About the company

Ador Welding Limited (AWL) is the second largest player in welding consumable and equipment market in India behind Esab India. The company was incorporated in 1951 as Advani Oerlikon as JV between Advani group. During 2002-03, Advani group acquired shareholding of the Oerlikon group and became a majority shareholder in the company.

Industry

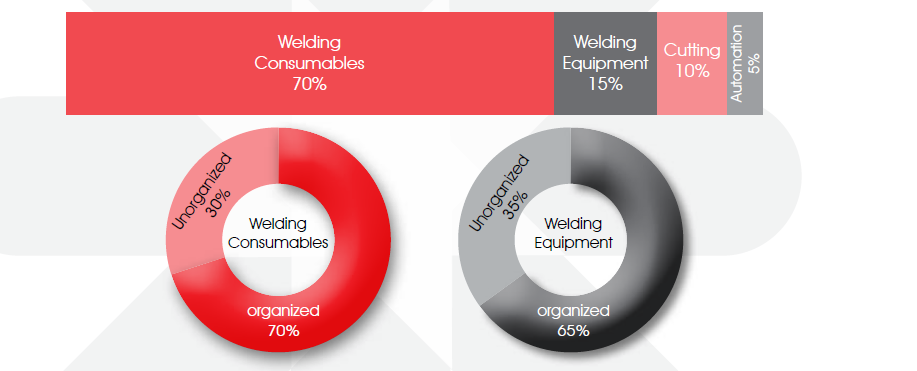

Welding industry is estimated at Rs.5,100 crore (source: Ador Welding AR - FY22) and is structured in following way:

(source: Ador Welding AR FY22)

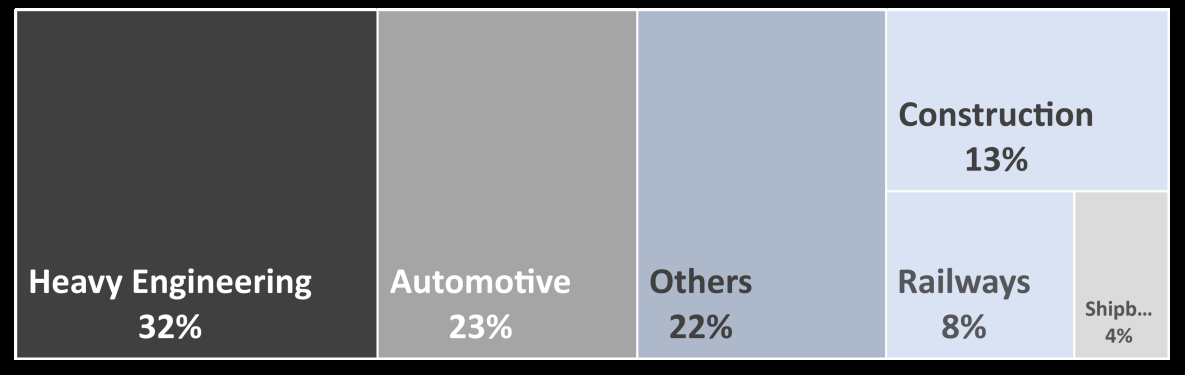

There has been increasing focus of government of India to increase the share of manufacturing in overall GDP to around 28 - 29% in 2025 from 20.10% in 2022 which augurs well for the welding industry. Manufacturing, automotive and infrastructure growth are expected to spur growth in the welding industry. Major markets for welding industry are oil & gas, power, heavy engineering, shipbuilding, automotive etc. Industry wise end user break up of sales of welding industry:

(source: Ador Welding invesor presentation dated June 10, 2021)

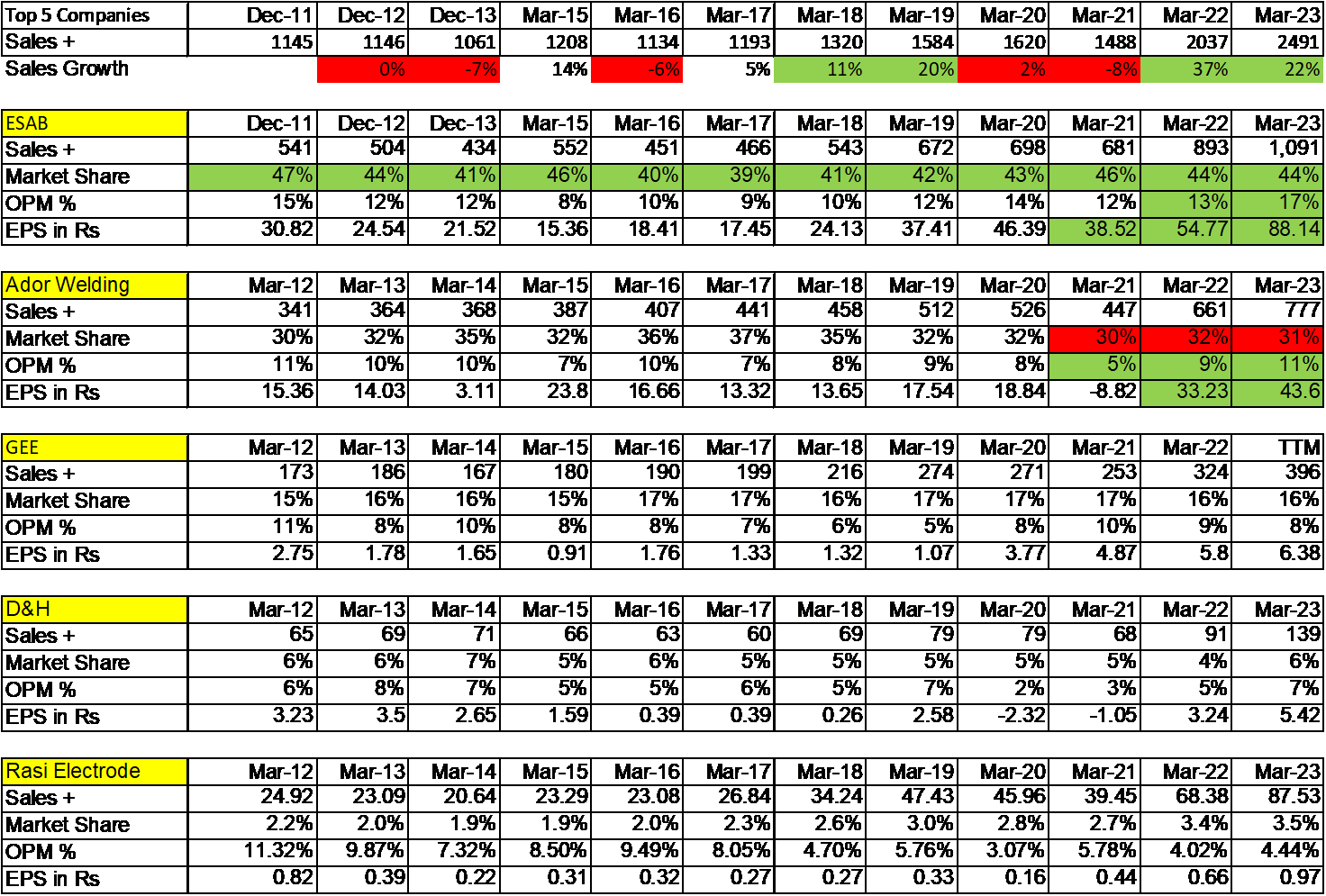

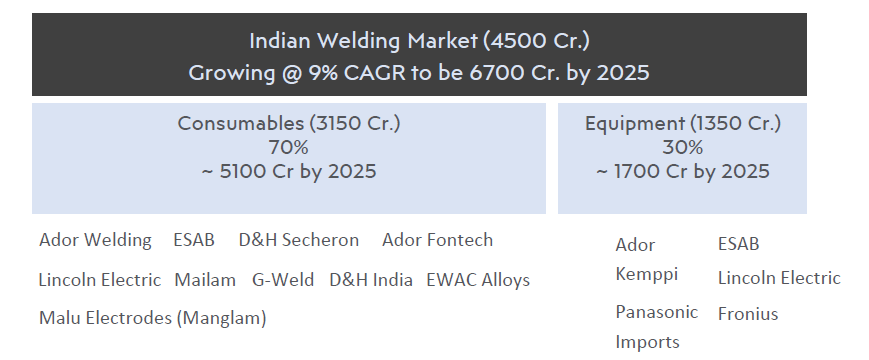

Competition

(source: source: Ador Welding invesor presentation dated June 10, 2021)

Esab India, the largest player in the Indian market, is a part of Esab group owned by Colfax corporation. Esab group is one of the largest player in the welding industry globally.

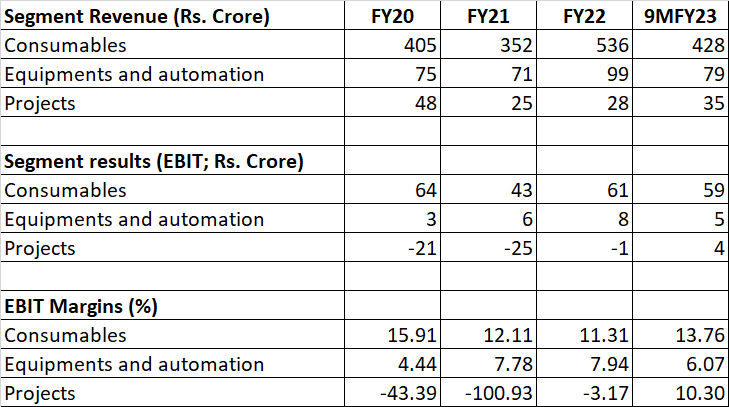

Segments - Ador Welding

The company has primarily three segments - welding consumables, welding equipment and flares & project engineering business (PEB). Prior to FY21, welding equipment and PEB business were clubbed together in a single segment. The performance of the three segments for the period FY20 - 9MFY23 is given below:

Consumables

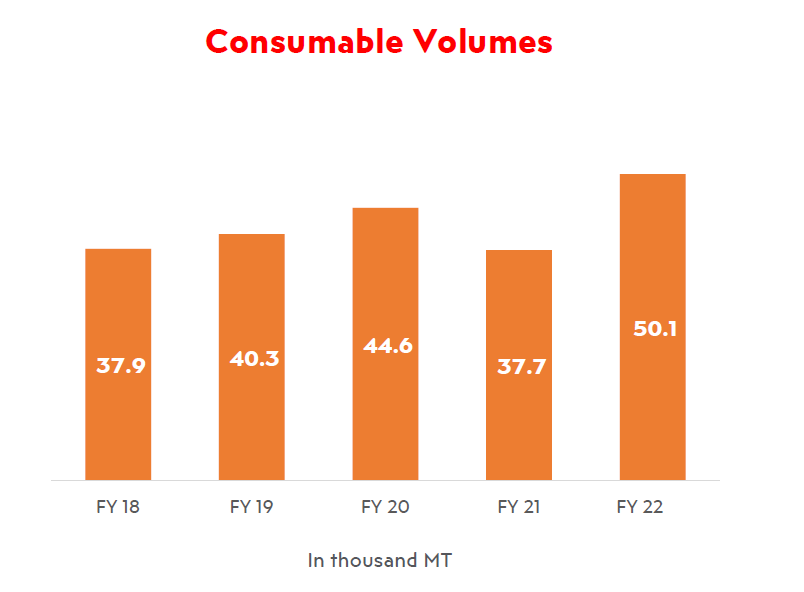

Consumables segments contributes around 75 - 80% of the total topline of the company. Consumables are sold through distributors all over the country as well as to large customers directly. The segment has had operating margins of around 15 - 16% which had declined in the post COVID due to increase in prices of steel which too time to pass on to the customer as well as time taken by new management (more on this later in the post) in understanding the dynamics of the business. The consumable volumes crossed pre covid levels in FY22. The volume for the period FY18 - FY22 is given below:

(Source: Ador Welding PPT dated June 7, 2022)

Equipment

Welding equipment is the second largest segment of the company with it contributing around 15% of the sales. Management claims that most of the welding equipments available in the domestic markets including of the large players in the market are imported while they manufacture most of their equipments in India. With the growth in manufacturing and uptick in capex cycle, the equipment segment’s growth is expected to pick up in the near to medium term. The equipment segment margins over the past 2 - 3 years have been mid single digits primarily due to supply chain issues for some of the raw materials which are imported. Management has aspirations that the segment can clock mid teens kind of operating margins.

Flares and project engineering business

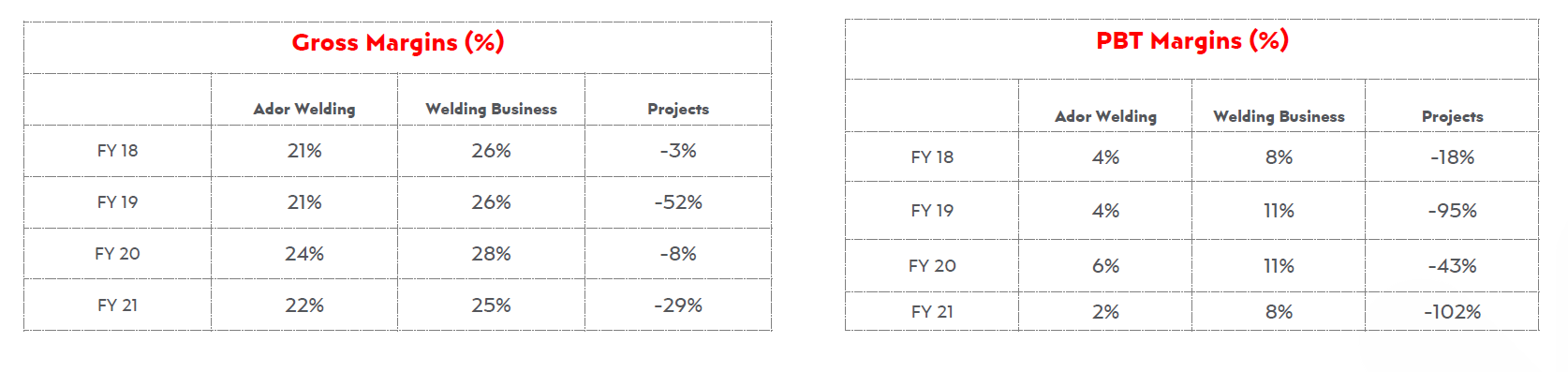

The company has been into the flare business for decades. However, the company entered EPC work for unrelated areas as well as bagged contracts in middle east for work like laying of pipelines and subcontracted it to other companies. The same led to company incurring losses in the segment during FY18 - FY22 period. The same also impacted the overall profitability of the company:

(Source: Ador Welding PPT dated June 10, 2021)

Change in management

The company was earlier run by professional management with Mr. SM Bhatt running day to day operations of the company and members of Advani family (promoters) being part of the board as non executive directors. In September, 2020, SM Bhatt, was removed as the MD of the company and one of the members of the promoter family, Aditya Malakani, replaced him and joined the company to run its day to day affairs. These was primarily done due to issues in the project engineering business incurring losses and impacting the operations of the company. Some of the measures taken by the new management to turn around the project engineering business and improve the performance of the welding business are as under:

-

Took entire write offs in the project engineering business in FY21 and focused on core business in the segment: The new management took write off of Rs.25 crore in FY21 primarily driven by write off of receivables and liquidated damages of the Kuwait project. The same led to company starting FY22 and beyond from a clean slate in the division. Furthermore, the company focused on its core expertise in the division which is primarily flares and more on engineering and designing expertise. In addition, the company hired new team to run operations of the company. Some of these new recruits include people from large MNCs. The same led to the division breaking even in FY22 (marginal loss of Rs.1 crore at PBIT level) from loss of Rs.25 crore in FY21 and turning profitable in 9MFY23 and reporting PBIT margins of around 10%. The company even won a large contract of Rs.145 crore in July, 2022 for flare stock project from ONGC. The same is expected to be largely executed in FY24. Management in concalls has indicated about healthy profitability and healthy cash flows from the project with working capital in check.

-

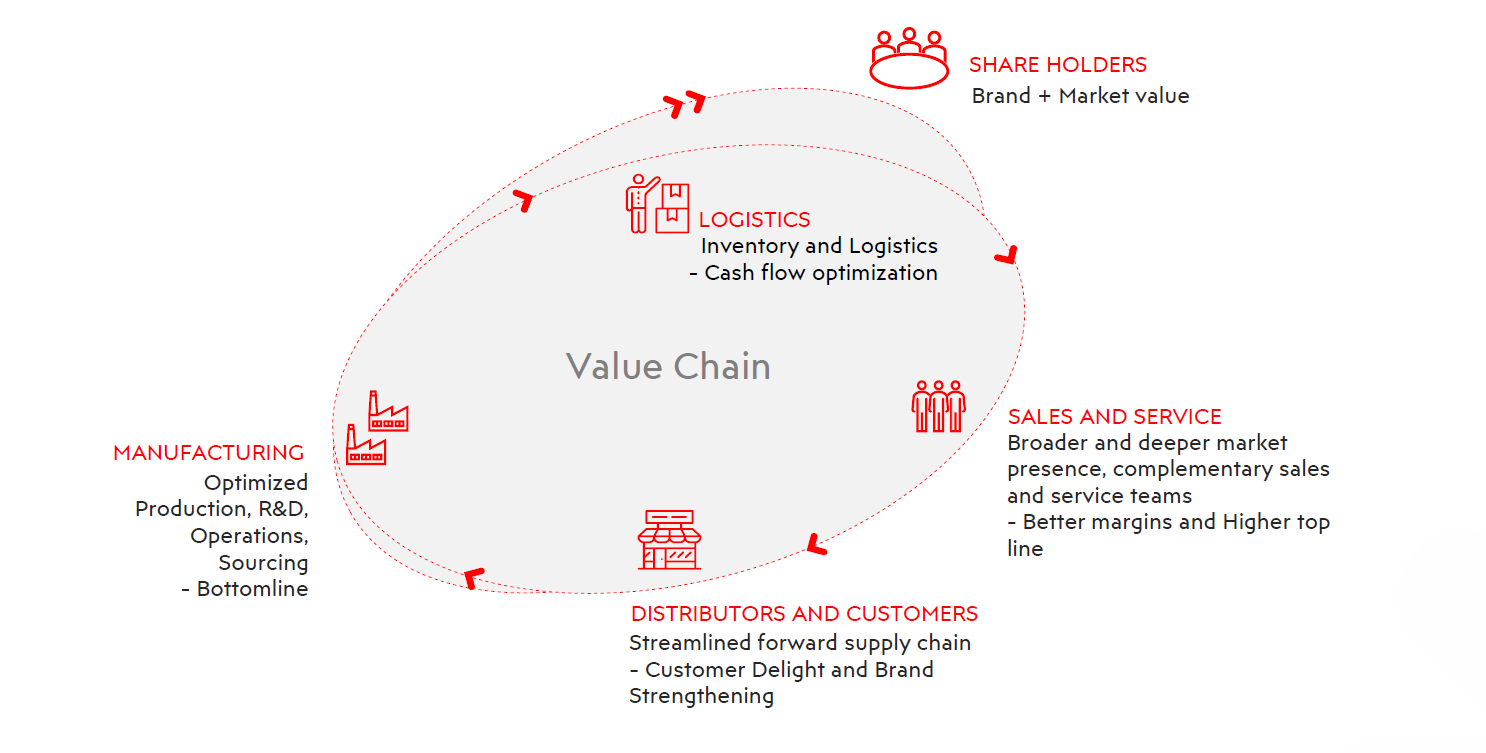

Improvement in welding business with strengthening of brand, efficient us of IT systems, improvement in distribution, reduction in logistics cost and sale of non core assets

-

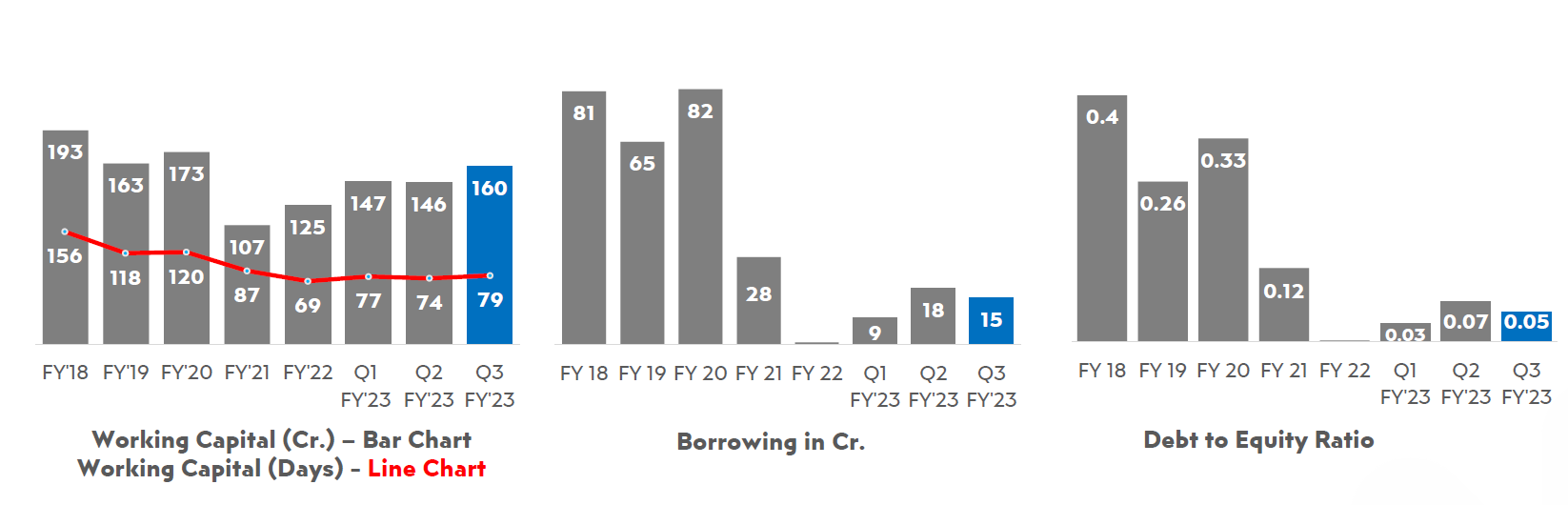

Improvement in working capital intensity of the business: The management has focused on cash flows and improved the working capital intensity of business by reducing the credit period being offered to customers. The same has led to reducing in borrowing of the company as well.

(Source: Ador Welding Q3FY23 presentation)

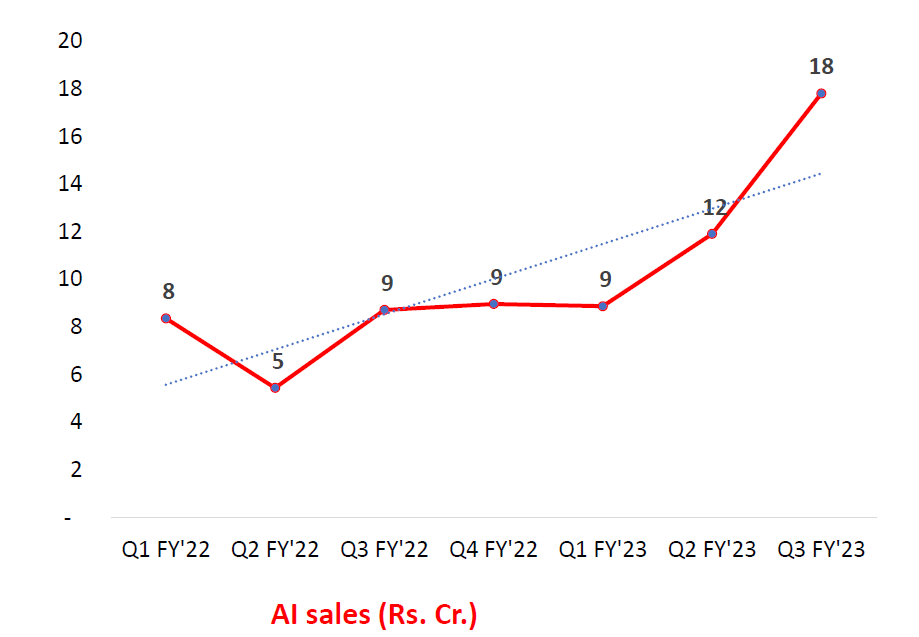

- Focus on exports for welding consumables: Management in their AGM speech and concalls has been indicating about potential of exports for cosumable business as they have a decent brand especially in the middle east markets. They had revamped the team for export markets in FY22 which has started showing some improvement in 9MFY23. Exports had long been stuck around Rs.30 crore. However, in 9MFY23, company has already done export of Rs.39 crore.

(Source: Ador Welding Q3FY23 presentation)

Merger of Ador Welding with Ador Fontech

In May 2022, the company announced merger of Ador Welding Limited (AWL) with Ador Fontech Limited (AFL). 5 equity shares of AWL having a face value of INR 10/- each fully paid up shall be issued for every 46 equity shares held in AFL having a face value of INR 2/- each fully paid up. Both the companies have Advani family as the promoter of the company. Many investors had in the past asked management about the need for having two different welding companies and requested management for merger of both the entities. AFL is primarily into repair and reclamation welding. Management expects some synergies post merger of both the companies. Some reasons highlighted for merger in Ador Welding’s presentation:

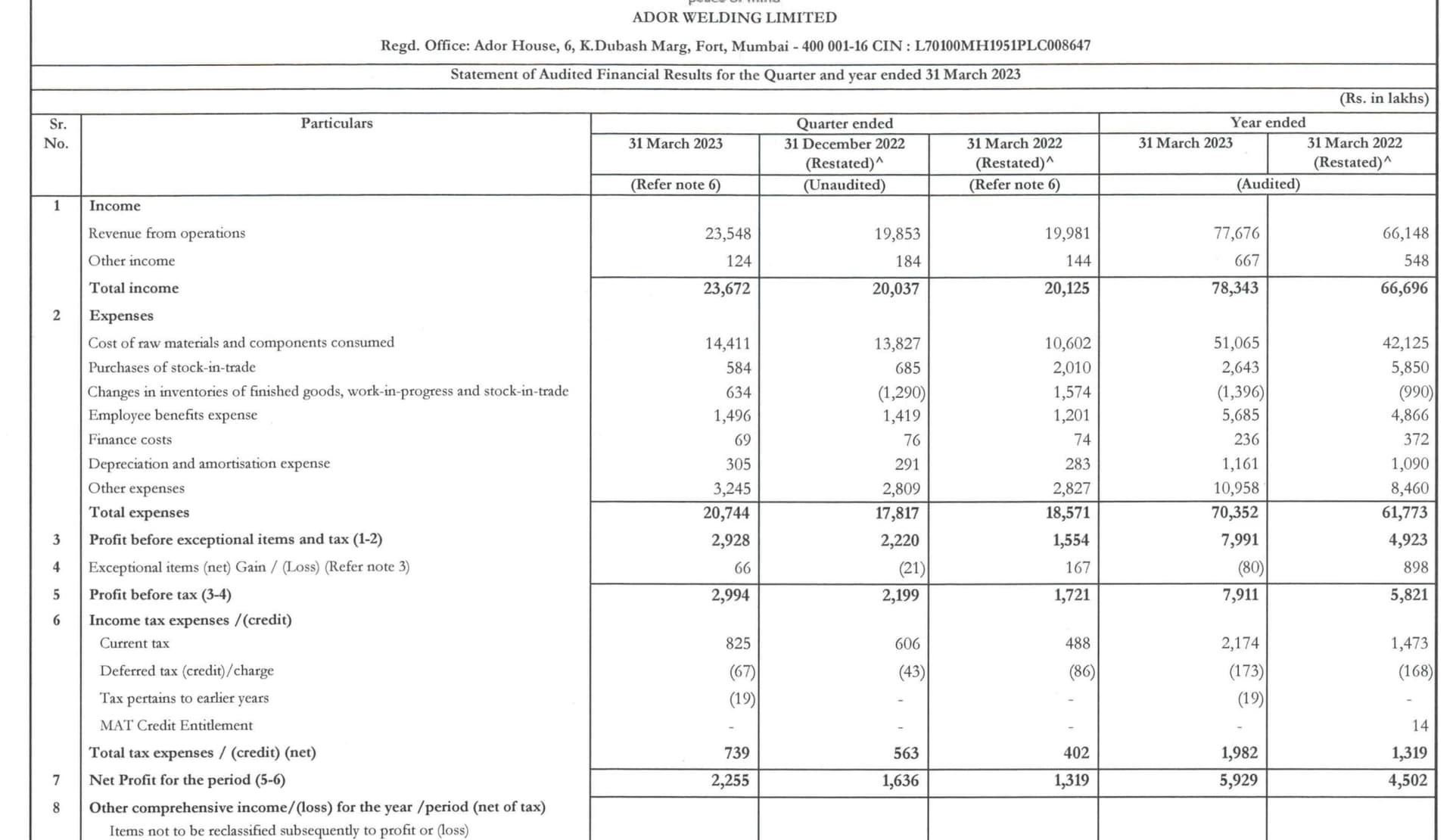

Financials:

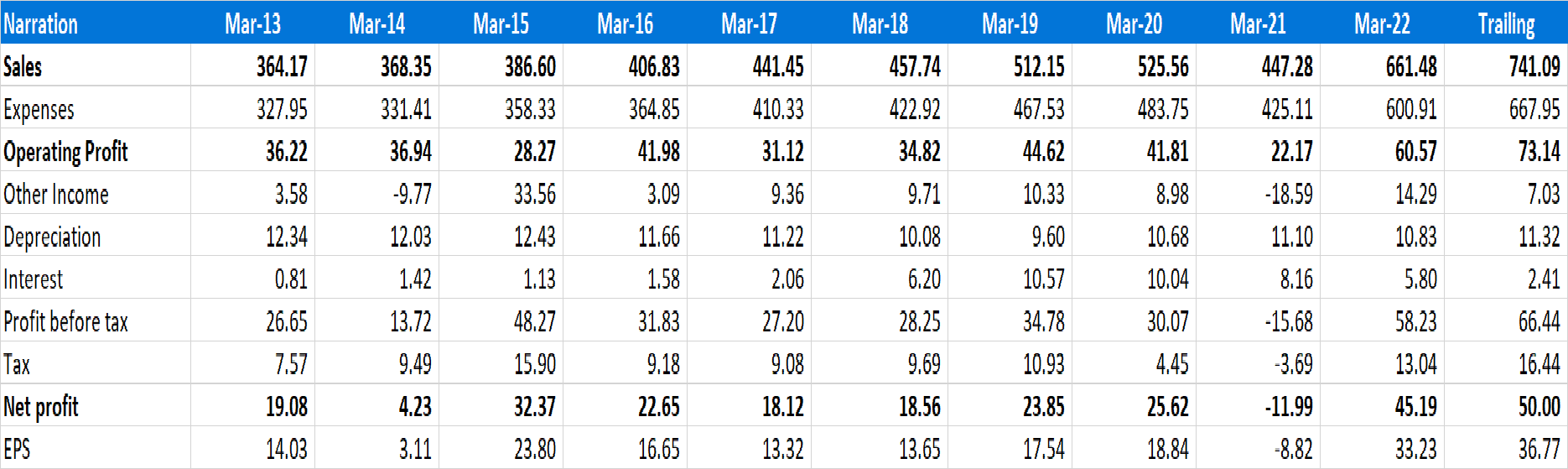

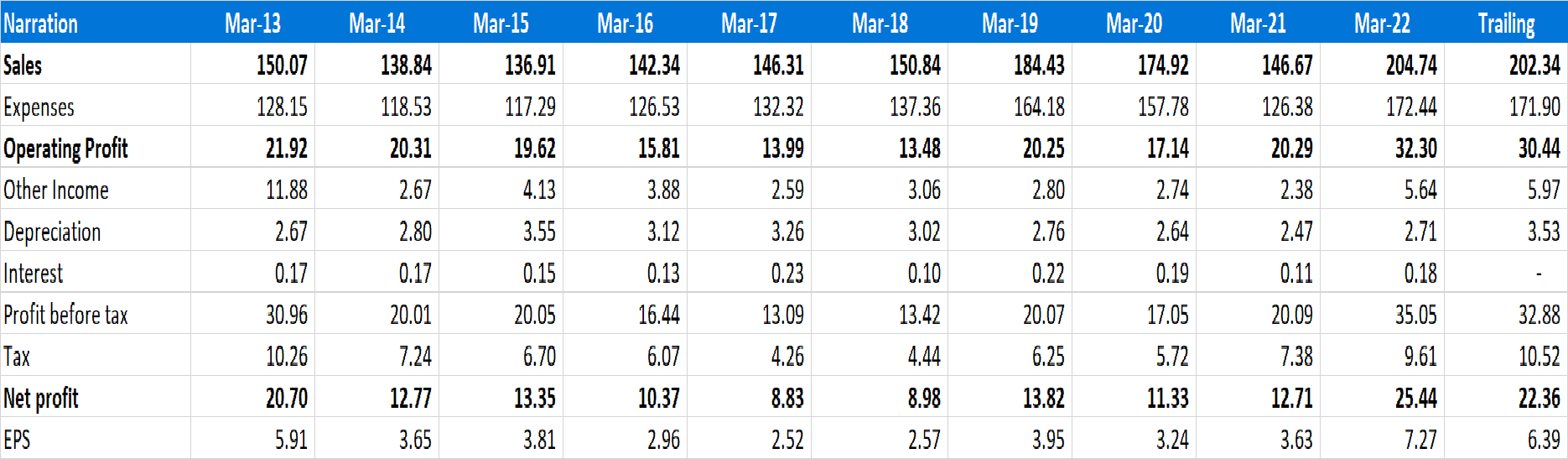

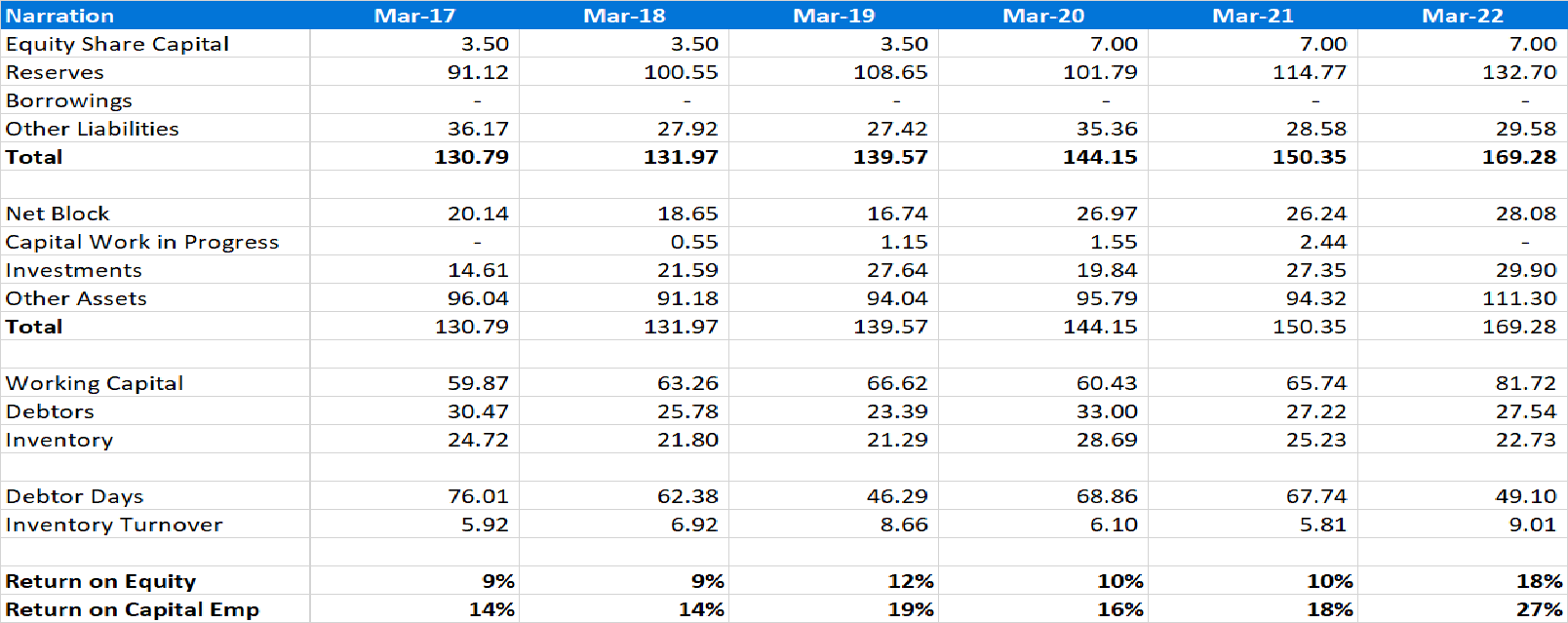

Ador Welding Limited

P&L

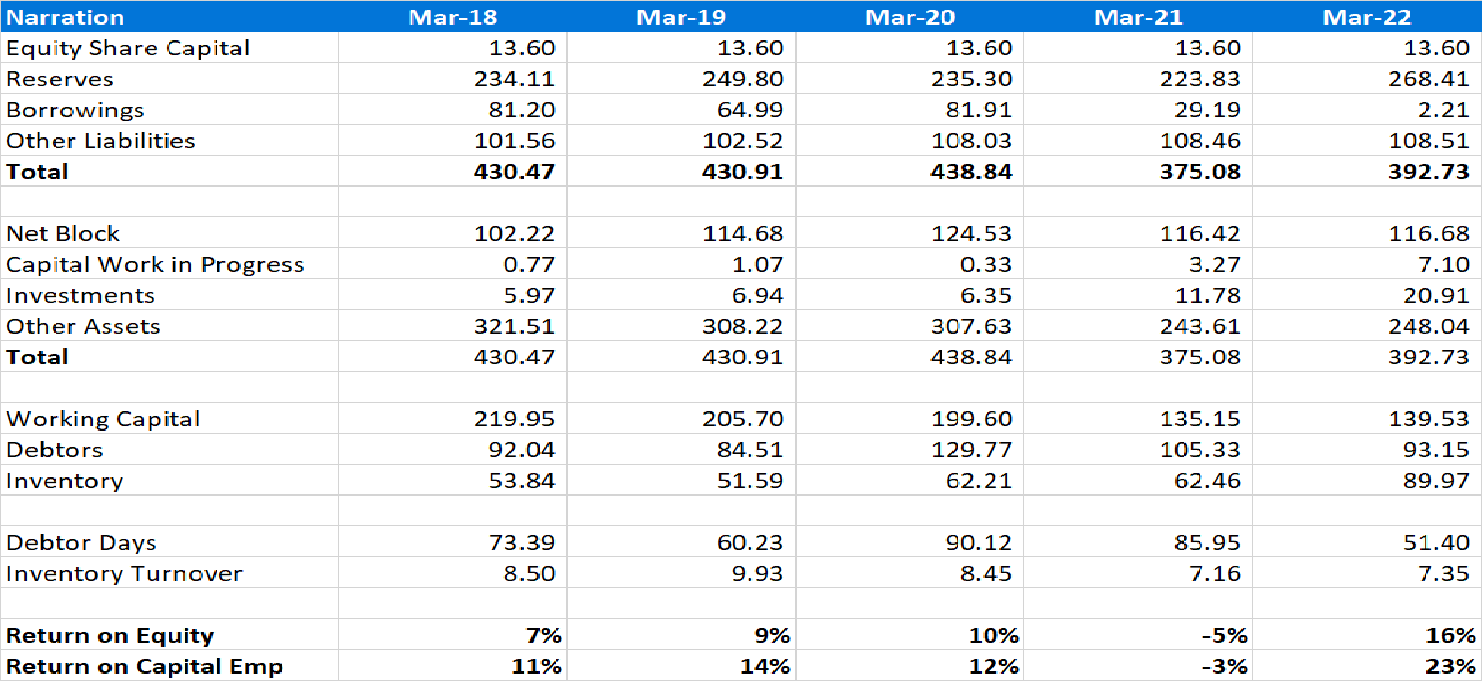

Balance Sheet

Ador Fontech

P&L

Balance Sheet

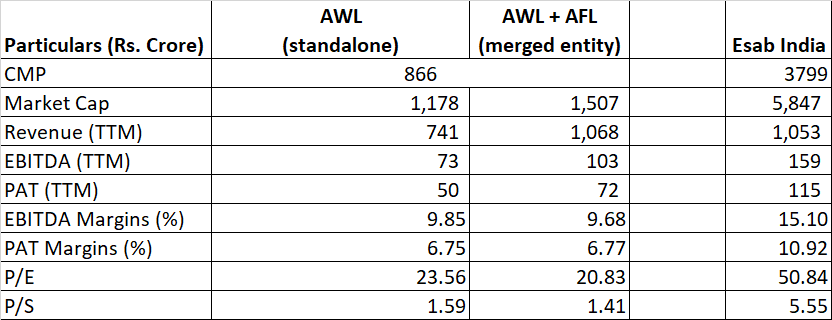

Valuations

AWL has started seeing improvement in margins from Q3FY23 onwards with consumable PBIT margins touching 15% during the quarter. Equipment margins continue to remain subdued primarily due to supply chain issues. Flares and project division has also reported 10% margins in 9MFY23. Management in the Q3FY23 concall seemed pretty confident of maintaining consumable margins and improve equipment margins. FY24 can see decent growth in both consumable and equipment segment while flare division will see execution of ONGC project which should lead to healthy growth in overall topline of the company. Furthermore, margins, even if sustained at Q3FY23 levels, can lead to healthy growth in bottom line during FY24.

There is huge difference in valuations between Esab and Ador (group or Welding) primarily due to higher margins, cash flows, return rations and MNC parentage of Esab. Furthermore, Esab’s parentage gives it advantage in terms of introduction of new age products in Indian markets for the first time. However, Ador’s management is also taking efforts to improve their margins and cash flows. Furthermore, Ador Welding started giving out dividend from FY22 onwards and management has plans to maintain healthy dividend payout of around 30 - 40% of net profits going forward as well.

Key Strengths

-

High ROCE, healthy cash flow generation and dividend payout

-

Consumable business is relatively less impacted by downcycle compared to product/equipment business

-

Capex cycle being in favour leading to higher demand

Key Risks

-

Flares and project engineering business can face challenges like earlier times despite new management being risk averse: Although, the management has become cautious on project engineering business, the new ONGC contract or any large contract can have some challenges like earlier times especially on working capital management as well as margins. The same can impact the performance of the overall company.

-

Headwinds in capex cycle: The capex cycle in India has picked up steam over the past year. Almost a decade 2011 - 2021 saw subdued capex cycle which impacted most of the capital goods companies. Although, unlike product business, consumable business is relatively less impacted by downturn in capex cycle, the overall growth for Ador will be impacted.

-

Margin improvement in the business is not as per expectations: The growth in earnings of the company and playing out of the thesis is not just dependent on topline growth but also on improvement in EBITDA margins of the company. Significant increase in steel prices might impact ability of the company to fully pass on prices to the company and can impact its profitability margins.

(Disclosure: Invested since last 2 years. Please do your own research and due diligence as I am not SEBI registered investment advisor and this post is purely for educational purpose.)