@whipsaw My point is regarding 51% revenue from single country that is Indonesia?

Sorry, misunderstood.

My understanding is, as follows :

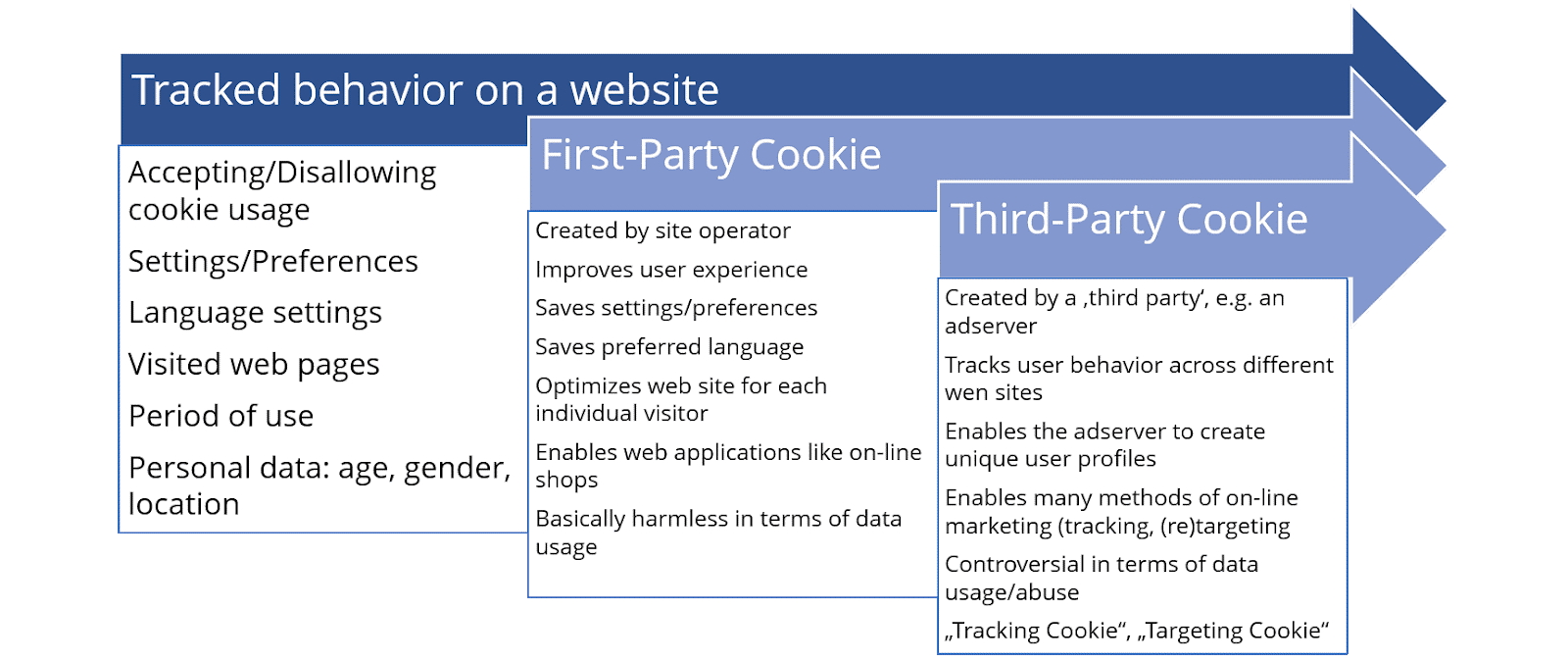

Adtech companies using ad networks collect user data. These data collections are mostly through cookies. Below is a simple representation of how data is collected.

If I go to moneycontrol.com, the cookies stored in my browser are first party cookies. Then when the page loads, third party ad servers store the third party cookies to track my behaviour.

The problem comes in data privacy with how these data are collected. Adtech companies like Affle use the above methodolgy to collect data. Only after collecting these vast data, whatever AI & machine learning they have can process it and identify and categorise user & their behaviour. So, IMO, there is nothing new here. They may be having some superior tracking algorithm but the user base is more or less common to all. Affle does seem to have the fraud prevention so ads clicked by bots can be prevented.

Regarding data privacy, I was talking about new government regulations coming into place . Don’t think this is relevant to their parent filings.

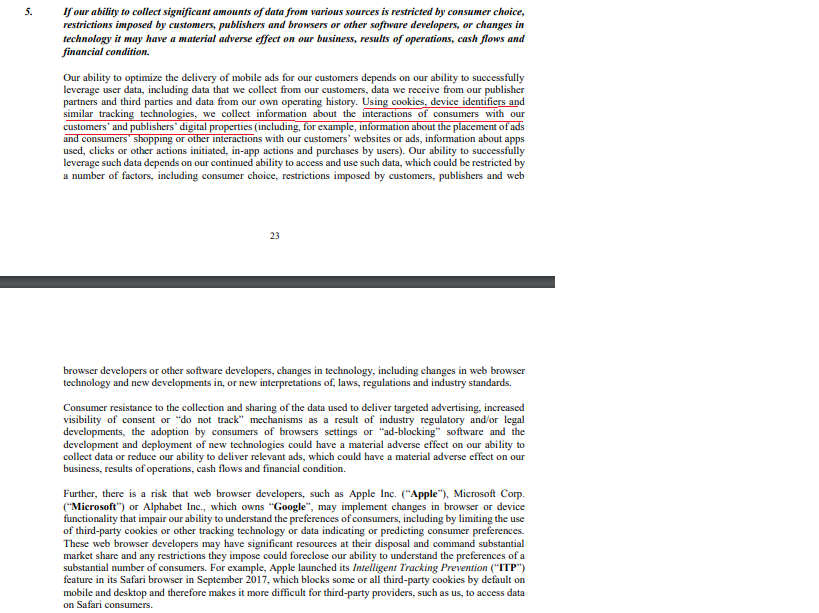

In fact Affle themselves recognized this in point 5 & 6 of RHCP under risks. They have explained how they track & how regulations like GDPR affected their revenue when it came in. Also these compliance should not only be adhered by them but mainly by their publishers & advertiser. So, not all is in their hands.

On this front, EU is about to go more stringent . GDPR only looked at personal data but there is serious discussions on another legislation ‘EU ePrivacy regulation’, where cookie’s are being looked into and explicit message & consent have to be given. This will seriously affect adtech companies. These regulations are coming not just at country level but even state level. Incase of US, California is coming with CCPA regulation on data privacy.

Basically, now it comes down to user consent. In all these cases, each country/region is going to mandate what information is going to be shared to 3rd party. If user says no, then adtech have to comply. If not risk millions in damage.

My point is, all these adtech companies have to be really nimble & adapt to the these changing regulations from time to time. Some of these could have serious & sudden implication on revenue.

This is the underlying risk, hence I am being cynical on adtech as a investment.

13 Likes

- They have very insignificant Non Asia business

- Mobile ad tech is on devices ids and not cookies and this is available with every other exchange running ads as well

- Anti-Fraud and transparency in supply to run performance campaigns is becoming a key differentiator and apart from walled gardens ( Snap, TikTok, FB/Google) and SDK based networks, others are not able to provide impression level transparency.

3 Likes

May not be a serious threat now but even Mobile App based advertisements are at a risk considering the advent of AdGuard (Freemium. Paid is very much affordable) or AdGuard DNS (free). This is the most popular one out there but there are others too which are capable of blocking ads in App UIs.

I don’t consider them as a significant risk now because:

- Google or iOS App Store do not allow them to list. Interested users need to go to their website to download.

- These are popular among geeks & their friends & relatives. So, the user-base is still not large.

But things may change epidemically if Google or Apple changes its policy and allow such apps in the App Store.

Ads are desirable only for Publishers but not for consumers, who are fed up seeing not-so-meaningful ads which sometimes redirect to malicious sites.

TBH, Ad-blockers are harmful for the publishers who publish freeware apps or websites, but it can’t be denied that ad-blockers are here to stay as long as they are in demand. I think the future of advertising will be quite different than what it looks now. For example: App makers may be willing to release much-less-featured freeware version and nudge others to upgrade to payware with better features or some other paid services without using third-party ad-servers [some already do].

Disc. The opinion is personal. I’ve been a tech savvy user & use Ad-blockers. I’ve been a publisher too but prefer to keep website Ad-free & choose to monetize in a different way. You can find relevant reference by searching on Google.

11 Likes

-

They have stated in risk 6 that their Europe revenue is 11% for last FY. Also non Asia geography is significant growth area , isn’t it ?

-

According to point 5 of RHCP risks , they have stated they use cookies. Also, one of the EU regulation is looking at cookies regulation. Tomorrow it could be something else. Key point is every government now is looking at data privacy seriously. All I am saying is these are headwinds that could affect company all of a sudden. Non compliance penalty is also huge

-

Agree that seems to be their moat

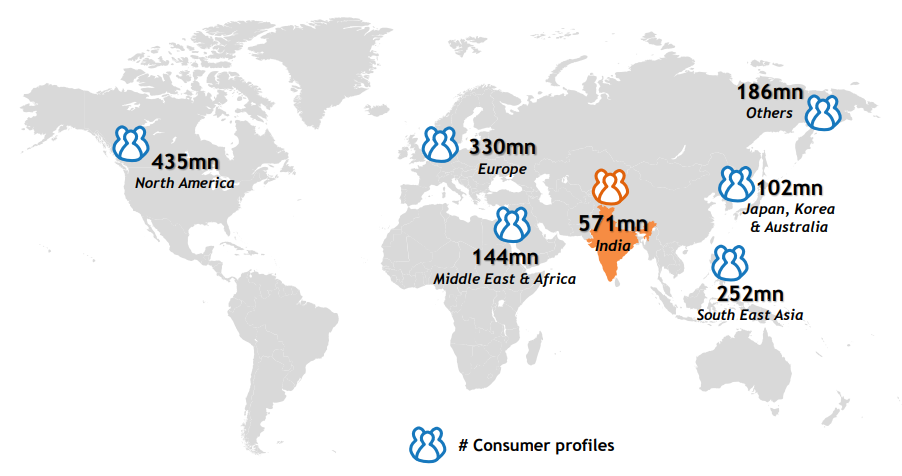

Affle claims to have 571 Million Consumer Profiles in India (Source):

That’s more than 40% of the Indian population.

Also nearly all of the Mobile Internet users in India (About 600 mn+).

Can anyone answer the following questions:

- Can a single ‘consumer’ stand for multiple consumer profiles? If yes, how do we verify what is the average for each ‘consumer’?

- If no, I’m curious to understand the method in which Affle collects this data. Because collecting the data of 99%+ of the Internet users in India is great. A little too great.

- In 2014, InMobie claimed to have about 800 mn active users (Source). I know some time has passed since then and I couldn’t find the current figure. Let’s say at 20%, it is about 2 Billion now. But Affle seems to have almost half as much as InMobi, which is spread across 200 countries. How is this possible? (Maybe there is a difference between ‘active users’ and ‘consumer profiles’, which could be certainly flying over my head).

9 Likes

As per their RHCP,

- ‘Each consumer profile represents a unique device id’

- How do they get data

Given Affle’s customer base is not yet big, I believe its by c) they have acquired the most data.

2 Likes

Great opening results by Affle India. Seems they are benefited by the seasonal factors in Q2 while growth in ex-India region is muted. Will be an interesting concall on Monday. But it is trading at steep valuation though.

1 Like

Can someone through a light on high recievables… I fear another MRSS repeating here

This is just one quarter after listing and they show substantial jump in OCF yoy. It is growing substantially and small company so some build up in working cap is given. One could wait till concall to have more clarity. BTW what was the key trait you think is common with MRSS? As far as I recall everybody and his uncle was bullish on MRSS till the fraud was found out. So the crowd was wrong on MRSS and this is opposite of saying I found another HDFC bank. Needless to say that I am biased as I am invested

2 Likes

Please dont delete your posts. I hold Affle. I would very much welcome all negatives to understand my investment better. I am not happy with the low cash flow from operations in comparison to profits. Receivables have increased and that is a fact.

I would be keen to understand if that is red flag or it can get resolved over time.

1 Like

I was very new to the market and had very little understanding of the BS when looking at the market frenzy and aura of MRSS i invested in the counter… Still i dont have much of knowledge… But all i know i had lost a sizeable amount of my hard earned money in MRSS. Today on seeing the result i noticed that receivables has doubled, ratios and other returns are superb. May be that is the nature of industry… I posted it because i dont want to loose my money again and want to have a view on it from the people at the forum because they know much more than i do.

Well, without adequate listing history and deep access to the management, we all are in for part speculation and part analysis as far as investment rationale for this stock is concerned. It is best to follow and build conviction to buy/sell before passing any judgement. I would just add that one needs to spend sometime to understand the industry. FYI, it deals with ad agencies and that is one reason for a longer working capital cycle. We’ll understand better as we go along but you could check a listed peer in US i.e. tradedesk which has done very well for its investors.

Regarding MRSS, there were enough red flags for me right from the beginning but folks ignored due to superlative P&L. Also, the stock gave enough signals to exit even when most were in profit.

3 Likes

Todays world things are changing rapidly so one can not take any longterm call …

In affles case u can be bullish for 3 5 qtrs but that much premium is already there in CMP…

So according to me dont be over optimistic on the story,!

management or decision making heads are very much concentrated and they dont have large experience …

Disc. Not invested

1 Like

Can anyone please share Nomura’s report on Affle released today?

did anyone attend today’s concall held at 11am. Looks like whatever they said has made investors happy.

If you have notes please share the same

The major concern before the concall was regarding increase in Receivables. They clarified that the bump in receivables was due to settlement of certain contracts related in acquired companies which happened in October. Corresponding bump in payable is also there.

They were confident that second half would be better like last year.

They clarified that privacy issue is not a concern for the company and the company is compliant with the regulations as per Singapore and European regulations and welcome any regulations in this regard.

They explained India is their focused market and see a long road ahead.

They have 280 people (180 technical) and no increase is anticipated unless some acquisition happens.

5 Likes