The markets are topsy turvy, and there is lot of unknown unknowns. Please be careful

1 . Mobile usage is increasing, and telco and infra firms will benefit. Not Ads players. Just because people are on mobile for longer time doesnt mean people will keep watching Ads and these Ads have an outcome. This is because, general consumption is down. Why would Myntra/Amazon advertise now when one part cant even open a warehouse and the other side like grocery/OTT is anyways getting huge organic demand and not able to service.

Brands are on digital, and if they would experiment they would goto larger players with cheaper inventory.

How is Affle comparable to Naukri/IndiaMart ? Please help me understand the profiling engine and outcome focus. What is different here, which is not available at much larger scale in other firms or even smaller affiliate networks. How many people have seen a Affle Ad on their mobile ?

They have cash, and would help them in these times. But valuation comfort is not there. All digital advertisers and startups in India/SEA are cutting or cancelling campaigns to reduce burn.

Everything has a fair buy price/valuations. IMHO - Affle, IRCTC and Indiamart are all buys in dips stage now - again we can agree to disagree.

Coming Qtr and possibly next is washout. Many small agencies will be in trouble and wont survive, those with deep pockets will gain.Affle is in good position to do that.

Profiling and outcome helps on stickiness - as far as their con calls go- still larger share is from top 10 or so customers - they got paid till now for a decade and dont see a reason to not see that continuing - infact on shrinking budgets an outcome based contract makes more sense.

Question on engine efficiency has been raised many times and is a valid one but am betting with past performance as proof.( you wont grow if outcome aren’t delivered, forget long term relationships)

These are the times where product/svc alone wont matter, it is risk, cash mgmt, mgmt quality and asset light model that will differentiate winners.

Again it is matter of conviction and future is really uncertain - I can be very well wrong as well , pl do you due diligence.

Mutual fund has increases its position slightly. However, Foreign port folio investors has decreased their position slightly. Any comment on shareholding pattern?

Teams are 100% working from home, management had experience with lockdown during SARS outbreak in Singapore!

They are well prepared and equipped to deliver from this wfh scenario.

Company has enough cash to survive for the next 2 years with Nil revenues, for the same reason none of the employees had been fired, although new hiring is paused

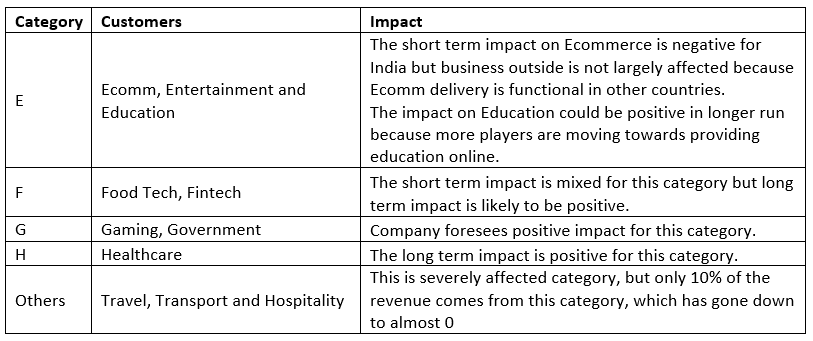

They had only 10% exposure to travel tour and hospitality, 30% in e-commerce worldwide, of that India is the most affected, rest are fine, they are hoping for a quick recovery in e-commerce worldwide!

Adoption of mobile phones is nothing like seen before, coupled with the fact that India is among the highest active mobile users, they are hopeful that advertisers would be forced to advertise in mobile platform.

Issues

Although they were unwilling to accept but there is going to be revenue decline and lower sales in this lockdown season.

Takeaways from Affle Covid19 Response and Outlook Concall on 5th May 2020:

Management laid out the effects of current situation at macro and micro levels.

At macro levels, there are three factors which are affected – Consumer, Customer and Competitors.

Consumers:

Screen time has gone up significantly during the lockdown period, which has increased the internet traffic. This internet traffic is more of inventory for the business.

Company’s efficiency to utilize this inventory at cheaper rate has also gone up.

However overall consumption (online and offline) has gone down because of the lock-down but management is positive that once lock-downs are lifted, the online consumption will increase as larger number of people would be moving towards online platform.

Thus both the factors – More screen time and more people moving towards online platform/shopping are favorable for company from long term perspective.

Customers:

Customers are nothing but the advertisers.

These customers can broadly be categorized as follows. The impact of Covid19 for these categories is as below:

Management is promoting and expecting positive impact on its Enterprise Platform (SaaS platform/ Licensing Platform) as there would more number of business which may want to increase their online presence.

The revenue so far generated through the Enterprise Platform is insignificant (approx. 3%), but any new business in this segment will have direct impact on the bottom-line growth as platform/product is ready.

Competitors:

Management believes that small competitors may not be able to survive in these tough times and thus Affle may get additional share in the market.

At micro level company covered 3 areas – Collaboration, Cash-flows and Consolidation.

Collaboration:

Management has experience of handling the business through similar situation at the time of SARC outbreak.

Benefitting from that experience management started work from home for South-east Asia offices and from 14th Feb for India offices.

Management has highlighted that lockdown has provided company with the level playing ground in the regions where company does not have their physical presence as all customers are being reached out through video calls. And management is hoping to get businesses from areas where they do not have offices, which wasn’t much of the case earlier.

Company has 80+ employees which are well versed and skilled in connecting with the clients online.

Cash-flows:

Cash-flows have been positive for last 6 years and management is working hard and in disciplined manner to keep cash-flows positive in these tough times as well.

Even if management was not openly accepting that revenues would be affected, but one could sense that there would be drop in sales and revenue.

Consolidations:

Company would be actively looking out for credible opportunities for the acquisitions are fair valuations.

Speaking on the question raised by the attendee on the cost effectiveness, management informed that they are not doing any hiring and are not planning to provide hikes. Management also highlighted that their travel and transport cost has gone down to zero because of lockdown and also informed that they are negotiating rentals for the leased offices as all of their employees are working from home.

Did some scuttlebutt on Affle, by having discussion with a friend of mine who is Senior Executive with a firm which works in mobile internet advertising. Had discussion on following

Business Model of Affle & its position:

In the simplest way, the business of the Affle can be explained as “Ad Exchange”, which is similar to stock exchange - a place where buyer and seller meets. In case of “Ad Exchange”, it is the advertiser and the publisher.

Like stock exchange, “Ad Exchange” also has bidding facility, where Advertiser bids for the online inventory of the publisher and whoever wins the bid, gets chance to feature their advertise.

Affle has product range which can be used throughout this value-chain. Affle has product for publisher and the advertiser. It also has strong AI which helps advertiser to find the appropriate/target audience for their ads and thereby increasing the ROI. It also helps Affle because of its CPCU model.

In this type of business having enriched user data is like a gold and since Affle is in this business from long, they have enriched user data and also has technological edge.

Thus as per my colleague, Affle has advantages that - It serves across entire business-cycle, enriched data and well developed products.

Sector Growth:

This is one of the fastest growing sector considering technological advancements of mobile devices and network.

Though the short term impact of the covid19 is negative for the sector, the long term impact would be positive.

My colleague’s firm has seen more and more people trying to increase their online presence these days, because online would be new way of business going forward. As a matter of fact, some of the clients from auto industry have seen growth in the online sales as people are booking the bikes/cars through online demo/tours rather than going for actual test-drives.

Thus overall mobile advertising sector and Affle could see positive growth in coming times.

Competitors for Affle:

I was giving stress on this topic because the answers given by Promoters of Affle in their calls were not encouraging and brief.

Though promoters of Affle like to call giants like FB and Google as their strategic partners rather than their competitions, the reality looks different.

There are various platforms provided by Google and Facebook which are very much similar to what Affle provides. Google has acquired the firm called “Double Click” which works in the same segment as that of Affle. The platform provided by google is “Google Display and Video 360” whereas the platform provided by Facebook is “Facebook Audience Network”.

There are two big advantages that Google and FB has over Affle - a) Quality and quantity of the data (which I already said, is a gold in this business) and b) Technology.

Google collects the highest volume of the data through Andriod devices, its own applications and by providing various kind of services used by other websites and apps. On the similar lines, Facebook also has vast amount of data.

Also, one more point to be noted here is, Google and FB get this data readily available and do not have to pursue anyone for it, which is not the case with Affle.

Affle has launched set of services for “Online To Offline” businesses, which is not much tapped by Google and Facebook, however FB has started to pave its way in this segment by doing tieup/acquisition of around 10% with the JIO. Facebook along with Jio are planning to go big in this business model.

Thus one needs to look out at Affle from its competition point of view.

Disclosure: 1.Currently analysing Affle, but not invested. 2. I am new to this field of investing and currently in learning phase/

I have super duper doubt on AI part which they have. I have tried them twice and i think they are far far away from any AI. Would be good to check with them what models do they use.

Most of the times in adexchange you rarely get consumer details. Hence, the data enrichment story I will take with lots of pinch of salt.

Having said that, like in an exchange business size matters which they have.

Pardon me if my question sounds rudimentary but I am kind of a person who is once bitten and hence twice shy. Can someone please let me understand what is happening in this script? Why it is in UC for last few sessions? What am I missing here?

Nothing has changed since last few days (or month at least) then why sudden euphoria?

I am asking this because similar thing has happened with me for couple of small/mid-cap stocks. They started making highs every day and before I could understand anything those shares took complete nosedive. Later I understood that some one big was doing “pump and dump”. Hence my alarms are up this time. All the companies were good but couldn’t recover thereafter.

Sharing some of positive developments that I see helping Affle stand out in current juggernaut

Management

Good and transparent preemptive con call about covid, details in thread and pl read transcript on bse if you haven’t

Recent leadership hiring for Product mgmt and engg - quality folks

Overall tone is very positive and aggressive( need to see in performance though)

Attractive offerings with outcome and demonstrated results ( this is subjective- deducing from reported numbers)

Macro

Digital mktg is easiest way to reach consumers in current scenarios, whatever mktg budgets are there for brands, digital will go up ( share will go up but absolute value may come down for short term, but that’s okay)

Demand supply for a listed player in this space- many hands chasing limited supply

Long runway

Performance

Decent performance for Qtrs gone by - limited history, it is perceived as high growth company

Governance seems good - again subjective and based on mgmt calls, walking the talk, investors in company( Microsoft)etc.

As per the last conf call they had mentioned if Jio is entering along with FB in Indian market for Retail then it will be competitive for Amazon and Amazon will try to push more for advertising. This may be one of the reason.

I think you have put out the sharpest of comparison, P/B 0.1, Revenue ~10X market cap.

Yes Brightcom is making profit and that too 30% OPM, I think the sale side company is doing great, no doubt on that

You would have to analyze the management, there is contingent liability & 50% promoters pledging, stock prices have dropped ever since October 14.

And to be fair you cannot do a direct comparison of companies like Brightcom with almost any other company, I guess its better to analyze the decisions taken by the company that led to this!

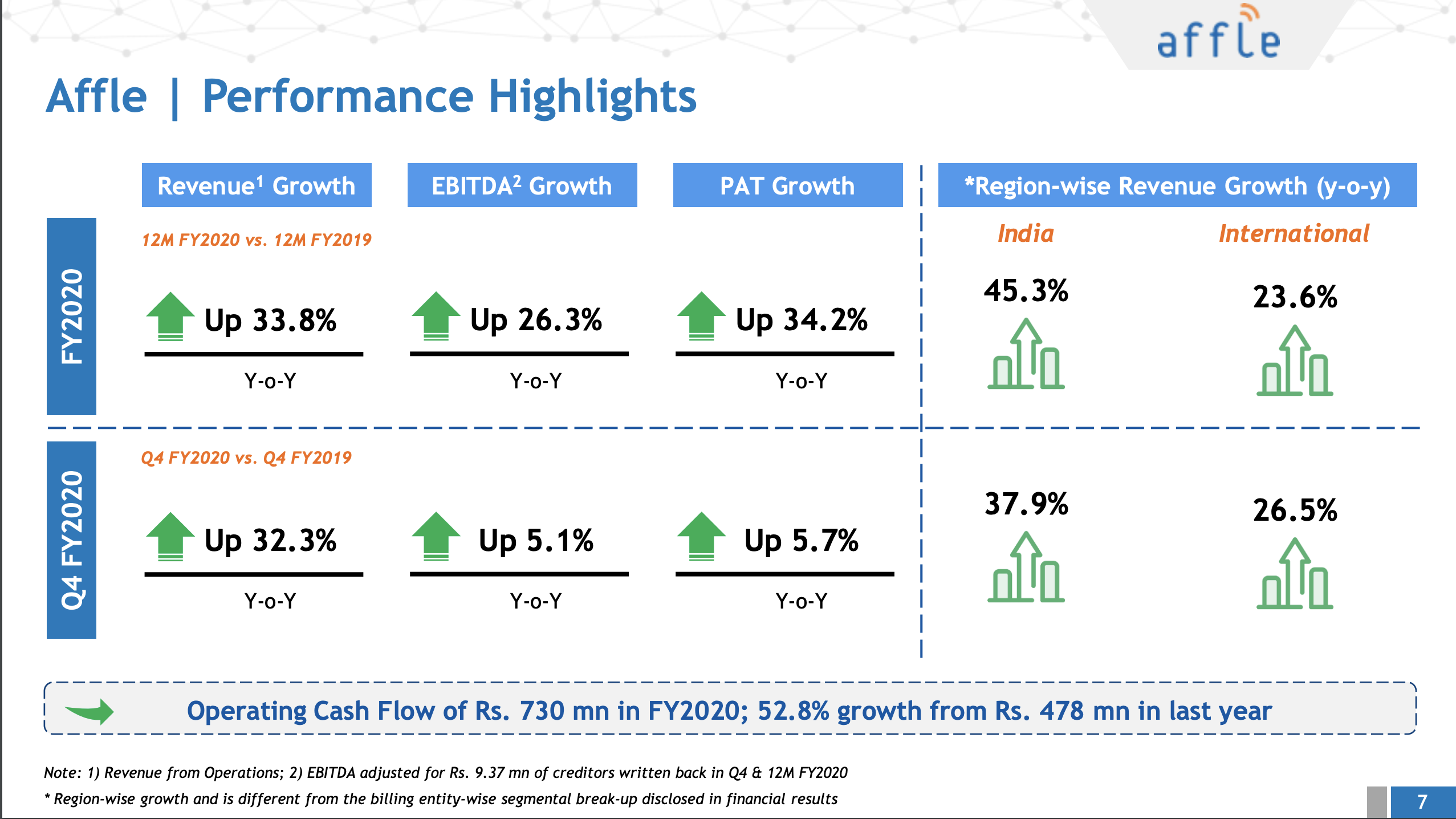

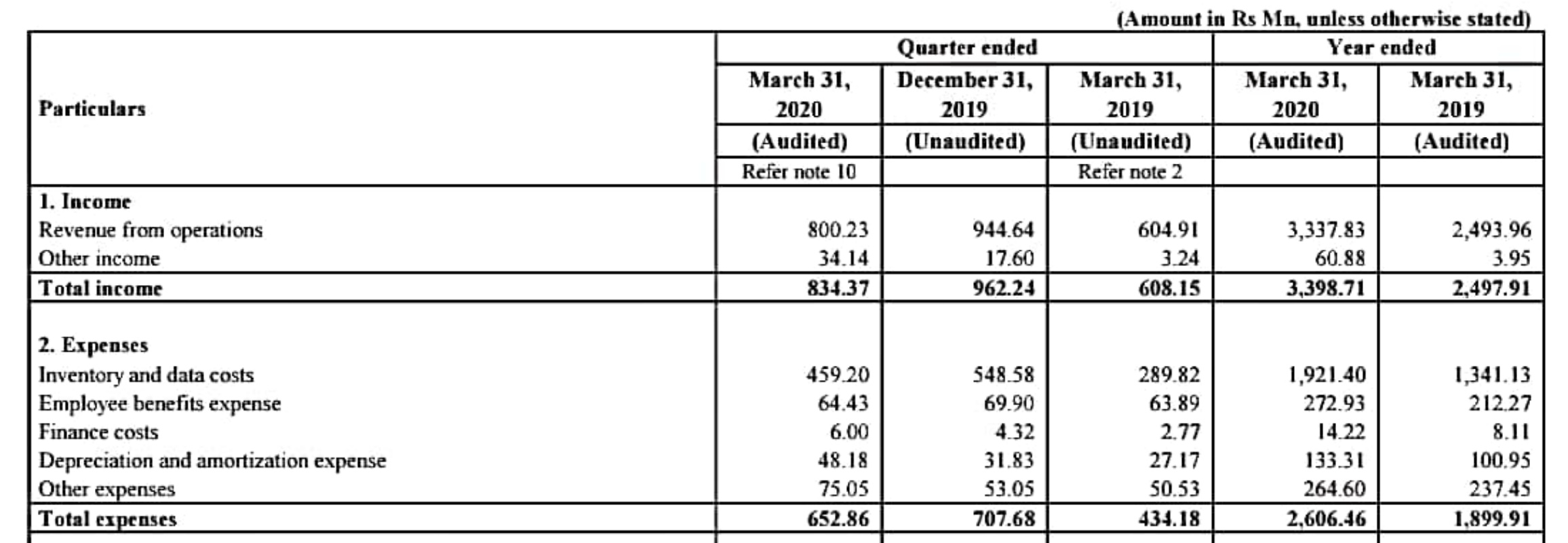

India Geo has delivered inline on top and bottom line. Global biz has got a drag on overall performance where bottomline hasn’t grown with topline.

Last con call ( early this month)Soham seems to be suggesting that they are buying inventory bit cheaper currently ( capex equivalent) as well as expect competition to weaken.

I would say good growth at annual numbers, mkt will be pleased in current context and need to hear mgmt commentary on bottomline challenges in Q4.

The data acquisition cost has increased substantially leading to EBITDA margin contraction of 5% yoy. Q4 performance is also propped up by one time write back included in other income. If you remove the same, PAT would have contracted yoy. Need to wait for concall to understand escalation in data costs and other expenses. I suspect other expenses item includes write offs of doubtful accounts or M&A related expenses. Cash flow is good but overall not a great set of nos. given the multiples it is trading.

Disc: Exited before the fall and remains in my watchlist.