I had attended the AGM of Ador Welding Ltd held on August 9, 2023. Was able to take running notes of the AGM which are presented below:

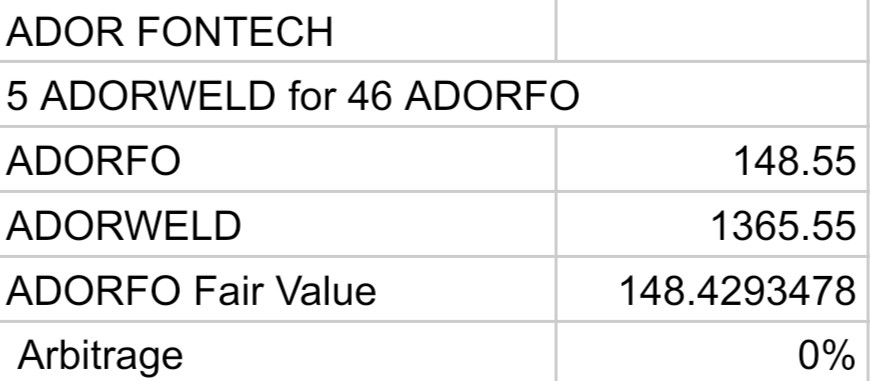

• Merger between Ador Welding Ltd & Ador Fontech Ltd – looking at December 2023 for completion. Advantages of merger? It basically enable consolidation of welding business, synergies between businesses, marketing & R&D strengths, production, supply chain and brand strengthening. All of these, will help in maximizing shareholder value. Access different market segments. Infrastructure and organizational capabilities will come in. Better financial leverage for combined entities. Leadership benefits too. Strengths – 800 – 850 people post merger. Cost savings achievable. Remove duplication. Amalgamation will lead to reduction in legal compliance & regulatory costs.

• RM prices to be passed on and how do we deal with volatility? Steel related prices. Time lag of 6 weeks.

• Don’t have debt at the moment. Not much issues.

• Geopolitical tension? Affects us like it affects others. Not seeing much slow down. Indian companies benefitting and benefitting us as well.

• Growth in next few years? Don’t provide guidance. Look at core sectors, steel sector and IIP nos. Projecting beyond 6 – 12 months is still possible but not beyond that. Outperform the industry and grow is what we are targeting.

• Guidance on Margins? Last year margins are base level of margins we want to maintain. Improve from there step by step.

• Q1 margins impacted due to performance of flare division. How should we look at its margins over near to medium ? When it comes to flare division, better to look at it on annual basis. Look at it on course of the year. Improve over the year compared to last year is what we are targeting.

• Challenges for the company? Liquidity in the markets, infrastructure etc – positive for next 6 – 12 months. Challenges always there – pricing, supply chain, raw material etc. Don’t see any major disruption to that.

• Think our market share is growing. Its growing in right path. Continue to pushing that factor.

• Outstanding work in flares for ONGC? It will continue for this year and get executed.

• BIS issue which led to levy of penalty? Product was imported by industry in large way along with us. Spill over material was there BIS issues objection for that. Unfortunately, hefty penalty. All remedial measures implemented now. Penalties applied earlier were lower. Optimistic we will see fair resolution to these.

• Capacity increase will keep going on. Expect 15% additional capacity to be added over the next 12 months.

• Inorganic opportunity – keep evaluating not defined strategy

• Treasury – keep evaluating it.

• Outlook for Ador International? Good outlook. Added new markets and new people too. They will outperform rest of our divisions.

• Top 2 – 3 segments and products we have? Consumables – depends on carbon steel related. Equipment front? Volume demand decides that. Flares? ONGC orders – different type of flares there.

• Execution timeline for flares ranges from 6 – 20 months. Margins of flare segment will keep seeing improvement for entire financial year.

• Don’t have asset monetisation strategy. Have asset relocation strategy. Identified Chennai as land for sales. Silvasa – adding capacity

• Some property get sold depending on our usage of the location.

• Plant wise capacity utilisation. Utilisation is 60 – 90% depending on the product line.

• RM – steel is critical RM. Lag for price increase as we are intermediary

• EBITDA guidance? EBITDA for last year is the base which we look to build

• Automotive industry? Expected to grow. Our role in fabrication etc will keep going up.

• Electric car? Still remains a small %age of industry. We will play a role in it as well.

• Working capital? As flare division revenue keeps increasing, some working capital will increase. Consumable WC under control. Ador International gets LCs from its customers.

• No write offs in trade receivable.

• JB Advani sells some gas cutting equipment for us and hence some related party transaction between us and group company.

• Going through very large and interesting capex cycle. Need to come out number 1 or 2 welding company in the medium term.

(Disclosure: Invested)