It’s a biased analysis…

crap

2 Likes

Advait Energy Transitions has secured a contract from Karnataka Renewable Energy Development Limited for the design, development, deployment, and maintenance of an online portal and mobile application.

This is part of the PM KUSUM Component ‘B’ scheme to implement and manage 40,000 off-grid solar pumps in Karnataka.

Duration: Deployment to be completed in 1 year, followed by 5 years of operations and maintenance (O&M).

2 Likes

Advait Infra

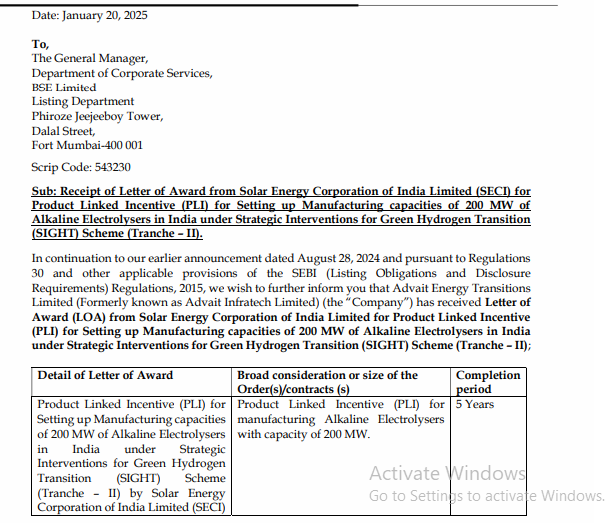

After solar pump order… Now expanding 200MW electrolyser capacity with PLI support under green hydrogen scheme

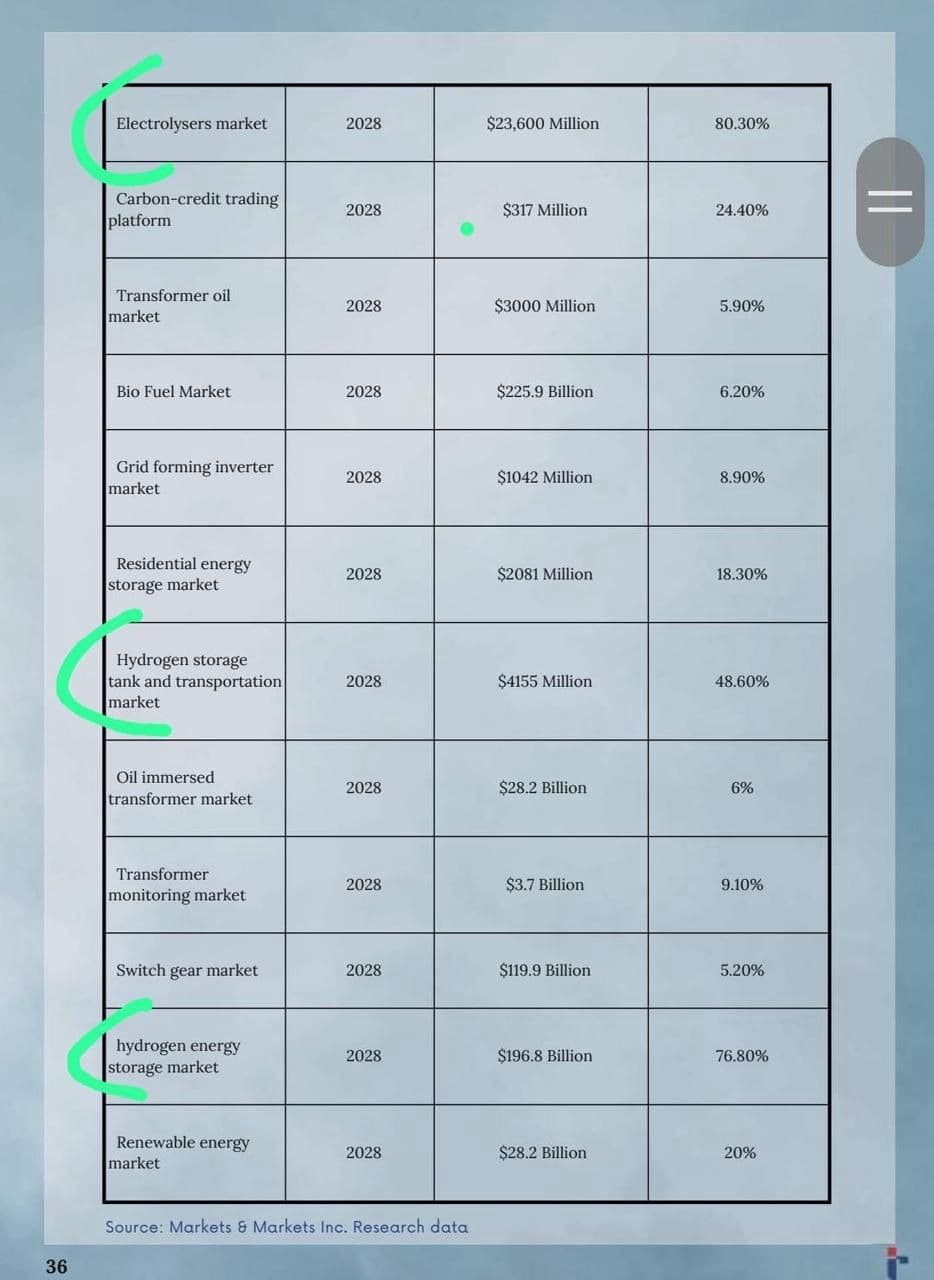

This is from annual report of TARIL, Electrolyser will be the highest growth market in renewable space

I see a bright future for Advait

9 Likes

any updates on this?

Sir, With all due respect I see that this analysis says that these guys are running all over, they are in IT (Software Development) department as well, but I could not see any such things in recent earning PPT.

Reason to ask : added few tracking positions

1 Like

Concall- Q3 FY25

- Carbon credit business can be 10X in coming years, They are expecting to generate ~2 CR in next year without deploying any money

- Order book 476CR Total- Out of which PTC business order book - 272 and NRE -203

- Fuel Cell JV target 4GW in 3 year

- EBIDTA should be in 15-18%

Note: Call was not very clear (Lot of disturbance), no transacript available, so if I misheard something apologies for that

Disc: Added tracking positions

4 Likes

is anybody aware of revenue share from these verticals ?

have they announced who is the JV partner ? Have their started fuel cell assembly already, if yes how much they are doing now ?.

i went through their latest concall transcript, couldnt find any mention or any question about the future of their JV with TECO as TECO has filed for bankruptcy in December

Also couldnot find any mention of their JV with Jiangsu Goofu and potential of this JV ?

does anyone have any insights into this ?

Q3FY25 Concall detailed analysis:

Business Update:

Q3FY25:

-

Power Transmission Solutions (PTS) Division:

-

Contributes 90% of revenue (~₹210 Cr), indicating high reliance on this segment.

-

Includes manufacturing & EPC services for OPGW (Optical Fiber Ground Wire), Emergency Restoration Systems (ERS), Optical Fiber Cables, and Aluminium-Clad Steel Wires.

-

Growth Driver: Rising power demand is expected to drive transmission infrastructure expansion over the next 5–10 years.

-

Competitive Position: Among the top 5 companies in India for live-line installation of OPGW.

-

New & Renewable Energy (NRE) Division (launched in 2023):

-

Segments: Green Hydrogen (GH2), Solar EPC, Battery Energy Storage Systems (BESS), and Fuel Cell Manufacturing.

-

Projects Underway:

Successfully completed a GH2 microgrid project in Feb 2024.

1 MW GH2 EPC project to be completed by June 2025, which is having the revenue recognition about INR10 crores to INR12 crores and a 15 MW project is in the pipeline.

Solar EPC:

Targeting 100 MW credentials, with 30 MW to be completed within this month. normally the solar EPC project is giving the revenue recognition of about INR3 crores to INR3.5 crores per megawatt. And we expect that by end of the project or by end of the month even our first project will also have the realization to these numbers.

Secured 30 MWp Solar EPC Project at Khavda, Kutch, Gujarat worth INR 59 Cr

Vision: Completion of 500 MW of EPC Solar projects by 2026-27, Providing Energy solution by offering integrated Battery Solar packages.

BESS: Secured 50 MW project with GUVNL, under a 12-year annuity model. our revenue will be INR16 crores per year for the battery business.

Electrolyzer Manufacturing:

Won PLI allocation from SECI for 300 MW electrolyzer manufacturing capacity (100 MW + 200 MW).

Plant under construction to support 300 MW annual production.

Fuel Cell Manufacturing: Technology partnership with a Norwegian company TECO, with production expected by FY26.

RED ALERT: TECO 2030 filed for bankruptcy in Dec 2024. Advait’s fuel cell assembly vertical is in deep water.

- Initially focused on marine, train power, and heavy-duty commercial vehicles.

- Carbon Credit Segment framework:

| Aspect | Key Observations | Risks & Concerns |

|---|---|---|

| Revenue Streams | - Two main revenue sources: (1) Consultancy services for clients to secure carbon credits, (2) Selling self-generated carbon credits. - Also provides ESG policy advisory to Fortune 500 companies. | - Small initial revenue contribution (₹2 Cr from consultancy, ₹2.5 Cr from carbon credit sales in FY26). - Highly dependent on carbon credit market prices, which can be volatile. |

| Carbon Credit Strategy | - Company does not purchase carbon credits from the open market. - Instead, it generates credits for clients by advising on green hydrogen, battery, and solar projects. | - Revenue realization risk: Carbon credits will be booked only upon sale, meaning unpredictable cash flows. - Execution challenge: Scaling carbon credit generation requires long-term project execution. |

| Capital Deployment | - No direct capital expenditure from Advait’s balance sheet. - Costs mainly involve employee salaries and consultancy tools. | - Limited upfront investment reduces risk but could also limit revenue scalability. - Without capital deployment, expansion might rely solely on external partnerships. |

| Future Revenue Growth | - Management expects multi-fold revenue growth in 4-5 years. (Estimated 13 crores is spreaded between 3 years to 5 years.) | - Unclear revenue projections: No concrete growth targets beyond initial ₹4.5 Cr expectation. - Regulatory uncertainty in carbon markets could impact long-term revenue potential. |

- Secured total preferential allotment (Including Convertible warrants) of Rs. 107.44 Cr in FY25 out of which Rs. 88.58 Cr has been received and started deploying towards the business expansion.

- Emergency Restoration System segment update:

we have already developed this product with more than 95% indigenization that is a local content. We are further developing two or three new models with the latest kind of channels. We already built up the team and our factory is set. Further this year, we are also going to deploy the automatic welding machine to take care of the proficiency of the channels. And we look forward that we being among the very few manufacturers in the world and maybe one or two manufacturers in India at the moment, we take a position so that we can take the maximum market share for next 5 years. And this year it is going to happen.

- Order book status and break down (as on 31st Dec,24):

| Segment | Order Book Value (₹ Cr) | % of Total Order Book | Key Observations | Risks & Concerns |

|---|---|---|---|---|

| Power Transmission Solutions (PTS) – ₹273 Cr (57%) | 57% | |||

| DISCOM EPC (Distribution Companies) | ₹165.5 Cr | 35% | - Largest portion of the order book. - Linked to government spending on power distribution infrastructure (RDSS schemes). | - Policy & regulatory risks: Delays in government approvals can affect execution. - Payment delays: DISCOMs are known for late payments, affecting cash flows. |

| OPGW (Optical Fiber Ground Wire) | ₹35 Cr | 7% | - Steady business but small contribution to overall order book. | - Market maturity: OPGW demand is stabilizing, limiting high future growth. |

| Manufacturing (Tools & ERS-related) | ₹49 Cr | 10% | - ERS (Emergency Restoration Systems) continues to be a niche, high-margin segment. | - Slow new orders: ERS orders have stagnated since 2021. |

| Other Services (Miscellaneous EPC & Installations) | ₹15 Cr | 3% | - Includes smaller service contracts. | - Low-margin business with minimal growth impact. |

| New & Renewable Energy (NRE) – ₹203 Cr (43%) | 43% | |||

| Battery Storage (BESS) | ₹130 Cr | 27% | - Largest NRE segment, driven by the 50 MW GUVNL project. | - Execution risk: BESS is a new segment for Advait, so delays in implementation or cost overruns could occur. |

| Green Hydrogen (GH2) EPC | ₹14 Cr | 3% | - Small contribution despite GH2 being a high-growth focus area. | - Slow adoption of GH2: Government incentives are crucial for scaling this business. |

| Solar EPC | ₹59 Cr | 12% | - Includes both small-scale solar projects and potential expansion in solar EPC. | - Highly competitive industry: Solar EPC faces pricing pressure from larger players. |

Execution Timeline for Order Book

The ₹ 476 crore order book is split into:

Power Transmission Solutions (PTS) Orders (~ ₹ 273 Cr) → To be completed within 9 months.

New & Renewable Energy (NRE) Orders (~ ₹ 203 Cr) → To be completed within 12 months.

-

At the moment, we are executing our first solar project of 30 megawatts, which will be completed in the month of February 2025. We are looking forward for the pipeline of 200 megawatts of solar projects. We are not taking solar projects on IPP basis. We have been taking on EPC basis with a clear focus that we want to develop the first credentials for the 100 megawatts of EPC, which will help us for our future foray into battery and green hydrogen business. Thank you.

-

Currently, Advait Energy Transitions Limited is utilizing about 30% to 35% of its OPGW manufacturing capacity in its second year of operation . The company anticipates significant market growth in India and globally, projecting a compound annual growth rate (CAGR) of 15% to 20%. The government plans to upgrade existing OPGW from 24 fibers to 48 and 96 fibers, and there are discussions to include optical fiber ground wire in all 66 KV transmission lines. Additionally, many new transmission lines are under construction, suggesting promising prospects for the company in the near future.

-

Regarding RDSS Scheme: We hope to have the order book about INR200 crores to INR300 crores for this division very soon. We will be choosing the projects very carefully because we are not looking forward to have the revenue only from the RDSS. We have the technology skills. We have the skill set. So we will be choosing mainly the revenue, payment terms of the end customer and the segment where we can complete the projects in time. So, we hope to continue growth in this segment as we have achieved the growth in the last two quarters.

-

Regarding Carbon Credit : Advait aims to scale its carbon credit inventory 10x by next year (From current 1.4 million to 14 million) at minimal cost, leveraging its green energy business such as BESS, solar, green H2 etc. However, the lack of a defined monetization plan, execution feasibility risks, and carbon market volatility make this revenue stream highly uncertain.

-

Update about PLI: Our first PLI scheme will be likely to commenced for us from year 2026-27. And this will be remain continue over the period of 5 years and we are supposed to get the total PLI benefit for300 megawatts per year over the period of 5 years. So total PLI incentive available to the company is approx**. INR440 crores**. Besides the total 5 years, and the major portion should likely to come in 3 to 4 years

-

Advait’s JV with Techo: The joint venture between Advait Infratech and TECO 2030 aims to develop, manufacture, and commercialize TECO 2030’s fuel cell technology in India and the SAARC countries. Key goals of this collaboration include fostering local development and production capabilities, enhancing the renewable energy sector, and strengthening Indo-Norway ties. Advait will hold a majority stake (51%) in the joint venture, which will focus on leveraging TECO 2030’s expertise in hydrogen fuel cell technology to deliver sustainable energy solutions.

Investment of $2 million (~ ₹ 16.6 Cr) in the TECO JV to manufacture fuel cells in India.

Licensing-Based Model : The JV does not develop in-house technology but instead relies on TECO’s expertise, meaning Advait will pay licensing fees while manufacturing the fuel cells domestically.

-

Green Hydrogen & Fuel Cell Adoption in India

-

Market Potential : The company expects high adoption in the next 2-3 years, driven by India’s limited fossil fuel resources and high-cost power applications.

-

Target Segments :

Heavy-duty transportation & shipping : Fuel cells could replace diesel engines.

Backup Power (Diesel Generator Replacement) : Feasible if green hydrogen supply scales up

RED ALERT: TECO 2030 FILED FOR BANKRUPTCY IN DEC,2024.

- Advait Allocated total capacity of 300 MW in MNRE’s SECI’s (Solar Energy Corp. of India) PLI for electrolyser manufacturing. Advait sees opportunities in India’s green hydrogen & electrolyzer market, leveraging PLI benefits and EPC expertise. However, its small-scale entry, dependence on imports, and lack of immediate large-scale manufacturing put it at a disadvantage against bigger players like Reliance and L&T. The company’s “learn-first” approach to EPC before moving into full-scale manufacturing reduces short-term risk but also delays revenue scalability. Investors should closely monitor electrolyzer localization progress, order inflows, and cost competitiveness before considering it a long-term value driver .

Advait is setting up a fuel cell and electrolyzer manufacturing facility 30 km from Ahmedabad , spanning 55,000 square meters . The electrolyzer plant aims to scale up to 1 GW capacity in the next 2-3 years , while the fuel cell plant will initially have 50 MW manual production before expanding to 400 MW per year with an automated assembly line from ThyssenKrupp . The fuel cell technology is developed in collaboration with TECO and AVL (Europe) , ensuring high-end manufacturing expertise. This strategic investment positions Advait to capitalize on India’s green hydrogen transition , but execution risks and competition from global players must be monitored**.**

Management guidance about future business parameters/future strategy/CAPEX etc.

Q3FY25:

- the entire segment that we are operating in is robust attributed to the boom in power transmission line requirements due to increase in power demand. To support this demand, a lot of transmission systems and substation systems are to be built in the coming 5 years which is expected to provide impetus to the product segment that we operate in. We foresee the growth momentum to continue over the next 5-10 years.

- Top and bottom line growth: Advait aims to sustain 50% CAGR growth in revenue and profit for the next three years, provided it successfully expands product lines and secures industry qualifications. While management remains optimistic, execution risks, market conditions, and regulatory approvals could impact these projections. Investors should track order book expansion, margin trends, and certification progress to assess long-term sustainability.

- our NRE division is working with the battery and solar as one part, green hydrogen equipment manufacturing is the second part and the carbon and battery solutions is the third part. So, each division for the last year were in a nascent stage. So, we hope to have the very significant growth for the next 2 to 3 years. So broadly I can say that this year where we have the revenue mix of 90% to 92% with the PTS and 8% to 10% of the NRE. Every year, while achieving the growth, we will be able to have the NRE division’s numbers taking more and more share of the total business of the company. Broadly we can talk that it will grow by 5% in terms of product mix per year

- EBITDA Margin: Advait aims to maintain 15%-17% EBITDA margins , consistent with past eight quarters, while expanding in the New & Renewable Energy (NRE) segment. Management is selective in taking low-margin orders only when they offer strategic benefits like industry qualifications or long-term positioning. The company remains focused on niche, high-margin products and markets, ensuring sustainable profitability in the power and energy sector. Investors should monitor how this strategy balances growth vs. profitability as NRE expands**.**

- The green hydrogen project, that electro-cell project: Our manufacturing phase for the first 300 megawatts should be completed by year 2026. And we will be able to supply the same by end of 2026 and the first year of 2027.

- Future Plan:

Risks/Threats/Headwinds:

Q3FY25:

-

Solar projects are getting delayed or not coming as predicted, that is because of the energy transition phase because solar projects are equally required to be contributed with the battery project and other energy transition phases. So that is what precisely we are also working to work on other aspects of the transition energy

-

Potential Risk regarding JV with TECO:

-

TECO 20230 FILED FOR BANKRUPTCY IN DEC, 2024 AND THE JV IS IN DEEP WATER NOW.

-

A licensing model limits Advait’s intellectual property (IP) ownership, making it dependent on TECO for future innovations, upgrades, and cost competitiveness.

-

The capital commitment is relatively small, raising concerns about the scale of the JV and whether it can compete with larger players investing heavily in R&D.

-

Challenges & Risks in adoption of H2 Fuel Tech:

-

Green Hydrogen Supply Issues : Adoption depends on availability & affordability of green hydrogen, which is currently scarce and expensive in India.

-

Competition : Major industrial players like Reliance, Adani, and L&T are investing heavily in hydrogen tech, potentially outpacing smaller entrants like Advait.

-

High Initial Costs : Fuel cell adoption faces cost barriers since conventional power alternatives (solar, lithium-ion batteries) are cheaper in most cases.

This means that Advait is not investing in or owning solar power plants (IPP - Independent Power Producer) but is instead building them for others (EPC - Engineering, Procurement, and Construction).

Layman Explanation with Example:

Think of it like a construction company that builds houses for clients rather than buying land and developing houses to sell or rent themselves.

IPP (Independent Power Producer): If Advait took projects on an IPP basis, it would mean they invest their own money to develop and own solar plants, then sell electricity to make profits.

EPC (Engineering, Procurement, and Construction): Instead, Advait is building solar plants for other companies that want to own them.

Why Are They Doing This?

Advait’s goal is to gain experience and credibility by successfully completing 100 megawatts of solar EPC projects. Once they establish this track record, it will make it easier for them to enter the battery and green hydrogen sectors, where similar engineering expertise is needed.

Real-World Example:

Imagine a new construction company that wants to enter the luxury skyscraper market. Instead of immediately investing in and owning a skyscraper, they first take on smaller high-rise building contracts for clients to prove their capability. Once they have experience and a strong portfolio, they can confidently expand into the high-end skyscraper business.

Similarly, Advait is focusing on solar EPC first, so that later they can smoothly transition into battery storage and green hydrogen projects.

Critical Analysis of Advait’s Green Hydrogen & Electrolyzer Business Strategy

1. Competitive Positioning in Green Hydrogen & Electrolyzer Market

- The PLI (Production-Linked Incentive) scheme has attracted major players like Reliance, Adani, and Waaree, all of whom are setting up large-scale electrolyzer manufacturing plants.

- Advait acknowledges competition but argues that big players like Reliance and Adani are primarily producing electrolyzers for captive use (internal hydrogen production), not external sales, which could leave space for independent suppliers like Advait.

![]() Key Risk:

Key Risk:

- While competition from large players may be lower in external sales, companies like L&T and Thermax are also entering the electrolyzer market.

- Advait’s smaller scale and lower capital backing could limit its ability to compete on pricing, technology, and economies of scale.

2. State of Electrolyzer Manufacturing in India

- Current Status : Electrolyzers were previously used only at laboratory scale, but large-scale production has started in the past 1-1.5 years.

- Supply Chain Issues :

- Core electrolyzer components (stacks) are still imported, making India-dependent on global suppliers.

- Advait expects 85% domestic manufacturing within three years, aligning with PLI requirements (currently at ~60% localization, targeting 70%-80% in the coming years).

![]() Key Risk:

Key Risk:

- Domestic supply chain is still underdeveloped : If localization targets are not met, PLI incentives could be delayed, and cost advantages over global players may not materialize.

- Dependence on imported components means higher costs and supply chain risks, especially in geopolitical uncertainty.

3. Green Hydrogen EPC Business & Future Strategy

- Current Model : Advait is not yet a full-scale manufacturer of electrolyzers or hydrogen plants but is using a step-by-step strategy:

- Phase 1 : Enter the market via EPC contracts, executing small projects.

- Phase 2 : Build manufacturing expertise and gradually expand production.

- Phase 3 : Move toward fully integrated solutions by combining EPC services with in-house manufactured electrolyzers & fuel cells.

- Execution Status :

- Completed one hydrogen EPC project (microgrid-scale).

- Two to three more projects planned in FY26.

- Manufacturing of electrolyzers & fuel cells to start post-FY27.

![]() Key Risk:

Key Risk:

- Scaling challenges : Advait’s gradual approach means it may lag behind competitors who are investing aggressively in full-fledged manufacturing from the outset.

- Execution & revenue uncertainty : No clarity on profitability of initial EPC projects and how quickly manufacturing can scale up.

6 Likes

This podcast features TECO 2030 founder Tore Enger and was recorded about a month ago. It appears that TECO is still operational. From what I gathered, TECO licenses its technologies to companies like Advait rather than handling manufacturing in-house. Additionally, TECO collaborates closely with AVL, an Austrian company specializing in hydrogen vehicles. He talks about TECO’s engagement in India and he is very enthusiastic about India.

1 Like

TECO 2030 filed for bankruptcy in Dec 2024due to an inability to secure sufficient capital for continued operations. This decision followed financial struggles, including a $30 million loss since its spin-off in 2021 and bankruptcy proceedings against its subsidiary, TECO 2030 Innovation Center. The implications for its joint venture with Advait Energy remain uncertain, as TECO 2030’s insolvency disrupts plans for local manufacturing of PEM fuel cells in India and SAARC countries. However, a new entity, Teco2030 Energy Solutions, has been formed to potentially continue operations regarding the JV with Advait under a revised structure

4 Likes

Advait secured a order of Rs 86 crores (approx) from Power Grid Corporation of India Power Grid Corporation of India Limited. Same solid reaction reflected in their price today as well.

2 Likes

As company is building new verticals, i.e., NRE here is my 2 cent

- Green Hydrogen (GH2) EPC & Electrolyser Manufacturing

Under an NGHM, the target si at least 5 million metric tons (MMT) of green hydrogen production per year by 2030. (i.e., $8 billion by 2030) The domestic electrolyzer manufacturing opportunity alone is projected at $5 billion by 2030. This growth is driven by expected demand from oil refineries, fertilizer plants, steelmakers, and export markets. Additionally, a production-linked incentive (PLI) scheme for electrolyzers (run by SECI) awarded 1.5 GW of manufacturing capacity to multiple firms in 2024. Incentives were won by eight companies for electrolyzer technologies, like Reliance Industries, Jindal Steel, Adani New Industries, L&T, Greenko (with John Cockerill), Ohmium, Advait Infratech (AETL’s group), and Homin, which secured capacity under this PLI.

Major Competitors in India:

Reliance Industries (building a gigafactory for electrolyzers with licensed tech from Stiesdal/Nel)

Adani New Industries (partnering with Total Energies, and with Ballard for fuel cells),

Larsen & Toubro (L&T) (engineering giant tying up for electrolyzer technology and projects), Indian Oil Corporation (IOC) (pilot plants and planned electrolyzer facilities with partners), ACME Solar (developing large green ammonia projects), and

JSW Energy is a notable entrant.

Global OEMs (Cummins, Siemens, and Thyssenkrupp) are also exploring Indian market entry via partnerships. AETL will compete with these well-funded players for both project EPC contracts and equipment sales.

On electrolyzer manufacturing, the PLI winners form the core competitor set: Reliance, Adani, Jindal, Greenko-John Cockerill, Ohmium (an India/U.S. startup), L&T, and AETL’s own planned 300 MW/yr plant.

High production cost is the primary hurdle—today green H₂ is 2-3 times (approx. 600/kg) more expensive than grey hydrogen (approx. 200/kg). The government’s goal is to cut costs to ~$1.5/kg by 2030. This hinges on cheap renewable power and cheaper electrolyzers.

Additionally Large-scale hydrogen will require new storage, pipelines, and distribution systems, as well as substantial renewable energy buildout dedicated to electrolysis. Regulatory clarity is still evolving (e.g., standards for H₂ purity, safety codes, and open-access rules implementation). There is also offtake risk—industries need confidence in supply and pricing before switching to green H₂. The government’s proposed consumption mandates and purchase tenders aim to mitigate this, but enforcement is yet to be seen. Additionally, water availability for electrolysis in arid regions and securing suitable land and grid connectivity for H₂ projects could pose constraints. For new manufacturers like AETL, scaling up local supply chains for electrolyzer components is a challenge—many parts (stacks, membranes, catalysts) are not made in India today

Competition from global players could squeeze margins for AETL. Chinese electrolyzers are already cheaper, so Indian firms must achieve economies of scale and tech efficiency

Additional Insights: India’s refineries and fertilizer plants are expected to drive early adoption by replacing grey hydrogen (from natural gas) with green— India consumes ~6-7 MMT of hydrogen annually for refining and fertilizer feedstock, a substantial latent demand to tap. Several public sector units (IOC, NTPC, GAIL) have pilot projects blending hydrogen into natural gas grids and running hydrogen buses. These pilots, alongside steel trials (e.g., hydrogen-based DRI in steelmaking), will prove use cases by mid-decade. Global developments are also favorable—countries like Japan, South Korea, and the EU have large hydrogen import needs (the EU plans to import 10 MMT by 2030), which Indian producers could supply if costs fall. This export angle is explicitly part of India’s strategy to be a “global hub” for green hydrogen and its derivatives (like green ammonia).

- Fuel Cell Manufacturing (Chicken-and-egg problem): One of the verticals where I am not sure how things will play out, as we are still in the nascent stage of growth in EVs, and in just the next 5 years again be changing from lithium to hydrogen fuel cells. I don’t know, honestly.

Fuel cells remain far more expensive than incumbent diesel engines or even battery systems and infrastructure. Scaling FCEVs will require a network of hydrogen fueling stations or on-site hydrogen supply for captive fleets. Competition from battery-electric vehicles (BEVs) is a strategic challenge

However, a study by Arthur D. Little projects that around 12,000 fuel-cell heavy-duty trucks could be on Indian roads by 2030. One forecast estimates the Indian hydrogen fuel cell vehicle market to reach about $4.7 billion by 2030, growing ~25% CAGR from the mid-2020s.

Notably, the Production-Linked Incentive (PLI) scheme for the auto sector (₹25,938 crore “PLI-Auto”) explicitly encourages advanced technology vehicles, including hydrogen FCEVs. In 2023, the government approved five companies under PLI-Auto to manufacture hydrogen fuel cell vehicles: Tata Motors, Ashok Leyland, Eicher Motors, Pinnacle Mobility, and Booma Innovative. The FAME-II scheme (focused on EVs) does not cover fuel cells, but future revisions may include e-buses with fuel cells as zero-emission vehicles.

Most competitors are in the form of partnerships or pilots.

Tata showcased India’s first fuel-cell truck prototype in 2023 (in collaboration with Cummins)

Ashok Leyland is developing fuel-cell buses/trucks with backing from Reliance Industries.

RIL has a partnership with Plug Power for the Indian market.

Adani Group has partnered with Ballard Power (Canada) to evaluate fuel cells for mining trucks and locomotives in India.

- Battery Energy Storage Systems (BESS): As of Dec 2024, India had only 110 MW / 0.11 GW of installed BESS. India would require ~47 GW/236 GWh of battery storage by 2030

Projections suggest India’s energy storage market (including batteries for grid, commercial, and EV applications) could reach tens of billions of USD by 2030. For example, India is targeting ~70 GW of cumulative BESS by 2030 (government estimate), which implies a market needing ₹14 lakh crore ($170+ billion) investment in storage by then.

Introduction of a Storage Obligation as part of Renewable Purchase Obligations—starting 2023, India set targets for DISCOMs to procure a certain percentage of their renewable consumption from renewables paired with storage

GST on batteries* has been reduced to 5% when sold with renewable systems, and customs duties on battery cells are being calibrated to encourage local assembly.

The BESS ecosystem involves battery manufacturers, system integrators, and project developers. On the grid-scale project side, many renewable IPPs are entering storage. For example, JSW Energy and Reliance won SECI’s first 1 GWh BESS auction in 2022 (500 MW/1000 MWh each) with record-low tariffs.

Fluence (a global storage integrator) has a JV with ReNew Power and executed India’s first 10 MW grid BESS in Delhi.

L&T is leveraging its power project expertise to offer turnkey BESS solutions, and Sterling & Wilson (Shapoorji’s EPC arm) has also announced plans to execute battery projects. In the C&I (commercial & industrial) storage segment, startups like ION Energy, SunSource Energy (now EDEN), and international players (like Tesla’s Powerwall or Sonnen for upscale residential) provide battery solutions, though this market is smaller relative to grid-scale. For manufacturing, Reliance (through acquisitions of Faradion (Na-ion) and Lithium Werks) and Ola Electric are likely to dominate Li-ion cell production by late-2020s, potentially supplying cells for stationary storage. Traditional battery makers Exide Industries and Amara Raja are also pivoting to lithium – Exide with an SVOLT tie-up, Amara Raja setting up a lithium cell plant – they could become key domestic suppliers for BESS projects. In summary, AETL will compete with large IPPs and global integrators for executing BESS projects, while relying on an emerging network of cell/module suppliers largely controlled by big players.

Risks & Execution Challenges: Despite a positive outlook, deploying BESS at scale in India carries challenges. The foremost issue is economics – battery storage is still expensive (current costs ~$250/kWh for grid-scale Li-ion systems installed). Even with falling battery prices (BNEF projects ~$100/kWh by 2030), the viability of projects depends on monetizing multiple value streams (peak power sales, frequency regulation, arbitrage). Regulatory models for energy storage remuneration are still developing – e.g. how DISCOMs contract storage or how storage can access spot markets. Policy uncertainty (e.g. possible changes in market rules, or delays in storage obligation enforcement) can affect investor confidence. Financing large BESS projects is also a hurdle, as banks have limited experience with the asset class and worry about technology and price risk. Another risk is technology and supply chain dependence: India currently imports almost all lithium cells – any global supply crunch (as seen during COVID or due to geopolitical issues) could raise prices or delay projects. Building local manufacturing (via PLI) will take time, and new tech like sodium-ion or advanced chemistries are unproven at scale. From an operational view, safety concerns like battery fires or thermal runaway are crucial – a well-publicized fire could set back public and regulatory acceptance. Projects must implement stringent safety standards (fire suppression, battery management systems) to mitigate this. Execution-wise, integrating batteries with the grid requires new technical capabilities for grid operators (managing charging/discharging, software integration for dispatch), so system operators need training and upgrades. At the project level, EPC players face a learning curve in handling battery systems (cooling, power electronics, software)—skilled manpower is in short supply. AETL and peers will need to acquire technical know-how quickly, possibly via partnerships. Finally, competition from alternative storage exists: India has a strong pipeline of pumped hydro storage (PHS) projects (the government is reviving dozens of GW of PHS), which can deliver bulk storage at lower per-kWh cost for long durations. If PHS projects come online faster, they might reduce the immediate need for very large BESS for bulk energy shifting, confining batteries to shorter-duration and ancillary services roles. Managing these risks will be key to scaling BESS deployments.

5 Likes

Do you have any more links of detailed articles on BESS ( India Scenario). i will study. Thanks

2 Likes

The investor whale Vijay Kedia bought stake as bulk deal. One of the factor which made this stock rallied this week.

2 Likes

actually can’t find any reason other than this Kedia factor for this sudden rally

Concall Analysis of Q4FY25:

Business Update:

1. Robust Top & Bottom Line Growth

• Standalone Revenue: ₹295 Cr (↑ 42% YoY; 3 year CAGR 60%)

• Consolidated Revenue: ₹399 Cr (↑ 90% YoY)

• Standalone EBITDA: ₹47 Cr (↑ 35% YoY), margin 15.9%

• Consolidated EBITDA: ₹45 Cr (↑ 252% YoY), margin 11.3%

• Standalone PAT: ₹31 Cr (↑ 48% YoY), margin 10.7%

• Consolidated PAT: ₹36 Cr (↑ 565% YoY), margin 9.0%

2. Segment Wise Performance

• Power Transmission Solutions (PTS):

o FY25 Revenue ₹295 Cr (→ 74% of total standalone)

o Key verticals: OPGW, RDSS EPC, stringing tools, reconductoring (HTLS), ERS, ACS wires

• New & Renewable Energy (NRE):

o FY25 Revenue ₹102 Cr (→ 26% of total standalone)

o Activities: Solar EPC (94%), GH₂ EPC (5.7%), carbon services

AGPL Carbon Market:

FY25 Key Milestones:

3. Order Book & Backlog

• Total Unexecuted Orders: ~₹800 Cr (as of May 2025)

PTS: 66% (~₹530 Cr) to be executed within 9 months

NRE: 34% (~₹270 Cr) to be executed within 12 months

4.. Profitability & Returns

• RoCE: 15.8% (Standalone) | 17.2% (Consolidated)

• RoE: 20.9% (Standalone) | 28.7% (Consolidated)

5. Strategic & Operational Wins

• Scaled OPGW manufacturing and executed 1,000 km live line stringing in a single month

• Entered RDSS EPC for DISCOMs; secured ~₹100 Cr in distribution projects

• Launched MAKE IN INDIA ERS, supplying to Powergrid

• Awarded 100 MW Solar EPC (Khavda, Gujarat); 30 MW commissioned

• Secured 50 MW / 100 MWh BESS annuity project (GUVNL)

• Completed 300 kW GH₂ microgrid (THDCIL) and progressing 1 MW + 15 MW GH₂ EPC

Management guidance about future business parameters/future strategy/CAPEX etc.

PTS: Strong power‑transmission capex (2.44 trn INR by 2030); niche import‑sub factories

NRE: Leverage PLI wins (300 MW electrolyzer); fuel‑cell JV; 1 GW BESS pipeline over the period of next 5 years

Carbon Services: 1.4 mn credits onboarded; targeting 8 mn+ by 2030

Guidance: 50% CAGR (top & bottom line) over next 3 years; maintain 15–17% EBITDA margins

2 Likes

There are some red flags for me, exited all my positions today. I’ve put up the below mail to the company w.r.t concerns as there were no investor call for last quarter (thiis too is red signal)

3 Likes

where did you find the call transcripts / audio recording. Couldn’t find in their website / BSE.