J. Jayaseelan, who owns Nuray Chemicals, a maker of drug ingredients, said many Indian firms are reconsidering, or putting on hold, U.S. expansion plans.

Ajanta Pharma is one such firm. The mid-sized generics drug maker said it had no plans to scale up its U.S. business and would invest more in Asia and Africa instead.

“It’s not a major market for us right now … you’ve got to look at the risk-reward ratio,” said Rajeev Agarwal, general manager of finance at Ajanta.

The risks comes as U.S. revenue growth for these firms is falling. U.S. revenues for Indian drugmakers rose 15 percent in 2016, half the average annual growth rate of 33 percent between 2011 and 2015, ratings agency ICRA said. It expects the growth rate to fall further this year.

Consolidation among U.S. drugs distributors and a federal investigation into drug pricing have also reduced the pricing power of drugsmakers.

The U.S. drugs regulator, the Food and Drug Administration, has also banned dozens of Indian drug factories from supplying the U.S. market following inspections that found inadequate quality-control practices. Companies have invested significant sums to raise their quality standards.

Firms that want to focus on the United States will have to increase investment in higher-margin niche therapies, or products requiring specialised manufacturing, said Mitanshu Shah, senior vice president of finance at Alembic Pharmaceuticals.

“Smaller companies with a few regular products and no long-term vision for the United States won’t last,” Shah said.

Even with a vision, the U.S. market is just getting tougher for companies to operate in, said Vijay Ramanavarapu, the head of the U.S. business of drugmaker Granules India.

“You have to fight twice as hard today,” Ramanavarapu said. “It will be harder for new entrants to enter the U.S. market unless they are able to find niche areas.”

Fda issue is long term positive for sure. A corollary could be how manufacturer in Taiwan scaled up when confronted with quality issues. Trump is a bit of enigma to me - could it be long term positive as well. Buy American and hire American does not mean American corporations. If Indian pharma can establish presence in US, it could be neutral. Buy then, it would impact overall cost competitiveness.

The other way to look at it is - Healthcare clearly has tailwind and India has a critical mass that can’t be ignored. Question is who will transform fast enough… Biocon kind of bets versus traditional generics bet?

Motilal Oswal has initiated coverage on Ajanta Pharma with a target price of 2027. Here is the link for the detailed report - http://institution.motilaloswal.com/emailer/Research/AJP-20170316-MOSL-IC-PG028.pdf

US ramp up expectations seem impressive. How much can be possibly done, especially under this regime, remains to be seen.

Disclaimer: Invested

Ajanta pharma promoters pledged part of their shares

Dahej plant inspected by US FDA … At the end of the inspection, no Form 483 was issued to the Company. http://www.bseindia.com/corporates/ann.aspx?scrip=532331&dur=A&expandable=0

- PM Modi’s mandate for doctors to write only generic names in the prescription, which as a standalone measure will only shift the discretion to pharmacists.

- Doctors urging Govt. to phase out branded generics drugs.

Are not these headwinds worrisome for branded players like Ajanta and its investors ? Seniors, valuepickr pharma-specialists - please provide your feedback / thoughts.

My take on this is, and I reserve the right to be wrong, that branded generics will remain. The power will slowly move from the doctors prescribing the medicines to the pharmacists dispensing them. If the doctor prescribes a generic, and your local pharmacist tells you a certain brand is better, most people would take that. So, the focus of promotion will move from the doctors to the pharmacists, in my opinion. However, brands will remain. Even in US, people still buy OTC meds from better known brands.

Another trend may also pick up - rise of chain pharmacies like MedPlus, Frank Ross, Apollo Pharmacy etc. After a while they will start pushing their own version of generics. That is when the real pain is likely for the current branded generics players.

I was checking with a pharmacist friend and he was saying few doctors remember only the brand name and don’t remember the molecule/salt name.Now they have to brush up some text books etc again  .

.

Not sure how true this is.

The other trend which is possible is govt itself getting into launching cheaper medicines with the jan aushadi stores.

http://janaushadhi.gov.in/list_of_medicines.html

MRP of medicines looks damn low.

some state govt news launching janaushadi stores

Now, how this all pans out remains to be seen.

Last quarter concall alembic management was asked question on this and they did not view on this yet.

H/T Alpha Ideas

ARE PHARMA BRANDS EQUIVALENT?

The answer is yes and no! Brands of the same category are chemically equivalent (contain the same quantity of the active ingredient). However, there can be important differences. This is with the excipients and the manufacturing process parameters of the brand. For example, if you compare the dissolution profile of albendazole tablets, you may be surprised; Zentel from GSK is said to have the best profile. Similarly, Advanced Crocin has certain excipients to improve dissolution and consequent absorption of paracetamol into the bloodstream, when ingested.

Hi

I am a doctor. My take would be I would never recommend a generic. The government doesn’t have some institute like usfda. I would write generic and recommend the name of drug. This is because I do not trust that all the generic are equal. In government hospital there have been many instances of name being meropenem but when tested was shown to ceftriaxone second point to think doctors don’t remember the generic name might be true for only certain drugs. Say fortwin is praztozocin. But it’s not regularly used. So we might forget the generic name. But for common drugs it’s not true.

I do believe generic and brand drugs are equal but generic drugs have to be thoroughly tested and that too regularly. And I don’t see that happening in recent future

I completely agree with your view on generics. In my practice I would use only the drugs that have worked for me; be it generic or branded. Bottom line is patient should get better! The present move by Govt and Pharma sector is nothing but shadow boxing. If they were sincere they would have set up something like USFDA to control the quality of drugs and in Indian scenario the price as well. Govt is least bothered about health of Indians as you can see the budgetary allotment on health is abysmal. Yet they want quality care for common man. On one side the Pharma cos are overcharging, Govt shirking it’s responsibility and encouraging the Insurance cos to rule the roost in tandem with the pvt hospitals catering to middle and upper class citizens. Poor has to depend on the govt hospitals where the medical supply is mostly generic the potency of which is unverified.

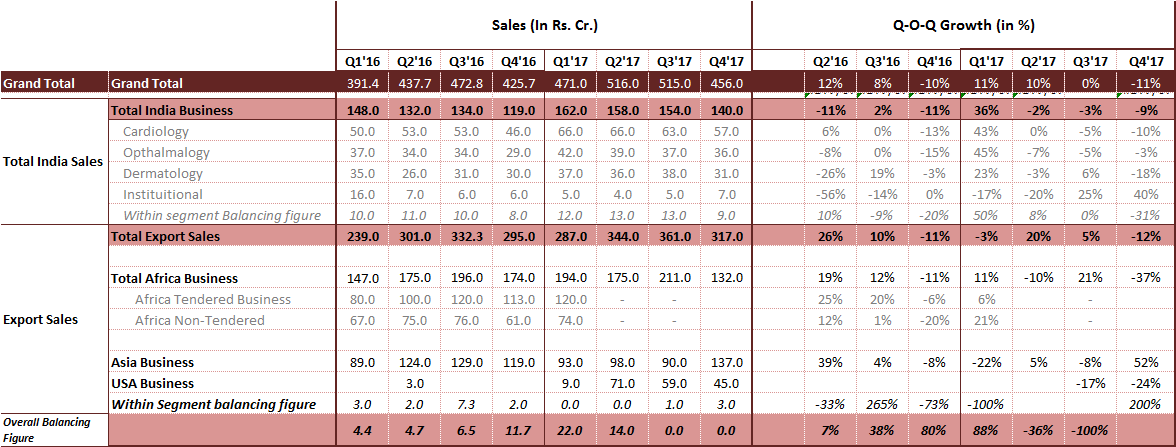

Today noon Ajanta announced Q4 and FY’17 results. Key summary:

Full year top line at 2002 Cr. Growth of 14% as compared to 17% Y-o-Y growth last year.

Segment wise break-up:

- Domestic business clocking 593 Cr. Growth of 12%. Last year also had a growth of 12%.

- Total export sales 1310 Cr. Growth of 12% as compared to 19% Y-o-Y growth last year.

- Africa market clocked 712 Cr for full year. Growth of 3% as compared to 29% Y-o-Y growth last year.

- Asia market had business of 417 Cr for full year. De-growth of 12%as compared to 3% Y-o-Y growth last year.

- Us full year revenue of 185 Cr. Y-o-Y comparison may be meaningless due to base effect. Q4 de-growth from 59 Cr. to 45 Cr.

EBIDTA of ~700 Cr for FY17. This is Y-o-Y growth of 19%.

Able to improve on EBIDTA Margin. As compared to 33.6% this year its 35%.

Hits and misses:

Guwahti facility phase 1 completed.

ANDA pipeline: So far 17 final approval, 2 tentative approval and 15 under review.

Improving the EBIDTA margin despite stress in certain geographies.

There were two dividends (Rs7 and 6) early this year. No dividends further.

I think a more granular and shorter interval -say quarterly- view will be more prudent to understand the directional drift. Here is a quick quarterly summary across segments as well:

- Domestic Business: seem that India business is struggling on a quarter on quarter basis for FY’17.

![]()

- Africa business: Little slowing down after good show for past 3 quarters.

![]()

- Asia business: Just reversed to Africa business, this one has picked up after 3 dull quarters.

![]()

- US business: Unfolding well however, currenlty is very small in entire scheme of things

![]()

Overall, seems that this will not infuse great enthusiasm for now.

Note: Have tried wrapping up this in quick 15 mins spare time within a busy working day. Possibility of error/omission etc. may be there.

Regards,

Tarun

Further granular view with therapeutically segment level quarterly break-down for India business - both in absolute rupee terms and in growth %. This surely will help understand whats working on the ground and whats not.

Attaching the entire spreadsheet where you can see the similar broken down data for past 5 Years in other tab.

Ajanta_Segments_Projections.xlsx (879.9 KB)

As you may notice, I am missing the information about Africa business quarterly break-up between tender vs non-tender business for past 2 quarters. Will be great if folks tracking AP closely can help me map this missing link. And by the way, this is one of the most crucial bit of info at this juncture, in my sense.

Disc: Holding since long. Significant part of core PF.

Thanks,

Tarun

Tarun,

Thanks for consistent excellent compilation of data.

Q2FY17: The Africa business included 90 crore from anti-malarial tenders

Source: http://content.icicidirect.com/mailimages/IDirect_AjantaPharma_Q2FY17.pdf

Q3FY17: The Africa business included 140 crore from anti-malarial tenders

Source: http://content.icicidirect.com/mailimages/IDirect_AjantaPharma_Q3FY17.pdf

Q4FY17: The Africa business included 80 crore from anti-malarial tenders

Source: http://content.icicidirect.com/mailimages/IDirect_AjantaPharma_Q4FY17.pdf

Overall African Anti-Malaria tender size has reduced. Hence, the company expects the African tender business to decline by 10-12% in FY18.

Investor presentation by Ajanta, post Q4

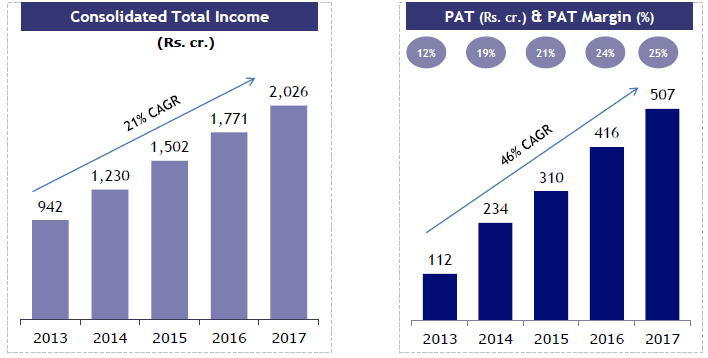

Ajanta Pharma consolidated income and profit growth is steadily dropping and now down to mid teens for revenue growth. Where is the future growth going to come from? For pharma all roads lead to US but that road is increasingly being paved with thorns.

Growing margins have partially offset slowing sales growth so profit growth is still respectable 22% but margins cannot grow forever.

Source: Company Annual Reports

Same information from company’s investor presentation.

Both charts are correct, just a difference of perspective.