A detailed business analysis with pros, cons & industry analysis is hereby upoloaded. If you find it useful, please like my post. Thanks

- Company Overview:

•`

• The clients of the co. are in Central and States Transmission Companies, major EPC companies of India and Overseas, Private Power/Transmission Utilities

• Timeline of Journey: About Us - Advait Group | Leading Transmission and Green Energy Company (VVI)

• 14+ years of business, 60+ customers, 300+ total projects served.

• As of the end of FY 2022-23, the total number of the employees of Company is 55

- Business Verticals:

• Manufactured Products: Aluminium Clad Steel Wires, Emergency Restoration System, Stringing tools, OPGW and Optical Fibre Cables.

• Traded products: Insulators, Earthing Solutions, Towers, Bird Diverters, GIS substation, Carbon Core Conductors.

• Services: Live Line OPGW Installation, trading end to end, Liaising, Marketing and Transportation, Optical Fibre and FOTE.

• The company has expanded its product portfolio by manufacturing OPGW (Optical Fibre Ground Wire) and OFC Cables.

• Revenue Mix: Sale of goods: 76% in FY21 82% in FY20, Supply of Service: 24% in FY21 vs 18% in FY20

3. Industry Analysis:

• Global Power Industry:

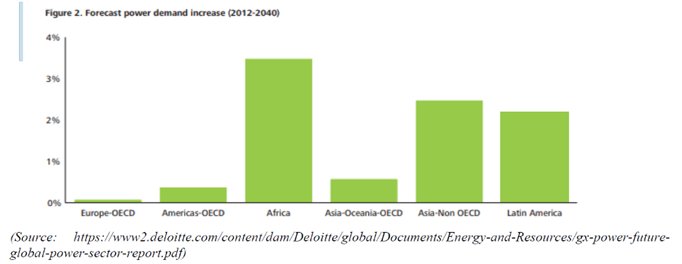

I. Global T&D Sector is expected to grow at 5.5% CAGR between 2022 to 2027.Due to higher levels of economic growth and anticipated improvements in the quality of life over the next few years, developing countries will likely see a rapid increase in power demand. India, for instance, is poised to see annual consumption increases of up to 3.2% between 2012 and 2040, while China‘s annual demand is forecast to grow by 2.1% for the same time period

• Indian Power Industry (Transmission & Distribution):

I. Power is one of the most critical components of infrastructure, crucial for the economic growth and welfare of nations. For efficient dispersal of power to deficit regions, strengthening the transmission system network and enhancing the Inter-State power transmission system network are required.

II.

III. Growth Drivers:

IV. Opportunities:

A. Strong growth in generation capacity led by per capita consumption, urbanization: There is strong growth opportunity in power generation led by exponential growth in economy, increasing propensity for electricity consumption and urbanization.

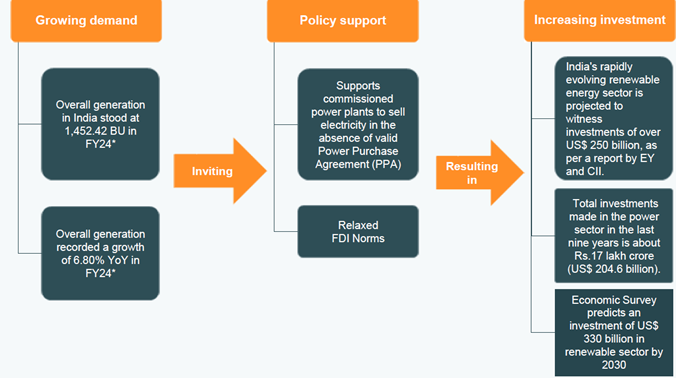

B. Alternate sources of energy: While Indian companies are largely focused on tradition sources of energy, global investments in renewable energy has jumped 32% reaching record USD 211 billion in 2010, which is over 5 fold increase since 2004. Even developing countries like China have ramped up their investments in alternate sources of energy. Steadily, India too is looking at building a strong renewable energy portfolio in coming years. Government of India is offering a number of incentives to renewable energy developers to accelerate investments in renewable energy space. RPO requirements set by state regulators and REC mechanism is expected to create demand for renewable energy across solar and non-solar sources. In addition, several benefits like accelerated depreciation, preferential tariff and generation based incentives offer attractive incentives to developers investing in renewable energy, and aim to enhance supply through renewable energy. The increased focus of Government of India towards renewable energy has created attractive opportunities for investments in this sector. The recent solar bids concluded is an indication the players are becoming increasingly competitive in the space while large scale capacity additions in wind continue across country (especially in Tamil Nadu and Rajasthan). As per the Central Electricity Authority (CEA) estimates, by 2029-30,

C. the share of renewable energy generation would increase from 18% to 44%, while that of thermal is expected to reduce from 78% to 52%

D. The nation has raised its target at COP26 to achieve 500 gigawatts of non-fossil fuel-based energy by 2030

E. In India, approvals have been granted for 50 solar parks with a combined capacity of 37.49 GW. Additionally, there is a target of 30 GW for offshore wind energy by 2030, with identified potential sites.

V. Challenges in power sector:

Social reasons like opposition from nearby residents due to concerns over loss of land, water and pollution;

Resettlement and rehabilitation issues;

Regulatory delays;

Environmental issues like afforestation;

State specific issues like unavailability of supporting infrastructure;

Financial reasons resulting from rising costs of land

Other issues:

• Telecom Sector

I. Indian Telecom Sector is forecasted to grow by 9% CAGR during the period of 2022-2028. The telecom sector is expanding dur to the surge in demand for 5G technology and internet consumption. This shall help the growth of the companies which are into the manufacturing, laying and installation of the Fibers, Optical Fiber Cables (OFC), Optical Fibre Ground Wires (OPGW) and Telecommunication Equipment’s.

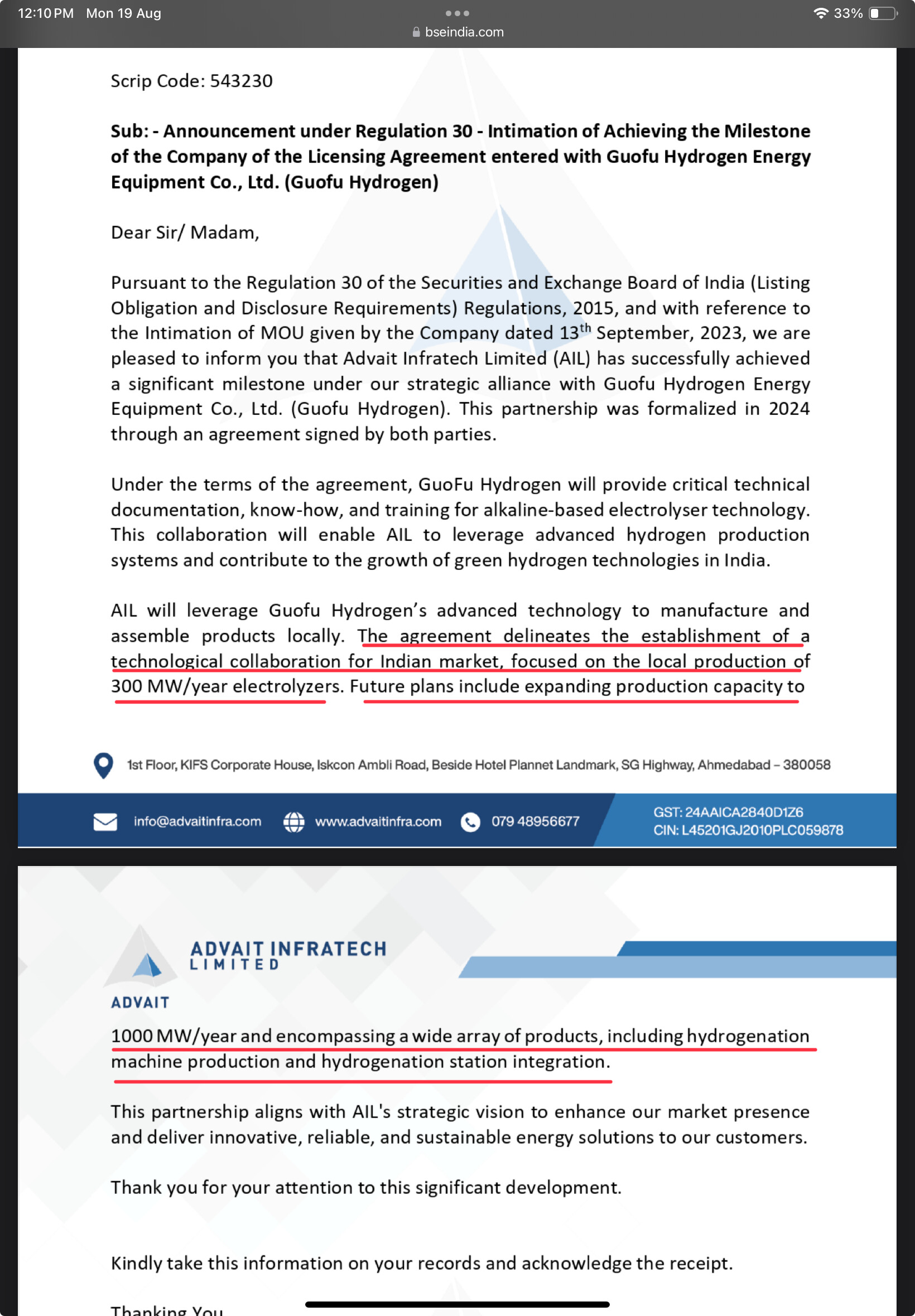

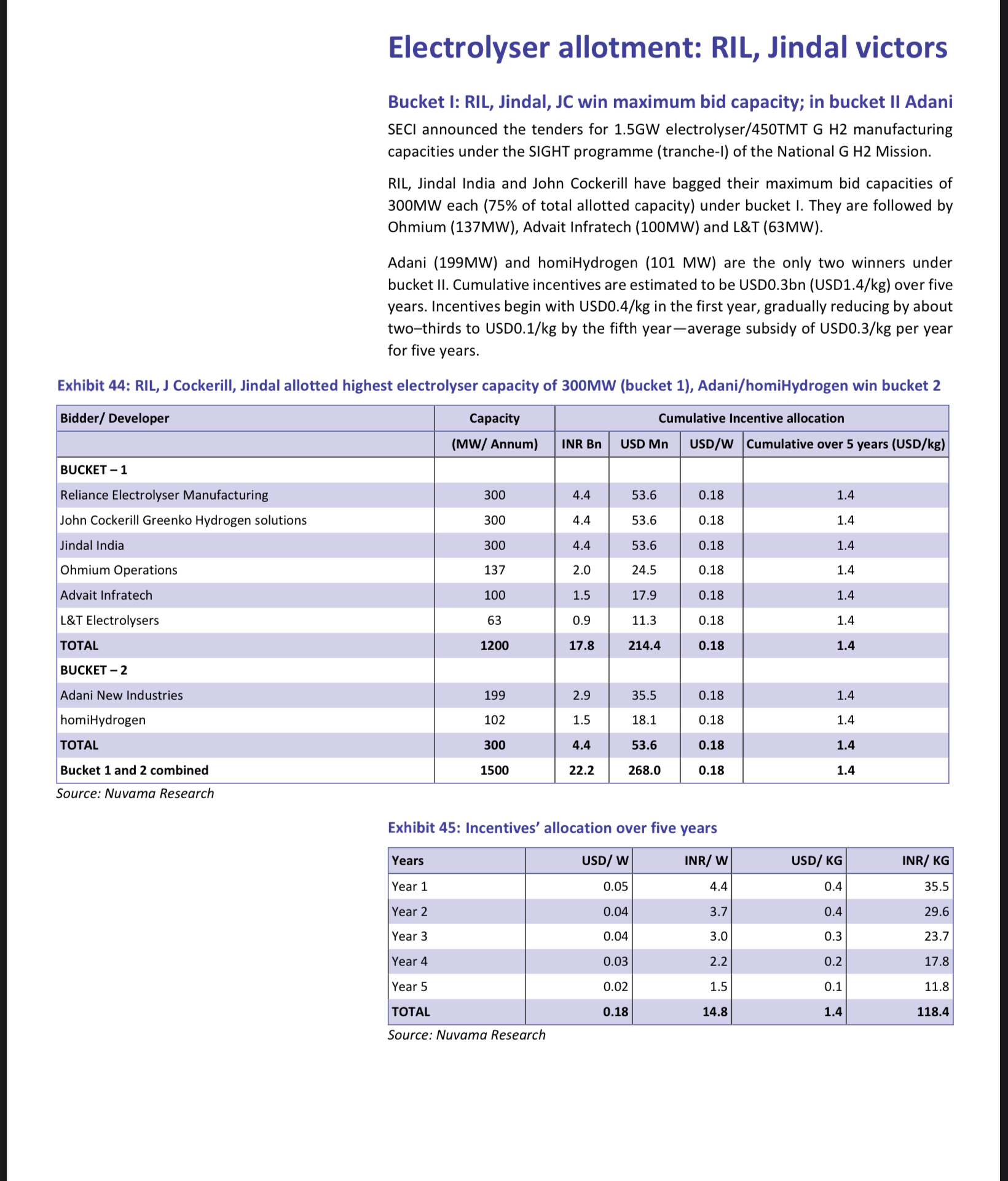

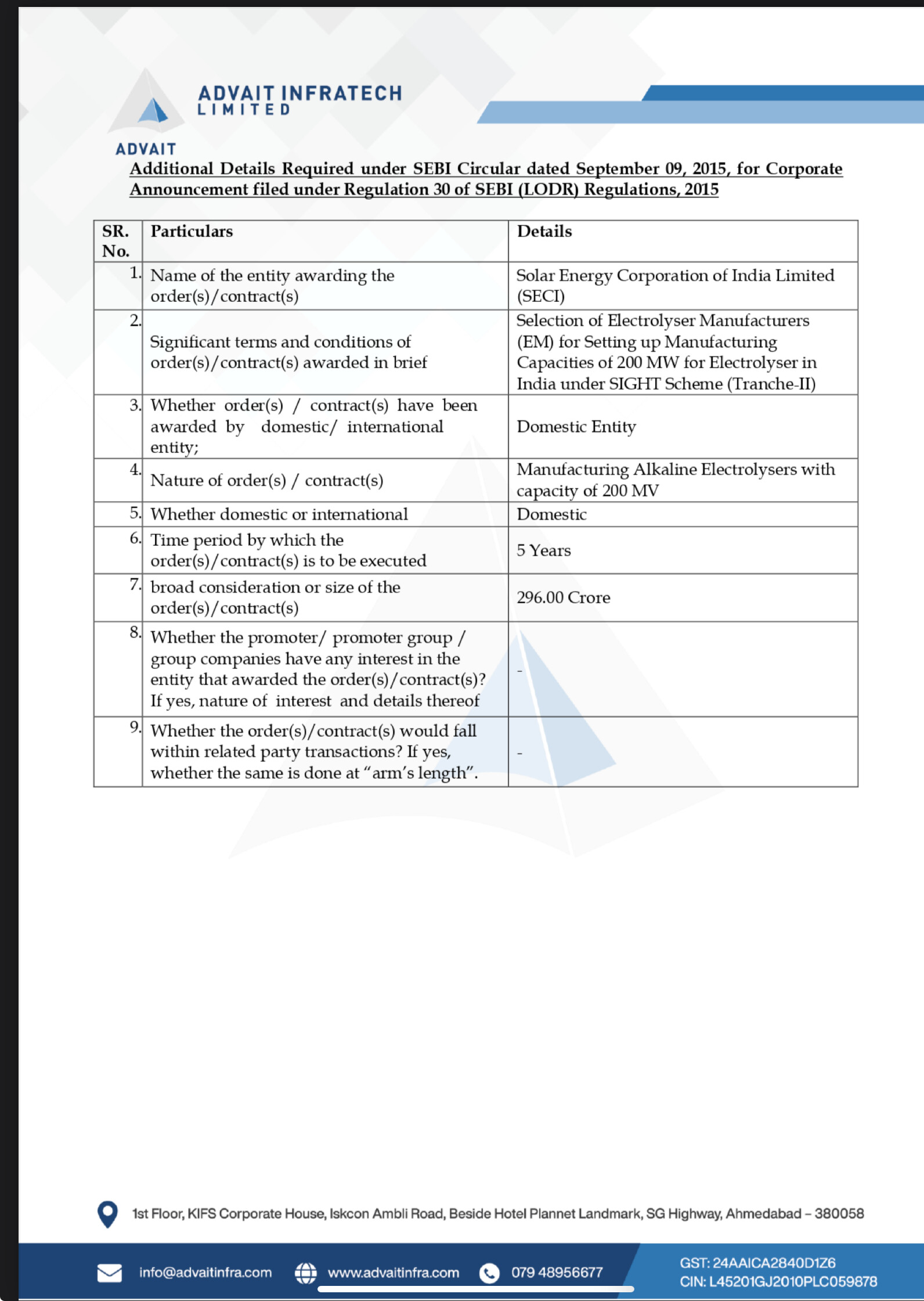

• Green Hydrogen Sector:

I. The global green hydrogen market is valued at USD 242.7 billion in 2023 and is expected to reach USD 410.6 billion by 2030; it is expected to record a CAGR of 7.8% during the forecast period. Morgan Stanley estimates that the total addressable market for hydrogen in India could reach USD 19 billion. Advait has ventured into Green Hydrogen with a vision to provide end-to-end infrastructure for GH2 production. Your company is soon going to have its own Electrolyser manufacturing units along with the Fuel cell Assembly facility. The increasing focus on GH2 is a consequence of increasing government focus on developing hydrogen-based economies and investment in the hydrogen infrastructure.

4. Management Analysis:

• Shalin Seth: aged 46 years, is the Promoter and Managing Director of our Company. He holds Bachelor’s Degree in Mechanical Engineering from BVM College, Sardar Patel University, Gujarat. He had done PGDMA from Ahemdabad Management Association. Post qualification, he had worked with Kalpataru Power Transmission Ltd. and Adani Power Limited. He has experience of more than a decade in electricity transmission and distribution industry. His functional responsibility in our Company involves handling the overall business affairs of the Company including planning business marketing strategies, capacity expansion, and overall development of the business of our Company.

• Rajal Seth (Wife of Shalin): She holds Bachelor’s Degree in Commerce from NM college of Commerce and Economics, University of Mumbai. She has been providing advisory services to the Company. Further, she leads the finance function of the Company.

• Dinesh Patel: Mr. Dinesh Patel, aged 61 years, is a Non Executive Director. He holds degree of B.E Mechancial from L.D College of Engineering (Gujarat University). Post qualification, he has worked with companies such as Kalpataru Power Transmission Ltd etc. He has experience of several years in the field of Power and Transmission.

• Bajrangprasad Maheshwari: He holds degree of Bachelor in Commerce from M.L.S University, Udaipur Rajasthan. He is an Associate member of ICAI and ICSI. He holds Diploma in Business Finance from the Institute of Chartered Financial Analysts of India. Post qualification, he has worked with companies such as Biotech International Limited, Kalpataru Power Transmission Ltd etc. Currently he is working with SK Fincap Advisors Private Limted as an Executive Manager. He has experience of several years in the field of Accounts and Finance. His areas of expertise include Treasury & Risk Management, Team building & performance improvement, Negotiations & Strategic Alliances etc

5. Financial Analysis:

• Available in screener

6. SWOT Analysis:

• Strength:

I. Existing Client Base: Company is providing products and solutions to major power utilities in India and abroad, and to all Main EPC actively working in this field. We have successfully retained clients from both private and public sector. the quality of our products and services is demonstrated by the fact that all of these customers have given us repeat orders.

II. Selective bidding with a focus on effective execution record: We have developed an experienced bidding team, and execution team and conduct extensive due diligence on project-specific, client-specific and country-specific risks and uncertainties. We endeavor to factor such risks and uncertainties into our bids and contracts to manage and allocate risks and uncertainties in a manner that reduces our financial exposure.

III. Strong Order Book and Financial Position

IV. Our business is not seasonable in nature

• Weakness: Very high valuation, High debtors day, high inventory & trade receivables + Other points as mentioned under the Heading “Risk and challenges”

• Opportunity & threat:

7. Valuation:

• Presently trading at very high valuation (@P/E of 87 against median p/E of 15.7)

8. Risks and Challenges:

• Regulatory risk, change of favorable govt policy, liability of compliance regarding to environmental laws

• Trade tension with China may adversely affect company’s business

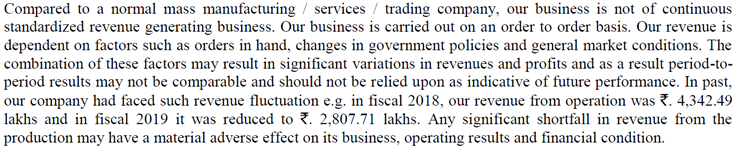

• Fluctuating revenue & profitability

• Company trademark logo and design developed by R&D are not registered due to requirements of maintaining confidentiality of intellectual property.

• Trade Receivables and Inventories form a substantial part of current assets and net worth.

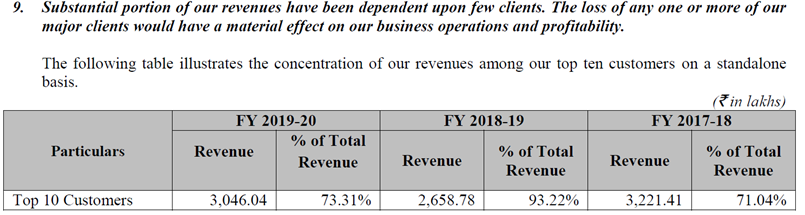

• High revenue concentration

• Group company TG Advait has incurred loss in previous years.

9. Investment Thesis:

• All the points mentioned earlier in strength and opportunities

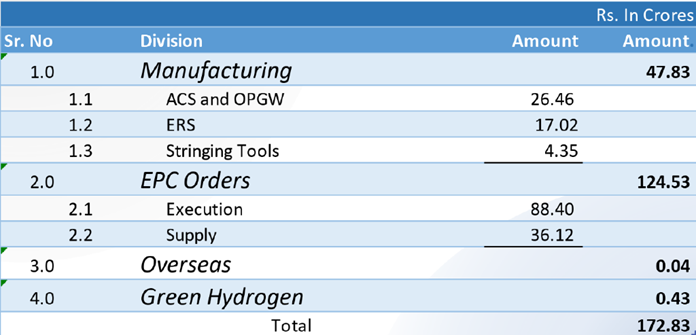

• Q3FY24 orders in hand: Rs. 172.83 cr

• Future strategy: Advait recognizes the urgency to address carbon emissions and offers a range of carbon credit consultancy services, as well as end to end carbon neutrality and net zero solutions. We also plan to develop cleantech tools

10. Conclusion: Advait Infratech Limited presents a strong investment case with its diversified business model, robust product portfolio, and strategic joint ventures. The company’s growth potential in the power and telecommunication sectors, combined with effective risk management, makes it an attractive investment opportunity. However, investors should remain aware of the inherent risks and closely monitor regulatory developments and market conditions.

type or paste code here