In any case, this is all temporary. The world won’t stop because of pricier ATF. Cargo movement will also go on. Only the final customer will bear the brunt of inflation. Till he won’t be able to. But that scenario seems a bit farther into the future. And if hyperinflation happens, all sectors and stocks will likely go down.

2 Likes

A few questions which bother me:

- 30%+ PBT and 20%+ PAT margin of the company. Is this normal? Can you fly aircrafts and drive such kind margin? If this not normal then what is Afcom doing operationally to have such high margins? If this is normal then why aren’t incumbents airliners competing for it? If this is not normal then what will the normalized margins look like?

- Why does the companies deferred revenue expense keep increasing? It increased from INR 24 Cr in FY24 to INR 64 Cr in FY25? Seems like it has increased by another INR 30-40 Cr in FY26. Is this classic capitalization of expenses to inflate profits? Good companies don’t capitalize manpower related expenses even if those are pre-operative. This can explain the high PBT and PAT margin. It would essentially mean that the company is barely breakeven.

- The company generated INR 90+ Cr in PAT for 9 months FY26 but it generated less than INR 10 Cr in CFO. The major impact was due to increase in other current assets - not due to the core working capital part.

This doesn’t smell good. Do you think the company is adopting questionable practices to prop up the profits? If profits don’t appear high then the stock price will collapse. The company is burning money. It won’t be able to raise capital through QIP etc. And even if it does raise then it won’t be able to raise at high prices - the promoters’ shareholding is low (just about 40%). At lower prices the promoters will get significantly diluted.

If we adjust this capitalized “deferred revenue expenditure” and take to P/L then the PAT margin would be 7-8%. This sounds about right for a company operating aircrafts. This also means the company’s actual PAT is INR 25 Cr for 9 months. The company is trading very richly 55x PE.

Will request folks to check this.

2 Likes

This is not just the initial lease rental. Seems like Afcom management is capitalizing all the expense. Also, this has kept increasing, it increased in FY25, it has increased for 9 months FY26. Questionable accounting practices in my opinion which has led to inflation of PAT.

Can you share the details of the prompt which you used to get the response from AI (and which model)? What were the references made by it etc. Routes and general data seems OK.

My manual search shows drastic decline since ATF price increase on 1st April.

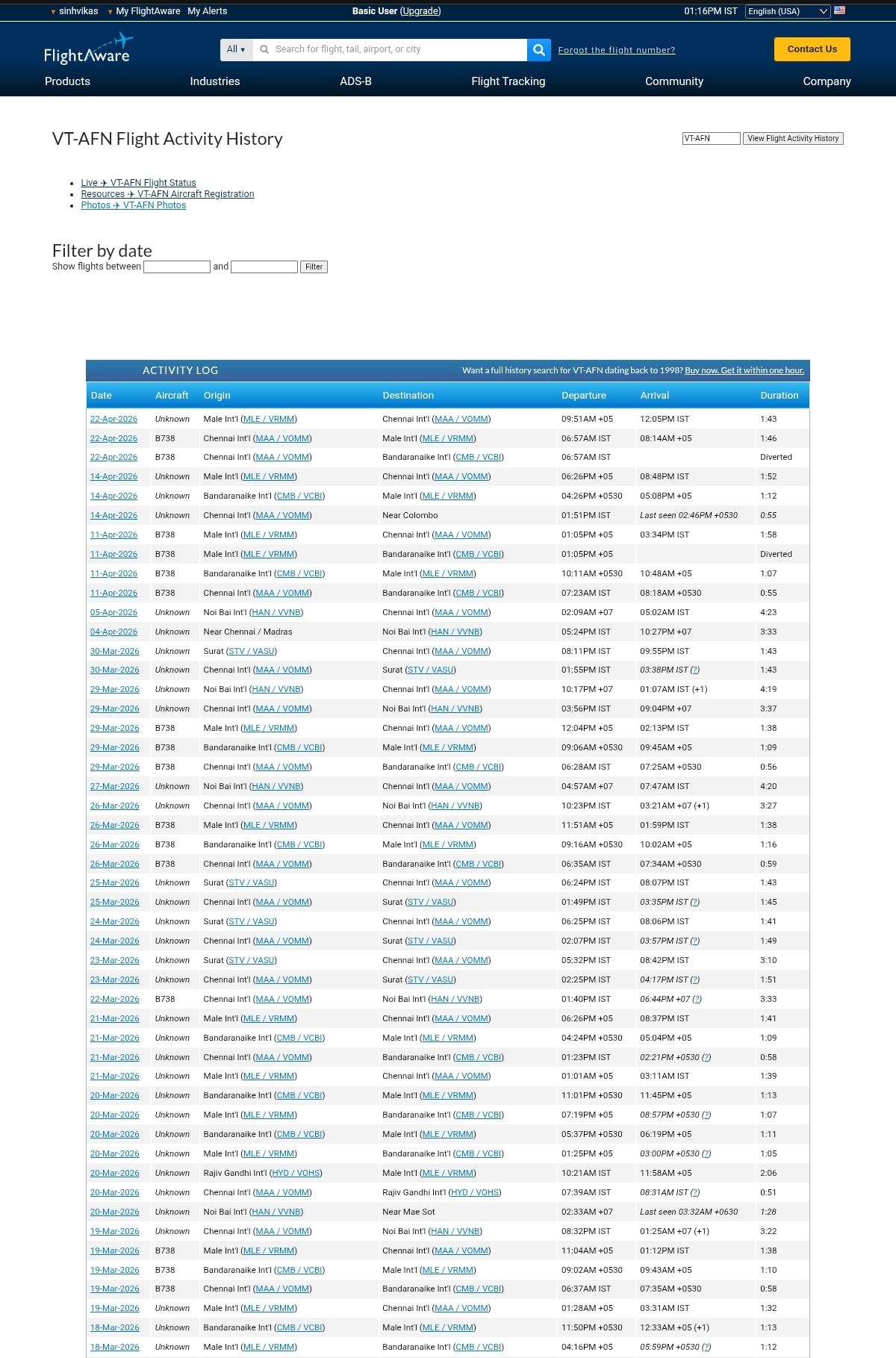

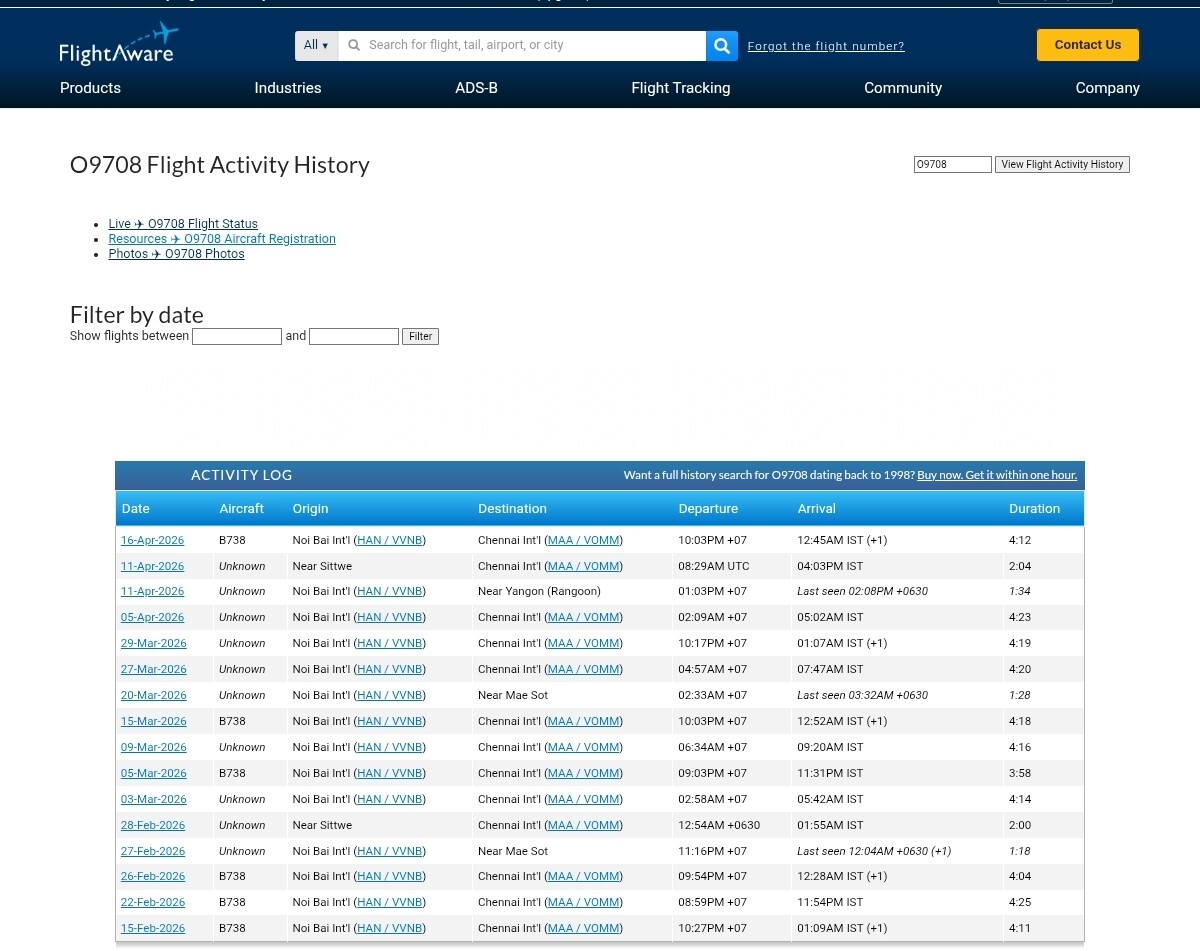

VT-AFN the newest addition

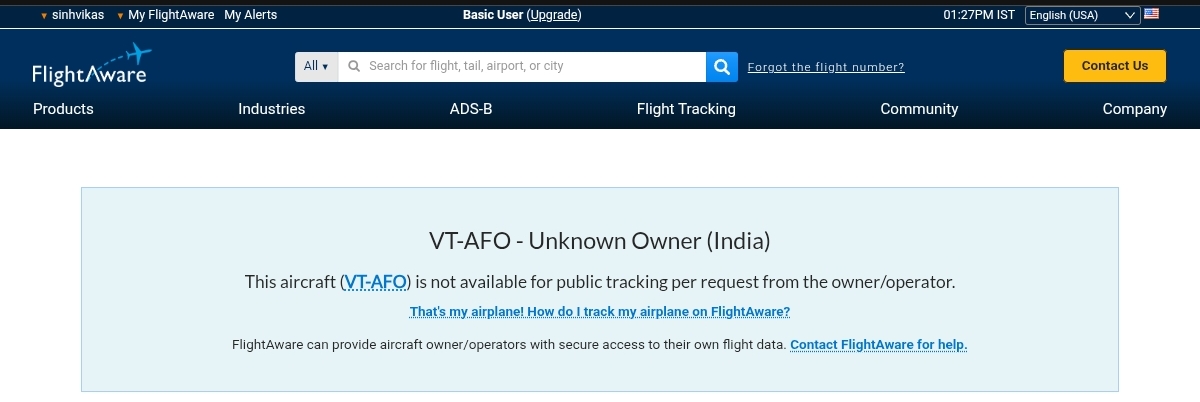

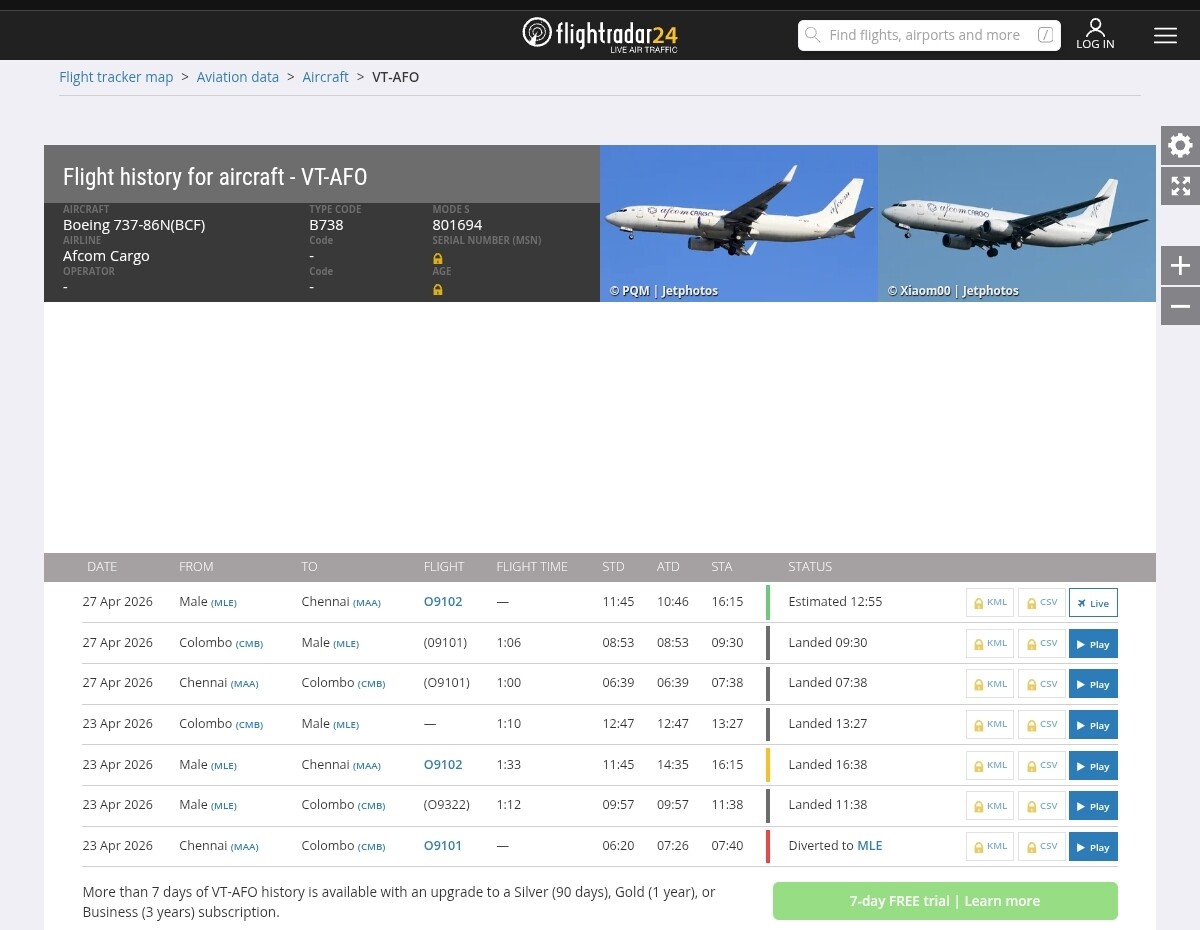

VT-AFO flightaware.com refused to give tracking info but limited info is available on flightradar24

But it was available with the flight number (which changes with the route) and the frequency seems mostly OK.

VT-AFC may be since pure domestic use hence couldn’t get the tracking information anywhere.

With domestic scheduled carriers getting ATF at heavy discount, it might be the case that passenger flights belly loading works much cheaper than Afcom. Also demand may be not so inelastic to the price shock.

Disc : invested

2 Likes

I think this is mostly incorrect.

Since the war started, after an intial rise, there has been a decline in flights to Hanoi, Myanmar, etc - a few gap days even. This is apparently due to fuel shortages in those regions.

The Male Colombo route seems to be in tact.

Also I could not find any flight information regarding the VT-AFC plane on public domain.

Can you quote the source cited by the AI ?

1 Like

VT AFN and VT AFO are the existing 2 aircraft.

Flightadar gives data for all flights as I have seen chennai to surat trip shown there.

There is no official info available for name of third plane that I could find.

I would like to study the balance sheet strength of the company if the situation continues while paying for 3 aircraft lease and crew salaries.

Disclosure-invested

I don’t understand why esteemed and learned members are ignoring capitalization of expenses which is inflating PBT and inability of the company to generate operating cashflow despite generate such high PAT. What am I missing? This kind of economics is just impossible to achieve in a aircraft business.

1 Like

Here is the missing link in my view…they need more funds so they are doing QIP @800.

PnL needs to looks better to get the better valuation.. I can’t see any other purpose to capitalise the expenses

1 Like

Do you think big investors who will pour in multi crores in the QIP will get so easily fleeced?

To answer this there is only one question.. is business is bad? No.. business is not bad.. They are planning expansion aggressively.. they will require a lot of funds for that purpose.. over the five years we may see a good business in this one .. PnL issue is very short term issue..

Long term growth story is still intact in this one..

Disc: Holding tracking position

What’s the problem with capitalisation of expenses?

In this kind of business, no one will account the acquisition of aircraft as a one-time expense when the aircraft will be used over multiple years in future

4 Likes

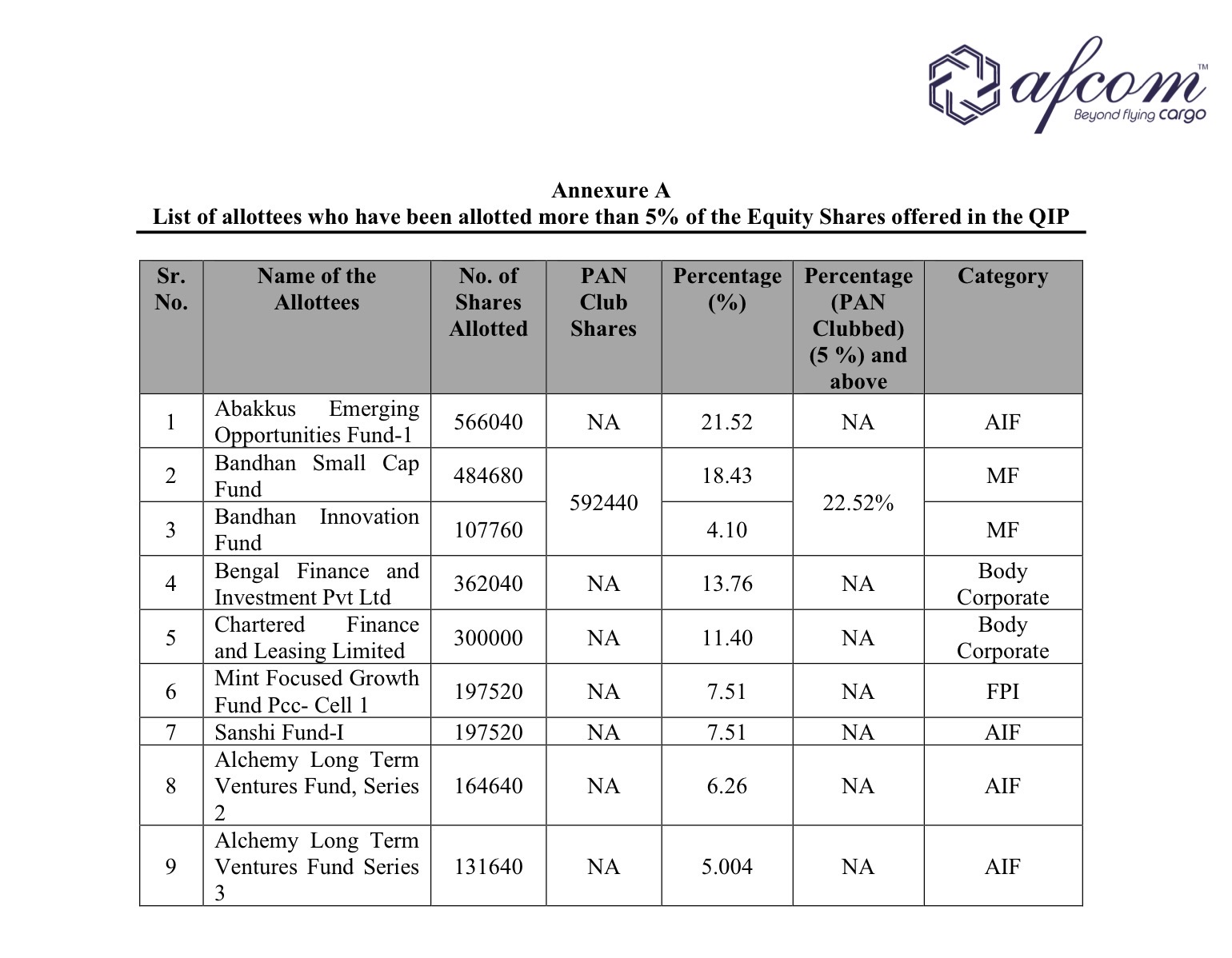

Do QIPs have a lock in period ? If not there could be selling pressure as these funds are already sitting on about 28% gains from the QIP price.

2 Likes

This leads to distortion in a few areas:

- The stock artificially starts to look cheap when the multi year forward growth is already baked in the price

- The margin profiles look very high which are not

- The theoretical profits never convert into cash, so the company needs to raise more fresh capital leading to more dilution of existing shareholders

- No one is questioning capitalization of purchase of any equipment which are put in long term uses. But they are capitalizing operating expenditure such as a significant portion of employee expenses get capitalized but the employee expense is for services provided by employees in the last month. It has nothing to do with future

1 Like

Yes absolutely. Fooling the investors. The artificial profits are not converting to cash flow, so the company needs to raise more fresh capital which leads to dilution for existing shareholders

1 Like

additional credit flow of Rs.2,55,000 crore (including Rs.5,000 crore for airlines)

Will afcom or FlySBS benefit from the credit scheme rolled out recently?

1 Like

It mentioned only scheduled passenger airlines

Eligible borrowers: MSMEs and non-MSMEs with existing working capital limits and scheduled passenger airlines having outstanding credit facilities, as of March 31, 2026, provided their accounts are standard.

3 Likes

I see, thanks for pointing out!

Any investor - big or small can lose money. As investors become they make more mistakes because they’ve analysts making a case for the stock without enough DD or more on the hope. Also for them beating benchmark is all that matters. Moreover, at portfolio level these small positions won’t matter to them.

Where do you see the capitalisation of opex like employee expenses, etc. Can you please share

1 Like