The resolution for splitting the shares at AGM didn’t pass as promoters themselves voted against it. (Why did promoters first brought the resolution, and then voted against it?)

It’s good, in my opinion, as having a smaller value share-price leads to unnecessary volatility.

Regarding low earning multiples, following are some of the potential reasons.

-

The corporate governance appears below average.

(Reason 1: All independent directors resigned in August 2023 on the same day. The curious thing is all sighted the same reason and all resignation letters have same format and fonts. Also none of the independent directors took any sitting fees, which is highly unusual. All these resonably indicates that independent directors are not independent.)

(Reason 2: The promoters itself voted against the resolution for splitting the shares, indicating an immaturity.)

(Reason 3: BOD seems nothing but the family get-togather.)

(Reason 4: The promoters have a history of issuing shares or warrants to itself briefly before a big positive for the company in terms of profits.) -

The fate of the company is dependent on one commodity as well as completely on imports. Any change in the stance of the Govt regarding import of Bitumen can completely destroy the company.

-

Some subsidiaries have been incorporated in Cayman. Why? Nobody know. Nothing of that sort has been discussed in any AGM or ConCall.

-

Low float.

-

Value addition is very low in the product. The company is engaged mostly in logistics and selling the Bitumen.

Now, above points are not sufficient to not own the company. So, I am highlighting some positive points.

- Good cashflow.

- Some degree of competitive advantage.

- Beneficial subsidiary structure to completely avoid income tax on a good portion of profits. (Why? How? Figure out on your own.)

- No planned capacity addition of Bitumen by domestic manufacturers. So, import has to happen.

- The company has imported high quantity of Bitumen between April-August, 2024 v/s the same period for last year. (This is a reason to own for short term, if you like to do it)

- Rain is heavy this season across the India. Good demand is anticipated for repairs. However, new road construction is expected to remain subdued. (Again a short term reason.)

Q2 FY25:

• Volume Growth: In Q2 FY25, the company sold 65,338.77 MTS of Bitumen and allied products, a notable 47.27% increase from 44,364.27 MTS in the same quarter last year.

• Strategic Initiatives: In a strategic move to strengthen its infrastructure role. AICL has acquired a Portland at new Mangalore port trust to develop a 40,000 mt storage terminal for bitumen and other liquid products. The project has already commenced with a capital investment of amount Rs. 40 crore and will significantly enhance AICL’s supply chain capabilities across south India.

The new terminal will join AICL’s existing network of fully owned storage locations in Dighi, Vadodara and Mumbai, formatting a vital part of its distribution backbone. This investment will not only expand AICL’s storage and distribution capabilities but also positively impact the company’s bottom line as it addresses growing demand within India’s infrastructure sector.

• Outlook for Fiscal Year 2024-25

o • Revenue Guidance: The company aims to grow over 20% at Revenue and Volume level Y-O-Y.

o • Earnings Guidance: A targeted CAGR of 20% for EPS aligns with the company’s historical growth trajectory.

o • ROCE and ROI Guidance: The company intends to maintain a healthy ROCE and ROI of around 20%, consistent with previous years

CONCALL NOTES

• Planning a million tonnes of volume by FY27 (Double of FY24) (Possible with current asset base with only a few more storage terminals required)

• 20% of revenues comes from all 3 OMC PSU’s

• Currently not paying any taxes in UAE. May change going ahead with new taxation policy (Maximum 9% rate could come)

THINGS TO TRACK

• VOLUME GROWTH

• ASSET ADDITION

• EBITDA PER TON

AGARIND_13022025190118_IntegratedFinancialsQ3.pdf (6.9 MB)

Waiting for management outlook on the business

Although consolidated revenue from operations increased 11%, PAT is flat.

The main reasons are Increase in depreciation and other expenses.

Could the reason for such increase in expenses be not using the 100% capacity of newly added vessels?

Understand some simple maths of the business

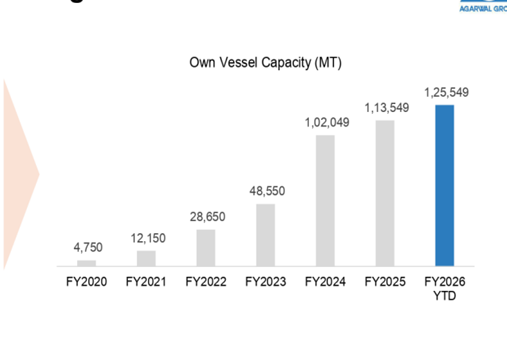

A) General rotation of vessel in the year = from 4x to 5x

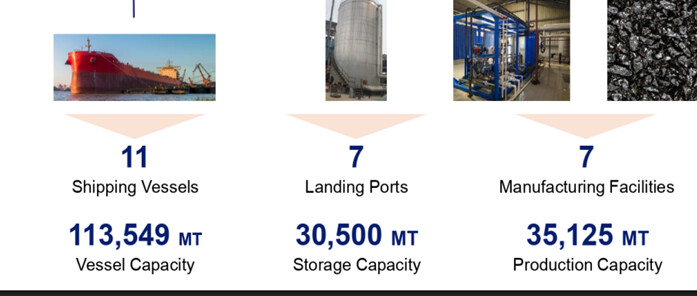

B) After adding 11th Vessel, own capacity ~ 113,549 MT

C) Considering lower side of rotation = 113,549 X 4 = 454,196 MT

D) Bitumen carrying from outside vessels = ~ 200,000 MT

E) EBITDA impact due to outside vessels = 25% or say additional cost

F) Realisation = 40000 Basic + GST and goes up to 47000 Basic + GST

Now comes to the calculation part

Assume, Carrying load 600000 MT and Avg Realisation @ 45000

Expected Revenue 2700 Cr

Expected NP 5.0%

Expected NP 135 Cr

Outstanding no of shares 1.495Cr

Expected EPS = Rs 90/-

General P/E range 11-13

ROCE = Reported 20%

Note: Calculation to be revisit and change accordingly

Hi guys, I am a new investor in the markets and have been tracking this company. The company looks interesting, but I had question on the roads in India. If concrete roads are considered to be better why would bitumen demand still exist few years down the line.

Is India not going to change to making concrete roads given that they are more durable, hold up better under the. weight and pressure of trucks won’t we move to concrete roads. I think I might be missing something here.

Any help or guidance would be great.

(Disc: Not invested)

It seems from your post that concrete roads could be taking majority incremental share, which, then, is a big risk to AICL.

Since Agarwal Industrial Corporation operates in the bitumen trading and processing business, and given that bitumen is a by-product of crude oil refining, could the long-term shift towards EVs — and the resulting decline in crude oil refining — lead to supply constraints for bitumen?

1.EV and ICE are contributing at least 10 years.

2. Bitumen is more related to construction of roads.

Agarwal Industrial Corporation

Results not Satisfactory.

-

On Annual basis EBITDA grew by 16.82% whereas Core EBIT ( Without Other Income Effect ) reduced to mere 7.96% growth.

-

On annual basis EBT reduced to 1.77%, due to increase in Interest & Depreciation by 44.16% & 58.9%.

-

Borrowings increased by 20.54%, whereas Net Block increased by 17.22%.

-

On Q on Q basis, sales grew by 6.05%, whereas Operating Profit reduced by 11.02%, due to increase in Operating Expenses by 7.49%.

-

Q on Q, core Net Profit ( Without Other Income effect ) reduced by 26.97%.

Waiting for management commentary.

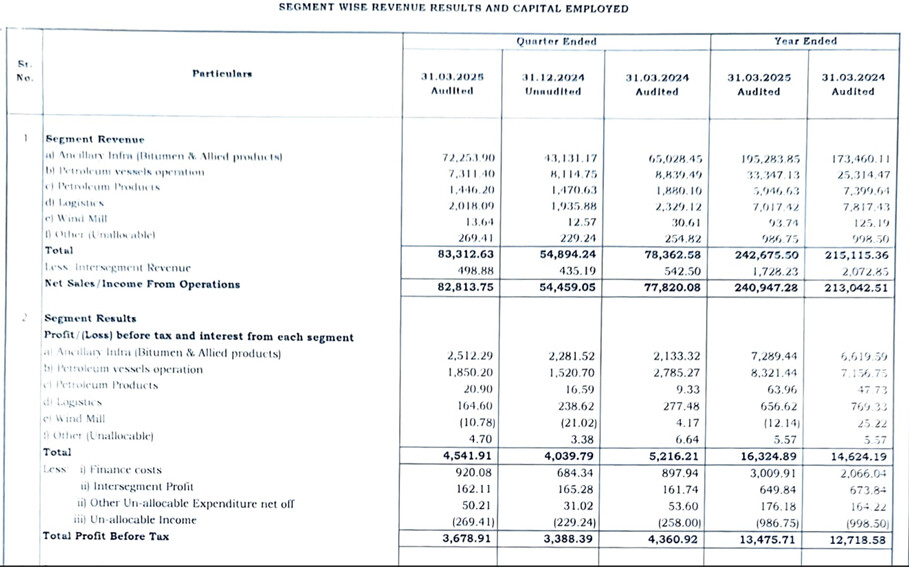

Q4FY25:

•

• During the Financial Year ended on 31" March 2025, the Company under its Ancillary Infra – Bitumen and allied products segment, sold 5,35,938.62 MTS of Bitumen and allied products as compared to 4,90,813.49 MTS sold during the corresponding previous financial year ended on 31* March 2024, thus registering a growth of 9.19 %\

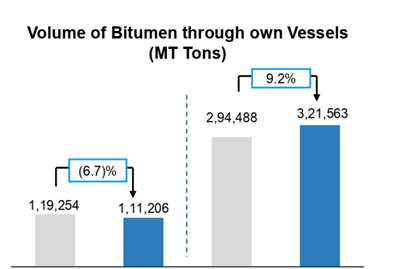

AICL’s own shipping vessels delivered 321,563 MT of this total volume, representing 60% of bitumen imports.

•

(7 manufacturing facilities for Paving Grade, Industrial Grade, Crumb Rubber Modified Bitumen and other allied products)

• Largest private-sector bitumen trading and product manufacturing company in India, with integrated shipping vessels and fleet logistics.

Vessel and fleet ownership enables logistical advantages in bulk bitumen sourcing and ensures delivery reliability.

Vessels, storage and logistics scale plus integration allows competitive bidding, high customer service and reduced throughput rates

Integrated infra-ancillary platform creates barriers to entry and allows AICL to capitalize on India’s infrastructure spending in the future

• Imported 486,546 MT of bitumen from Middle Eastern refineries and intermediaries during FY2025, reflecting a 9.2% YoY increase

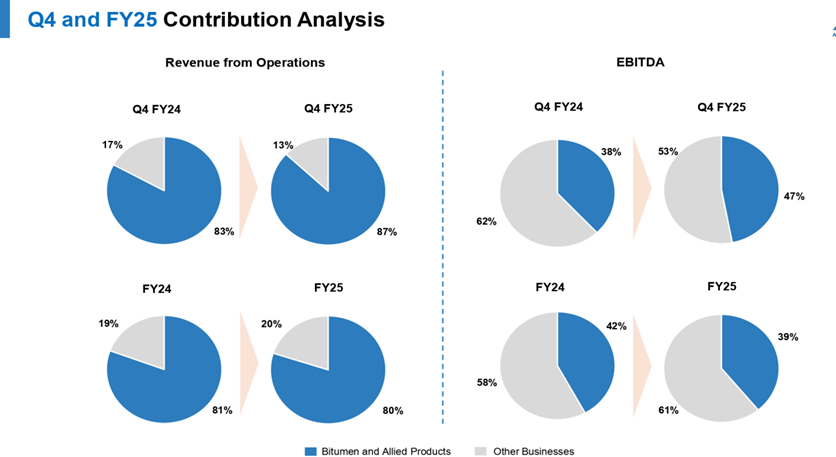

• 72% of revenue from bulk sales to road construction firms (direct and via PSUs); 28% from allied products

• PSU customers receive bulk bitumen from port storage; non-PSUs are served from both manufacturing and port locations

• AICL plans to enter the bitumen market in north India, to diversify the customer base and capture new market opportunities

• New manufacturing facility of Rs. 5 Cr in Guwahati to address eastern states road construction and other infrastructure projects. Commissioned.

• Q4 FY25 Volume: 185,344 MT (-6.7% yoy growth)

• To the extent these shipping vessels were not deployed for AICL’s bitumen imports, especially during the monsoon season, they were chartered to third parties. Revenues for the shipping business were Rs 334 Cr representing 13.7% of Total Revenues and contributing an EBIT margin of 25.0%.

• During the year, AICL signed four major contracts with its PSU customers for a total quantity of 151,000 MT and an order value of Rs. 635 Cr. These orders are a reflection of the significant underlying demand for bitumen that is primarily required in the construction of road networks all across India.

• AICL invested Rs. 40 Cr in a new 40,000 MT storage terminal at Mangalore Port, comprising 10,000 MT for Bitumen and 30,000 MT for Allied Products, to strengthen its supply chain in south India. This storage facility is expected to commence operations during Q2 FY26, taking AICL’’s total bulk bitumen storage capacity to 40,500 MT.

•

•

• A vessel was acquired in Q4 FY25 and became operational in April 2025

CONCALL NOTES:

• GUIDANCE: This year we are again targeting 20% volume growth. So around 650,000 to 700,000 tons.

EBITDA per ton should be around Rs. 4,200 to Rs. 4,500.

• REASONS FOR DROP IN MARGINS: The vessels were in dry dock and the dry dock was little bit prolonged whereby the maintenance time was increased in that dry dock. That is the reason that we have a little bit of profitability impact in the shipping segment this year. Going forward, I think we will be on track as the last few years that we have been doing.

15000 Tons vessel capacity was in dry dock.

30-40K MT sales volume impacted due to vessels in dry dock.

• REASONS FOR SALES DROP: See, we already had products lined up, and in the last week of the quarter we had significant volumes that had come in which we sold in April. That is one of the reasons that the timing of the product landed at the last few days of the financial year, otherwise we might have closed around 555K volumes. These are all logistical operations that we are taking care wherein if we miss two, three days of the working days. then the product lands on the last day of the financial year.

volumes, we have vessels in sea always which landed in the last few days of this financial year, which could not be sold in this year, and thereby some volume has gone because of the product landing in the last few days.

• I do not see any chartering rates falling in the region that we are operating in. That is, I think you are talking about the containers wherein the rates may have fallen, because I am not aware of the containers. But in the bulk segment, I do not think there is much of a fall in rates.

• CAPEX: As I have always been saying, any CAPEX we are focusing on increasing the logistical advantage that we can gather. That is one of the reasons we have set up Mangalore terminal. So, any other opportunities if we get in this segment, maybe a terminal or ships needed to be added, we will take a call. And accordingly. it is a mix of debt and equity from the company promoters, and the company.

• End market demand is doing very well. No issues on the demand front.

• New vessel cost – 13 million USD

• COMPETITIVE ADVANTAGE: See, there is no entry barriers to the sector as such. But to enter and maintain the supply chain, it’s very difficult because we are the only company having a USP in this entire Indian segment wherein we have end-to-end solutions for bitumen wherein we have our own sourcing arrangement, we have logistics in sea to bring the product, we have storage, we are manufacturing, we have land transport, we have our own customers, end users to cater to supply product. And for them one point of solution helps them to do their work better and in a convenient manner and doing it faster. So, there is no entry barrier as such, but yes, any of the companies who is entering, they may have one segment, they may not be having all the entire supply chain that we have. That is the USP that we have created in the last few years. The logistical advantage that we have in sea, at the ports, and in land, that is the focus that the company has been doing in the fast few years, which is maybe helping us do our volumes now in the last few years.

• From FY26 onwards, Own vessel contribution can be 65-70% in overall bitumen volumes imported.

• Rain may affect a few days demand in this quarter. Demand gets shifted to Q2-Q3.

• In FY26, we have about two vessels in dry dock, but those should not take more than 20 days, 22 days. So, there should not be a drop down, because we always consider vessels operating at around 340 days in a year. 15000 Tons will go into dry dock.

THINGS TO TRACK

• VOLUME GROWTH

• ASSET ADDITION

• EBITDA PER TON

Volume Growth on own vessels or third-party vessels.

He was said on concall about 20% growth on revenue and margin.

It was poor Q1 by Agarwal. Marred by external headwinds, especially the shipping segment as their vessels operate in UAE and Oman region which was near Iran and Isreal war.

Will be holding it till atleast March qtr results to see if management delivers on its word.

DISCLOSURE: HOLDING

Q1FY26;

•

• The quarter was marked by significant external developments that impacted operations. The India–Pakistan war led to disruptions in trade flows and shipping schedules, resulting in an estimated 15 days of impact. Additionally, heightened geopolitical tensions across USA, Iran, and Israel disrupted UAE and entire Middle east regional trade and caused close to one month of impact on shipping movements. Further, the early onset of the monsoon slowed construction activity, leading to softer demand for bitumen.

• Despite these headwinds, India’s road infrastructure sector continues to provide a positive demand environment. The Government has targeted project awards worth ₹7 lakh crore by FY26, scaling up to ₹10 lakh crore annually thereafter. Programmes such as Bharatmala and PM Gati Shakti are expected to drive this growth, while the target of building 100 km of roads per day reflects the scale of opportunity. These Government initiatives provide visibility of sustained demand for bitumen as a key raw material for road construction.

• Started full-fledged operations in Q2 FY26, manufacturing and storage facilities at Guwahati, Assam

CONCALL NOTES:

• GUIDANCE: 600K MT (10% Growth from FY25). [Revised down from 650-700K MT] {Subject to geopolitical risks}

EBITDA per Ton Guidance remains same. More than 4,300 for the year. (4200-4500 was guided in Q4FY25)

• There is improvement in vessel movements and utilization in this quarter.

• Guidance of doubling FY25 volumes by FY28 remains unchanged.

• Market share loss? Indian Bitumen bulk volume imports were lower by almost 8% to 10% in the 1st Quarter, While Agarwal lost volumes of 27%.

• Fixed costs in the shipping vertical: Fixed costs remain the same in any business that you do. Even in the shipping side, your fixed cost of wages, crew, the shipping operation, everything remains the same irrespective whether the vessel is moving or not. As explained due to the geopolitical situations, when the vessels were not moving, but your fixed cost remains the same and you tend to lose on the revenues because the voyages are not complete due to the factors explained. That is the reason for EBIT drop. The expenses side remains the same, whereas the revenues are on the lower side.

• MANGALORE AND KARWAR STORAGE (ACQUISITION): We are already operating at both the places, even in Karwar and Mangalore, both the places are giving almost 35% to 40% of the Company’s revenue every year, and at both the places, we are having tankages on lease. Hence, we have acquired existing Company in Karwar and building our own storage in Mangalore. That will contribute in saving of our rental expenses that we are paying towards the operations in both the two locations, thereby adding to the bottom line in terms of saving any additional rentals by increasing throughputs.

The new acquisition is having existing capacity of more than 24,000 tons and the total Capex will be more than Rs. 30 crores in this.

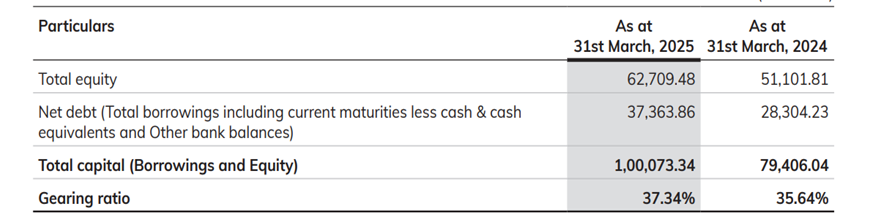

The Company has funded all the cost of these two projects through internal accruals. (Check debt position in H1 balance sheet)

• We are working only during eight months in the year, four months of the monsoons, we are not bringing any product into India or you can say lower volumes moved into India. So, hence, for India, we are only doing eight months of vessels turning around.

• Chartering margins will bounce back. As and when we start increasing the volumes and the vessels are utilized 100%. all the numbers and EBITDA that we used to see in the earlier quarters, you will be able to see in the next three quarters.

• Usually, even Quarter 2 is a slow quarter for us if you see year-on-year but Q3, Q4 should be a good quarter this year.

•NHAI TENDERS: With the opening up of NHAI tenders worth Rs. 3.4 lakh crores this year, so, do you think we could see a higher volume growth than 10% what we are guiding now or could there be a much better growth in the following year? I assume we should be able to grow better than the guidance that we are giving. As you mentioned, there are a lot of tenders being awarded which are scheduled to be executed in the next two, three quarters.

• When we get any good opportunity for acquiring any new vessels, the Company will definitely go for it, because we still require vessels as we are taking from third-parties.

• As the number of vessels increases, there will be one or two vessels which are required to do dry dock in a year. And that is part of normal business. So, it is not that. But those periods you have to count as non-operational, which affects in a particular quarter when they are in dry dock.

This year dry dock of two vessels is already being completed as on date.

THINGS TO TRACK

• VOLUME GROWTH

• ASSET ADDITION AND BALANCE SHEET POSITION

• EBITDA PER TON

MISCELLANEOUS ANNUAL REPORT FY26 NOTES:

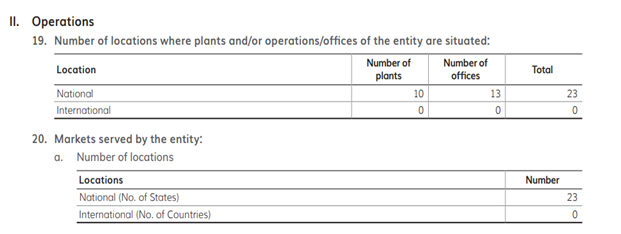

• MANUFACTURING & BULK BITUMEN STORAGE FACILITIES: The Company has its manufacturing and storage units at Taloja, Belgaum, Baroda, Hyderabad, Cochin (through its wholly owned subsidiary – Bituminex Cochin Private Limited) and at recently added unit at Pachpadra City, Dist. Barmer, (Rajasthan). Further, the Company has started full-fledged operations at its recently established manufacturing and storage facilities of Bitumen and other value-added Bituminous products at Guwahati, Assam and which would endeavor to expand and develop Bitumen trade in Eastern states as Bitumen is extensively used in infrastructure projects more specifically in road construction projects initiated by the State Government.

• An Application under the IBC Code has been made by the Company against a debtor of the Company who owed a huge outstanding amount towards the Company during the year under review and thereafter till the date of this report.

•

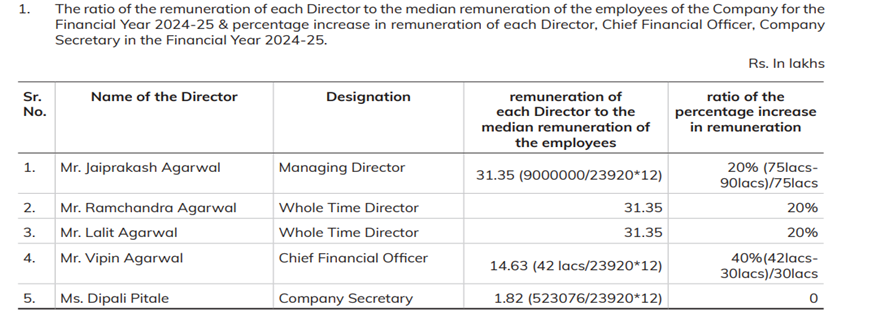

(There was no increase in managerial remuneration last year)

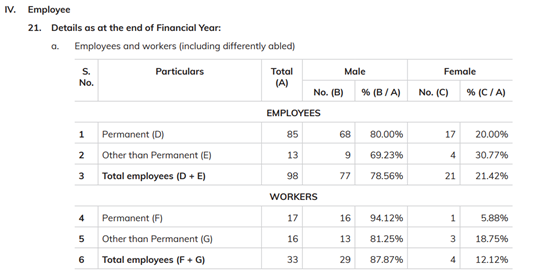

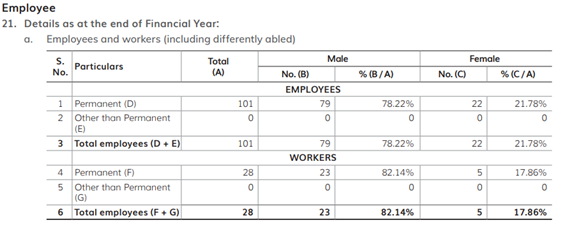

o The median remuneration of employees of the Company in the financial year 2024-25 is ₹ 2.87 lakhs. (vs 2.35 lacs in FY24)

o Number of permanent employees on the rolls of the Company as on March 31, 2025: 102 (VS 101 in FY24)

o Average increase in remuneration for Employees other than Managerial Personnel is 22.12% (3.5% in FY24)

o Average increase for Managerial Personnel Remuneration is 20% (0% in FY24)

• During the financial year under review, Independent Directors Mr. Dinesh Muddu Kotian (DIN: 01919855) resigned with effect from May 1, 2024, and Mr. Saurabh Mahesh Sarayan (DIN: 07969125) resigned with effect from July 31, 2024, citing personal reasons. There were no other material reasons for their resignations.

• MANAGEMENT DISCUSSION AND ANALYSIS

o Bitumen consumption scaled a decade high last fiscal due to a surge in road construction ahead of the general election. Sales of bitumen, used mainly for building roads, rose 10% to 8.8 million metric tonnes (MMT) in FY25, according to oil ministry data.

o More than 42% of bitumen consumed in the country is imported. India paid $1.4–1.6 billion for bitumen imports in FY25.

o Last fiscal, western India was the largest consumer of bitumen and the East the smallest.

o Development of biobased bitumen and EME (Enrobés á Module Elevé) binder is anticipated to provide lucrative opportunities for further development of the market.

o The major key players operating in the India bitumen market include Indian Oil Corporation Ltd., Hindustan Petroleum Corporation Limited, Bharat Petroleum Corporation Ltd., Oil & Natural Gas Corporation Ltd., Total India, Tiki Tar Industries India Ltd., Agarwal Industries Corporation Ltd., Juno Bitumix Pvt. Ltd., Universal Bituminous Industries Pvt. Ltd., and Swastik Tar Industries.

• Market share gain over the years, spurred by superior product quality and increased customer satisfaction though no identified identical business peer.

• OUR CHALLENGES:

• Imports – Shipments at Right time, Right Pricing, Quality Material.

• Pricing – Competition with other players in the industry.

• Continuous development of Infrastructure Sector.

• Timely payment to our clients from the related government authorities.

• Huge deficit in bitumen indigenous supply and demand leaving tremendous scope for imports.

•

(FY24)

•

(FY24)

•

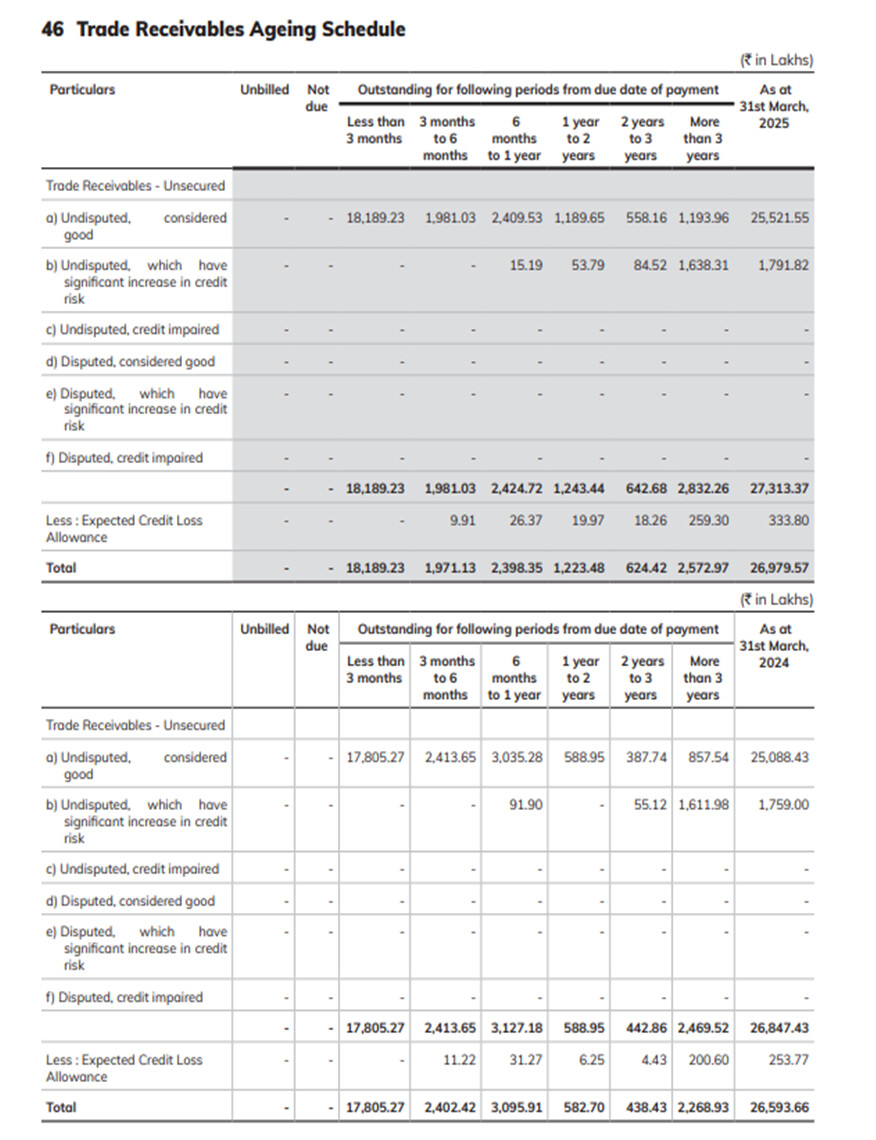

• Expected credit loss allowance – 80 lacs vs 42.5 lacs yoy

Bad debts (recovered) / written off (net) – 2.65 lacs recovered vs 4.2 lacs written off

•

•

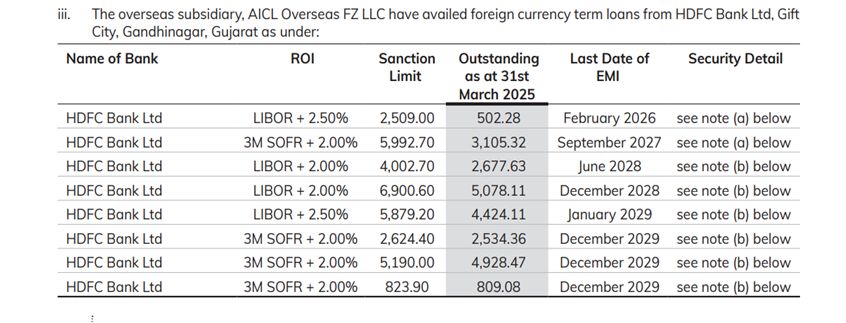

(SOFR was 4.34%)

o Working capital loans ROI is in the range of 8.2% - 10.5%

o There has been an increase in Working capital loans ROI from last year

•

•

•

•

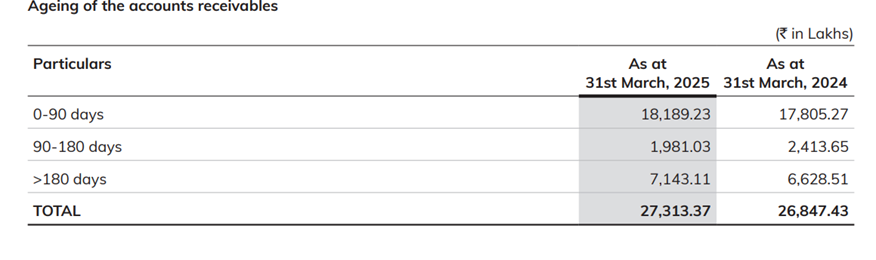

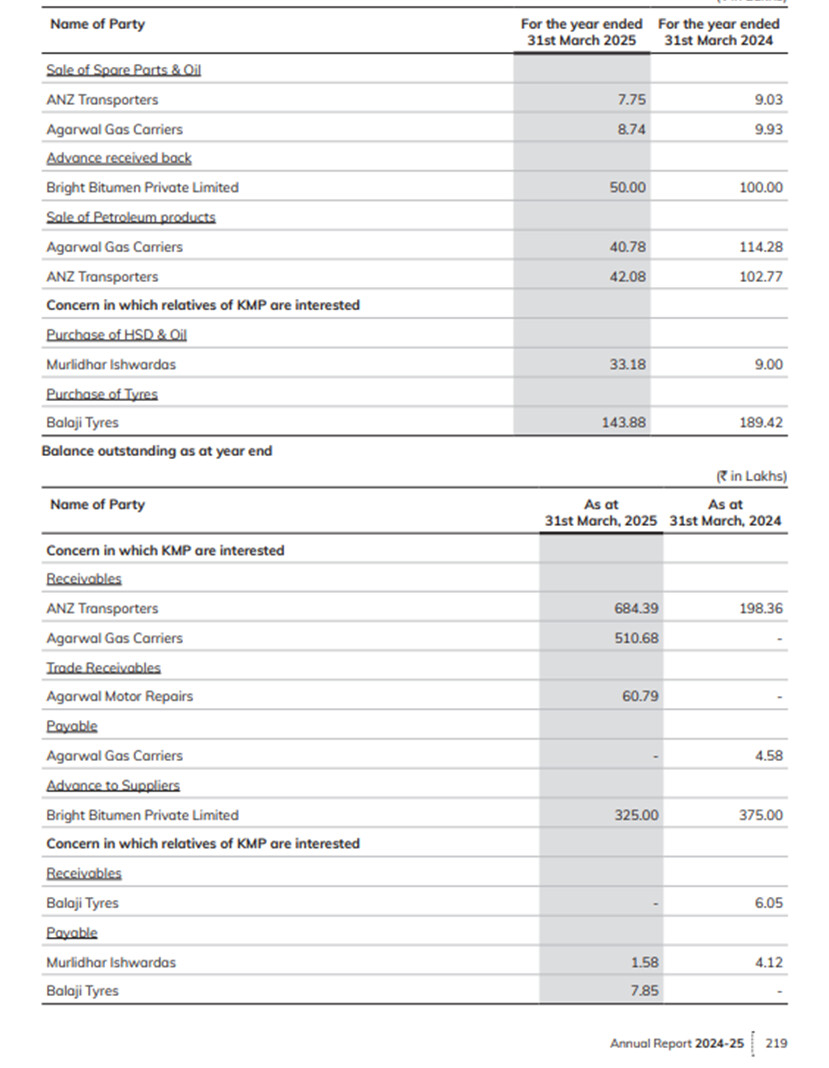

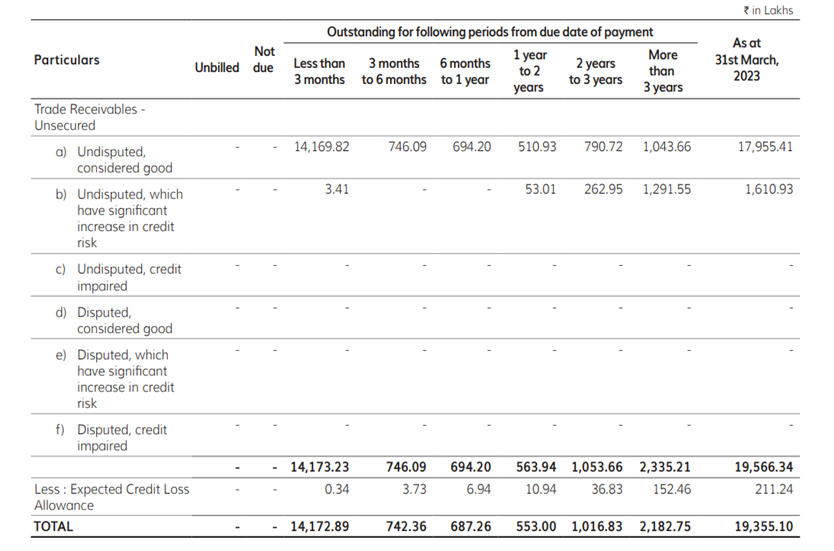

(Noticeable increase in receivables over 1 year time period)

REMARKS - The only red flag was the Recievables aging situation. There has been a noticable increase in receivables over 1 year time period.

Though in the past years as well there have been recievables in the period of over 1 year, The company filing IBC application over its debtor could mean that those receivables could be at risk of being written off.

Bad debts written off have been negligable historically. But it’s something to monitor and keep track of going ahead.

Hi @pranavpallod12 any view on management not doing a concall after the Q2 results?

The company was already facing supply issues before the Iran war as updated in Q3 results presentation. Now, with Hormuz closed, the supply of bitumen is fully cut, which has lead to sharp drop in share price.

But I was wondering if their ships are unable to get Bitumen and lying idle, would the company not be chartering them on other routes since the prices of shipping are going through the roof at the moment.

If that is case, the company might earn a great deal in Q4 even if they are unable to do their core buisness.

Mangalore storage build-up is done as per latest announcement by the company. Also, co owns ships in current environment where ships are scarce to get, freight rates are very high and volatile. Bitumen demand after the crisis will increase due to the current supply shock, pent up demand will come up. Current price bakes in perhaps the max pessimism.