I believe inventory and data cost will increase with increase in the revenue because as number of clients or number of advertisement grows, affle will have to buy more and more ad inventory. The thing to look out it is the number of CPCU should also increase with increased inventory because that’s where revenue comes from and it also indicates efficiency of the algorithm/AI with which consumer platform finds out target audience.

If we look at the Inventory and data costs in comparison with the Income, then it is around 50 to 55%.

What is the scalability of the business? People are taking scalability of affle? or will some other big player through affle from market. Slow in revenue is not good sign for affle.

Looks an interesting presentation on understanding the terms and overview of Adtech Business

from Brightcom Group a listed player in the same line of business as AFFLE, TradeDesk, AOL, etc.,

Adtech is what makes of the Internet tick. Ads are the lifeblood of the

internet, the source of funding for just about everything you read, watch

and hear online.

This company generates more revenue from foreign susbsidaries so consolidated financials is better compared to standalone

Promoter pledged shares are decreasing and once the company becomes DEBT Free this will go away

Yes Adtech companies like even TradeDesk do not pay dividend as they reinvest in business to grow multifold and capture market share

Profits and revenue will grow as the company says they are now going for a debt financing with a US bank and due to the cash cycle of adtech industry they are restricted by the growth due to tight cash flows

Disclosure: Invested in Affle and BCG both, above are my own personal opinions pls use discretion

Affle to acquire Appnext to strengthen the mobile app recommendation platform globally

Appnext basically an app discovery platform, it recommends app to the users, it is rated 3.7 in glassdoor.

I like this clause Affle will initially acquire 66.67% equity ownership in Appnext Singapore, with a clear path to acquire 100% equity ownership upon attainment of mutually agreed growth targets

Affle2.0 will focus on building sustainable market leadership in India as well as enhancing our competitive advantage globally through our technology innovations. The Appnext platform transforms ads into app recommendations as a service for consumers and thus strengthens our CPCU business model by enabling greater ROI for advertisers.

Sounds nice but easily are these executable is to be seen

You may be right about the company, but this point of yours cannot support your cause. There isn’t anything bad in changing name of the company after you acquire, especially when you are going to be in altogether different segment.

Subsequently in January 2006 the entire equity share capital of Tejus Securities Private Limited was acquired by Anuj Khanna Sohum individual Promoter along with Anuj Kumar and Madhusudan Ramakrishna. Thereafter the name of the Company was changed to `Affle (India) Private Limited’ on September 29 2006 https://www.business-standard.com/company/affle-india-73060/information/company-history

Although I very much want this Affle story to be true, but maybe you are right

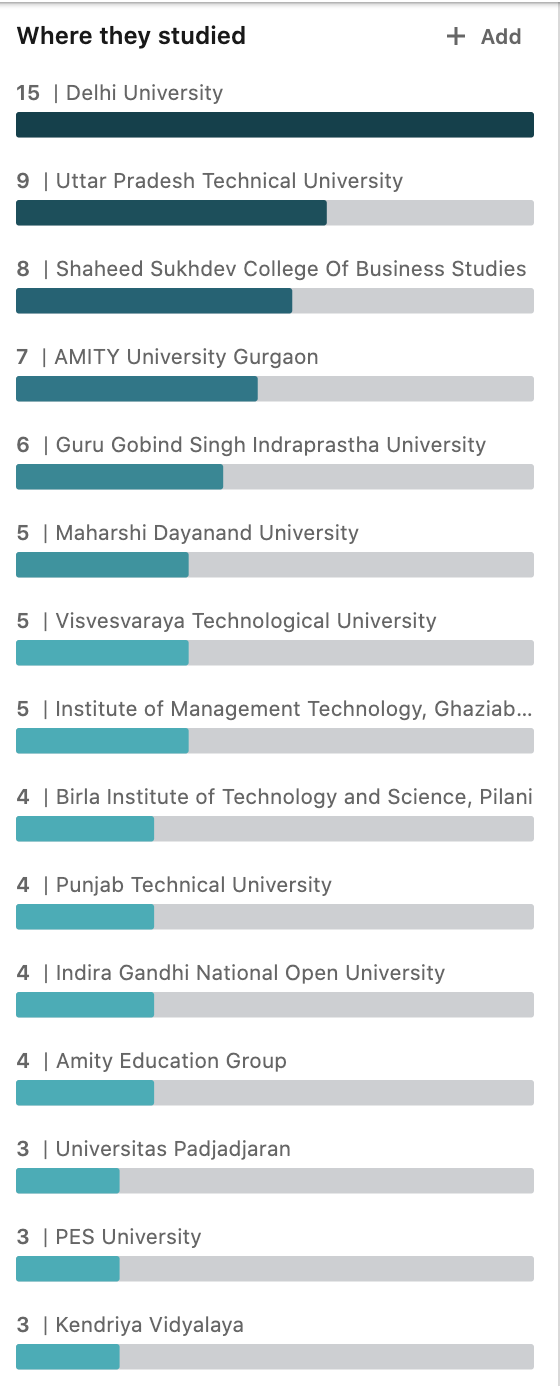

I did not find a single such tech profile worthy of being in such a team:

Their Lead Architect & technology director did his M.Tech from IGNOU(for those who don’t, it’s an open schooling program). Most of the license certification in his profile are not that great or expire this year, when in fact they should be shouting greatness! https://www.linkedin.com/in/kulpreetsinghlibra/

Many other employees have either no experience before joining or had little.

Also I talked to many employees, there ain’t any high end ML/AI being used, just data analytics, which is synonymous to using excel!

A look at what college the employees have been to LinkedIn Login, Sign in | LinkedIn

From a tech perspective there are only two engineers from BITS, Pilani.

Yet another concall to discuss (market!!) the acquisitions and the recent development. Don’t know it is over enthusiasm/transparency or the desire to prop up the stock or both. And a new term “Affle2.0”. I still feel this is a good bet if they don;t distract themselves but it is getting into my annoying zone.

I did not attend and will wait for call transcript. Q1 will not be great and there is a doubt about coming quarters as well. One must keep in mind that Chinese apps and other products like cell phones have been the biggest digital media spenders offlate. If they decide to take a backseat due to ongoing geopolitical tensions, it would hurt Affle during FY21. I think FY21 numbers will be in consolidation mode also due to the acquisition and folks need to be ready for the writeoff as far stock performance in the near term or FY21 goes.

This is major shift and of Google follows, only Self attribution networks and owned apps/OEM ad networks can run retargeting and personalized ad campaigns.

For rest , this effectively ruins the user preference targeting

In the short term and in India the iOS business for Affle may not be big, but retargeting business of RevX and Vizury will suffer. iOS users are also premium.

From what I know , the Amazon ad campaigns(significant part of revenue) came back in June but with half the budgets. Need to check how the advertiser spends and margins were this quarter across India and SEA for Affle.

ROAS and CPE campaigns will only be possible via the SANs that are able to do any form of fingerprinting via their proprietary SDK data and the revenue data they collect;

My point is not on iOS market share, but Google can also react the same way. Separately, iOS are premium users and high LTV

With the China app ban, the supply side disruption is more in favour of owned properties and app stores. Glance, Roposo etc can do better with self attribution.

This is a very good acquisition. Indus OS has Samsung supply and powers their app store, and hence better than Appnext acquisition. Samsung is a significant owner in Indus OS.