Ajanta’'s profit growth is so consistent

1 Like

Most remarkable point from Q2:

- Developed market (read US) coming from nowhere to contributing ~12% of total sales, all within a quarters time!!!

- ability to maintain 35% EBIDTA despite stress in certain geographies.

Investor presentation: http://www.ajantapharma.com/analyst-presentation.aspx

3 Likes

Akin to pulling a rabbit out of the hat ![]() (just when the doctor ordered)

(just when the doctor ordered)

How can one complain about staying put in a business like this ![]()

@ankitgupta @ananth @lustkills

Time to re-validate US Portfolio strength/sustainability

4 Likes

The revenue, profit, EPS graphs are so perfect in the investor presentation. As much as it looks suspicious, I feel if one was to do creative accounting wouldn’t they make it look just a little off… I want to continue to believe in Ajanta. I really want to.

@Donald

Sir, are you still invested in Ajanta?

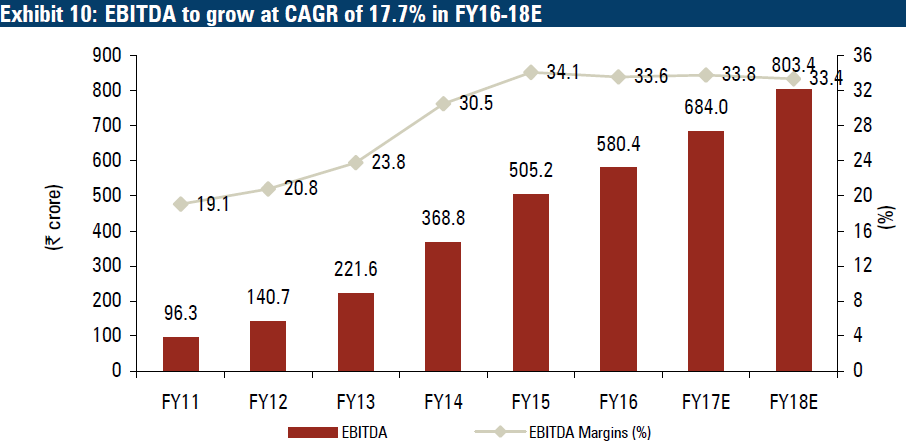

Next is the time to understand the ‘Why’. Why such high margin leading to high marked-up sales leading to best-in-class ratios? What is the MOJO?

More precisely, what has helped Ajanta Pharma EBIDTA to propel from ~19% in FY11 to 34% by FY’16?

First answers to cross the mind are…. AP is a niche player with uncanny knack for identifying the gaps, ability to fill that by first-to-market products, some top of the segment drugs (Melacare, 30+ etc.), growing far more than the overall industry/segment etc. etc.

Lets evaluate usual suspects:

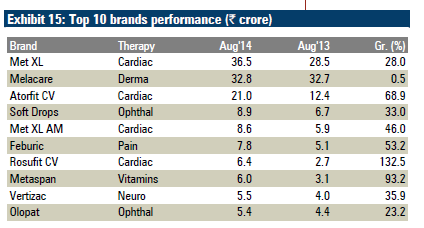

- Top of the segment drugs: Below is the table of top 10 brands of AP as of 2014. (Unfortunatelydon’t have a more Recent view).

Key thing to note is that top 5 out of those were already introduced even before 2010.

Great that these continue to top the domestic formulation chart for AP but very unlikely that they would have started improving the EBIDTA this greatly few years after the launch and continue doing so for further next few years.

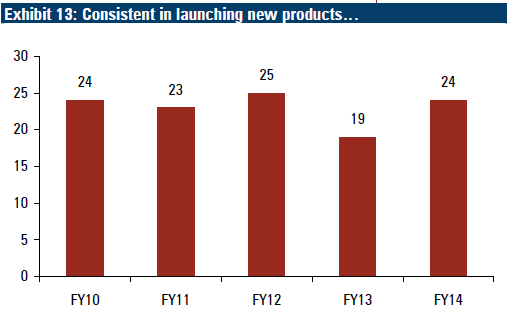

- First to launch – Agree, AP is a juggernaut churning out new products year after year. The count has been even better for FY’15 and FY’16. However, my uneducated guess is that the ‘first-to-launch’ does not mean ‘forever monopoly’. Guess, competition will try catching up sooner or later. May not necessarily displace from numero-uno but at least can eat into market share/erote margins. Even if that’s not true, keep in mind domestic business is only ~30%-33% of total revenue. Can that catapult the EBIDATA this significantly between FY10’- 16?

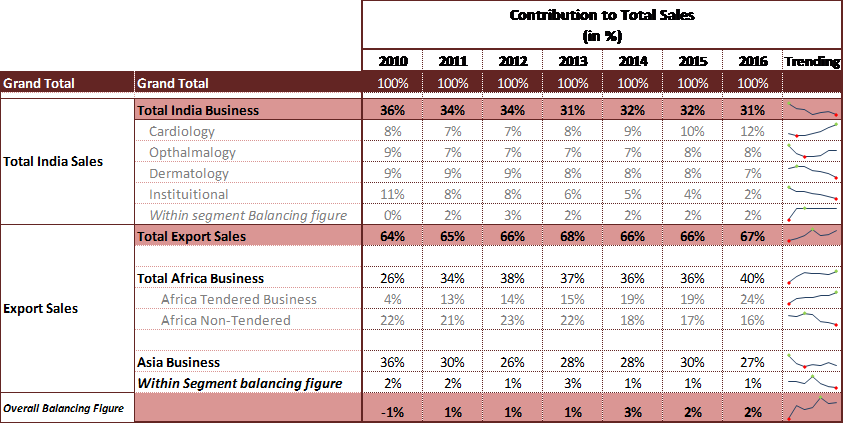

- Sum of total observation – I have tried breaking down the Total sales into segments and components within segments, if possible. What I have observed is that tender business used to contribute ~4% of total revenue in FY’10 and now accounts for ~25% of total revenue in FY’16. That too when overall revenue has grew by significant ~324%. Rest each of the segments are growing from the previous year however the growth rate in Africa tender business overshadowed all to make it biggest component of total sales.

Can this have the potential to launch the EBIDTA from 19% to 34%?

Think so, was the first generic company to secure WHO prequalification for Artemether + Lumefantrine. and Artemether + Lumefantrine tablets. It was also among the first companies to have Introduced the same composition in higher strengths. Except most recent literature its right to conclude that AP had near monopoly in malaria tenders

(P.S – out of academic curiosity, did a regression between Africa tender revenue and total EBIDTA to see the correlation. Surprisingly the R square comes out to be 94.8% indicating a reasonable correlation. Regression equation = EBIDTA (in Rs. Cr.) = 31.5 + 1.44 Africa Tendered Business

P.P. S – Regression is tricky topic with certain underlying assumption and context. Please don’t draw conclusions and projection by this reference to regression, it was more of an academical exercise to get additional perspective)

With that I tend to think that the MOJO was/is the Africa tender business.

@Donald – Sorry for the delay in getting back with promised info. Was a balancing act between busy festival time.

Attached is the segment wise revenue break-up/growth rate/contribution weightage etc. data for past couple of years for Ajanta Pharma. This also has Q1 to Q4 data in same format for FY’16. Initially I clubbed entire Africa sales together, thanks for suggesting a tender vs. non tender break-up of Africa business. This has helped immensely in having granular view.

Ajanta_Segments_Projections(3).xlsx (59.5 KB)

As takeaway, I think we need to:

-

Delve a level deep into the Africa tender business to understand firmness of the existing business (top line and margin projection)

-

clear visibility on US road map (sustainability and road ahead) for gauging next trajectory for AP.

Disc:

- AP is biggest contributor in my PF. No transaction in last ~90+ days.

- still learning.

21 Likes

Hi Tarun,

Nice work! I agree with your insights. I also think that usually such successes are rare and a combination of several factors coming together. In this case the management has done fantastic exectution on some of the following points:

- Being ahead of the market in bringing new products continously

- If a drug gets success the margins are very healthy

- They went for outsourcing at appropriate times and used it in their advantage as their brands grew on volumes

- Moved out of any of the low margin business. They don’t do APIs. They stopped doing institutional business etc etc. Just continued to focus on products which are unique and they have an advantage and can get good profitability.

Yes, the scale-up in Africa business would have been a key point. The product they are selling in unique. They were the first to introduce the same and get approval. The no of players are still just 5 or 6 even after few years and now the volumes are big.

Pharma is one area where if one has a niche product and gets volumes on the same, then the profit margins are pretty high. In this case, as all of the business is under their brand they get to capture the cream.

Regards,

Ayush

16 Likes

Ajanta gets approval for gAzor (Almodipine; Olmesartan Medoxomil) from US FDA and the same has been launched in the US market.

- Innovator: Daicha Sankyo Inc (Azor)

- Medicine to treat high blood pressure

- Azor has been retailing in US at ~$280 for 30 tablets currently; was ~$175 three years back ( www.goodrx.com/azor)

- US Market size: $174m ( http://content.icicidirect.com/mailimages/IDirect_HealthCheck_Aug15.pdf)

- Other ANDA holders: Teva and Macleods (limited competition); Torrent has tentative approval

3 Likes

Ajanta launches antifungal Voriconazole tablets http://www.walb.com/story/33645529/ajanta-pharma-announces-the-launch-of-voriconazole-tablets

2 Likes

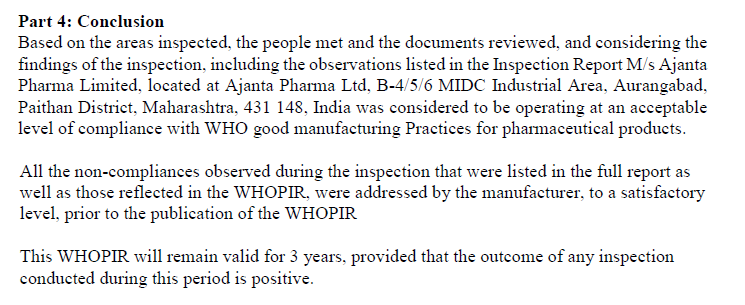

I landed at this WHO inspection report (not sure if it has been seen earlier) - apps.who.int/prequal/WHOPIR/WHOPIR_Ajanta25-28April2016.pdf . It is for a regular site inspect that’s done every 3 year or so. The result of this particular inspection were satisfactory.

3 Likes

Another ANDA approval

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=bb54f19d-def7-47e1-8e7c-090e3f03a0ab

2 Likes

Good development this.,

But, Aurobindo Pharma Ltd., Dr. Reddy’s Laboratories Ltd., Lupin Ltd., Sun Pharma Global FZE, Teva Pharmaceuticals USA, and Torrent Pharmaceuticals Ltd. had received exclusive 180 day FDA approval to market duloxetine in various strengths in the year 2013.

Cymbalta (duloxetine) generated sales of $5.08 billion in 2013, of which $3.96 billion came from the USA

The opportunity size, as of now, might not be too high., as the revenue sharing & margins might already be on the lower side.

1 Like

The gZegerid (Omeprazole and Sodium Bicarbonate) shipment activities snapshot for Q3FY17.

Source: Export Data and Price of omeprazole sodium bicarbonate to united states | Zauba

Note: Post Nov 22, 2016 export data is not reflected in Zauba and similar other sources. Seems temporary hiccup.

2 Likes

@sandeep, is the result out?

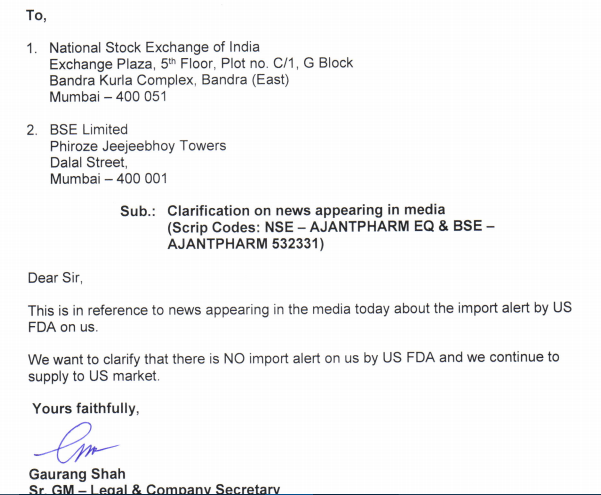

On TV now - US FDA import alert for Aurangabad plant

CNBC - Ajanta’s paithan, aurangabad unit got import alert. Stock down 13%.

Unfortunate. Quick search says it is related to Kamagra. Digging more info…

Import Alert Type: DWPE (Detention Without Physical Examination of Unapproved New Drugs Promoted In The U.S.)

Source: Import Alert 66-41

4 Likes

looks like it is only for a product which is not even selling in USA by AP.

2 Likes

Clarification from Ajanta Pharma

3 Likes

Unlike Divi, good to see company’s officials coming out to defend the FDA news -

“Speaking to BloombergQuint a company official said the import alert has been made for its sildenafil citrate tablets, which is the generic version of Viagra. “We do not sell the product in U.S. at all. It is only sold in India and emerging markets,” the spokesperson said.”

Amrutanjan bam, B-TEX ointment, Dabur Hajmola, Emami Zandu bam, HUL Fair & Lovely cream, Hamdard Safi…

You’re probably curious what are these names doing on the Ajanta thread. Well, all these products have received Import Alert of 66-41 type (i.e. Detention Without Physical Examination of Unapproved New Drugs Promoted In The U.S.) at one or other point in time. One such product is Kamagra from Ajanta (and Ajanta is not even selling it in the U.S.).

Source: http://www.accessdata.fda.gov/cms_ia/importalert_190.html

Comparing the above with Wockhardt Ankeskleswar/Aurangabad plants and/or IPCA Patlampur/Ratlam/Silvassa plants Import Alerts of 66-40 type (i.e. Detention Without Physical Examination of Drugs From Firms Which Have Not Met Drug GMPs) is an irresponsible reporting. Wrong and grossly exaggerated.

Source: http://www.accessdata.fda.gov/cms_ia/importalert_189.html

Doesn’t the news media have more important things to report about?

7 Likes