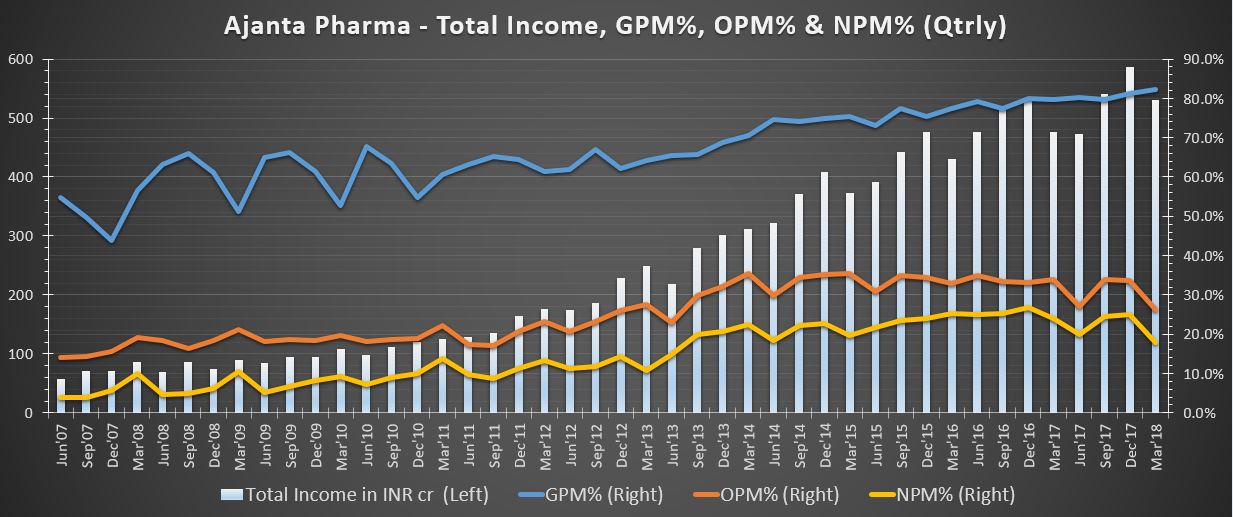

1.Indian and asian business have shown decent growth of 6 % and 4 % of revenues this quarter.

2. massive growth in Africa branded business has more than compensated for de growth in Africa Institutution business

3. US business seems to be coming back on track. Price erosion continues but slowing down

4. co. has withdrawn 3 products from US market due to its incapability to maintain the margins - shows co. is more focused on efficient use of resources rather than just increasing their top line.

5. EBITDA margin has massively dropped this quarter from 36 % last year to 26 % same quarter this year. this is because of jump in employee expenses from 76 cr to 105 cr. also because of increase in other expenses from 32 % of sales to 32 % of sales. Might be due to the expenses of operating the new facilities.

6. co. has almost completed its capex plans as of now with just 61cr remaining as CWIP.

7. working capital management was a bit poor this year with receivable days climbing to 87 compared to 61 days last year. inventory was 62 days compared to 40 days last year.

8. Assuming better working capital management next year ( atleast not worse) it will be interesting to see what the company does with 400-500 cr of free cash flows given it has no capex plans in the near future and zero debt on balance sheet. Mcap of co. is around 11000 cr, so we r looking at cash flows around 4-5 % of market cap.

Q4Fy18 Conference call highlights (from ICICISecurities)

- India MR strength at 3000+

- Total 18 pending ANDAs and two under tentative approval.

- Approved ANDAs were at 19. In FY19, the company expects to file 10-12 ANDAs in the US

- The company has drastically reduced its African tender business guidance to 115-120 crore in FY19 vs. 380 crore in FY18 mainly due to 15-20% of price erosion and reduced overall size of tender due to stoppage of procurement from some countries.

- Due to this, the company expects negative to muted revenue growth in FY19. It expects the domestic business to grow in midteens in FY19 while the African and Asian branded businesses are expected to grow in low teens. The US business is expected to grow in high mid-teens

- The management expects gross margins to remain in the range of 80-81%. However, it expects EBITDA margins in FY19 to come down to 30% mainly due to commissioning of new plants

- Guided for 24% tax rate in FY19 and ~22% in FY20

- FY18 capex was 275 crore. The management expects to spend ~250 crore every year in capex for the next two to three years

- Despite commissioning of new plants in FY18, full in house production of domestic dermatology and ophthalmology segment will start only from FY20. In FY19, the company expects 30-40% in-house production for these two segments

Source: http://content.icicidirect.com/mailimages/IDirect_AjantaPharma_Q4FY18.pdf

On the technical analysis weekly chart, seems head & shoulder pattern formation is in progress.

- Operating leverage - a relatively large change (growth) in operating profit for every INR of change (growth) in sales; kind of disproporionate growth. Ajanta enjoyed this phase in last 4-5 years.

- "Risk" of Operating leverage - a relatively large change (de-growth) in operating profit for every INR of change (de-growth) in sales; kind of disproporionate de-growth. Ajanta may pass through this turbulent phase in Fy19.

Operating leverage is a double edged sword.

That’s a really dismal picture that icicidirect has painted. Need suggestions from others on what to do with Ajanta Pharma. It is my largest holding and has been there in my portfolio since 2011,

You need to take your own call about buy/sell. No one can or should recommend what you need to do.

Please share the full article if you have access to the trailing article

http://mybs.in/2VnYWDm Ajanta Pharma: Reduction in Africa biz may offset branded generic sales

Hi @Donald

i am learning the valuation process from one your your old vauation xls file of ajanta pharma you had taking screener as your one of the source of the data for the valuation there is another data source is used in that excel could you please share from where are you getting the data for this tab of your spread sheet .it willbe a great help I know you might be bussy but i will wait for your reply thanks and reagrds

Latest Annual report is out. Any idea why there has been a lot of pledging.

http://www.ajantapharma.com/AdminData/AnnualReports/AjantaPharmaAnnualReportFY2018.pdf

Some of the pledge has already been released

I attended AJP’s AGM on Jul 5, 2018. I have tried to list everything that was spoken about. If I end up stating something incorrectly (including typos and grammatical errors) please excuse such lapses. Also kindly excuse formatting issues.

Ajanta Pharma: FY18: AGM Notes

A. Management Addressing Shareholders:

-

Three pillars on which the company grows:

- Branded generics and generics business in India, emerging markets and US

- Enhancing manufacturing capabilities

- Continuously enhancing the R&D capabilities

-

All together 30 countries contribute to the bulk of the sales / revenues of the organization.

-

India biz:

- Focus on 4 therapeutic segments – Cardiology, Ophthalmology, Dermatology and Pain management.

- Amongst the 4 segments they have a sizable chronic portfolio which most companies aspire to have.

- Consistent effort to differentiate the product portfolio by launching first of kind products. So, being the first to launch or be amongst the first few to launch new products.

- Focus is on enhancing field productivity as they go forward.

- Ranking (Mar 2018): Ophthalmology Rank# 3 / Derma Rank# 14 / Cardo Rank# 16 / Pain Mgmt Rank# 43. Overall ranking jumped to 33. Consolidated rank #32 – this despite them not being in many categories like cold, cough, antibiotics, anti-effectives, oncology etc.

- Industry grew @ 6%, they had similar growth. Growth affected by GST and Demon.

- All segments grew other than Derma. They have taken several corrective measures and they expect that Derma will start seeing growth coming back in the 2nd half of FY19.

- All segments growing at 1.5 – 2x the growth of the market, this will continue and with improved performance expected in Derma they will grow more. They will try and grow Derma at the rate which the market grows or around that in FY19.

-

Global Biz:

-

Asia: Major territory for the co. Have launched 8 products there.

- In 5-6 years, they’ve achieved good growth.

- Ranked # 17 in Philippines

- Branded business, posted 18% growth

-

Africa: 20 new products launched

- 4th largest player in Franco Africa

- Branded business grew at 30%

- Institutional biz (Anti-malarial) saw a decline of 13%. De-growth due to price pressure, a competitor that was out of the market entered the market (IPCA I believe) & took away some market share and overall the monies allocated for this program shrunk. Everything that could go wrong, went wrong at the same time.

-

US: Have received 19 approvals. 21 tentative approvals. Under approval are 18. Aspiration to file 10-12 ANDAs in FY19.

- Biz grew at 5%. This is despite heavy price erosion in the US market.

- Many competitors de-grew. They’ve managed to grow despite a challenging environment. This was due to combination of new customers and new launches.

- Management’s assessment is that price erosion is slowing doing. It should be lesser than earlier years. Going forward the price erosion should go back to single digit erosion as seen in the US market earlier.

- They are gaining market share in most of the products they’ve launched and operating in.

- USFDA inspections have gone okay so far in Paithan. No observations.

-

Branded business contributes to ~60% of the company’s revenue and is still growing (and growing at a healthy pace).

-

Dehaj facility newly launched and it is shaping up nicely.

-

New facility launched in Guwahati. The plant has already started producing tablets, capsules and derma products. The setup of the facility is still going on, there are two more phases to go. Ophthalmics and then after there will be another solid dosage facility that will come up. In the next 12-15 months, they will operationalize the rest of the Guwahati facility.

-

R&D at 9% of revenue on a higher sales base. From Rs.50 crores they’ve increased it to Rs.180 crores in the last 4-5 years. 850 scientists that work in the company.

-

In FY18 two quarters impacted biz. Q1 due to GST implementation. Q4 due to decline in anti-malarial business (Africa Institutional business). Branded generics business did well and continues to do well.

B. Shareholder Queries Answered:

1. More details on Africa business?

Large footprint in Africa. 19 markets where business can be done and the company is exporting there. Very strong in Franco Africa – 4th largest company there in fact it is the biggest Indian pharma company in that territory. In Anglo Africa, they are present in Ghana, Nigeria, Tanzania, Uganda. Still growing at double digits in the branded generics space there.

The only two big markets in Africa they are not present in are Ethiopia and South Africa. They are late in RSA and they will look at Ethiopia later as there is a still lot of head room to grow in existing African markets.

2. Capex?

They’ve been capex heavy over the last few years and will continue to remain capex heavy in FY19 and FY20 (~18-24 months kind of time frame). Capex to be Rs.250-300 crores this year and next. Monies on capex being utilized in R&D, Guwahati plant (phase 2 and 3 under construction) and they are also building some corporate facilities. Thereafter the capex will taper down and it will go on to maintenance capex as the capex on new facilities will reduce.

3. Plant in US?

Not prudent for the organization of AJP’s size to setup a plant in the US as their revenues are hardly Rs.200 crores in the US. A plant here requires larger bandwidth to manage the facilities. No reason to setup a facility there – its costly, more management bandwidth is required and it will all add up to the cost. Existing facilities have enough room to supply to the US markets.

Mapping done by management for the next 3-4 years. Existing plants and capacities are good enough to cater to the US market.

4. US market status, has the price erosion bottomed out?

Price erosion seen in the last 2 years were unprecedented, it was ~25-28%. The reason for it was heavy consolidation on the buyer’s side and supply side increased.

Price erosion is now slowing down and the base has been reset. For e.g. if the product was selling at Rs.100, it is now selling at Rs.70. This now has become the new base (as it has reset). After such a reset, it doesn’t have room to go down further to say Rs.30 – 40. This year the base will reset and the price erosion will revert to traditional erosion of ~8-10%.

To sum up, this year things will consolidate and going forward with the new base set it will revert to ~8-10% erosion on the new base.

5. 5-year outlook?

Management only spoke about the US market while answering this question. However, they’ve alluded to significant room for growth in the branded generics space in both India and Africa (double digit growth in Africa) while speaking earlier.

As per them, due to the consolidation in the US market, the company will be prudent going forward. Scenario has changed drastically in the last 3 years. The rate at which the company was looking to file earlier has to be curtailed keeping in mind the circumstances (10-12 filings being planned vs 15-20 planned earlier). However, management still believes there is money to be made in the US market if the strategy, execution and product selection is right. Many products are in R&D and the company has enough products to file for the next 3-5 years.

Company also discussing internally what will be the future growth driver in the US market (after 3-5 years).

6. Products under DPCO? Pricing pressure in India?

25% of domestic sales is coming from NELM product list.

Govt. thinking keeps on changing and evolving. This makes it difficult to predict anything on pricing pressure in India. To be dealt with as and how things evolve.

7. Plans to fill Africa Institutional business loss?

In FY19 the plan is to accelerate as much as possible in the emerging markets business.

Company was aware that the institutional business is not perpetual. It was a program for a set timeframe which had to come to an end. However, it has come to an abrupt end – something the company could not anticipate or has liked.

Whatever happens in FY19 will be the new base for the institutional business for the next 2- 3 years. The company is not looking to grow this business anymore. The focus will be to grow emerging markets, India and US going forward.

8. USFDA inspections?

Company has invested heavily to ensure the company is complaint for USFDA audits. More than 10-12 USFDA audits conducted across two facilities and the company has come out with flying colours in each instance.

Audits will keep on happening going forward too.

9. Dividend and Bonus (the most asked question during the AGM :))

Thoughts on dividend and bonus expressed by the shareholders has reached the board directly (as they were present in the AGM). It will be deliberated and the right decision will be made as and when the time arises.

No reason for the company or the board to hold back the dividend – the company has positive cash flows and a healthy balance sheet. The board felt some other effective measures should be looked at for distributing the earnings rather than dividend.

The next steps here will be discussed in the board meeting and a suitable decision on how to reward the shareholders will be taken.

The company has assured investors they will work in best / right interests of the company and shareholders - they always have and they always will. The company takes these things very seriously and it is deliberated at length during board meetings.

C. Some more stuff picked up after the AGM, enjoy

-

EBITDA margins in early 30s for AJP, why are not other companies coming in and taking a piece of the pie and hence impacting their margins?

-

Every company has their business priorities and would like to focus on a certain market. For e.g. the way Lupin has grown in the US, AJP cannot do. $500-600 mil vs $30 mil of AJP (in US). Lupin wanted to go and achieve big numbers. When put in perspective AJP derives only $30 mil from Franco Africa (for example). It cannot go beyond that. In the US one molecule can give you that much, here the entire Franco Africa market is around that (of course growing in double digits).

-

So, big companies / other competitors may not want to spend their time and effort in such markets as time and effort involved are same (monies to be earned lesser), hence they focus on markets where they can get the best out basis their aspirations and priorities. For AJP’s size this priority is best and works well for them.

-

Similar reason for AJP to be in only four therapeutic segments in India as compared to some companies being in 20-30 segments. Helps them focus, also helps them keep raw material costs lower as they only focus on a few segments (e.g. AJP’s RM are 18-20% of costs vs 40-50% of costs for players that are in 20 odd segments)

-

Branded generics business will continue to grow in every market. Many markets in Africa and Asia will continue to grow in double digits. Even India should be close to double digit growth. The aim of the company will always be to surpass the rate at which the industry is growing. Because of AJPs product selection, the company should be able to do better than industry growth. It is the same strategy the company has been following for the last 5-10 years, they will continue to do so going forward as well.

-

-

Derma segment to turnaround in 4-5 quarters.

-

Every 3rd eye drop sold in the Indian market is from AJP. Their eye drop product ranking keeps at the 2nd or 3rd spot month on month and this has been the case for years. Their eye drop gives relief in 3 mins as opposed to 15 mins earlier and hence doctors are happy prescribing them.

-

Company is focusing on products that are difficult to make and draws less competition, hence as a company they always focus on making such products to begin with. R&D’s focus has always been on making products that are difficult to make and are mostly first in any market they are present in. There are 4 such products already present in the US market. In India, 60% of AJPs products are first time in the country. This shows the company is doing something different than others.

-

Filing costs in the US have gone up from $70,000 to $170,000. Maintenance costs have also increased. Hence the company has decided to be judicious in their filings in the US (filings to be reduced from 15-20 planned earlier to 10-12 each year going forward).

-

Pledged shares of the promoters coming down directionally.

-

It is difficult to hire scientists. AJP can attract them due to their culture and the challenge which the company provides to the scientists it hires. It isn’t always about money for these guys. It’s about the satisfaction of doing something different and challenging – especially at the senior position level.

-

A new product takes 3-4 years to launch. From conceptualising to launch.

— Ends —

Disc: Invested

Drug controller allegations against the company saying without license n approval it’s selling d drugs n exchange has sought reply from the company and its awaited.

The company has replied to this. Copy pasting their response from BSE’s site.

On BSE’s website, it is mentioned that BSE has sought clarification from the company with respect to news article appearing on hindi.moneycontrol.com - July 12, 2018 titled “Drug Controller’'s Action on Ajanta Pharma”. However, we have not received any letter/e-mail from BSE in this regard.

Nonetheless, we are giving below the clarification on the news item, which we have submitted to NSE:

- There is no action against Ajanta Pharma Ltd. from the office of Drug Controller General of India and we refute the allegations made against the company in the said article.

- The action is taken against M/s. Safetab Life Sciences, who is the manufacturer of drugs. We are only marketing the drugs.

- There is no impact of this article on the Company as Ajanta Pharma Ltd. is fully compliant with all the applicable regulatory requirements.

- Since this would have no bearing on the performance or operations of the Company, the same is not required to be disclosed under Regulation 30 of the Listing Regulations, hence not disclosed.

We hope above clarifies the position.

Thanks for the update., Aman

The company has tried to come clean.

But, yet, it is completely illegal to market a drug that has not been approved by the Regulatory Authority.

The drugs that were confiscated had the label " Manufactured by Safetab Life Sciences" & “Marketed by Ajanta Pharma Ltd, Aurangabad, Maharashtra”

Let us await further details and investigation.

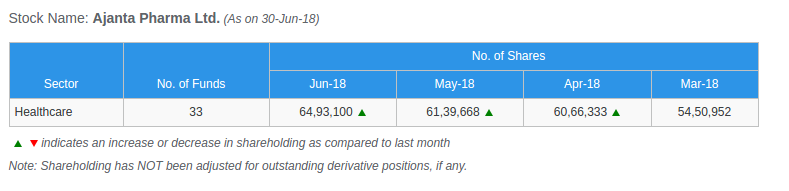

Mutual Fund holding of Ajanta Pharma has shown a increase from the last 3 months ( i.e Apr’18, May’18, June’18)

Source : https://www.rupeevest.com/Mutual-Fund-Holdings/132331

Ajanta got clearance from USFDA for it’s Dahej facility. Good days for Pharma companies on regulatory front continues.

decent set of results

good to see OPM back to 32%

Income from operations at Rs. 511 cr. against Rs. 473 cr., up 8%.

EBITDA at Rs. 157 cr. against Rs. 127 cr., up 24%; EBITDA at 31% of revenue.

Profit after tax at Rs. 106 cr., against Rs. 95 cr., up 12%; PAT at 21% of revenues.

India sales were Rs. 178 cr as against Rs.143 cr posting growth of 24%.

Emerging Market branded generic sales was Rs. 209 cr. (against Rs. 169 cr.) posting 23% growth.

Africa branded generic sales was Rs. 77 cr. (against Rs. 71 cr.) posting 9% growth

Asia branded generic sales was Rs. 129 cr. (against Rs. 96 cr.) posting 35% growth

Africa Institution sales was Rs. 54 cr. (against Rs. 97 cr.) posting 44% de-growth.

US generic sales was Rs. 61 cr. (against Rs. 54 cr.) posting 13% growth

Disc - Invested

investor presentation for the quarter

Key highlights of Ajanta Pharma’s last nine years’ Annual reports. It is interesting to see the company’s milestones and growth over the years.

Disclosure: Not invested currently.

http://www.careratings.com/upload/CompanyFiles/PR/Ajanta%20Pharma%20Limited-10-03-2018.pdf

CARE rating reaffrimed

- company trying to increase its presence in new specialty areas like segments such as ENT, Gastroenterology, Orthopedic, Male erectile dysfunction, Musculoeskeletal as well as Antibiotics.

-company planning to spend 750 cr on fixed assets for next 3 years from internal accruals. - margins in FY 19 expected to remain under pressure due to rise in fixed costs from new plants at Dahej and Guwahati.

disappointing set of results

Income from operations at Rs. 544 cr. against Rs. 540 cr., up 1%.

EBITDA at Rs. 166 cr. against Rs. 184 cr., down 10%; EBITDA at 31% of revenue.

Profit after tax at Rs. 125 cr., against Rs. 132 cr., down 5%; PAT at 23% of revenue.

India sales were at 179 cr vs 178 cr ( no growth)

Asia branded generic sales was Rs. 135 cr. (against Rs. 104 cr.) posting 29%

growth.

US generic sales was Rs. 80 cr. (against Rs. 26 cr.) posting 203% growth

Africa Institution sales was Rs. 45 cr. (against Rs. 130 cr.) posting 65% de-growth

Africa branded generic sales was Rs. 91 cr. (against Rs. 89 cr.) posting 3% growth

overall flattish results, good perfromance in US and Asia were countered by negative growth in Africa and flattish performance in India

Another quarter of disappointing results Q3FY2019InvestorPresentation.pdf (1.8 MB)

India business showing some improvement but exports across all markets is done.