tax. Investors will pay capital gains tax is applicable.

1 Like

3 Likes

good to see company back on track after a disastrous q3fy19.

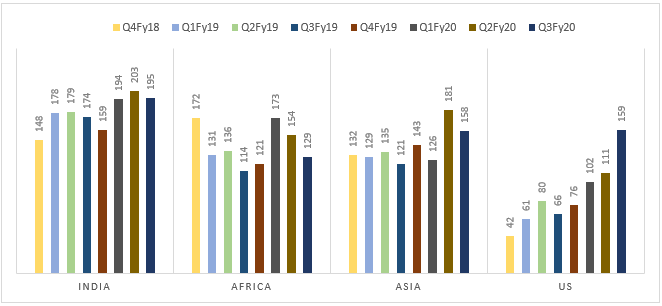

Africa branded business has degrown , from 109 cr in q4 fy18 to 75 cr in q4 fy19 ( degrowth of 31 %)

Africa instituion business has de grown 26 % yoy , from 63 cr to 46 cr yoy

Asia business showing slight growth of 9 % yoy , from 132 cr to 143 cr.

USA business has done well, shown a massive growth of 79 % yoy , from 42 cr to 76 cr .

Indian business has done decent growing 8 % yoy from 148cr to 159 cr.

overall flattish results , great performance in USA , decent performances from Asia, India , helped to mitigate the bad performance from Africa.

4 Likes

Isn’t it concerning that their Africa branded business has degrown so much?

1 Like

Yes Ayush, even I think so.

The continuous de-growth in Africa Institution was on expected lines., due to competition in anti-malarial drug contracts.

Institution has shown a massive de-growth of 49% on annual basis.

But Africa branded de-growth comes as a negative surprise.

Also, it would have been much better, if the company would have also shared profits earned from different regions, along with the revenue figures.

It would have given us an indication about how profitable their US venture has been until now.

2 Likes

The reply from management also doesn’t give any details

The decline was in line with guidance and our MDs comment in third quarter press release. Now the things have normalized and from here onwards u will see mid to high single digit growth from the region.

1 Like

news update

disc: invested

Ajanta Pharma’s AR is out.Key takeaways:

-> Company registered a growth of 16% in the domestic market as against 11% for the industry.This was led by 28 launches in the branded generics segment.9 of these were “first to market”.

-> The anti-malaria business in Africa was the worst hit.Company says it has always been forthcoming about the unpredictability of this business.The immediate future remains uncertain.

-> US business grew 46% on the back of 8 new launches.This takes the total number of “on the shelf” products to 25.Company expects to make 10-12 filings every year(13 ANDA filings in FY19) However,the cost of servicing the US market has risen and thus,Ajanta expects this market will be challenging.

-> Due to a 49% decline in revenues from the Insttl. business,the company registered a de-growth in revenues.This is the first time in 15 years that Ajanta has reported a YoY decline in revenues.

-> Company generated OCF of 375cr. which helped fund capex(361cr.) entirely from internal accruals.In Fy20,construction work on Ophthal section at Guwahati and greenfield manufacturing facility for oral solid at Pithampur in Madhya Pradesh will continue to put some pressure on margins.The total capex for FY20 is expected to be 350cr.

-> EBITDA Margins contracted by 250 bps.This was on the back of higher costs from capex at Dahej & Guwahati.The utilisation at both these facilities is still quiet low and thus Ajanta couldn’t offset the hit on margins.

-> The African markets started facing major issues two years back post Crude price decline.Thus,the company decided to fix any inventory issues they had in those geographies.Moreover,the management took a conscious decision to go slow in that market.The decline in FY19 was on “expected lines”.The US market has helped the company neutralise the adverse impact from Africa to some extent.

-> The company operationalised it’s expanded R&D wing in Mumbai.Total spend ~100cr. over last 2 years.

-> Inventory has risen due to growing US ops.The US market has a longer WC cycle.

All in all,I found the AR to be quiet subdued and “cautiously optimistic” at best.The company is preparing itself for better days(whenever they come back) …getting the new facilities stabilised and having an improved R&D centre.I got the sense that the management expects the issues in the Insttl. business to persist and thus the revenue growth may be muted in FY20 as well.On the other hand,the US market is looking good.However,higher cost of servicing and a stretching WC cycle are key things to watch out for.

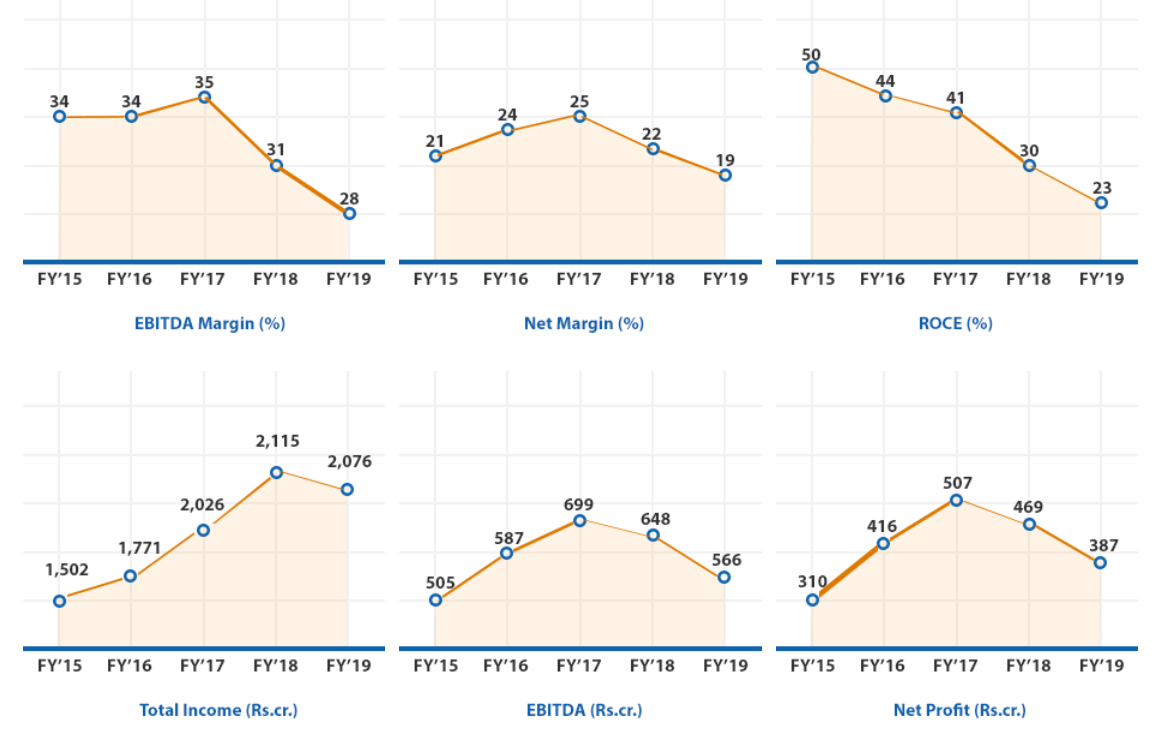

The stock has done very little in an overall weak market over the last 1 year.RoE,RoCE and margins are at multi-year lows.Imho the time to buy is still a bit away.

Disc.: Not invested.Views are biased.

13 Likes

decent set of results.

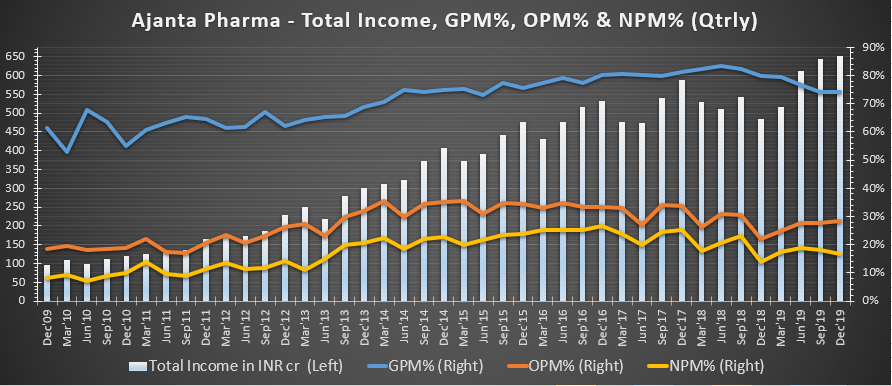

lncome from operations at Rs.612 cr. against Rs. 511 cr up 20%.

EBITDA at Rs. 168 cr. against Rs. 157 cr., up 7%; EBITDA at 28 % of revenue.

Profit after lax at Rs. 115 cr. against Rs. 106 cr., up 8%, PAT at 19% of revenue

Q1 FY2020, total export sales were Rs. 404 cr. (against Rs. 324 cr’) posting growth of 25%

Emerging Market branded generics sale was Rs.221 cr’ (against Rs.209 cr.) posting

6% growth.

Africa branded generic sale was Rs. 92 cr. (against Rs. 77 cr.) posting 20% growth.

Asia branded generic sale was Rs. 126 cr. (against Rs. 129 cr.) posting 3% degrowth.

US generic sale was Rs. 102 cr. (against Rs.61 cr.) posting 67% growth.

Africa Institution sale was Rs. 81 cr. (against Rs. 54 cr.) posting 50% growth

India sales grew by 9 % from 178 cr to 194 cr.

overall a very encouraging set of results, good to see revenue growth coming back after some dull quarters. very encouraging to see growth in africa branded business.

7 Likes

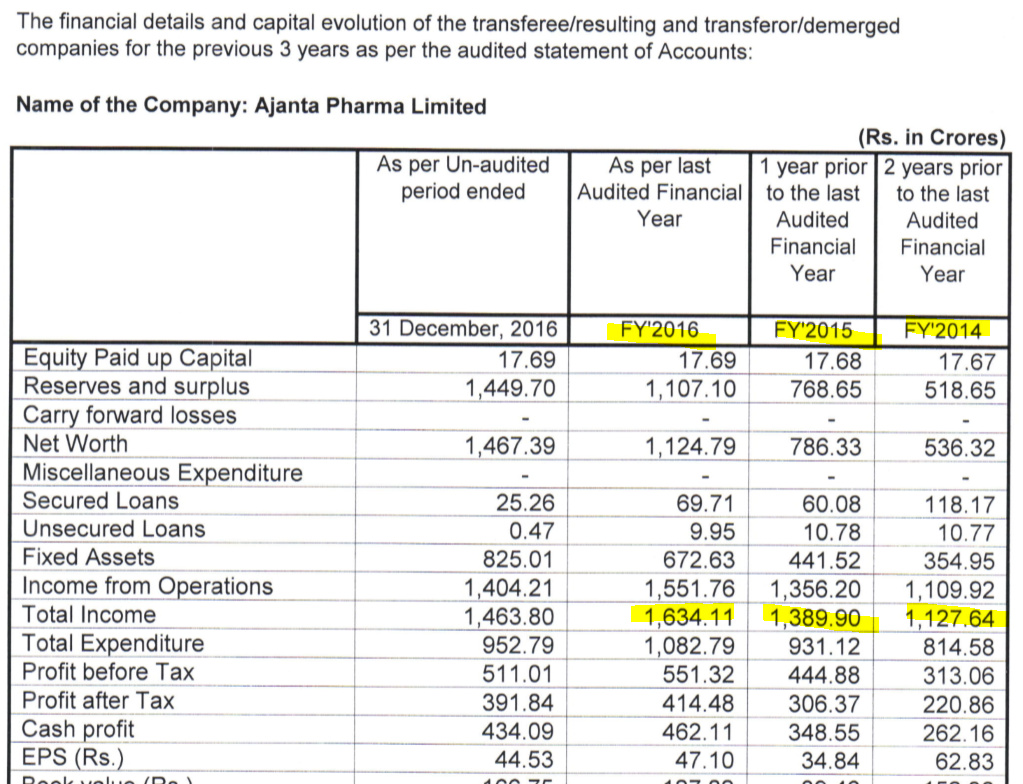

snippet from companies website :

as per screener data

top line revenue is as below

but when i saw three audited statement he number are different

source; www.ajantapharma.com/AdminData/AnalystDisclouser/StatementofAuditedFinancialsofAPLNGIPLforlast3financialyears.pdf

can someone help me to understand this @ayushmit

Isn’t this capture something market know and a an investor we don’t know ?

regards

disc: invested . this is not any Buy sell or hold recommendation

1 Like

5 Likes

Decent sales growth in Q2.Growth was led by US markets again.EBITDA fell to 28% from 31% yoy.The company has done very well in the domestic markets too.Ajanta’s growth was 16% vs. 10% for the industry.Ajanta is No. 2 in Ophthalmology in the domestic market now.The investor presentation is very good & has all the key details.

Only disconcerting part for me is the stretched WC cycle.Receivables are now at ~3 months.Company had said earlier that US market has a longer inventory cycle,but the trend continues to deteriorate.Hope it stalls soon.The numbers from Africa are a bit confusing for me.Institutional biz. surged 60% in Q2,yoy. While branded shrunk a bit.Branded sales & institutional sales are almost the same after Q2.

5 Likes

Numbers looks very good. Technically too the stock is looking very good from investment perspective

6 Likes

Better than expected Q3Fy20 on all fronts. Primarily driven by strong growth in US and Emerging Market branded generic.

- US: 140% (q3) and 80% (9m) growth, albeit on low base. Growth consistency is noteworthy. US accounts for ~20% of the sales in 9mFy20; this % to go up as per co guidance (~30%)

- India: 12% growth in Q3 and 9m; Ophthalmology, Pain Management and Cardiology reported better than segment MAT growth. However, the first time launches driven magic charm (that Ajanta was once known for) has been missing currently

- Africa: 13% (q3) and 20% (9m) growth in branded generic + institution combined

- Asia: Sales in the last two qtrs has been good; need to monitor sustainability

Source: Q3Fy20 results and presentation

10 Likes

From Edelweiss report

Key takeaways

India

AJP(Ajanta Pharma ) expects to grow 11-12% in India business over the next two years.

The company expects to launch two first-mover products per quarter.

Dermatology faced challenges three years ago where its largest brand melacare’s (anti

pigment cream) sales fell. But now it has started growing and is expected to surpass

industry growth in next two years.

US

US revenue in FY20 to be around INR5bn. The company has 27 pending approvals and

expects 25% growth over FY19-22E.

US is segment agnostic and the focus is on oral solids.

AJP has witnessed sharp price erosion in the US portfolio; however, going forward, it

expects single-digit price erosion.

The company hopes to file 8-12 ANDAs each year and launch ~10 products per year.

Currently, 10 products contribute 70% to US sales.

80% of filings are from Dahej plant.

Africa

Franco African market, the largest in export branded market for the company, is

growing at 3-4%. It is USD40-45mn market for AJP.

Asia Africa collectively growing 2x market growth.

Global fund is 70-80% of total malaria business.

Asia

This geography has faced hurdles during the past year, but has made a come back and

has normalised from this quarter. Major contributors being West and Central Asia.

Going forward mid teens growth is expected.

6 Likes

Any reason for sudden rally In Ajanta pharma in such volatile market?

Ajanta Pharma got USFDA nod for Metformin Hydrochloride tablets

Metformin is an oral diabetes medicine that helps control blood sugar levels. Metformin is used together with diet and exercise to improve blood sugar control in adults with type 2 diabetes mellitus. Metformin is sometimes used together with insulin or other medications, but it is not for treating type 1 diabetes

https://www.accessdata.fda.gov/scripts/cder/daf/index.cfm?event=overview.process&ApplNo=213651

4 Likes

Hi…

I am trying to explore some opportunities in Pharma space.

To me, Alkem Labs and Ajanta Pharma look descent at CMP.

Just a querry…

Can anyone on this thread tell me as to what percentage of their revenues come from Turkey ???

Just a little worried about the geo-political situation and the shadow boxing thats on between India and Turkey these days.

Thanks,

Ranvir Dehal

1 Like

There is no mention to Turkey in their FY19 annual report. It will be <2% (in others revenue segment)

1 Like