humnn… so you have almost touched the Achilles heel for many of the long term AP investors, at least I am going through some thoughts specifically around this. So, here is my take:

Growth Rate:

Very true. the growth “rate” has slowed down. To help see the directional drift, here is a quick summary:

It surely will help to understand each of the moving variables separately - and importantly in respective context - to understand predominant concerns. My reading of this is:

Domestic business slowing down from comparative high growth era of 2012 -15. However, is still maintaining health growth rate wiz a wiz IPM (indian pharma market growth) as reported by IMS. Within domestic, Cardio as a segment is still maintaining >35% growth for past 5 years (except for this year where its 25%).

Africa Malaria tender: comparative slowdown however still managed a 28% YoY growth FY17. Can be under pressure going forward though on account of lower expenditure projection.

Asia - Truly a concern.

US Export: Unfolding well. High growth rate, partially due to low base effect. Not much of foreseeable roadblock at this moment. In totality, they have decent ANDA pipelines of 15 under review and recently FDA approved Dahej plant. As said somewhere in earlier post, they can do anything between average/ good/great here.

–

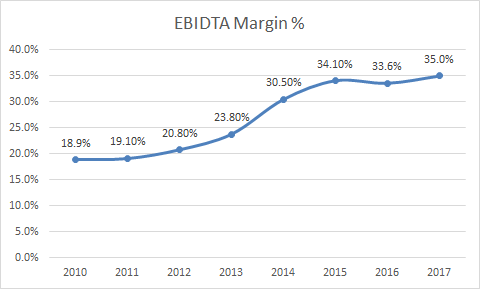

Profitability:

Another critical and equally important aspect is about profitability. What is re-affirming my faith in AP is that this is STILL able to increase the margin % despite all those top line stagnation.

In summary, I share the apprehension that in few pockets the growth is slowing down (comparative for past years, not necessarily from industry peers), and causing some uncertainty. However, some of the other fundamental tenets - visibility, management foresight, ability to execute, compliance etc. - has not changed yet for AP.

Therefore, personally I may want to give this story some more time/quarters (of course, under little extra monitoring). Looking back this may appear to be a transitory journey.

On a lighter note: even otherwise, at this stage I dont have any stock name to replace AP with. Please help, if you have something.

Disc: Invested since long. I am in a watchful state, as indicated above.

Future growth is likely yo come from US and only complex generics are left to copy there. US bound companies are spending 12-15% of sales on R&D with no set timeline on when that will pay off. If Ajanta has to follow same route, its R&D spend will increase ( = low margins) and sales growth will not pick up for some time.In short, we are looking at at least a couple of years of subdued growth both topline and bottomline. Can investors be patient enough?

Understandably, investment decisions (or deferment of the same) should not be driven by hope/wish/pray sentiments on either sides. Thanks @Yogesh_s for posing the question in this thread, this has forced me to get back to drawing board and look at things more objectively.

Spent some time to delve deep and understand one of the important piece of this jigsaw puzzle - called Africa Tender business. Whats better source of truth than the WHO artifacts to understand where we are and where all this is headed towards.

And, a follow-though detailed report-out with very comprehensive 14 lead indicators scorecard and subsequent granular data cut/info-graphics etc (cant load here, 150+ page full of info-graphics and data).

Unfortunately, Africa has a real long way to go when it comes to conquering Malaria. Approx 6 Lac mortality in 2013, mostly under age 5 in Africa. WHO target of 40% reduction by 2020, 75% by 2025.

Strategy is around three pillars:

1.Prevention, Diagnosis &Treatment

2.Country by country Malaria eradication - Attain and sustain.

3.Proactive - Information system, health management enabling optimal resource/effort allocation)

Challenges -

1.Gross lack of Funding. Total funding of US$2.9 billion in 2015 against required US 6.4 billion till 2020. Acute 55% shortage. With current state of funding not possible to clear the 2020 milestone.

2.Funding patters - Page 44 of WHO Malaria Report_2016 is enough to explaining all.

3.P. falciparum resistance to CAT observed in certain regions. Fear of spread to Africa.

4.Eruption of other severe disease like Ebola putting extra strain on already stressed infrastructure/resources.

Other notable developments:

First of its kind Malaria vaccine RTS,S/AS01 in phase 3 of development. ~40% success observed. Can be effective in early stage mortality and gradually an immune generation (in the long run)

Extrapolating these finding to Ajanta investment context:

Pledges to the Global Fund for financing for 2017–2019 have increased by 8% compared to 2014–2016 pledges.

Unfortunately, Malaria is far far away from being over. WHO own target of 90% reduction by 2030 (another 13 years from now??)

Curious to know, how does the AP/pharma veterans read the first 2 paragraphs on page 20 of the GTS document?**. Essentially, policy directive on prohibiting unapproved Malaria medicines (in retail context) to mitigate the further risk of parasite resistance to Antimalarial. Can this lead to an altogether new tender independent retail B2B/B2C avenue for AP? Or rather, what is the current size and scale of non-tender retail malaria market in the first place?

Initially I had a very long write-up on this however realized that I may be stepping on copyright issues. Therefore, strike down all. Encourage all to go through the reports first hand. Though long reports but are worth the time to understand landscape well (have also highlighted relevant parts.

Disc: Invested since long, no transaction in last 90 days.

Hi @T11, thanks for your analysis. However, your post has raised more questions than answers (at least for me).

How big is this Africa opportunities?

How much of it Ajanta can capture and over what period of time?

How much will it affect bottom line?

And finally, how much of this is already priced in?

I know that answers to these questions will be “it depends” but I try to put a value on all opportunities (however approximate it will be) so I will know if there is margin of safety.

I am not invested in this company anymore but I am genuinely interested in knowing the perspective of long terms investors as to where do they see the value.

It will be good to break down the business into the smaller segments and ask questions patiently around each of them. Few questions from my end:

There has been huge competition in the US business and price erosion has been severe for the generic players - How has the same been for Ajanta? They could get very good nos and market share for couple of drugs - what is the current status on those drugs? To be an effective player in US, cos need to have a big basket - comments of the company on the same? What kind of nos are they aiming for from US over next 3 years? Given the heightened competition in US - will it be possible to maintain the high margins co has been having?

Co has undergone a major capex - how will the new plants be utilized? Will it be for decreasing the out-sourcing or the same will be used to increasing revenues? What is the current outsourcing %?

Clarity on the Africa tendering business. There have been concerns that the competition will increase and the dream growth from this segment may stop for sometime?

Company had been facing currency headwinds in the emerging market - whats the update on the same?

As the co is relatively big now - it would be a different and difficult ballgame to grow from here and more importantly maintain the kind of margins the company has had. It would be great if the top management can share their thoughts, vision and actions around the same.

Unfortunately, I had to cancel my trip to Mumbai, due to an emergency.

I was looking forward to hearing from the management on the company’s future prospects., specially in the African tender business & their new play in the US.

The company has been a late entrant in the US generics play & would have been interesting to understand how they position themselves.

I would appreciate if anyone who has attended the AGM to share their observations / notes for the same.

Ayush & others

Any other contrasting views or should one get out.I just get an eerie feeling as a similar incident happened with Kaveri and similar reasons (personal needs) were given,

I dont know much about this. But if you look at the recent past, even eicher and pi ind promoters sold big. ( in fact it was more than this). page industries promoters have been selling for a long time and it has come down to < 50%

Thanks, just feel it is a wrong time, when pharma stocks are in the dumps.

Most of the pharma stocks that we discussed here just find it difficult to scale the 15000cr market cap barrier.

Have doubts crept into the promoters minds.

Torrent had a few observations at their Dahej plant.

Just wrote a mail to Yogesh Agarwal on what the reasons could be, I doubt if he would reply.

For the time being Ajanta Pharma is going to go nowhere in my opinion. I had 33% holdings which I exited fully in March.A racehorse like Ajanta suddenly started slowing from last Aug and it continues till date.US business needs to grow significantly to make up slowing growth in Africa and elsewhere.There are lots of headwinds for the company and the industry.After some time again it will start but opportunity cost in this market is very high so it is better to get out at the first sign of slowing growth. Page Industries was a similar story and Titan at some point.Of course everyone has his/her own views and calculations

Got a reply from Rajeev Agarwal.It says the funds were for their personal requirement and they didnt want to do it by further pledging of shares and the mail ends with “do not panic”.The business is intact.

I guess, premium valuations commanded by Ajanta has cooled of now due to derating commensurating with cool down in growth. We should wait for quarterly numbers before the story is written off… I believe if quarterly numbers dont show degrowth and if the stocks corrects 10-15% or more from these levels, it may at some point provide an interesting entry point for long-term value investors…

Disclosure: Invested but trimmed down my exposure to 50% couple of months back.

I’m surprised to see the concerning messages (got some personal emails also) on just a 3% selling by promoters when they already hold above 70%. I don’t think it means too much…atleast one shouldn’t panic. The co has an extra-ordinary track record and it should be a case study on what a fantastic work has been done in a short span of about 10 years!

Now coming to Ajanta Pharma and its prospects - I think on VP, we all have been discussing for sometime that it seems that the growth part has stagnated for the company and given the high base, it won’t be easy for them to grow maintaining the margins they have had till now. I agree with that. At the same time, I think the company is excellent. They have a branded drugs portfolio with field staff on the ground and they have very good ranking in so many regions…this should be considered like an FMCG. They have one of the highest margins in the whole industry + super efficient balance sheet.

On the growth - I like that they continue to invest + increase R&D expense and are putting up two new plants and investing more than 500 Cr into the same etc etc. But will all this translate into meaningful growth - I don’t have an answer.

I think the valuations are ok and not expensive given the quality of earnings though the future returns will depend on how they grow the business from here. But I feel we should be patient and see how things evolve.

An article in Moneycontrol.com on Ajanta Pharma’s play in the US :

Excerpts from the article :

But analysts say those days of high margins (in the US generic business) are over owing to intense competition and consolidation of the distribution channels.

“Earlier Indian generic drug makers used to enjoy margins of over 35-40 percent with relatively less competition in US, but now margins have contracted to 15-20 percent,” said an analyst tracking the pharma sector. “However 15-20 percent margins are still decent for late entrants, also given the low base, Ajanta Pharma is expected to grow much faster than its Indian counterparts in US."

Would be interesting to see how Ajanta positions its products in the US., inspite of being a late entrant.