Have spent some time re-evaluating my investment hypothesis. Summarizing some of the pointers:

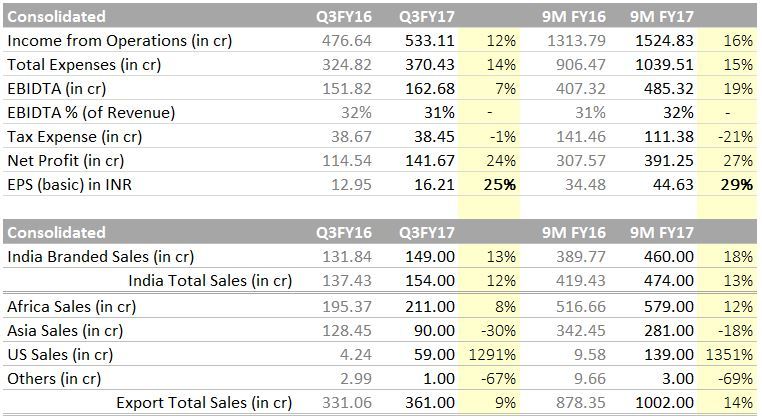

India: Overall ~13% growth from INR 420 Crs to INR 474 Cr between 9M FY16 to 9M FY’17.

- Cardiology: Almost stagnant for past 3 Quarters at ~65 Cr INR.

- Optho: 7%ish de-growth QonQ for past 3 quarters.

- Derma: Again stagnant for past 3 quarters at INR 37ish Cr.

- Institutional: Is not significant and management is moving away with intent.

Asia Export: De-growth of 18% from INR 342 Cr. to INR 281 Cr between 9M FY16 to 9M FY’17.

US Export: Unfolding well. pretty much in line with management commentary. 12 products already in commercialized out of 16 approved. Other 16 ANDA are in pipeline with additional projection of 8-10 per year for next 2 years. clocked approx. 140 Cr for 9 months.

Africa Exports: Fortunately, flag bearer of the family is doing good. 12% growth registered between 9M FY16 to 17 despite approx 30% squeezing of Artisiminin prices in tenders and currency issues.

Overall Positive Considerations:

- Recent FDA inspection and 1 observation at Paithan plat can still be treated as a positive in this environment.

- Dahej facility expected to come on steam any time soon.

- Guwahait facility phase 1 expected to be operational by March 17. Key consideration is that this facility is to cater to domestic and emerging markets. So, by extension, management is still positive about growth prospect here.

- US is going to be extremely competitive but at least FDA ghost is behind and ANDA pipeline is there. They can do anything between good to great here.

Overall Negative Considerations:

- Appears to be saturated in its own niche i.e domestic cardio/optho and darma in Indian market. (not sure if this is an outcome of they running at 100% capacity utilization and next leg of supply will come from Assam)

- Asia de-growth.

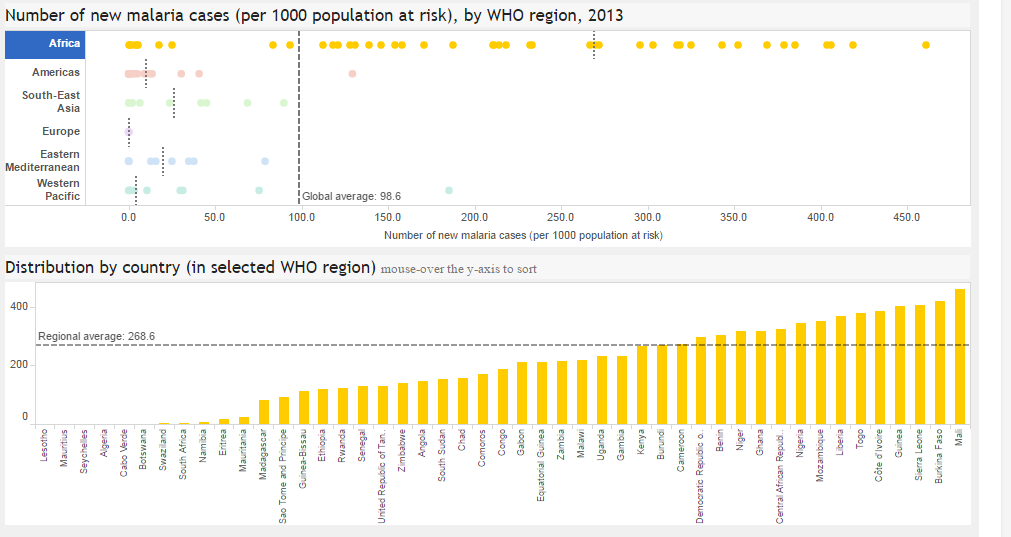

- Changing landscape of Africa Tender business. Africa’s fight with Malaria is way far from getting over any time soon. They expect a 90% reduction by 2030.

However, the challenge is that as per WHO site, in some regions of the globe, Malaria parasite have developed resistance to current set of ACT (Artimisnin combination therapy). Thus the effective/preferred approach for them is to go traditional way of vector control (mosquito net, fumigation etc.) OR expediting new drug discovery in this.

Not sure how sever this is perceived at this moment or what kind of impact these new findings will have on new tender/budget etc. Invariably, Ajanta need to be on top of the game, once again, with respect to change in finding/marketing new set of effective medicines to save the turf.

In conclusion, for now I have a very neutral kind of POV. In short term, don’t find any immediate positive triggers rather a status-quo can take it down. In mid term, I will observe for some time to see how each segments move.

Dics: Invested since long. Had some purchase within last 60 days (market was reacting knee jerk on one FDA news).