Strong management commentary, giving volume guidance for 5MT which would be 18% yoy growth over 4.2 MT of last FY.

As H1 volume was around 1.8 MT, H2 volumes would be around 3.2 MT

PAT margin improvement seen over last year in the results.

Strong management commentary, giving volume guidance for 5MT which would be 18% yoy growth over 4.2 MT of last FY.

As H1 volume was around 1.8 MT, H2 volumes would be around 3.2 MT

PAT margin improvement seen over last year in the results.

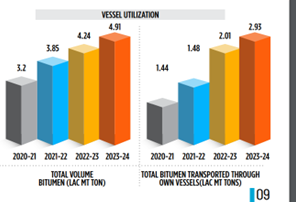

New vessel acquired. 10 total vessels now with a carrying capacity of over 1L MT.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/b95d9b47-fa63-4a5a-bbb5-f2458fc700c8.pdf

Q3FY24:

• The volume growth of the consolidated business (in terms of metric tons) stood at 2,92,057.31 Mt. tons in 9M FY24 compared to 2,72,088.50 Mt. tons in 9M FY23. (Growth of 11.3%)

• THE COMPANY IS GUIDING TO ACHIEVE A VOLUME OF 5 LACS MT IN FY24, COMPARED TO 4.24 LACS MT IN THE PREVIOUS YEAR WHICH IS AT A TARGETED GROWTH OF ~18%

Confident of achieving volume guidance. (5-10k here and there)

Targeting volumes of 7lac,8lac or even million MT in the coming year.

• Price dropped for bitumen in 9mFY23 – Prices have stabilized now and have started to improve – expecting both price and volume growth now.

• Have started executing BPCL and HPCL orders.

• Not looking to set up the company as a shipping business – Shipping business is to support bitumen business in India, so that dependency on 3rd party is eradicated and also to save costs (40 to 50cr cost savings)

• Can now support 5lac volume through own vessels

• Key challenge is procuring the product and making it available always – Demand is not a problem, can do 1.5x of what we are currently doing even today, getting the material is the real challenge – Delays in loading happen, many times we’re dry in our port storage facilities because we’ve run out of product and ship is yet to arrive – So strengthening our fleet to improve on these factors.

Delays in loading happen because there are many traders who want to trade, so it takes 7 to 10 days sometimes to put my vessel. So, it’s a port challenge, not a sales challenge.

So, having more vessels can help in alleviating this challenge. Our goal is to have 1lac MT of product per month in India

• PSU production capacity for bitumen is 5-5.5 million tons – Existing demand is 9-10 million tons – projected to grow to 12-14 million tons in the next 3-4 years – There is no additional capacity planned as such, demand has to be met through imports.

• 30-40% manufactured product, rest trading

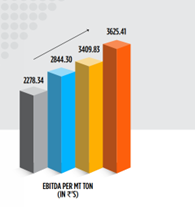

• With the addition of new vessels, EBITDA per MT should go to 3600-3700 from 3400 currently (which was 2200 five years ago)

• Value added in manufactured products – 5 to 6%

• Bitumen realization was 47000 last year, 40000 currently. Prices have already started to move up.

• During Monsoons we give our vessels to different areas for 3rd party – rest of the quarters we use for our own requirements – 90 to 95% sales is for internal requirements.

• Plans to expand geographically into new countries: We are not able to fulfill our own demand in India, so focusing only on India currently. Once Indian market is saturated, then we can look to expand geographically.

•

Volumes are increasing and projected to increase

Ebitda margin is going to increase

Demand is superstrong

All in all, very good going. This has the potential to be a consistent compounder.

One of the answer was agreed by Vipin Agarwal , CFO: So, whatever is your capacity, let’s say, if it’s 1 Lakh, can we take a 5x or 4x rotation on that number of the capacity?

Answer: Easily

So on that basis in FY 25 and FY26: They will easily handle 5 Lakhs Tonne own and 2 Lakhs Tonne third party, so net net 6 Lakhs - 7 Lakhs possible.

and Margin as per his statement ~ 3600 / 3700 per MT, then easily reach to EBITDA 220 Cr!!!

Negatives - Bitumen is not a clean business. Bitumen is imported via a lot of illicit routes. The above is general comment on bitumen import and not necessarily Agarwal Industrial. I have no way to check this out for the company.

Plus promoter issuing regular equity to itself, transfer pricing issues further adds to complication.

Although we may have gotten the No. of days per voyage calculation wrong, as travel to eastern part of country will take much longer, plus one needs to take into account the days spent for loading and unloading as well so the number would be much higher. But yes point taken that they do utilize idle capacity for 3rd party chartering etc, especially on way to pick up Bitumen.

Company Analysis & Thesis:

Management Guidance and earnings calls:

Impressive Growth Momentum: The company is demonstrating impressive growth across key performance indicators (KPIs). For the first nine months of FY24, we’ve achieved a healthy 11.02% volume growth. Furthermore, operational efficiencies have improved significantly, reflected in a 13.64% increase in EBITDA and a 9.56% growth in PAT for Q3 FY24 compared to Q3 FY23.

There has been significant improvement in the profitability: The addition of new vessels is expected to drive a significant increase in EBITDA per MT, with projections reaching Rs. 3600-3700 compared to the current Rs. 3400.(Five Years ago it was 2200 EBITDA per MT)

Confidently Targeting 18% Growth: On track to achieve the 5 lakh MT target set by management, representing an 18% y-o-y increase, compared to 4.24 Lakhs MT in previous year.

Ambitious Growth Plans: Management is guiding for a target volume of 7-8 lakh MT in the coming years, with the potential to exceed 10 lakh MT. This growth will be driven by leveraging our internal fleet and efficient logistics network.

Achieving the targeted volume of 7-8 lakh MT in the coming years, combined with our current EBITDA per MT of Rs. 3400, translates to a projected EBITDA of Rs. 220-230 crore.

Despite a robust 500,000-volume target for FY’24, achieving a 35% volume increase in Q4 presents a significant challenge, we can ensure successful achievement of our FY23-24 target, we’re positioned for a potentially exceptional final quarter of FY24.

Significant improvement in scale of operations or sustained improvement in operating margins above 8%, leading to higher cash accruals.

Opportunities:

The Indian government has allocated Rs. 2,78,000 crores for road, transport and highways in the 2024-25 interim budget. This represents a significant increase compared to the Rs. 2,70,434 crore total order value carried over from 2023-24.

PSU like HPCL and BPCL have a combined production capacity of around 5.5 million metric tonnes per year (MT/year). However, current demand sits at 9.5 MT/year, and this gap is expected to widen further to 14 MT/year in the next 3-4 years.

Challenges:

Port Congestion Hinders Growth: Our biggest operational challenge is congestion at loading points in ports. This intense competition for loading space can delay our vessels by 7-10 days. As a result, securing raw materials becomes difficult, and we may be unable sometimes to meet the full 1.5x surge in total demand.

Strength’s:

The market opportunity is tremendous and we have captured almost 20%-30% of the bulk market share in Bitumen in the private sector. [ Market Leader in Bitumen Space]

Our Unique Edge: Our nationwide presence with manufacturing plants near key ports gives us a logistical advantage unmatched in India. We combine shipping with this robust network, unlike competitors who lack either our integrated infrastructure or extensive distribution.

Promoters with over 40 years of experience provide deep understanding of local and global market dynamic has resulted in a significant 36% CAGR in sales for the past three fiscal years.

The group’s ship chartering business is a strategic move, expected to offset 60-70% of the parent company’s freight expenses. This creates a cost-saving loop that leverages their diverse operations. By optimizing logistics costs, the group is well-positioned to achieve its EBITDA per MT target of Rs. 3600-3700.

The company plans to use debt to finance new vessels. However, this strategic capital expenditure (capex) is not expected to negatively impact the capital structure in the medium term. As of March 31, 2024, our key financial ratios remain healthy, with a projected gearing ratio of 0.51 times and a total outside liability to adjusted net worth (TOLANW) ratio of 0.77 times.

The company prioritizes order-backed purchases, minimizing the need for excess inventory. However, a small buffer stock (averaging 16-23 days’ worth) is strategically maintained to fulfil urgent customer demands. This approach has been successful over the past three fiscal years.

Counterparty risk is mitigated to some extent by a large and diversified clientele and established long relationship of 3-4 decades with major clients. It is also able to pass on its foreign exchange exposure to customers.

Healthy Liquidity Buffer: The company boasts a comfortable liquidity position. Expected annual cash accruals of Rs. 120-155 crore significantly exceed our medium-term repayment obligations of around Rs. 26-42 crore. Additionally, as of March 31, 2023, we held a substantial amount of readily available cash (Rs. 37 crore) and liquid mutual funds (Rs. 25.66 crore).

Weaknesses:

Although, company is able to pass on this increase in prices of bitumen to customers, inability to do so fully or lag in passing on, has led to some volatility in operating margins that have ranged from 6.3% to 9.1% in the past five fiscals, through fiscal 2023.

While the entity caters to cyclical sectors like infrastructure, industrial gases, and power, these industries are susceptible to economic downturns. During past recessions, construction slowdowns weakened the creditworthiness of some players in the sector. This can also lead to extended payment collection times (debtor days) from smaller clients.

Threats:

Vulnerability to Oil Price Swings: A key challenge for the company is the inherent volatility in bitumen prices. As a derivative of crude oil, bitumen’s price fluctuates significantly. These sudden increases or decreases can impact our operating margins.

Substantial increase in its working capital requirements or large debt funded capex, weakening its liquidity and financial profile.

AIL Research Report.pdf (614.4 KB)

2024-04-12T18:30:00Z

@pkeday

You are right about the tax benefit AICL as a group is getting because they set up a company in UAE. It is a smart move. But it much more smarter move than it appears. Why? The answer to this question will also answer the query you are struggling to solve.

You are not able to find the payment by parent to UAE subsidiary because the transaction is structured in the following way.

So, legally there is no transaction for freight between AICL and AICL Overseas. By structuring the transaction in such manner, the company has avoided the income tax as well as the transfer pricing police. You can cheer for the management here.

Now, with regard to your suspicion of overstatement of profit in UAE Entity, the management’s ability to park higher profits in UAE depends upon their relationship with the bitument suppliers, which are few as highlighted by @Rhythm on the basis of Credit Rating Agency report.

I hope your doubt is clear now.

Famous magazine ‘Wealth Insight’ from ‘Value Research’ has covered ‘Agarwal Industrial Corporation’ in the latest June issue.

I have blurred the main content because of subscription requirement.

Can you post a gist?

It was mostly what we already knew. They said that most important thing for the company is their assets, like Vessels, storage terminals, transport vehicles, because of which it is able to provide faster and cheaper bitumen to its clients.

Amongst the risks, one is that its growth is chiefly related to infrastructure sector mainly.

Q4FY24:

• FY24 Volumes: 4,90,813 MTs vs 4,23,925 MTs (15.78% growth)

•

•

• Company has plans to enter into the Bitumen market in North region of India, to increase its customer base and revenue

CONCALL NOTES:

• Our volume target for FY '25 is set at 6 lakh metric tons, aiming for a 20% year-on-year increase. So we expect some increase of around 15% to 20% in terms of revenue.

• With capacity constraints in India for bitumen and AICL being the only integrated player in the private sector for bitumen, we have been able to increase our market share.

• India saw a 6% increase in bitumen consumption to nearly 9 million metric tons.

• Currently, EBITDA per metric ton is around INR3.625 which we expected to increase to INR3,800/3900 per metric ton, reflecting our ongoing efforts to enhance profitability.

• Our economies of scale achieved from own feet of bitumen logistics vessels and road transport vehicles enable us to outbid competitors, secure tenders and ensure high standards of supply and service to our customers.

• Targeting 65-70% volume through own vessels (60% this year) (25-35% growth)

• Red Sea is not a problem for us because we are not going towards that side. We are coming from the Gulf countries to India, where we do not fall in between Red Sea.

• BITUMEN REALIZATION DETAILS: The total realization for the entire year has been comparatively low. Last year, the total realization was around 42,000, which this year it is around 36,800. We have lost nearly about INR300 to INR400 crores of turnover due to the price fluctuations.

Realization for this year should be than FY24.

• So ultimately our dependency on third party will stay till the time we have in house capacity of around or more than 2 lakh tons.

• COMPETITIVE CHALLENGES: Challenges we don’t see a great challenge because the company is well positioned in terms of locations and the logistics advantage that we have. I don’t think any other player in the entire Indian state is having the setup that we have already built in the last few years. We just have to turn around the throughput from the storage tanks or the storage manufacturing capacities that the company is having. So, we don’t see a very good or much challenge from the market.

• We have always been focusing on forward and backward integration. So, in the coming future, maybe the company may produce bitumen on its own as well.

• Debt is always cheaper than equity. If there is any plan for the company to add more vessels in terms of capex, the company will not dilute.

Agarwal is such a simple thesis.

Consistent demand for bitumen → consistent growth + increasing margins due to own vessels (This has been playing out for last 5 years and should continue to play out)

There’s lack of any big risk factor apart from execution risk.

All they have to is keep on prudently adding logistics assets and ensure product avaliability.

A consistent compounder.

DISCLOSURE: INVESTED (2ND highest allocation in terms of cost in portfolio)

This could be a concern for the company.

Can I anyone shed some light on the size of the production the govt. is targeting for bio-bitumen?

Or if someone gets an opportunity to ask the company directly about it, please do ask.

My thoughts on the latest guidance given by the promoters.

Volume growth: The management hinted towards growing the volume to 6lakh tones per annum for FY25. For them to achieve this number they will have to grow volumes by 36% annually (which they say is possible because of the factors like: Road infrastructure development and aftermarket, government spending)

Realizations: Better EBITDA per tonne and margins are expected in this financial year. If they are able to achieve realizations around Rs. 3900 per tonne. Then with the estimated volume growth they should be able to achieve an estimated EBITDA of =6,00,000 * Rs 39,000 = Rs 234Cr approx.

If we keep the pat margins unchanged (keeping the interest cost similar for the sake of the calculation) then the company should achieve a pat of approx Rs148 Crs with EPS of = Rs148 / 1.50 = Rs 98 (100 round off)

So can anyone from the esteemed members help me understand how does the valuation part work here: Company is trading at a P/E multiple of 11.60x for FY25 (considering this is the best case)

Even if the company’s realizations do not improve and remains same then also they will be able to do an EBITDA of 216Cr (@Rs 36,000 realizations) and a pat of 130Cr

Why is a company poised for growth is trading at this valuation. What are the risk factors here that the investors are taking into account?

Also the management has hinted towards doubling the volume in the next 2-3 years. So where does the valuation part lies. how should we value a company like this which claim that it is the largest bitumen logistic suppler player in the country.

As a disclosure, I am invested in the company and am trying to evaluate whether one should hold or dig deeper to find value.

One of the bigger factors keeping the valuations low is the absence of Institutional investors.

With the total free float just around 600-700 Cr, it is very difficult for FII/DIis to get a meaningful stake.

Nevertheless, i personally feel the situation is perfect for the company to grow at high speed.

Why the stock is sideways from a long time even after 2 quarter of good results?