ABSL AMC

Steadily Gained Market Share to Become No.3 Mutual Fund in India

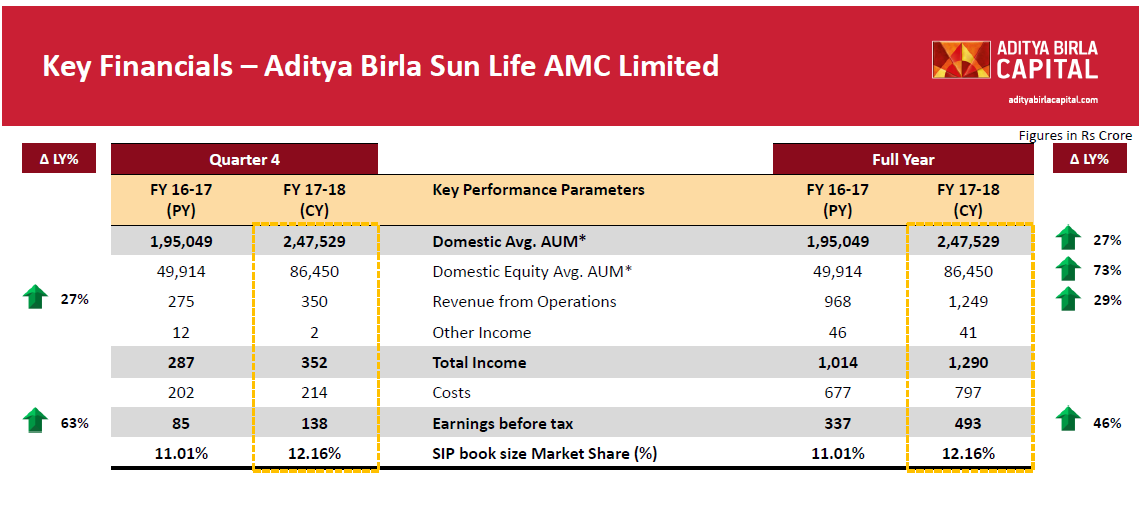

AAUM market share of 10.75%, AUM Size: 267739 crores

Monthly SIP book1 over Rs. 950 crore

Pan-India presence across 226 locations

Other segments like health insurance, broking business and others are currently small but has sizeable addressable market.

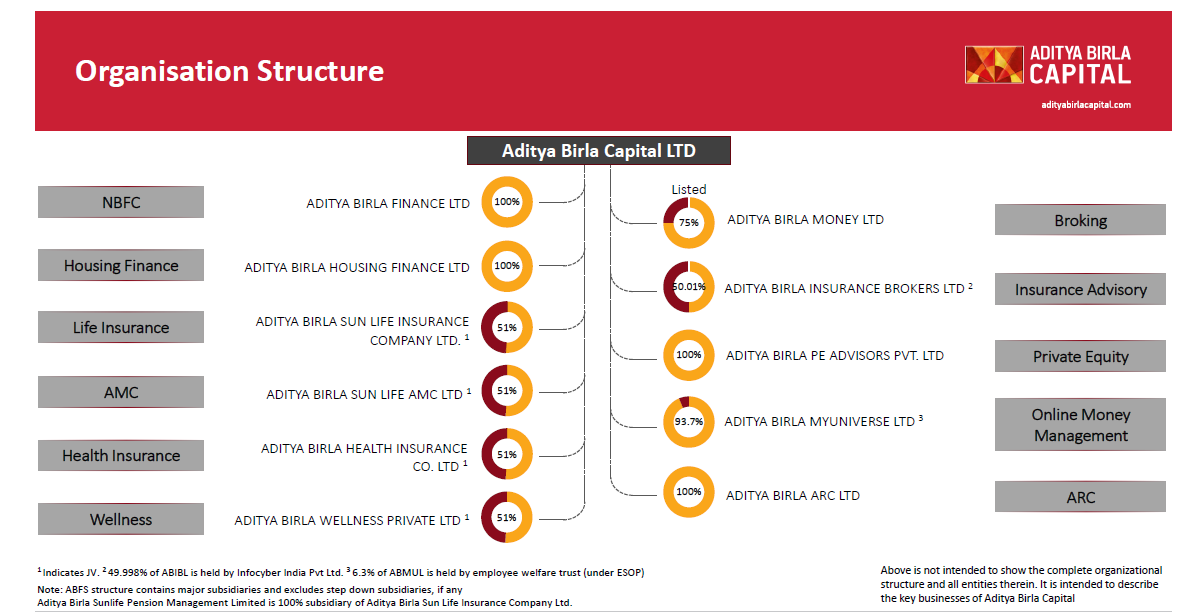

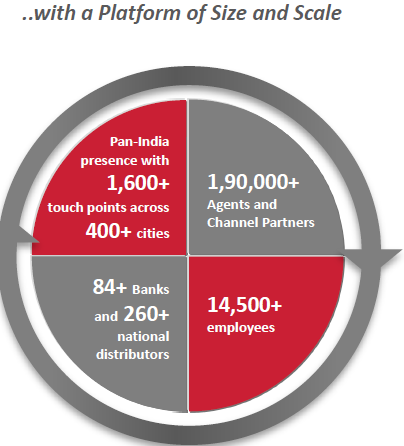

Valuation and Rationale Low Mcap compared to the size of the opportnuity served: The current market cap of the company is around 30K crores. I guess the most comparable peer is Bajaj finserve and bajaj finance which together have market cap of 2 lac crores. However, I am not sure how to combine both and compare them with AB capital. On a rough cut basis i could potentially foresee AB Cap reaching to 1 lac Mcap in next 5-6 years (i.e. more than 3.0x) Good Market Share and Presence in high growth buiness segments: I particularly like this company as it not only caters to under-penetrated segments like Insurance, financial savings and lending but has sizable market share in all three segments, particularly in AMC and Life Insurance business. Broad Reach and Distribution Network;Furthermore, they have wide reach and network with 1600 plus touch points across 400 cities, closed to 2 lac agents and 15k employees. Cross selling of products: High quality management team and corporate governance Sizable investments incurred in last 18-24 months, thereby the benefit of the investments are expected to accrue in the coming years.

Risks

Competitive landscape; There are number of competitors and some of them are well established like ICICI pru, HDFC life in insurance segment while private banks and NBFC in Lending business. I believe since the since the size of the addressable opportunity is very large, it can encompass quite a few players.

High borrowing cost in comparison to CASA established banks: It remains a risk compared to CASA banks but has good presence in capital markets and can issue NCDs and bonds at reasonable price compared to other NBFC. Credit rating on long term debt: (AA+/Stable) by ICRA. AAA rating could further lower thier borrowing costs. Peers like India bulls housing fianance NCDs are rated one notch higher at AAA.

Low profits in some of the businesses which are in nascent stage of operations including losses in the recently launched health insurance business.

I was thinking of valuing each business separately but then I realize my lack of expertise to do that…It would be great if our fellow colleages can throw some more colour on it and their thought process on the entire company.

Really looking forward to the views/opinions of the great minds that we have in this forum.

Aditya Birla group has a very poor record of dealing with minority shareholders, so there is a possibility of getting a valuation discount from the market due to this.

@basumallick sumallick, Sir, thanks for your reply…could you please share some examples. I was unaware of AB poor track record of dealing with minority shareholders.

@Bhavik, Re 1 lac of potential market cap in next 5-6 years, stems from the following reasons;

Predictable overall growth rate of 20%+, which results from leading market share in AMC and Insurance segments and robust growth in lending business. These are highly under-penetrated segments.

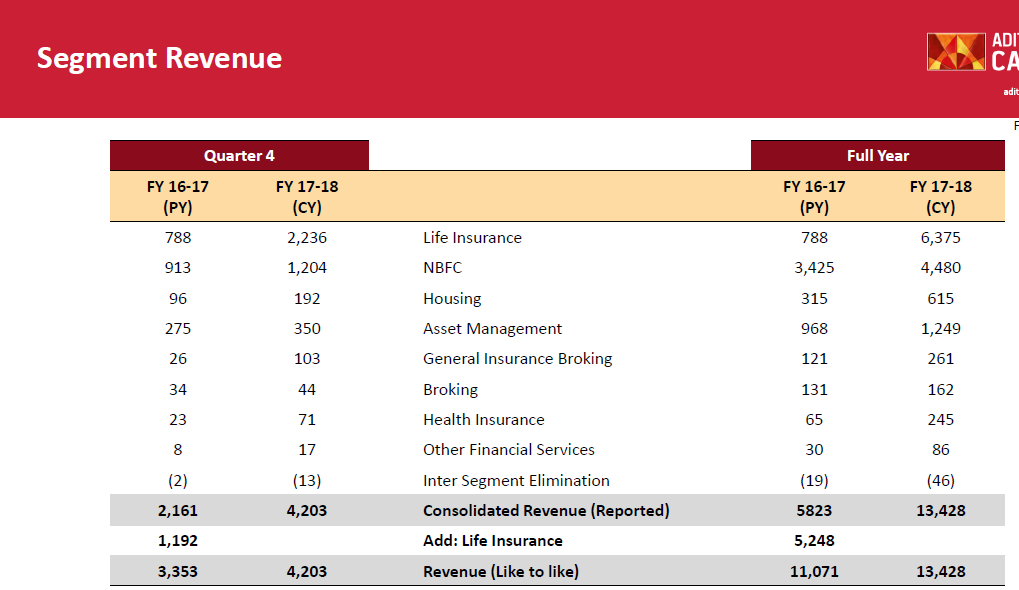

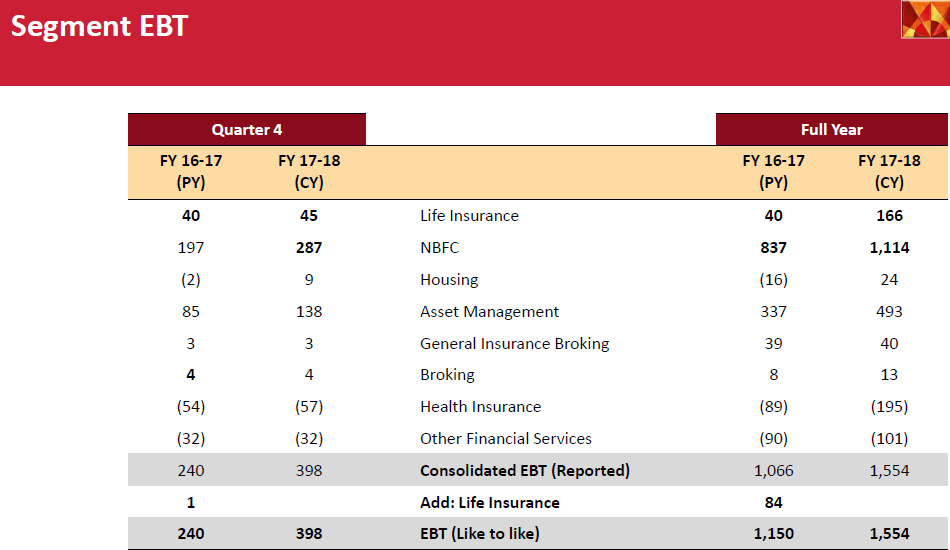

If you put a CAGR of 20% on about 13.5K crore revenue and about 1K crore profit it can treble it’s revenue and profit in next three years and hence the market cap.

Do let me know your thoughts, thanks.

Mr Basu could you please elaborate. I have heard something like that from Anil Shingvi of IIAs, but did not go into detail. If time permits you please do write. It will be interesting to know your views.

Thank you @basumallick for the two links.

It does appear that the minority shareholder has been excluded from key decision making events in the past.

for the AB Nuvo-Grasim merger allegations that the goal was actually to give Idea a helping hand, was that concern proven true subsequently (given that the article is dated almost two years back, & I dont follow the telecom sector much ) ?

As far as the ABNL and Grasim transaction is concerned, one of the key reasons to do the transaction was to get ABFL (NBFC) a credit rating upgrade, with the stronger parentage of Grasim…which has successfully happened and it is now IND AAA, which significantly helps a NBFC. In case of Century and Ultratech, one must look and compare the key matrices of the business acquired with the peers and compare valuations (including recent deals). You will definitely get your answer.

Thanks Guys for bringing that perspective. But is that the only reason why the current valuation is at discount, especially compared to its peers (e.g. L&T Finance, Sundaram finance) which are trading at better valuation. Some of the investments made by AB Capital is yet to bear fruits, for example Health insurance business. It seems that there is significant operating leverage and cross selling benefits to accrue over next few years.

Also, the scaleability of the major verticals, like lending, insurance, AMC is very much feasible.

Overall, the AB group seems to have much better market perception and capable management team to tide the rising boat of financialization of savings.

I am curious to know the impact of the rising cost of capital in the coming months (since the rate cycle has bottomed out clearly).

For every 25 basis rise,is it correct to expect a proportional rise in costs (I.e interest costs)?also it will be interesting to watch whether ABcapital is able to pass on increasing costs to consumers or end up absorbing it…

Yes, certainly it is a risk and like all other NBFC and banks, this company will also pass on the increased cost of borrowings to its customers. CASA franchisee do have some advantage over NBFC in terms of access to low cost borrowings. Nonetheless, there is a huge pie to garner due to under-penetrated retail borrowings and shift of market share from PSU banks to private lenders and NBFCs.

And remember ABC has the advantage of diversified business (with presence in insurance and AMC) to de-risk it’s business, which only a few others have.

KM Birla has denied categorically that money will be put in idea in interview on cnbc after this concern was raised. But 2 concern that I understood-

In past many years promoter has issued preferential share to raise their stake which has diluted minority shareholder. Eqitymaster and moneylife raises serious question about corporate governence issues surrounding whole group that they are not worried about minority shareholders.

So as of now the only negatives and supposedly a big one is -“overlooking the minority shareholders”

Any other negatives/positives people can think of?.

ABCL was de-merged from the Grasim Industries last year. I am not exact sure if the Grasim shares benefitted from the spin-off. On its own, ABCL is a an interesting , one shop stop for almost all financial products. Is is displaying early signs of gaining grounds on back of marketing and brand building. It will be good to watch how it performs on next few quarters. I am not sure how to wrestle around the minority shareholder issues of Birla group in past.

Interesting read on the company when it got listed.

What has happened since listing, that the marketcap has come down by 20K crore which is about 40% and earnings in the recent quarter has been quite stupendous.