Intresting. 80% of liquor sold in Plastic bottles. Alcohol being corrosive, inert material is essential for high alcohol content liquids.

If small percentage of it converted to glass packaging (article mentions > 800 Rs/bottle) in multiple states, it shall consume significant capacity of glass industry.

2 Likes

Any update or views on the same as stock appears to be fairly valued at this price available at P/E of 14.5

1 Like

My views are the same. The valuations were neither cheap earlier nor are they now. The biggest question mark as stated earlier imho still remains revenue visibility in the next 1-2 years.

First quarter results were great. Second was flat. I would take even a 6% growth for this financial year in its revenues. 6% growth for a 8 times EVEBITDA looks like a stretch but it’s comfortable to me.

Overall, my views remain unchanged. Valuations are not cheap, there’s no doubt about it. Fair price, probably, but definitely not cheap.

There is Debottlenecking happening in the company. The management expects H2FY26 to be much much better. I expect FY27 to be robust for this company.

1 Like

Anyone following it ?

Slow but steady fall in share price in last 30 days bringing it to below 600 Rs range !

Results were decent. Anyone on reason for fall ?

QIP price management?

Worth buying at this price ! No big issue in the stock shall grow post Q4 fy26

But fall continues ….slow but steady fall, day-by-day everyday. This is very surprising given the very attractive valuation at CMP.

PGP Glass (erstwhile Piramal Glass, now owned by Blackstone) is planning IPO at 37000 Crore Valuations ($4 Billion) . This is apparently around 25X EV/EBITA Valuations. These are almost 4X of AGI ! They have similar 1720 TPD capacity like AGI but with slightly better margins as their 70% capacity is into Specialty glass. With these dirt cheap valuations, hopefully there nothing negative which we don’t know which others know and hence this perpetual fall. Blackstone Considers $500 Million Mumbai IPO for Glass Packaging Maker PGP Glass

I have been tracking and wondering on fall in AGI.

Is it due to cost of gas and energy going to rocket due to Iran Issue or something deeper we cant see. Because at this price, its eye-watering cheap

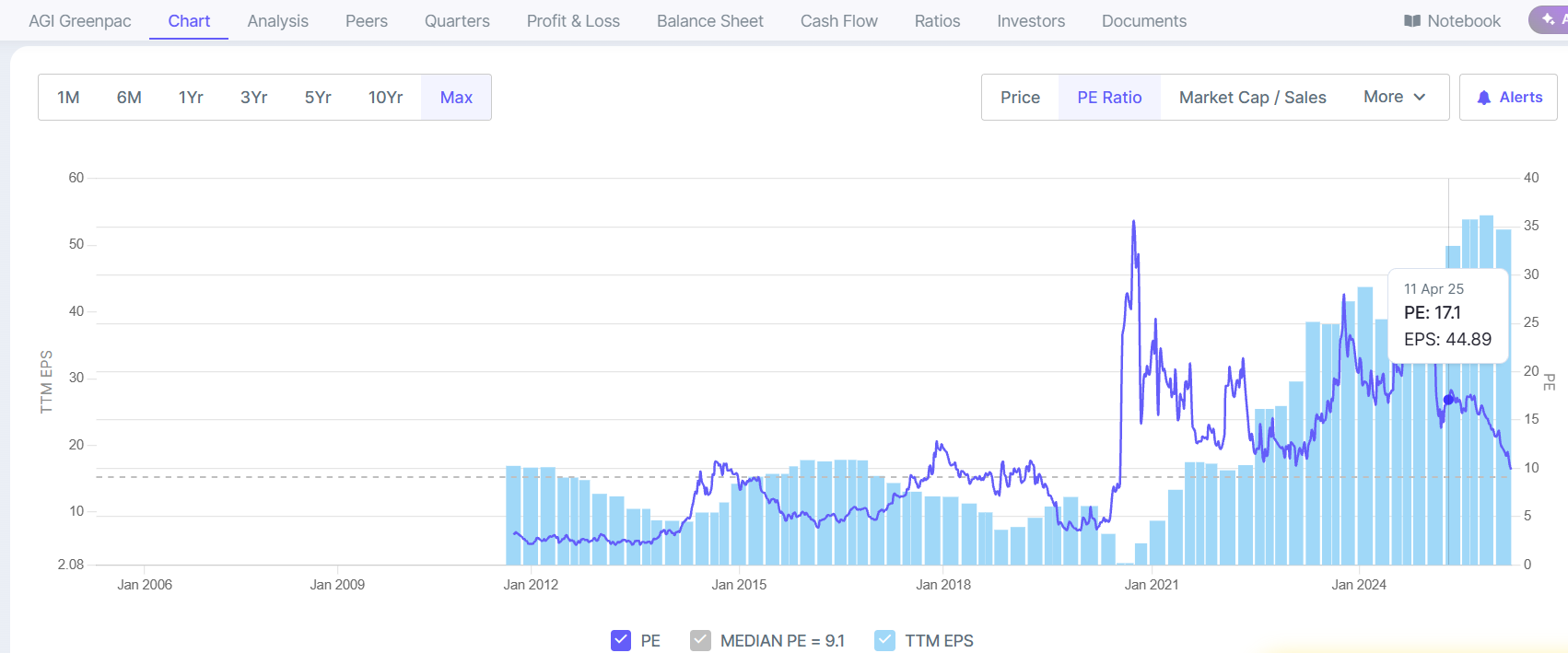

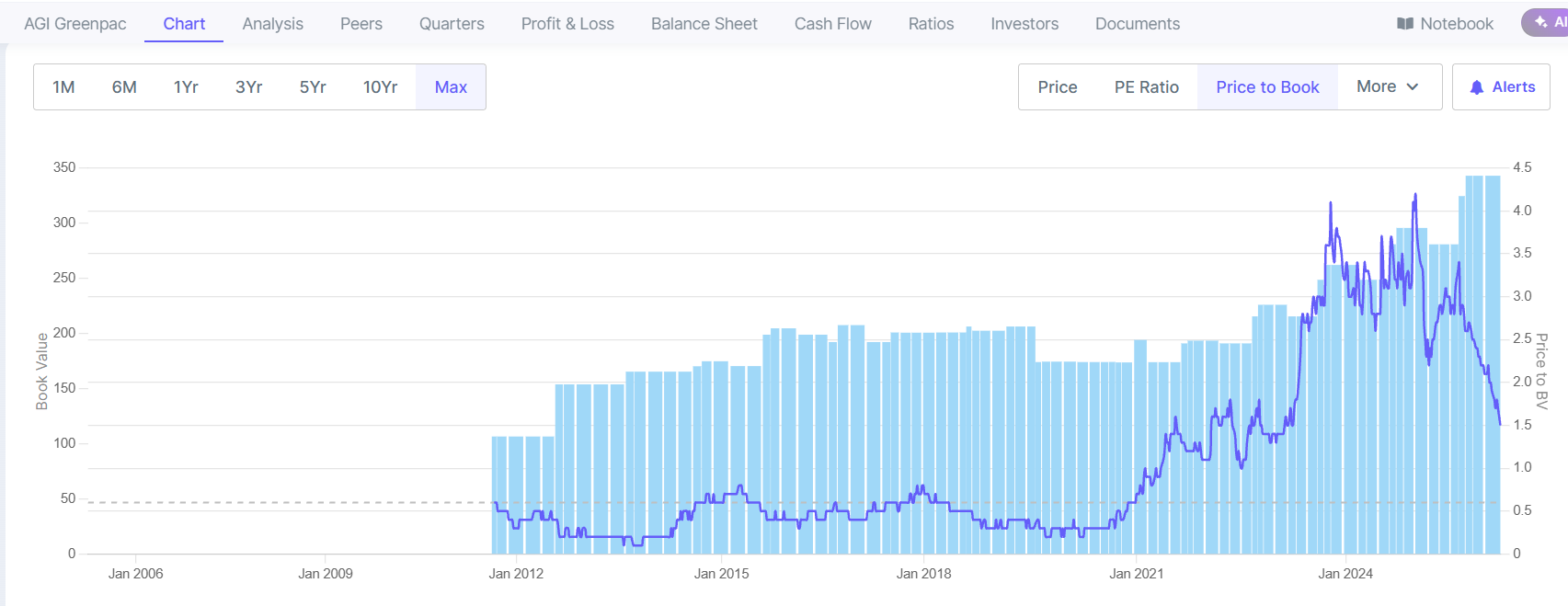

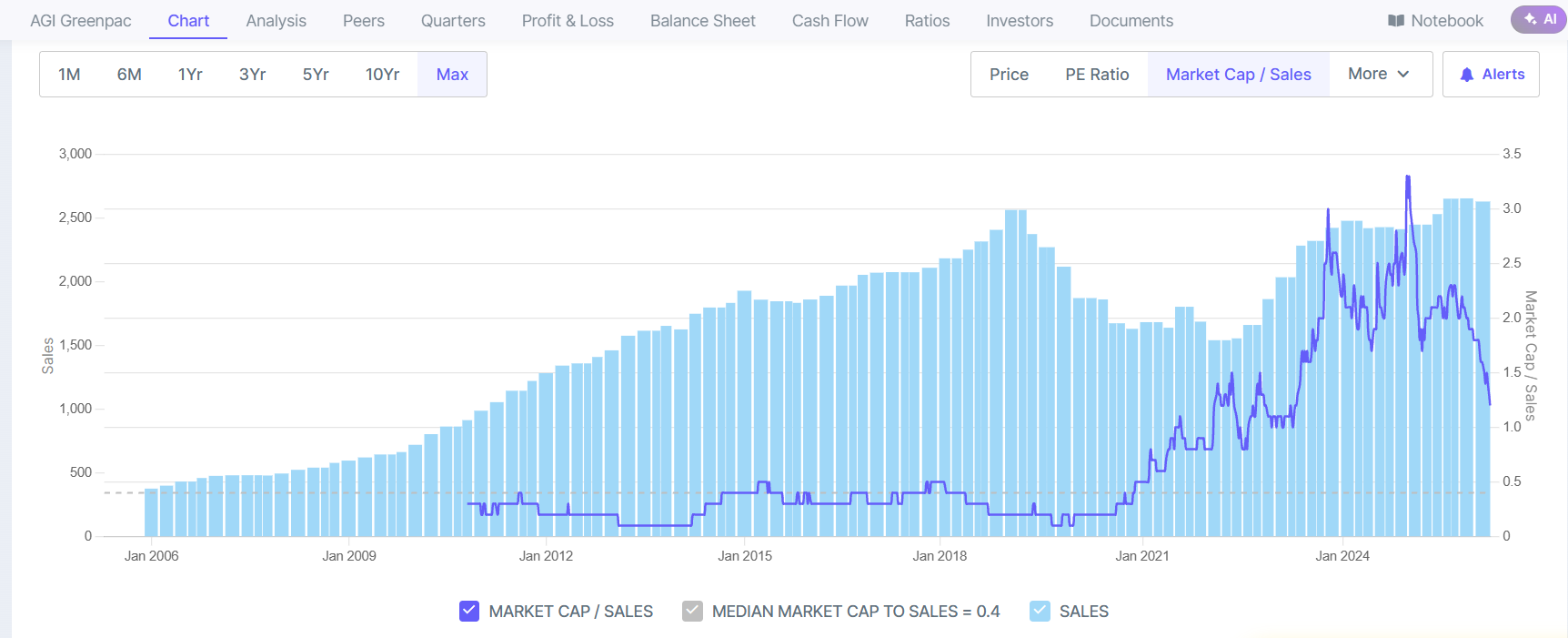

Looking at the long-term valuations, it is still above median valuations on the PE, PB, and P/S basis

PE basis

P/B basis

PS Basis

To me, it looks market is anticipating drop in margin once HNG capacities are live.

Looking at “Max” charts will be incorrect as the company , “AGI greenpac” came into existence post demerger from HSIL in 2019 Only. Even after 2019 till 2022 it was carrying a vary heavy “load” of being TOLL/contract manufacturer of HSIL bath ware/kitchenware etc with ultra low margin. The REAL demerger happened only in 2022 when these heavy assets were transferred back to Hindware home innovation limited post Covid. So, look from 2022. The current fall may be triggered by its deletion from MSCI Global Smallcap index which meant passive ETF outflows. It may also get deleted from NIFTY smallcap index. It is one of the most efficient Glass manufacturer globally. The Multifuel furnaces allows it run on multiple kind of fuels and unlike HNG - Which may face shutdown/slowdown due to Gas shortages post Iran war, it shall continue with electricity and/or Biofuels.

3 Likes

I am aware that it might be “incorrect”. But I have also seen the long-term valuations tool/Charts more often than not, correctly show the trend. It might be what you say is correct. Or it might be that investors are wedded to a higher price in their minds due to price anchoring and recency bias. Anyways, it’s worth watching how it unravels.

“AGI Greenpac’s operating margins have expanded from 11-12% in FY18-19 to 23-24% in FY24-25. ROCE went from 3% to 20% over the same period. The balance sheet has been cleaned up materially, with debt halved from Rs 1,230 crore to Rs 553 crore. On the surface, this is a business that has undergone a structural transformation. The single most important variable behind that margin expansion was the prolonged insolvency of the largest player along with a couple of more factors.”

1 Like

I have been studying this for some time now and have been puzzled by its cheap valuations in the recent times.

These may be the reasons for current valuations:

- Aggressive capex may lead to 1000-1200 Cr in debt/ equity dilution as indicated by management in concall.

- Diversification into lower margin Aluminum Cans business (15-17%) compared to glass business (20-22%). No matter how much business and profits that will come from this diversification, market always punishes when your margins will come down due to product mix change. (Speciality glass (above 25% margins) can increase the margins but it is still a small contributor to revenues)

- The first phase of new capex will come online at the ems of FY 27 and futher additional expansion by FY 28. Capacity utilization is already at peak and debottlenecking at current plants will have low impact on sales.

Until the above overhangs remain, stock price movement will be range bound.

Please feel free to correct me if I am wrong.

Disc. : studying for investment.

1 Like

I have few observations to the contrary.

This is a blue chip available at dirt cheap rate. Strange are the ways of the market. You will find scores of dubious companies quoting at premium level compared to this one. Yes, equity dilution overhang is there. But for how long? In fact the stock has been in down trend for more than a year. I also disagree with the rationale that margin dilution will not allow higher price. Why? And what is higher price? PE of 10 or 30? Why I value is cheap ; competent management, near monopoly market, no competition at least in near term, PE of less than 10, expansion into can business, expansion.

These are my views. But I may be wrong. I am invested in the stock and so my views may be biased.

HNG is bigger than AGI Green, AGI could capture more market as HNG was in bankruptcy, once HNG start functioning after takeover completion current margins will drop to 17-18%. This is reason i feel markets is not valuing it higher. This was a 5X for me, entered around 170-180 levels and exited fully above 1000. Did not lookup after medhani group was declared as winner for HNG.

202604140428_AGI_Greenpac_Limited.pdf (203.3 KB)

Latest credit rating rational

See, the problem is equity is not that much of a drag compared to Debt and raising debt is still a possibility.

True that a lot of dubious companies trade at premium and a lot of good companies trade at discount but that’s how market is. We have to understand it and take benefit from it.

Companies will flat growth, debt overhang and margin mix reduction can trade below 10 PE as well. I have seen quite a few examples.

If management can find a way to keep debt minimum and increase capacity utilization of the upcoming plant rapidly and increase speciality glass mix, then who knows, it can still be a multibagger from here.

All in all a good risk to reward ratio but I am happy to wait on the sidelines to see how things pan out in the next 2-3 quarters.

Is company operations affected due to Iran-USA was led fuel or material shortages? any news around it?