Airo Lam Ltd

Airolam is ranked #7 among the leading brands of the Indian laminate industry

Follows rigid international quality standards like NEMA (USA) and BS1406 (UK). For its superior design, quality, systems & environmental commitment, Airolam has been awarded ISO 9001, ISO 14001, Green Label, Green Guard & FSC certifications

Keep developing new laminates, which excel in quality & affordability

Focus on technological advancements to facilitate better production

13+ years Experience In Laminate Industry

10+ Brands

8+ Branches

Presence in 16+ Locations

69+ Distributors

170+ Employees

Rational steps by management after listing,

- High cost debt converted into low cost

- Mr Mahindrabhai Patel who had criminal/fraud cases is no longer a director

- Management remuneration is rationalised

- Many pending tax related issues seen in RHP(2017) are not seen in FY20 Annual report

- Number of permanent employees reduced even though sales has increased

Investment Rationale : -

Company don’t seem to have any competitive advantage, but industry has good tailwinds for next few years,

The industry is seeing a shift in market share from the unorganised to the organised sector,

In last 2 years many unorganised small players must have gone out of business, so we can see rapid increase in market share shift.

the changes being made in the goods and service tax in the country has resulted in lowering the price difference of plywood and laminates sector between organized and unorganized sector

Increasing urban population, rising per capita income are other key factors driving the growth of laminates industry in India

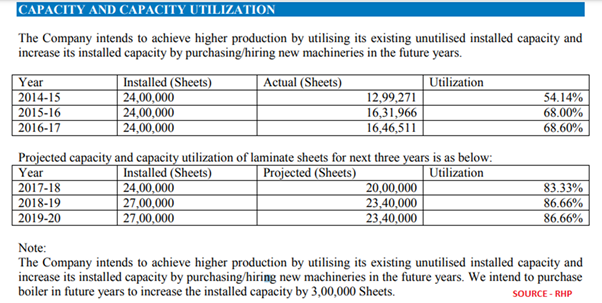

ALL is setting up a manufacturing plant of plywood and veneers adjacent to its existing location with envisaged total cost of Rs.6.30 crore and installed capacity of 67.20 lakh square feet per annum. – May be completed

ALL has expanded its installed capacity to 48 lakh sheets per annum during FY20 at its existing location considering increase in scale of operations and growing demand from the user industries. –

Seems completed (evident from March21 results - 80cr+ top line.)

It’s a big capacity expansion and from 105cr in FY20 now it can produce 350 to 400cr top line and 15 to 20 cr bottom line(5cr in FY20) , at 80cr market cap it’s no brainier opportunity.

They are sitting on expanded capacity at the right environment, may be luck.

Operating leverage can kick in as capacity utilization increases, bargaining power with suppliers may increase going forward.

Lot of scope to increase dealer/distributor network and penetrate deeper.

Risk : -

- No competitive advantage is business

- 90L bad debt written off in FY20

- Trade receivables for more than six months are consistently very high over the years

- They have to push sales through high credit period to its customers

- Many micro, small, Medium size competitors exist

- Limited to no bargaining power over suppliers from whom company imports raw material

- Cyclical Industry

Discl.:- Invested and may be biased

Not an investment advice, data sharing just for study/discussion purpose.

Data source :- RHP, Annual reports, Credit ratings etc