Thanks for sharing, but I fail to understand how is this profitable?

Net cost is 25k. So how is this profitable? You have considered profit of just 50$ /mw.

Thanks for sharing, but I fail to understand how is this profitable?

Net cost is 25k. So how is this profitable? You have considered profit of just 50$ /mw.

Please kindly review if this is possible.

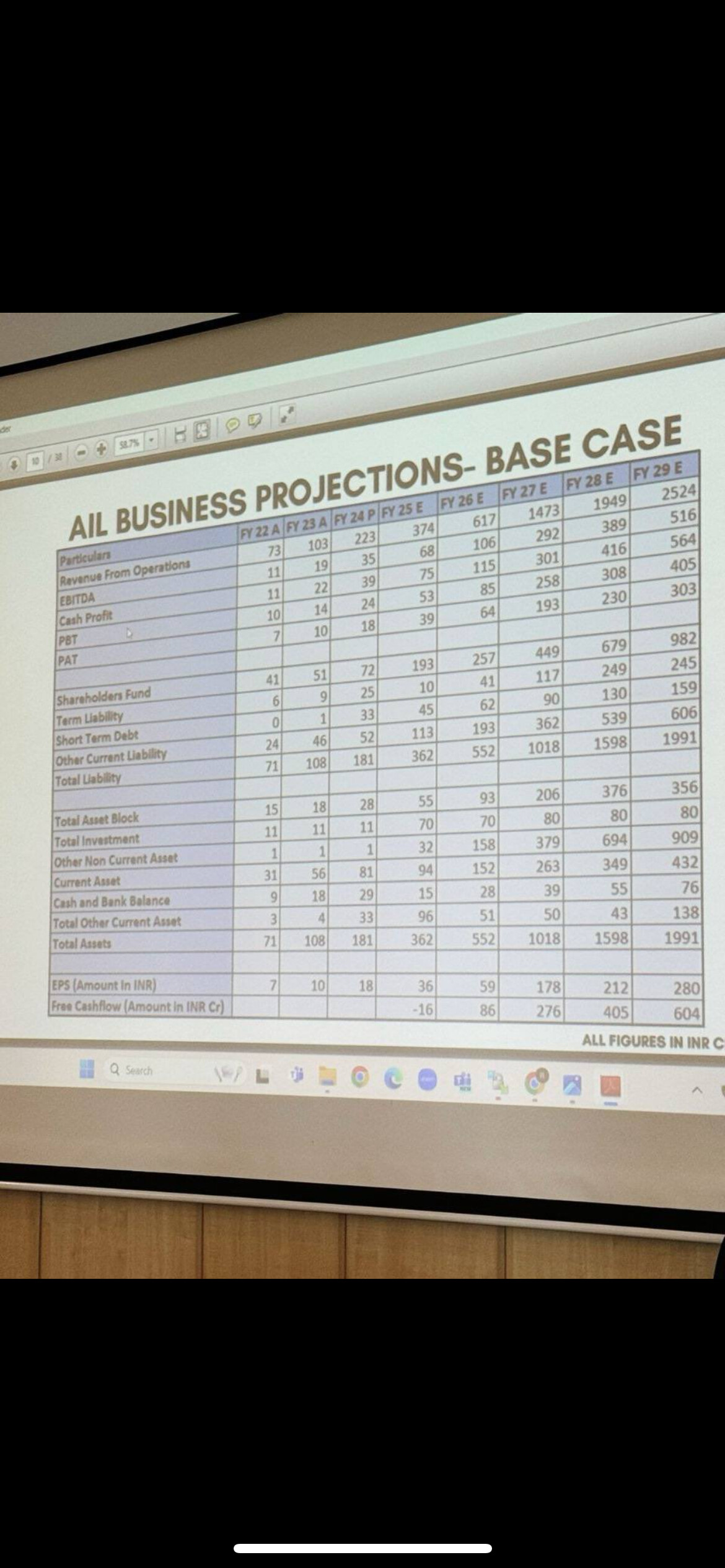

Got at some presentation by AIL to HNi’s and some institutions

Does anyone know the reason for QoQ decline in revenues for Q4FY24 and Q1FY25, essentially stagnating now?

Most of such heavy engineering and defense have higher revenues in H2. So could be why

Hi @Midhunjoe

Poor set of numbers from Advait

When can they possible add GH2 numbers to their topline?

Any idea regarding this

Correct me if I’m wrong, but from their alpha sme stars pitch, green hydrogen would start after a few years … 2026-2027 iirc. In the mean time ERS, optical cables and other electrical will be main. They are also adding new products in the electrical side. Also given the their subsidiaries are just starting out, wouldnt it be prudent to look at standalone numbers only. This is better YoY. Not by much but still up (11.8%)

I think revenues from GH2 is still some time away. They have so far executed a pilot project only and rest I believe is in testing phase. As mentioned in the previous post by @Aloysius_De_Sa the standalone numbers looks better although not great.

But what is worrying for me is the lack of communication from the management in terms of ppt , calls etc after a subdued set. Shows the lack of character….

P.S : Invested

Although I do agree that it is about time that Advait and for that matter many other >1000 Cr mcap companies to start doing concalls, I do not take it as a red flag as they never did concalls earlier too. It would be worrying if they used to do earlier and didn’t do this quarter which could mean they have something to hide. For that matter you could check the link for the latest facts and guidance from the promoters. https://youtu.be/WekO_KeNCAk?si=mLfL0BTDpsOGA5h-.

Edit - I see that Advait has always released a ppt after results at least in the recent past. I hope they continue. Else maybe they have taken the October ppt from the webinar for this quarter. I hope it is not the case

They have heard it.

Talk about timing! Who knew Mr.Shalin and team is active on Valuepickr ![]() . Very happy with the update

. Very happy with the update

Have they deleted the tweet ?

Yeah .

I’m going to attend the conference on Dec 3

Kindly put up your questions.

If any

Thanks

Hi,

Please ask about the progress on the renewable energy business side, specifically about how the electrolyser manufacturing and fuel cell assembly businesses are coming along. When are the revenues expected to come in and how they’ll scale up. Doubt there was anything in the Q gone by but good to check nonetheless if you can as I think they have a plant in Gujarat operational.

Thanks!

Yeah, one from my side. So the electrolyzer business is a good 3-4 years away, so where do they see immediate revenues coming from? We do not want a stagnation with just hopes of future revenues. So kindly talk about the EMS, their new electrical systems and also about their recent BESS products on timeline of execution and maybe on their total orderbook and pipeline estimation.

Hope to have your feedback post the meeting.

I wasnt allowed there.

Only nuvama research analyst were allowed

no concall pdf avalaible in public forum. do you have it?

Any update post the TECO 2030 bankruptcy with whom Advait had a partnership. Looks worrying as they had invested around 40 crores as well which is potentially all gone to waste.

A good detail analysis link found on internet : Advait Energy Transitions Ltd: Fundamental Analysis - Dr Vijay Malik