Ab capital recently demerged from Grasim/nuvo . Also it’s subsidiaries listing would me management decision and depend on multiple factors. If that would happen and when would be all speculation and hard to comment on.

What is Ex-ILFS … Thats also an exposure and have to be included in all calculation …

This money if lost (likely) will be absorbed on BOOK of AB CAP.

Maybe you didnt understand clearly. No one is asking NOT to count IL&FS. IL&FS is a known name and the investor presentation clearly states the % exposure to IL&FS (which is 0.45%). Ex-IL&FS is mentioned separately to let investors know the stress from the unknown names.

So that YOU understand clearly, as per the presentation, Gross Stage-3 exposure (as of Q2FY20) is 1.85% (incl IL&FS) and post provisioning, Net Stage-3 exposure is 1.24%.

Trust that replies your query.

2 Likes

Price action, in my opinion, would start only once liquidity issues are sorted out for the NBFC industry per se. Besides, we need to see some concrete evidence of our macro economic situation improving. Only then will sentiments towards the sector improve.

The investor presentation clearly states their exposure to IL&FS, which is 0.46% of their book as of Q2FY20.

What was the GNPA earlier (Q120) in absolute amount and what it is in this quarter.

An increase of almost 50 crore GNPA QoQ …

Also LOAN growth is FLAT … Look at the BOOK …

Don’t pay dividend and also EPS growth has decreased due to equity dilution,

Just it has box of business does not makes it a good business … ROE/ROA / EPS / Dividend etc matters

Also Birla listed it at a share price of 250 and now themselves diluted equity at 100 rupee… I mean themselves brought at 100 Rs …Phew !!!

Anyways this is critical aspect of business … Good side everyone knows

3 Likes

Very true. Company has not extended loan to corporate also some prepayment came hence aum stayed flat or little down.otherway increasing high margin unsecured personal loan. Hence NIM is improving and NNPA too.but most of your observations are true.company has to improve its ratio .probably when health insurance business will be profitable around fy22. Company will get more market attraction.

2 Likes

Money time article:

(BSE Code: 540691) (CMP: Rs.81.45) (FV: Rs.10)

Aditya Birla Capital Ltd (ABCL) belonging to the renowned Aditya Birla group was listed on the bourses in September 2017 at Rs.250/share. It is engaged in housing finance, broking, corporate lending, structured finance, wealth management, private equity as well as life and health insurance businesses. In the lending business, it is one of the largest non-banking financial companies (NBFCs) in India with an AUM (assets under management) of more than Rs.50000 crore. It is among the top 5 asset management companies (AMCs) with total AUM of over Rs.200000 crore as at FY19.

Listed here are some major businesses that ABCL houses, all of which are ripe for a demerger in the next 3 years quite like the way HDFC did with HDFC Standard Life and HDFC AMC business or ICICI Bank did with ICICI Securities, ICICI Prudential Life Insurance, ICICI Lombard General Insurance, etc.

| Name | Business | Potential Demerger Candidate? |

|---|---|---|

| Aditya Birla Finance | NBFC | YES |

| Birla Sun Life Insurance Co. | Life Insurance | |

| Birla Sun Life Asset Management Co. | Asset Management | |

| Aditya Birla Health Insurance | Health Insurance | |

| Aditya Birla Housing Finance | Housing Finance |

Interestingly, the promoters hold ~70.4% stake in ABCL, followed by Azim Premji of Wipro who holds 4.11% stake through his family office and LIC which holds 2.4% stake. Recently, the promoters raised capital from private equity giant Advent International by diluting around 4.14% besides a preferential allotment to the promoter group companies.

ABCL to some extent weathered the IL&FS storm. Its bottom-line is expected to grow at over 25% CAGR over FY20-23, driven by strong traction in its lending and asset management businesses. Being a part of a large and reputed conglomerate with big auditors like Deloitte Haskins & Sells LLP, Price Waterhouse & Co. and BNP & Associates managing its books, ABCL has the advantage of multiple financial relationships and easy access to liquidity compared to its peers. The stock has the potential to touch Rs.150 in the next 6-9 months with very limited downside from the current level.

7 Likes

Appreciate you highlighting the drawbacks, as perceived by you, to the discussion. Here’s my take on your points:

#. Any parameter that i track for companies, i do it on a relative basis and not on an absolute basis. Meaning, i track NPAs as a % of outstanding loans and look at how this ratio is moving. In that context, i, not too -vely surprised by the ratio movement in AB Capital. More so, considering the operating environment we are traversing.

#. While its nice to note that the loan book is flat, a closer look at the book probably hints at conscious strategy that they ‘might’ have taken to de-risk the book. So, a change in the mix, within the loan book, may have caused a flat overall growth. For instance, the retail book has grown by 32%, SME up by 5% & LAS de-grown by 27% YoY.

#. These institutions will always keep requiring growth capital. And if they have been in a position to raise capital, during the toughest phase, i would look at it as a demonstration of their ability in doing so. While this may lead to EPS dilution in the near term, a prudent use of this capital to grow future business with improving margins would again be EPS accretive. Isnt it? Unless your argument is that they have raised capital, diluted EPS now and the deployment of this capital is also going to be EPS dilutive?

#. Needless to mention, parameters like RoE, RoA matter a lot in this industry. And hence, you should compare these metrics for AB Capital, business wise, and compare it with the rest of the industry to see how they fare. Doing so will let you know their competitive positioning.

#. You should know that the direction of a stock price essentially is (and should be) beyond any managements control. So whether a stock lists at 250 and then goes to 500 or 150 is largely dependent on their performance and how investors perceive this performance to be, also keeping in mind the overall sentiments. That the broader markets are in stress over the last 18 months and NBFCs are more in stress over the last 12 months is not rocket science. Given the perceived risk attached to assets of NBFCs, is it surprising that prices of NBFC stocks are beaten down? Im not too sure. Despite this difficult operating environment, they have raised Rs.21 bn (a mix of promoter infusion as well as external investor infusion). Promoters infusing capital along with external investors is a sign of promoter confidence, in MY personal opinion. Mind you, a coin be be looked at in both the sides ![]()

2 Likes

PAT up 37% to 256 crore

Revenue up 8% to 4299 crore

2100 cr raised at 100 per share

Lending book: 60477 crore

NIM: 5.34%

GNPA: 1.39%

Credit Cost: 0.9%

RoE: 15%

AUM: 2.7L crore

Tracking / No investment done.

Aditya Birla Finance has 109 cr exposure to Karvy Group. But fully secured with prime real estate property in Hyderabad

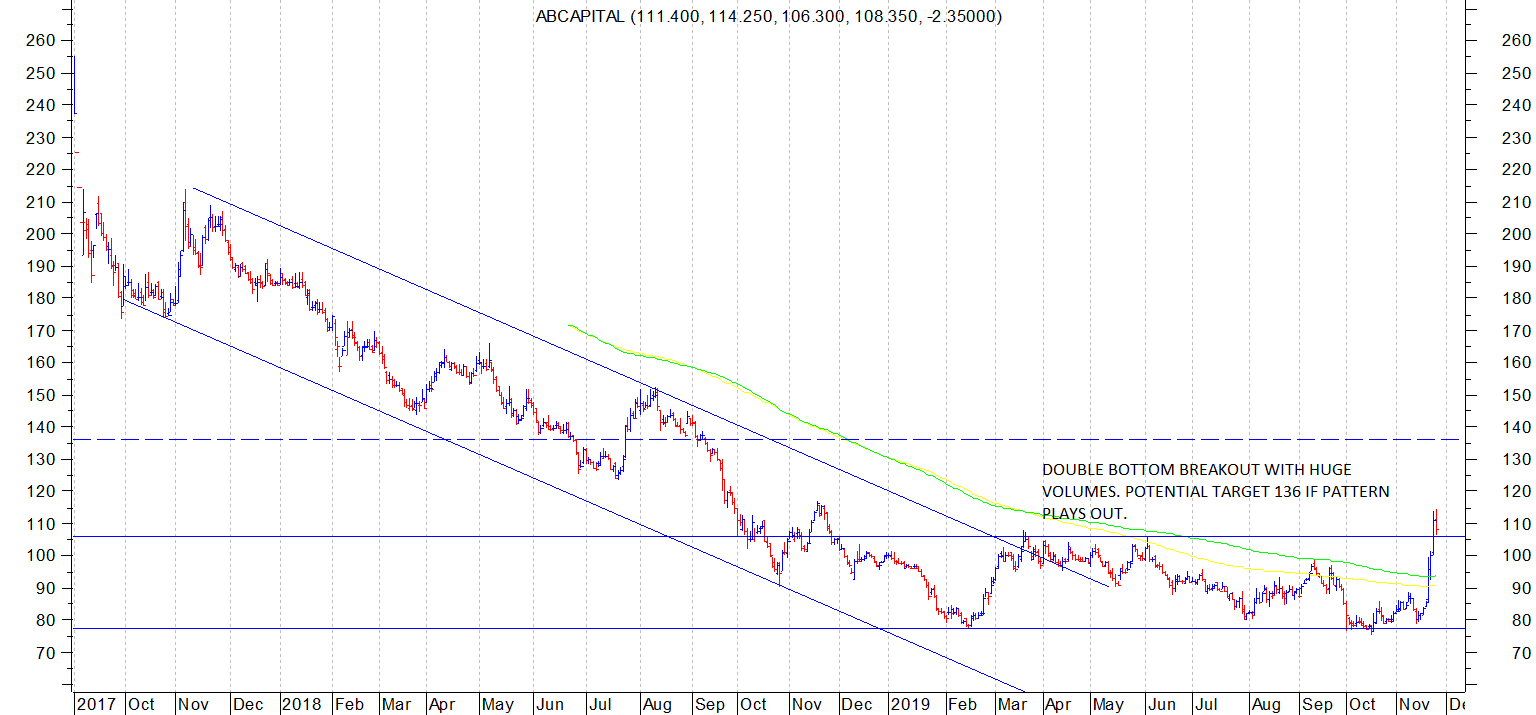

AB CAPITAL has formed an interesting double bottom breakout pattern. Height of double bottom (trough to intervening peak ) is 30. Adding that to 106 (breakout point) provides a potenital target of 136. Two solid horizontal lines enclose the double bottom and dotted line represents potential target.

Sometimes there is a few days of small range sideways moves post these kind of breakouts which provide good entry points.

As of now no positions, only in watchlist.

14 Likes

Any clue on what would be the potential liability on ABCAPITAL incase if IDEA-Vodafone goes bust ?

What’s your view now after serious correction?

Hello,

Any views on the current situation affecting AB capital??the share price is below 50 and seems to be cheap.

Thanks,

Deb

All the strengths that existed previously for AB Cap remain unchanged - diversified earnings streams, low cost of borrowing and strong parentage. They are one of the few financial cos who can come out of this stronger. Back of the envelope valuation suggests there is decent margin of safety at current levels. However they have been a value story for a long time (just see this thread) and yet been consistently punished by the market. Results on 5th June should give more clarity

Recent credit report - https://www.icra.in/Rationale/ShowRationaleReport/?Id=93199

Disc. Invested

3 Likes

Health Insurance business continues good traction towards attaining breakeven. 70% yoy growth in premium income during April-May. They were the fastest growing health insurer last year as well.

AB Capital - Q1 FY21.pdf (5.6 MB)

On the face of it, looks like a decent set of numbers. Topline has grew. Drop in profit is due to “change in valuation of liabilities” in life insurance operations.

Is anyone aware that why there is no price action.

Their insurance segment also seems to be doing quite well.

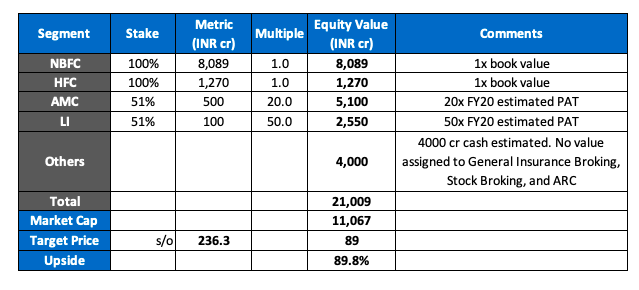

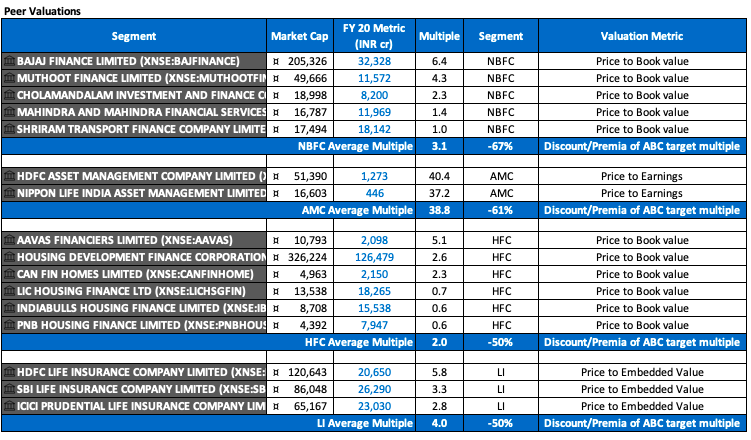

Benchmarking AB Cap valuation to peers:

takeaways:

- On an absolute basis, ABC is trading 20% below what I consider bear market multiples, even after including a 20% holdco discount. We are well out of that period of uncertainty now.

- Many peer financials have already moved from bear market prices of March '20 closer to their historical multiples. While ABC does not deserve the leaders valuation in any segment, fair value imo can be closer to the mean of each segment (e.g. NBFC does not deserve 6x p/b like Bajaj Fin, it also does not deserve 1x p/b like Shriram Transport which is also a AAA rated lender but has one major line of business and 70% of its book under morat vs 28% for ABC.)

- There are many reasons not be invested in financials now and stick to what’s working in the market, but the converse is also true: this is a once in a decade kind of opportunity to get into these names at throwaway prices.

disc. Invested

2 Likes