Market for Aripripazole is getting crowded. Ajanta also getting approval http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/99A38AFD_FD31_4A35_BCF2_AC4B0D119DF0_112230.pdf.

3 Likes

Can you please share your views on this :

- What has been the price erosion of Abilify until now, since going off-patent ?

- Given the present rates., can you put an estimate to the margins on aripripazole for a generic producer ?

In short,i am trying to gauge what would be the impact size of this approval on Ajanta’s bottomline.

I found the rates to be as low as USD 0.15 for a 5 mg tablet.

@mukesh_gt I am not privy to any reports/data about Abilify. Your guess is as good as mine! Torrent concall gives some hint about their share of more than 4%. He also says that the litigation procedure is going on and anything they estimate may be used in court against them. So he refused to comment on the price erosion and other related data. You may check it out http://www.torrentpharma.com/download/financials/gen_info/Transcript-Q4-FY16.pdf

2 Likes

Hope you will get some answers ( indirect though) from Torrent concall (dated 05/23). During the call many questions answers entirely around Abilify and below two answers has key indications for you.

Answer 1:…So, I would not comment on prices beyond what we have said in the past, and so I prefer not to comment on the prices prevailing in the market currently, beyond saying that they are much lower than where they were at the time of launch.

Answer 2: In the last 12 months fiscal year we have benefited from the relatively higher prices prevailing on the Aripiprazole market place. The prices during the last quarter were much lower than the previous quarters and we should all expect as additional entrants come into the market for the prices to go down, so reasonably we cannot guide you to the same level of sales in the next 12 months for Aripiprazole compared to the previous period.

Recommend you to track Torrent VP thread/AR/concall transcript etc. to decode all thing related to Abilify since they were the first to get the ANDA and exclusivity on Abilify post patent expiry.

In general, I am not entirely ruling out Abilify for Ajanta but am not expecting much form it at the same go. Likewise, not much extraordinary for Torrent at this stage from Abilify.

Disc:

- Invested in both Ajanta and Torrent, no transaction in last ~6 months on the above two.

- Still learning.

1 Like

Just realized that I am referring to the same concall trancript which @sajijohn has provided immediately before. Hope you can go through the entire Q&A from the .pdf and get a first hand sense of Torrents perspective on this. Thanks

1 Like

Understand the competition and other players…In my mind, Ajanta is principally a marketing company and should be able to draw better mileage from this approval…will keep my fingers crossed.

Disclosure : Invested in Ajanta since long and it forms significant % of my portfolio.

Dear All,

Being a newcomer Went thru all the past posts in Ajanta Pharma… Fear,hope , expectations and some fantastic analysis. AP has always surprised on the upside. Now that they have entered the US market -wary about FDA inspection issues. The track record is impeccable and yes often valuations will gallop but the Co is delivering QoQ and YoY. So no complaints.Thanks to VP for providing a clean forum on knowledge sharing

Disc- AP forms 22% of my portfolio

2 Likes

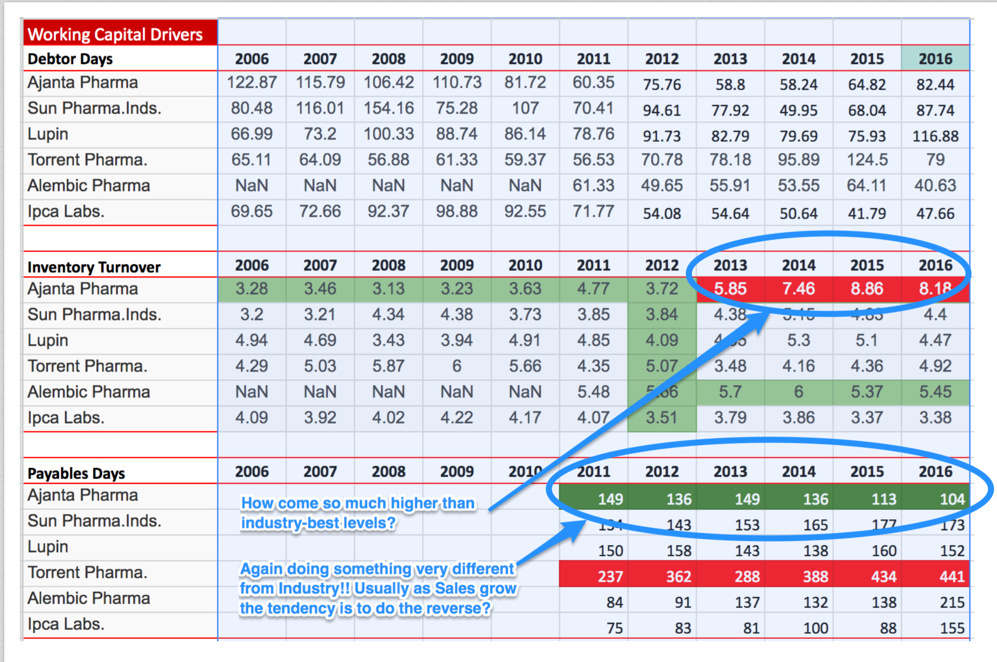

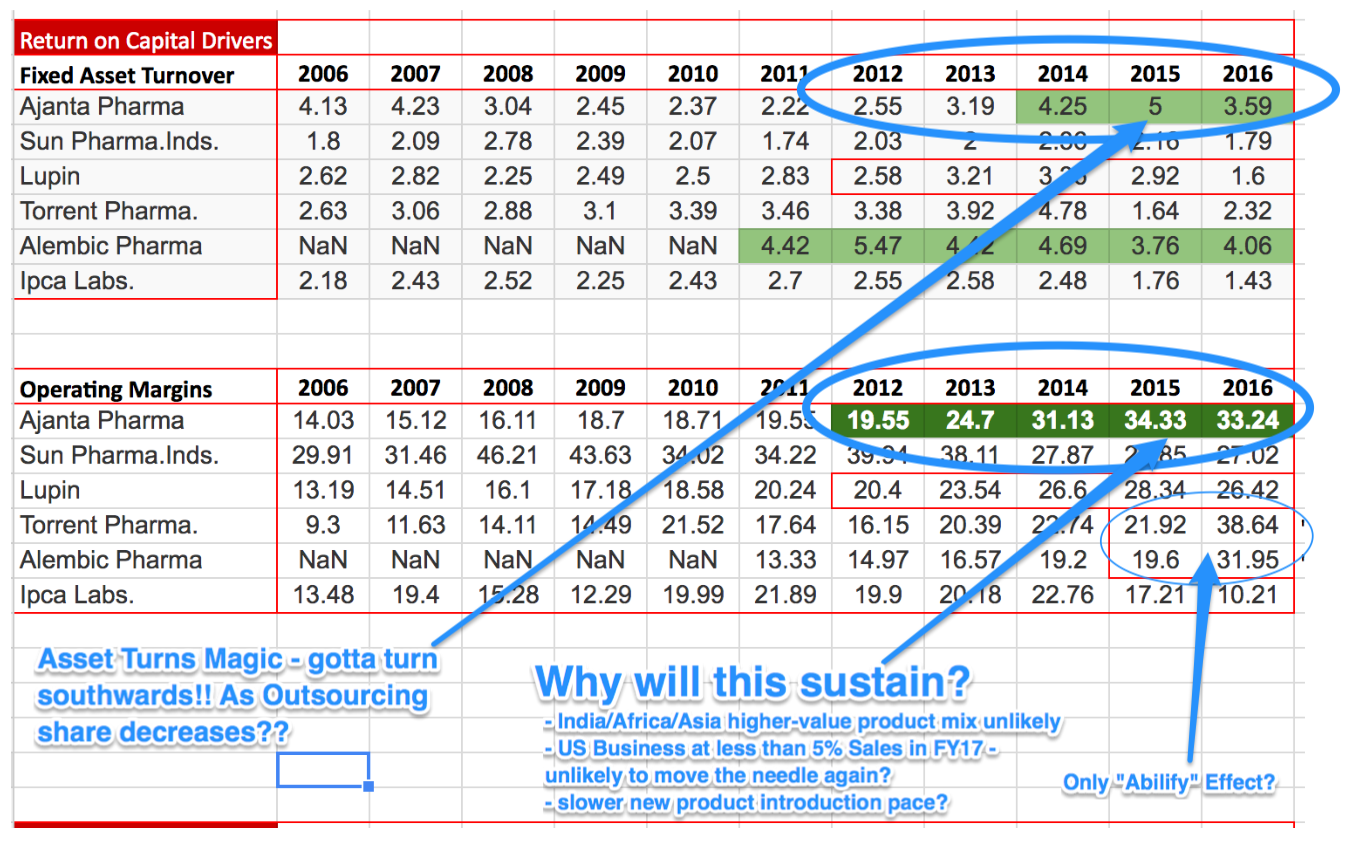

I started re-looking at Ajanta Pharma picture - to re-visit our earlier assumptions.

There is a un-stated objective from Management - to emulate Sun and Lupin benchmarks - in its strive to go to the next level

While it is clearly faltering in Topline growth (which may be temporal, and we need to understand from Management what they are doing to set things right - they have always been growth-hungry, creating avenues when they don’t seem to exist), I am more worried about Sustainability of Op Margins from the lofty 33-34%

PS: will be hopefully posting a few more such EverNote Notes (falling in love here) - to help bring everyone on same page - and help us become willing to expose the thinking behind our “Assumptions” about a business

Data Source - Screener.in; while there may be some discrepancies, broad trends should be in-line; please ALERT if you spot major discrepancies

16 Likes

Here’s a look again at Ajanta’s superior Asset Turns and Operating Margins

Why are we sure this will sustain?

Can we examine the assumptions we are making behind such conviction/opinion??

Disc: Invested, but cautiously re-examining

No transactions in last 30 days

9 Likes

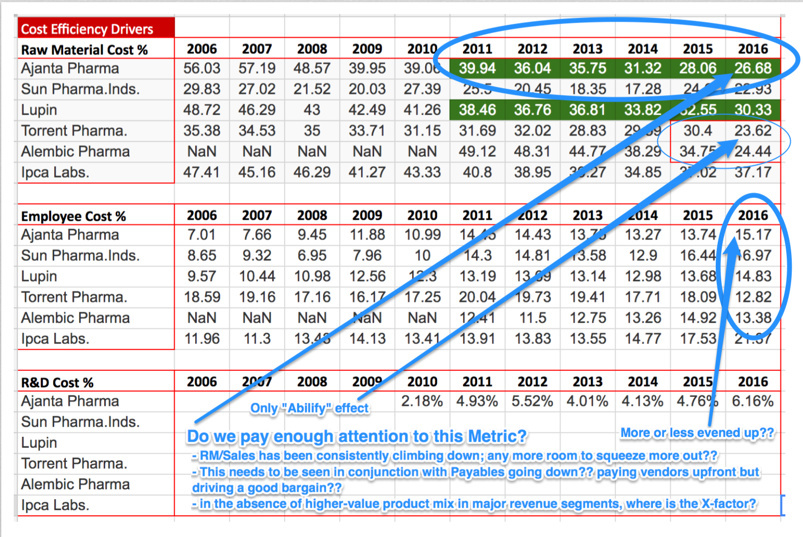

And another look at the Cost-Efficiency Drivers

What assumptions are we making in the sustainability/betterment of the same??

Don’t have the time to complete the R&D Expenses snapshot - upcoming travel.

Hoping some of you will be inspired to take this further - and throw in more data/expose the assumptions we inherently make behind a continuity picture ![]()

Attaching the Excel data - for you to tinker around

Ajanta_Assumptions_Picture.xlsx (50.4 KB)

Disc: I have a completely OPEN mind at the moment; but as is my wont, wanting to QUESTION HARD!!

All interested/invested/tracking can help ![]()

13 Likes

Hi,

With great caution I am trying to take a stab at this for two eminent reasons.

a. The nudging came from someone whom I hold in high esteem for two qualities (hard and detailed work, eloquence). No flattery by the way.![]()

b. Equally importantly, AP has proved to be best workhorse in my PF. As a result over a period this has become significant % of my total PF. Gotta behave circumspect.

@Donald – Always helps to challenge the trap called complacency. Glad that you still want to short of play devils advocate here.

In the true spirit of ensuring a productive outcome from this exercise (looking at some of the ration/metric to see how much steam is left), I am trying to firstly establish that all of us are looking at the numbers from same and correct vantage point.

So, here I go………at some places I am observing some ‘significant difference’ between your quoted numbers and what I have observed from Morningstar. I am concluding that you have taken the standalone numbers from screener, whereas Morningstar has consolidated numbers. Having said that, difference between the two should not be this wide (since consolidated is ~only 10% higher to standalone topline for FY’16).

Apologies the format is not perfect, posting from mobile and facing technical issues. but dont want to miss the important points for semantics hence just “jugaad-ed it”.

Somehow, it appears to me that Morningstar data is closer to reality. Cross verified the RONW and Inventory turnover numbers from the Q1FY17 investor presentation and both set of numbers are stacking up pretty smugly.

Now, to answer the direct question, will the investment be equally rewarding going forward?

To answer this, for a moment I am taking the liberty to consider Morningstar as my reference data:

- Growth/De-growth:

Bottom line: Looking closely at the numbers, AP has improved the margins at all levels consistently till this year. Gross margin from 63% to 73% between FY12-16. What does that means? To me, company ‘still has pricing power by virtue of first-to-market strategy’ Equally important, AP has gained significant operational efficiency across each of the possible steps (operating margin 14% to 32% and Net profit 12% to 24% between 2012 to 2016). By extension ROA/ROE/ROIC each followed a northward journey.

Now, at this juncture, and in context of Morningstar data, I tend to believe that any further squeezing/efficiency may be little difficult since they are mostly far superior to peers and industry best in some cases.

Top Line: On the other hand, FY’16 top line growth of 16.68% is on the lower side by AP benchmark. Even FY’15 was nowhere close to peak ~35%ish growth. Historical top line growth trend:

FY16: 16.68%

FY15: 22.53%

FY14: 29.81%

FY13: 37.41%

FY12: 34.17%

As expected, that’s why we have sign of stress on DSO, assets turn over, inventory turn over etc.

Coming to your well intentional questions (food for thought), after connecting the dots, IMHO for AP the question to be worked upon further is related to avenues for top line growth more than improving/sustaining the efficiency/margins.

Specifically on top line growth, Ajanta’s USP has always been:

a) Introducing first-to-market (approx. 70% of 190 branded formulation so far, if I recall correctly).

b) Targeted marketing effort (country/geography specific go to market approach).

What I have observed is that AP is ‘slightly’ moving away from its forte…i.e. the first-to-launch margin rich new formulations in the underdeveloped/developed markets (read Africa, Asia). Somewhere seems that company is now aspiring highly regulated, competition intensive USA market via ANDA route. Upcoming Dahej facility (coming to steam in FY17), already filed 18 odd ANDAs and stated aspiration to file ~8 ANDA per year for next 3 years etc. all are indication of STRETCHED FOUCS towards US market.

Though by management commentary and even by notes from AR, seems that management is still intends to play by strength (first to market products, below radar marketing, underdeveloped markets etc). However, will be interesting to see how much successful they will be in the fine balancing act.

Attached is a template that I use to evaluate any prospect (standalone and within sectors) thanks to Pat Dorsey.

My investment hypothesis for Ajanta is entirely based on the success/failure in getting top line traction. Do let me know if I am missing something in concluding that issue worth evaluating is top line growth NOT bottom line incremental improvement.(I.e raw material cost℅,employee cost℅ etc.)

MS Consolidation Sheet_Pharma.xlsx (25.6 KB)

Disc:

- AP is significant (~18%) of my PF. Averaged-up periodically since first position. No transaction in last 1.5 years.

- Still learning

15 Likes

I loved your template. They are absolutely best in everything. Their ROE and ROIC’s are matched by only Torrent and Alembic which also includes the effects of blockbuster drugs. Next year picture should make AP the best in even those. As Donald pointed out we have to find if the OM will sustain or not in future. You guys are Godly in raising the questions related to business also. Deep respect

Kanv

Ajanta Pharma Guwahati Facility To Be Ready By March

Drug maker Ajanta Pharma said its new formulations facility at Guwahati will be commercialised before March 2017 and the Dahej manufacturing facility, mainly dedicated for developed markets, will be operational in next financial year.

“Our new formulations facility being set up at Guwahati with a capex of over Rs. 300 crore to cater to India and emerging markets will be commercialised before March 2017, which will enable us to build our strength in

manufacturing and get more tax efficient,” the Mumbai-based company said in its annual report.

The facility will produce tablets, capsules, creams/ointments and sterile ophthalmic liquids.

“The company is also adding manufacturing capacities for different markets. The Dahej manufacturing facility mainly dedicated for developed markets, will be operational by FY 18,” Ajanta Pharma managing director Yogesh

Agrawal said in the annual report.

With substantial investments of Rs. 106 crore in R&D in 2015-16, use of latest platform technologies and developing niche and complex formulations, the company is confident of reinforcing its exclusive positioning in the markets it operates in.

The company has a strong presence in the branded generics space in more than 30 emerging countries across India, Africa, CIS, Middle East and South East Asia, generics in developed markets of the US, and institutional sales.

The company has stepped up its presence in the US market with a select product portfolio.

It has 26 abbreviated new drug applications (ANDAs), out of which we received 8 final approvals and two tentative approvals. “We are awaiting for approvals of 16 ANDAs and plans to file 8-12 ANDAs every year for every year with the US FDA going forward,” Mr Agrawal said.

The company plans to remain focused on few high growth specialty therapeutic segments in India and building leadership in cardiology, dermatology, ophthalmology and pain management.

In the emerging markets, its vision is to provide differentiated products, customized to suit individual marketplace with a bouquet of 1400 plus product registration in hand and another equal number under approval, the company said.

2 Likes

Sorry for the delay in replying - busy travelling before and last week festivities.

Absolutely- Top Line is where we should focus attention on.

And I will come to that, shortly.

The reason for underlining/drawing attention to industry-best efficiencies is two-fold

-

Not many adopt the PAT Dorsey 2nd doctrine seriously - Understanding Sources of Profitability/Quality of Profitability - when we take that seriously (and observe/monitor/question over 2-3 years), I have seen that I learn a great deal about inherent Mgmt focus/strength areas - that again helps in separating the wheat from the Chaff

-

If someone is beating the best-of-the-best hollow in certain parameter(s) - we better question hard again - too good to be true? how is it even possible? how can Ajanta Pharma a midcap pharma business have (almost) double the Inventory Turns of some one like Sun, Lupin, or for that matter anyone else in the industry - some industry analysts might tell you, NOT POSSIBLE!

I have seen I understand more every year about a business like Ajanta - by asking more…thinking more …connecting the dots, more ![]() . Anyone who has followed Ajanta over last few years might confess - it’s not easy to understand the Sources of its Profitability… ha ha.

. Anyone who has followed Ajanta over last few years might confess - it’s not easy to understand the Sources of its Profitability… ha ha.

Some folks may consider above unnecessary for successful investment, but for me these are crucial to my investment style. So those interested in such Insights, might like to ponder over those questions …and try and connect.

Now, you have rightly pointed out, the first PAT Dorsey doctrine is to Understand the Sources of Growth/Quality of growth. And its not hidden, there should be genuine concern here!

But perhaps if we take this seriously enough, we would try and get under the skin of the flattish kind of growth being exhibited by Ajanta of late. Profitability levels being where they are, its unlikely - as correctly pointed out again by you - of squeezing out more. Instead one could make out a case that profitability is bound to also decline if the growth rates remain flattish.

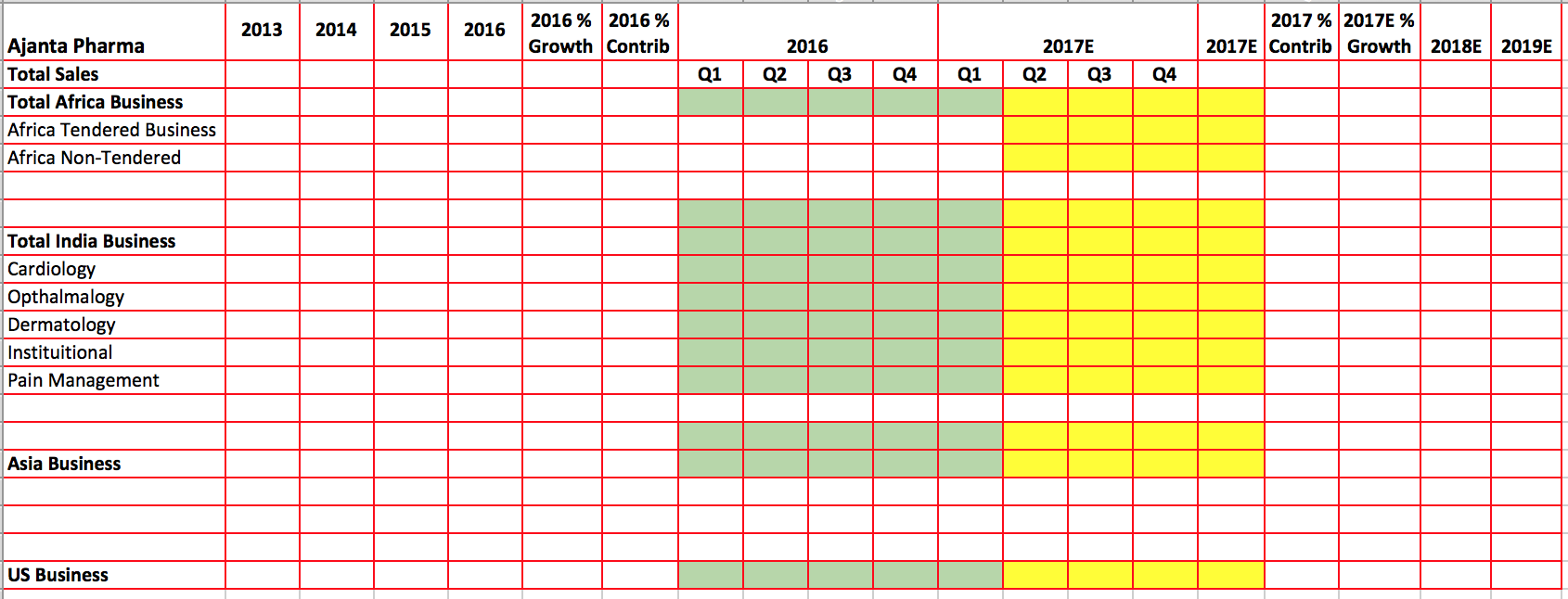

I like data points - the devil (often times) is in the details. Ajanta Investor Presentation provides segment-wise data, every quarter. Why not try and present a segment-wise break up - to SPOT where the lacunae is, ask questions IF …some of these are in their control, or probably not, and if not …how much time would these things take to revive…other things remaining equal ![]()

Please see if you want to take the trouble to fill up this simple segment-wise template.

Ajanta_Segments_Template.xlsx (61.7 KB)

Think, all the questions/(and most of the answers too) are in the data!!

2 Likes

Hi @Donald,

Incidentally, i have been diving into available data and facts to build a level deep understanding of all the moving pieces around AP. Have started towards consolidation of all in given format.

Along the way, am trying to look at all this from a ‘why’ and ‘how’ perspective. Allow me some time to come back and share the understanding.

2 Likes

Ajanta Pharma gets ANDA approval from USFDA for Lansoprazole Delayed Release Capsules for 15mg and 30 mg.

- Used to treat gastric acids produced in stomach/ peptic ulcers.

- Generic name for the brand Prevacid, marketed by Takeda.

- Total 12 approvals (Anchem, DRL, Krka, Mylan, Natco, Sandoz, Sun, Teva, Wockhardt, Zydus and Takeda).

- Per PharmaCompass, the total sales in the US is about $166m (generic) + $47m (innovator).

Source: Lansoprazole - Uses, DMF, Dossier, Manufacturer, Supplier, Licensing, Distributer, Prices, News, GMP (Global Sales Information)

6 Likes

If it can get approval for Kamagra in the UK, it would really be great. Unlike the US, UK has legislation for online consultations and ever since the patent expiry of Viagra, generics have flooded the UK market. Kamagra is still being sold by unregulated websites in the UK but is not dispensed by the NHS or by the UK regulated online doctor services because of this. Historically lot of people liked to procure this in the UK via the unregulated route (check Google search numbers) whilst the Viagra patent existed.

Very true, someone is beating the best-of-league hallow on ‘certain’ parameters. Time and again - since real long time. This has troubled me a lot for quite some time. Therefore, as a first step, have tried to understand the ‘HOW’.

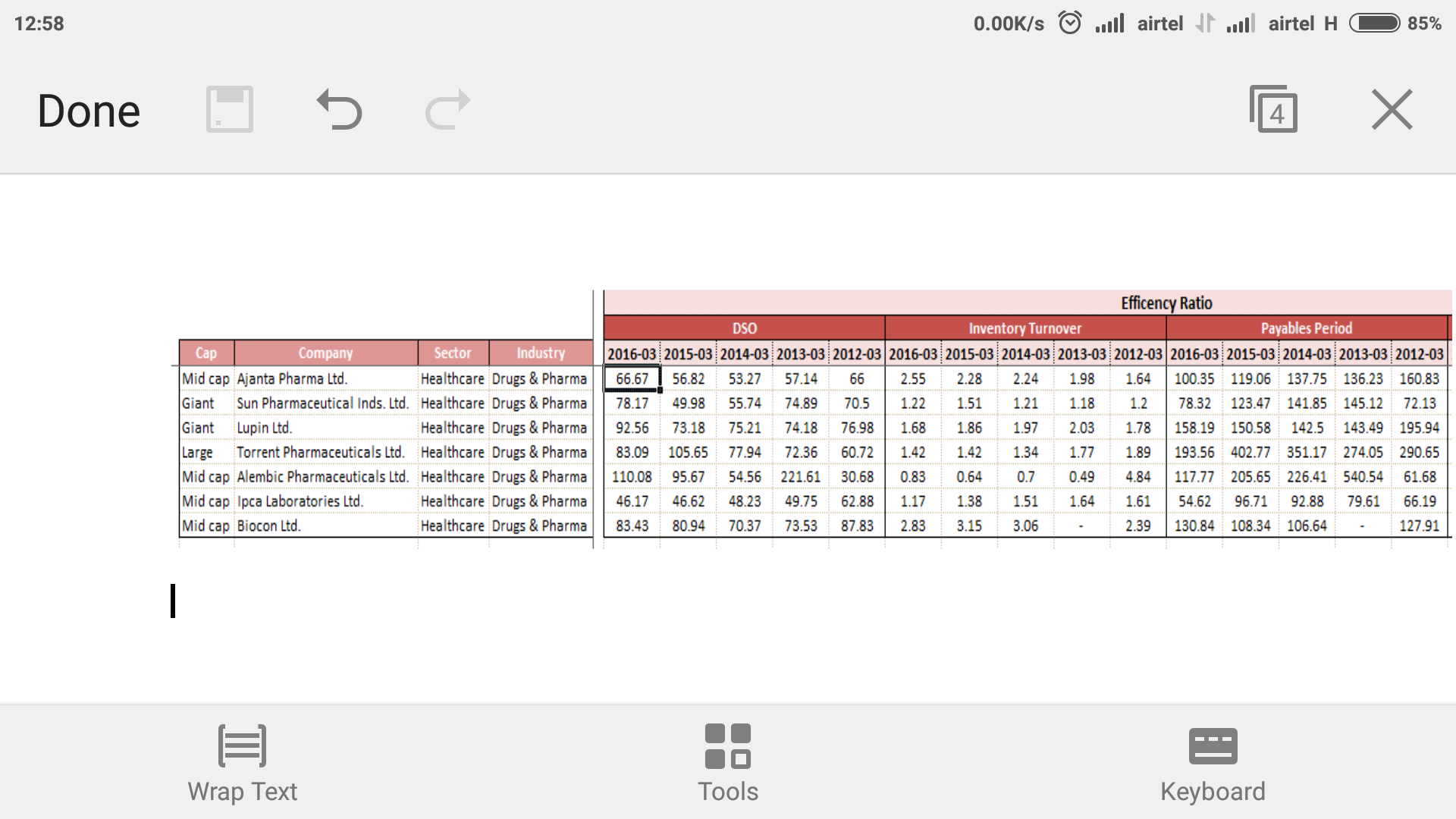

To begin with, let’s paint a mental picture of how much AP is different from peers and on which all parameters. Hope this attached spreadsheet will help create an industry level vivid view.

MS Consolidation Sheet_Pharma(2).xlsx (36.2 KB)

With this comparative view, I tend to think Ajanta performance is in top of league in some of the metrics but not really astronomically high/low. What really stands out is the ability to tick most of the boxes of efficiency.

Now the mental questions:

- How come someone can have such best-in-class assets/fixed assets turn over?

- How come someone can have such decent inventory turnover?

- Exemplary below EE cost% and raw material % etc?

Initially zoomed-in greatly from a process door (geographical spread, segments, fist to file contribution, block busters like Melacare, Kamagra etc.), only to end up getting even more perplexed. Later on, tried to zoom-out entirely and just think bit arithmetically.

At the cost of sounding overly simplified approach, lets do a simple mathematical/financial calc.

Cost of manufactured good is Rs 40.

Company C: Sell the same for Rs.100 (mark-up/gross profit is 60 Rs.)

Company B: Sell the same for Rs.120 (mark-up/gross profit is 80 Rs.)

Company A: Sell the same for Rs.140 (mark-up/gross profit is 100 Rs.)

Now, try calculating the key metrics for these three companies.

- Rest all things being same; which company looks good for any ‘higher-the-better-metric’ where total sales goes as numerator? ((i.e inventory turnover, assets turnover etc.)

- Rest all things being same, which company looks good for ‘lower- the- better metric’etc. where total sales goes as denominator? (% of EE cost, % of row material cost, other cost %)

Do I hear company A?

So, what I tend to think is that this company A is reflecting superior efficiency metric by virtue of significant marked-up sales.

No No, it cant be this simple.

Fine, I apply some counter thinking. This company A should look comparatively inferior for a ‘lower- the- better-metric’ where total sales goes on numerator. Check the DSO on the above attached sheet for Ajanta. For sure, nowhere close to the best.

Hummn…fine that’s partial explanation, AP is great in so many other aspects as well.

Ok, lets look at the SG&A expenses (delta between Gross to operating margin%), on the attached spreadsheet, 13 out of 22 other companies has narrow delta (representing more efficient SG&A expenditure) than what AP has.

Talk about tax efficiency, (delta between operating to net margin %), 17 out of 22 other companies has narrow delta (representing better tax efficiency than what AP has).

Connecting the dots, what I see here is the evidence of handsomely marked-up gross sales playing a key role in making some of the ratios look envious. For validation, look at the gross margin % column (col W of attached sheet). Gross margins only behind Sun and way above rest all -year after year after year.

Well, this revelation is nothing new. We always ‘knew’ that AP got a high margin play. What is significant is that at least I have started recognizing how fat profit margins can make you look great at so many other places.

9 Likes

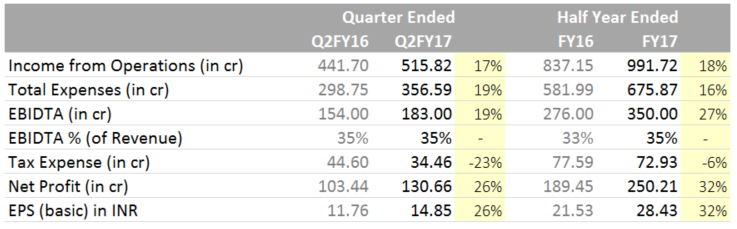

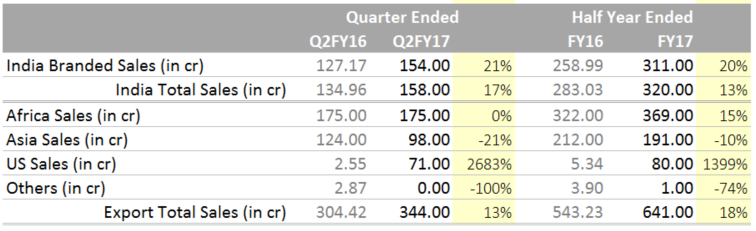

Ajanta Q2 FY17… PAT up 26%, Income from Operations up 17%…

Q2 FY17 growth driven by US & India. Africa and Asia reported flat/de-growth numbers.

4 Likes

Thank You Sandeep for results Update.

To add that, APL announced Payment of interim dividend of Rs. 6/- (300%) per equity share on the face-value of Rs. 2/- per share for the Financial Year 2016-17.

Investor Presentation

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/E51CFE56_A74A_49B2_B4BA_95BD8B08D646_151801.pdf